Global Urethral Discharge Syndrome Market

Market Size in USD Million

USD

500.05 Million

USD

684.35 Million

2024

2032

USD

500.05 Million

USD

684.35 Million

2024

2032

| 2025 - 2032 | |

| USD 500.05 Million | |

| USD 684.35 Million | |

| % | |

|

Urethral Discharge Syndrome Market Size

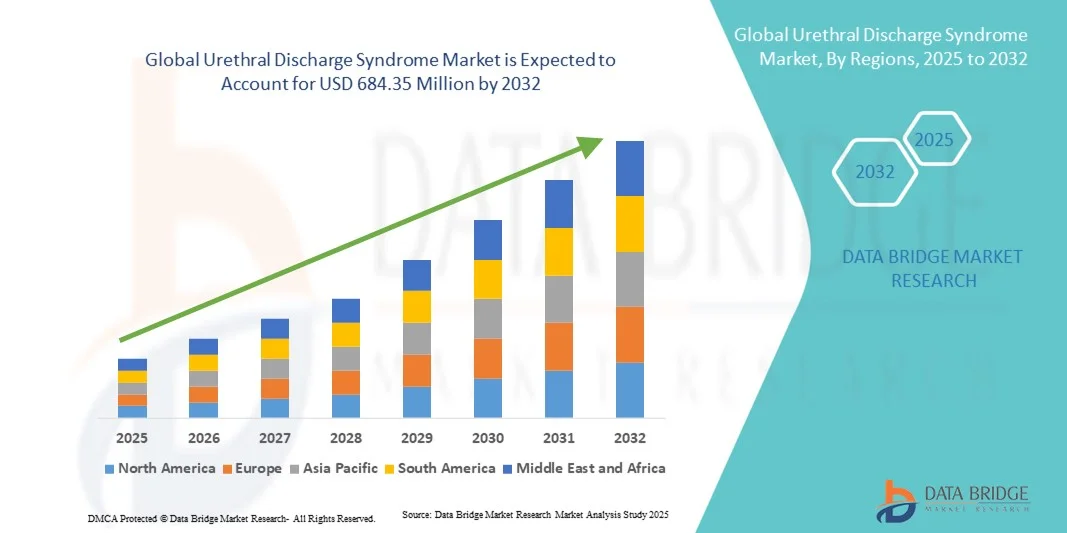

- The global urethral discharge syndrome market size was valued at USD 500.05 million in 2024 and is expected to reach USD 684.35 million by 2032, at a CAGR of 4.00% during the forecast period

- The market's expansion is primarily driven by the increasing prevalence of urological disorders such as benign prostate hyperplasia (BPH), urinary tract infections (UTIs), urinary incontinence, prostate cancer, and end-stage renal disease. In addition, advancements in medical technology, improved hospital infrastructure, and heightened awareness regarding urological health are contributing to the market's growth

- The demand for secure, user-friendly, and integrated solutions for diagnosing and treating urethral discharge syndrome is establishing these medical interventions as the modern approach to urological health. These converging factors are accelerating the uptake of urethral discharge syndrome treatments, thereby significantly boosting the industry's growth

Urethral Discharge Syndrome Market Analysis

- Urethral discharge syndrome (UDS), including conditions such as spontaneous urethral discharge, burning with urination, mucoid exudate with urethral stripping, and more than 5 WBC per high-power field of urethral exudate, is increasingly recognized as a critical healthcare concern due to rising prevalence, improved diagnostic capabilities, and growing awareness of urological and sexual health

- The escalating demand for UDS diagnosis and treatment is primarily fueled by infections caused by pathogens such as Neisseria gonorrhoeae and Chlamydia trachomatis, the prevalence of gonococcal and nongonococcal urethritis, advancements in medical technology, and the increasing use of combination therapies such as azithromycin plus ceftriaxone and doxycycline plus cefixime for effective management

- North America dominated the urethral discharge syndrome market with the largest revenue share of 38.9% in 2024, characterized by advanced healthcare infrastructure, strong presence of key pharmaceutical and diagnostic players, high adoption of diagnostic centers and hospitals, and government initiatives promoting sexual and urological health, with the U.S. experiencing substantial growth in treatment adoption and rapid diagnostic testing

- Asia-Pacific is expected to be the fastest-growing region in the urethral discharge syndrome market during the forecast period due to increasing urbanization, rising disposable incomes, expanding access to diagnostic centers, hospitals, and clinics, and growing awareness regarding sexual health management

- Male patients dominated the urethral discharge syndrome market with a higher share of 60.5% in 2024, while diagnostic centers and hospitals led end-user adoption due to the rising use of advanced diagnostic tools, widespread awareness programs, and accessibility of combination antibiotic therapies

Report Scope and Urethral Discharge Syndrome Market Segmentation

|

Attributes |

Urethral Discharge Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Urethral Discharge Syndrome Market Trends

Advancements in Rapid Diagnostics and Point-of-Care Testing

- A significant and accelerating trend in the global UDS market is the adoption of rapid diagnostic tests and point-of-care (POC) solutions that enable early detection of urethral infections and sexually transmitted pathogens, significantly improving patient outcomes

- For instance, the GeneXpert CT/NG assay integrates POC testing for Chlamydia trachomatis and Neisseria gonorrhoeae, allowing clinics to provide results within hours and initiate timely treatment for infected patients

- Rapid diagnostics allow healthcare providers to reduce misdiagnosis and overtreatment by distinguishing between gonococcal and nongonococcal urethritis, optimizing antibiotic usage and improving care efficiency

- The integration of rapid testing into diagnostic workflows facilitates better patient management, as healthcare providers can monitor infection patterns and implement targeted therapies more effectively across clinics and hospitals

- This trend toward more accurate, faster, and patient-centric diagnostic approaches is fundamentally reshaping expectations for urethral infection management, with companies such as Cepheid developing AI-assisted POC devices that enhance testing speed and reliability

- The demand for rapid, accurate, and easy-to-use diagnostic tests is growing rapidly across both public health and private healthcare sectors, as early detection and treatment become key priorities in managing UDS prevalence

Urethral Discharge Syndrome Market Dynamics

Driver

Rising Incidence of Urethral Infections and STI Awareness

- The increasing prevalence of urethral infections and sexually transmitted diseases, coupled with heightened public awareness about sexual health, is a significant driver for the growing demand for UDS diagnostics and treatment

- For instance, in 2024, several clinics reported adoption of combination antibiotic therapies such as azithromycin plus ceftriaxone, aiming to address rising rates of gonococcal infections efficiently

- As patients become more informed about infection risks and complications, healthcare providers are adopting faster diagnostic methods and effective treatments to reduce disease burden

- Furthermore, government and NGO-led awareness programs promoting STI testing and sexual health checkups are making UDS diagnosis an integral part of routine healthcare in several regions

- Integration of advanced diagnostics with hospital information systems (HIS) is enabling faster reporting, tracking, and management of UDS cases, driving adoption in large healthcare networks

- Pharmaceutical companies investing in next-generation antibiotic therapies to combat emerging resistant strains are creating opportunities for expanded treatment adoption and revenue growth

- The availability of combination antibiotic regimens, improved hospital and clinic infrastructure, and growing sexual health awareness are key factors propelling market adoption in both emerging and developed markets

Restraint/Challenge

Antibiotic Resistance and Regulatory Compliance Hurdles

- The rising occurrence of antibiotic resistance among Neisseria gonorrhoeae and Chlamydia trachomatis strains poses a significant challenge to treatment efficacy, limiting the effectiveness of standard therapies

- For instance, resistant strains have led to treatment failures with commonly prescribed azithromycin plus ceftriaxone combinations, raising concerns among clinicians and patients asuch as

- Addressing resistance through development of new antibiotics, updated treatment guidelines, and antimicrobial stewardship programs is crucial for improving clinical outcomes and patient safety

- Furthermore, stringent regulatory requirements for new diagnostic kits and therapies can delay product launches and increase compliance costs, particularly in North America and Europe

- Variability in diagnostic standards and laboratory capabilities across regions can create inconsistencies in test accuracy and treatment decisions, restricting broader adoption

- The social stigma associated with sexually transmitted infections can reduce patient willingness to seek timely diagnosis and treatment, presenting an additional challenge to market growth

- While awareness is improving, limited access to diagnostic centers and high treatment costs in developing regions can hinder timely diagnosis and therapy, slowing overall market growth

Urethral Discharge Syndrome Market Scope

The market is segmented on the basis of type, causes, treatment, sex, and end-users.

- By Type

On the basis of type, the global urethral discharge syndrome market is segmented into spontaneous urethral discharge, burning with urination, mucoid exudate with urethral stripping, and more than 5 WBC per high-power field of urethral exudate. The spontaneous urethral discharge segment dominated the market with the largest revenue share of 35% in 2024, driven by its high prevalence among affected populations and its straightforward detection in clinical settings. Patients with spontaneous urethral discharge often seek immediate medical attention, leading to higher diagnostic and treatment adoption. Clinics and hospitals prefer this segment due to its clearly defined clinical presentation and ease of treatment tracking. The segment also benefits from well-established treatment protocols and widespread awareness campaigns emphasizing early detection. Furthermore, combination antibiotic therapies targeting spontaneous discharge are highly effective, reinforcing market dominance.

The “more than 5 WBC per high-power field of urethral exudate” segment is expected to witness the fastest growth rate of 8.1% from 2025 to 2032, driven by increasing adoption of laboratory-based diagnostic tests and microscopy for accurate disease detection. This subsegment enables precise differentiation between bacterial infections and inflammatory conditions, enhancing clinical decision-making. Hospitals and diagnostic centers are increasingly relying on WBC-based detection for early-stage infections, improving treatment outcomes. Rising awareness among clinicians about advanced diagnostic markers contributes to adoption. The availability of rapid testing kits for WBC quantification further accelerates market growth. Its adoption in epidemiological studies and public health programs is also expanding.

- By Causes

On the basis of causes, the global urethral discharge syndrome market is segmented into Gonorrhoeae, C. trachomatis, gonococcal urethritis, and nongonococcal urethritis (NGU). The gonococcal urethritis segment dominated the market with the largest share of 40% in 2024, owing to the high global prevalence of Neisseria gonorrhoeae infections and rising awareness of gonorrhea-related complications. Patients often seek rapid treatment due to symptomatic discharge and associated discomfort, increasing therapy adoption. Diagnostic labs prioritize gonococcal testing due to its clear clinical guidelines and mandatory reporting in many countries. The segment benefits from well-established combination therapies such as azithromycin plus ceftriaxone. Public health initiatives for STI screening further boost this segment. Hospitals and clinics actively participate in surveillance programs targeting gonococcal infections, reinforcing its market dominance.

The C. trachomatis segment is expected to witness the fastest CAGR of 9.2% from 2025 to 2032, driven by increasing screening programs and improved POC diagnostics for chlamydia. Asymptomatic cases often remain undetected, creating a growing need for proactive testing. Rapid diagnostics and telemedicine consultations for C. trachomatis are expanding, particularly in developed regions. Public health awareness campaigns promoting regular STI testing drive early detection and treatment adoption. The introduction of advanced NAAT (nucleic acid amplification tests) kits supports faster diagnosis. Rising prevalence in sexually active populations globally fuels market expansion.

- By Treatment

On the basis of treatment, the global urethral discharge syndrome market is segmented into azithromycin plus ceftriaxone and doxycycline plus cefixime. The azithromycin plus ceftriaxone segment dominated the market with the largest share of 50% in 2024, owing to its high efficacy against gonococcal infections and widespread inclusion in treatment guidelines. Hospitals and clinics prefer this combination due to its proven clinical outcomes and reduced treatment failures. The regimen’s rapid symptom relief encourages patient adherence. Regulatory approvals in multiple regions facilitate easier prescription. Public health programs promoting combination therapy further strengthen market dominance. High availability and distribution networks of both drugs enhance adoption in both urban and rural healthcare centers.

The doxycycline plus cefixime segment is expected to witness the fastest growth rate of 7.5% from 2025 to 2032, driven by increasing usage for treating nongonococcal urethritis and chlamydial infections. This subsegment benefits from strong clinical acceptance due to efficacy in asymptomatic cases. Hospitals and diagnostic centers prefer doxycycline-based regimens for mild infections and patients with penicillin allergies. Rising awareness of treatment alternatives and antimicrobial stewardship programs fuel adoption. Telemedicine and online pharmacies are supporting greater patient access. Its inclusion in combination therapy protocols enhances treatment coverage globally.

- By Sex

On the basis of sex, the global urethral discharge syndrome market is segmented into male and female. The male segment dominated the market with the largest share of 60.5% in 2024, due to higher prevalence of symptomatic urethral infections and more frequent clinical visits for diagnosis and treatment. Men often exhibit clear discharge symptoms, prompting early intervention and higher therapy adoption. Diagnostic centers see higher male patient throughput, increasing testing volume. Hospitals prefer standard treatment protocols for male patients due to predictable symptomatology. Awareness campaigns targeting male sexual health further reinforce this segment.

The female segment is expected to witness the fastest CAGR of 8.0% from 2025 to 2032, driven by increasing screening programs for asymptomatic infections and rising healthcare access among women. Early detection through POC diagnostics and routine checkups is becoming more common. Rising awareness of long-term reproductive health complications drives higher testing and treatment adoption. Telemedicine platforms provide convenient consultation options for female patients. Public health initiatives focus on reducing undiagnosed cases, contributing to rapid growth.

- By End-Users

On the basis of end-users, the global urethral discharge syndrome market is segmented into diagnostic centers, hospitals, clinics, and others. Hospitals dominated the market with the largest share of 45% in 2024, driven by high patient volumes, availability of trained staff, and advanced diagnostic and treatment facilities. Hospitals often implement combination therapy protocols and maintain infection control programs, increasing therapy adoption. The presence of multidisciplinary urology and STI care departments strengthens hospital dominance. Diagnostic labs within hospitals enable rapid testing and monitoring. Public health collaborations further enhance market share. Hospitals are also focal points for epidemiological studies, increasing their centrality in the market.

The diagnostic centers segment is expected to witness the fastest CAGR of 9.5% from 2025 to 2032, fueled by increasing adoption of rapid testing, point-of-care devices, and laboratory-based detection methods. Diagnostic centers provide convenience for early detection and monitoring of asymptomatic cases. Growth is supported by mobile and private lab services offering home collection. Rising awareness among patients about confidential and quick testing promotes adoption. Technological advancements in NAAT kits and immunoassays accelerate growth. Partnerships with clinics and hospitals enhance diagnostic center outreach and patient volume.

Urethral Discharge Syndrome Market Regional Analysis

- North America dominated the global urethral discharge syndrome market with the largest revenue share of 38.9% in 2024, characterized by advanced healthcare infrastructure, strong presence of key pharmaceutical and diagnostic players, high adoption of diagnostic centers and hospitals, and government initiatives promoting sexual and urological health

- Patients and healthcare providers in the region highly value early diagnosis, effective combination therapies such as azithromycin plus ceftriaxone, and advanced diagnostic tools such as nucleic acid amplification tests (NAATs) for accurate detection of gonococcal and nongonococcal urethritis

- This widespread adoption is further supported by robust public health programs, easy access to diagnostic centers and hospitals, and increasing sexual health awareness campaigns, establishing UDS testing and treatment as a critical component of regional healthcare services

U.S. Urethral Discharge Syndrome Market Insight

The U.S. urethral discharge syndrome market captured the largest revenue share of 82% in 2024 within North America, fueled by increasing prevalence of urethral infections and high awareness of sexual and urological health. Patients are prioritizing early diagnosis through rapid diagnostic tests and combination antibiotic therapies such as azithromycin plus ceftriaxone. The growing adoption of point-of-care testing and telemedicine platforms further propels the market. Moreover, robust public health initiatives and STI screening programs, combined with access to advanced hospitals and diagnostic centers, are significantly contributing to the market's expansion.

Europe Urethral Discharge Syndrome Market Insight

The Europe urethral discharge syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent health regulations and the rising need for effective STI management in hospitals and clinics. The increase in urbanization and awareness campaigns, coupled with adoption of rapid diagnostic technologies, is fostering market growth. European patients are increasingly seeking convenient and accurate testing and treatment solutions. The market is experiencing notable growth across private and public healthcare facilities, with UDS diagnosis and treatment being incorporated into routine sexual health checkups and epidemiological programs.

U.K. Urethral Discharge Syndrome Market Insight

The U.K. urethral discharge syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by heightened awareness of urethral infections and a desire for timely diagnosis and treatment. In addition, concerns about complications from untreated STIs are encouraging both patients and healthcare providers to adopt rapid testing and combination therapies. The U.K.’s well-established healthcare infrastructure, along with accessible diagnostic centers and strong public health campaigns, is expected to continue stimulating market growth. The increasing adoption of telemedicine consultations and home-based testing kits further supports market expansion.

Germany Urethral Discharge Syndrome Market Insight

The Germany urethral discharge syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of STIs and demand for advanced diagnostic and therapeutic solutions. Germany’s well-developed healthcare infrastructure, emphasis on research, and availability of point-of-care diagnostics promote the adoption of UDS testing and treatment. Patients and clinics are increasingly integrating laboratory-based testing for precise detection of gonococcal and nongonococcal urethritis. Public health initiatives and combination therapy programs further drive market growth, particularly in urban regions.

Asia-Pacific Urethral Discharge Syndrome Market Insight

The Asia-Pacific urethral discharge syndrome market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing prevalence of urethral infections, expanding healthcare infrastructure, and rising awareness of sexual health in countries such as China, Japan, and India. The region's growing focus on STI prevention programs and point-of-care diagnostics is driving market adoption. Furthermore, improving affordability and accessibility of rapid diagnostic tests and combination therapies are expanding the patient base. Telemedicine platforms and government initiatives for sexual health awareness further enhance market growth.

Japan Urethral Discharge Syndrome Market Insight

The Japan urethral discharge syndrome market is gaining momentum due to the country’s high healthcare standards, urbanization, and emphasis on preventative sexual health. Adoption of rapid diagnostics and combination antibiotic therapies is increasing, particularly in hospitals and diagnostic centers. The integration of telemedicine for STI consultation and follow-up care is fueling growth. Japan’s aging population is also driving demand for easier-to-use and accurate diagnostic solutions. Public health programs and clinical awareness campaigns further contribute to market expansion in both residential and commercial healthcare settings.

India Urethral Discharge Syndrome Market Insight

The India urethral discharge syndrome market accounted for the largest revenue share in Asia Pacific in 2024, attributed to the country’s growing population, rising awareness of STIs, and expanding healthcare access. India represents one of the largest markets for rapid diagnostics and combination antibiotic therapies. Patients increasingly prefer quick and accurate diagnosis at diagnostic centers and clinics. Government initiatives for sexual health awareness, expansion of point-of-care testing, and affordability of treatment options are key factors propelling the market. Strong domestic manufacturing of diagnostic kits and combination drugs further supports market growth.

Urethral Discharge Syndrome Market Share

The urethral discharge syndrome industry is primarily led by well-established companies, including:

- BD (U.S.)

- Boston Scientific Corporation (U.S.)

- Cardinal Health (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Medtronic (Ireland)

- Siemens Healthineers AG (Germany)

- Olympus Corporation (Japan)

- Coloplast Corp. (Denmark)

- Stryker (U.S.)

- Fresenius Medical Care AG & Co. KGaA (Germany)

- Baxter (U.S.)

- Richard Wolf GmbH (Germany)

- KARL STORZ SE & Co. KG (Germany)

- Endo Pharmaceuticals Inc. (U.S.)

- HealthTronics Inc. (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Cook Medical (U.S.)

- General Electric Company (U.S.)

- American Medical Systems (U.S.)

What are the Recent Developments in Global Urethral Discharge Syndrome Market?

- In August 2025, Iterum Therapeutics announced the U.S. commercial launch of a new oral antibiotic designed for uncomplicated urinary tract infections (uUTIs). Given the overlap between uUTIs and urethral discharge syndrome, this launch provides additional treatment options for patients presenting with UDS symptoms

- In August 2025, the FDA granted priority review to a supplemental new drug application (sNDA) for gepotidacin (Blujepa) as an oral treatment for uncomplicated urogenital gonorrhea in patients aged 12 years and older. This development underscores the growing recognition of gepotidacin as a key therapeutic option for managing gonococcal infections related to UDS

- In April 2025, the World Health Organization (WHO) released a comprehensive global reporting framework for sexually transmitted infections (STIs), including urethral discharge syndrome. This initiative aims to standardize data collection across member states, enhancing surveillance and response strategies for STIs such as gonorrhea and chlamydia

- In March 2025, the U.S. Food and Drug Administration (FDA) approved gepotidacin (Blujepa) for the treatment of uncomplicated urogenital gonorrhea in female adults and adolescents. This oral antibiotic represents a significant advancement in STI treatment, offering a new option for managing gonococcal infections associated with UDS

- In January 2025, Germany updated its evidence-based guidelines for managing urethritis, emphasizing the use of ceftriaxone for suspected gonococcal urethritis. The guidelines also stress the importance of dual therapy to address co-infections with Chlamydia trachomatis, reflecting the evolving understanding of STI treatment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.