Global Uro Gynecological Surgical Devices Market

Market Size in USD Billion

USD

28.84 Billion

USD

52.52 Billion

2024

2032

USD

28.84 Billion

USD

52.52 Billion

2024

2032

| 2025 - 2032 | |

| USD 28.84 Billion | |

| USD 52.52 Billion | |

| % | |

|

Uro-Gynecological Surgical Devices Market Size

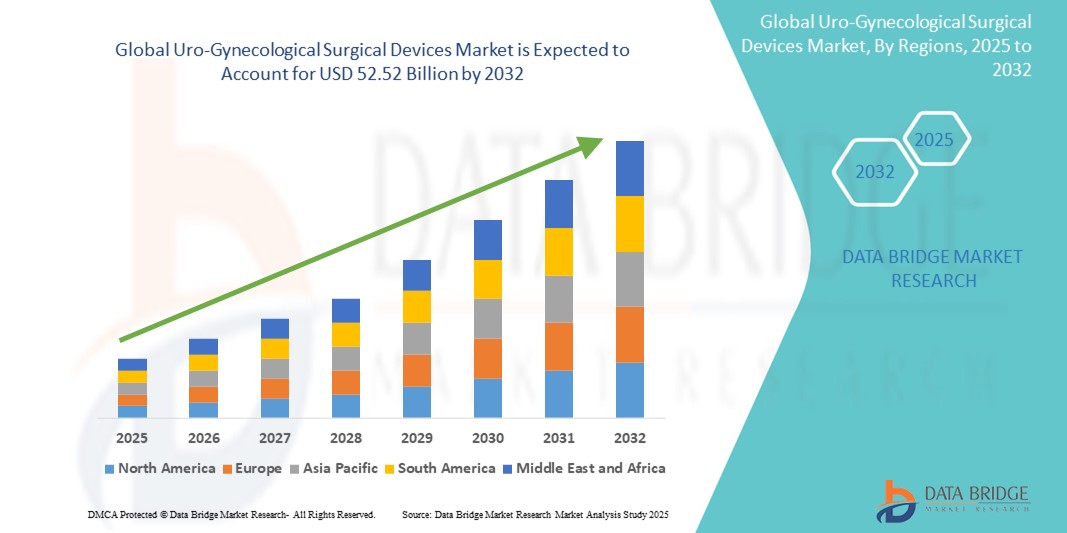

- The global uro-gynecological surgical devices market size was valued at USD 28.84 billion in 2024 and is expected to reach USD 52.52 billion by 2032, at a CAGR of 7.78% during the forecast period

- The market growth is primarily driven by the increasing prevalence of pelvic floor disorders, rising awareness of women’s health, and advancements in minimally invasive surgical techniques that offer improved patient outcomes and reduced recovery time

- In addition, the growing geriatric female population and rising demand for effective treatment options for conditions such as urinary incontinence and pelvic organ prolapse are contributing to market expansion. These factors collectively position uro-gynecological surgical devices as essential tools in modern gynecologic care, thereby propelling industry growth

Uro-Gynecological Surgical Devices Market Analysis

- Uro-gynecological surgical devices, designed for the diagnosis and treatment of pelvic floor disorders, urinary incontinence, and pelvic organ prolapse, are critical tools in women’s health and minimally invasive gynecologic surgery, used extensively in both hospitals and ambulatory surgical centers for their precision and patient recovery benefits

- The growing demand for these devices is primarily driven by the increasing global incidence of uro-gynecological conditions, greater awareness of available treatment options, and technological advancements such as robotic-assisted surgery and enhanced mesh materials

- North America dominated the uro-gynecological surgical devices market with the largest revenue share of 39.2% in 2024, supported by a well-established healthcare infrastructure, early adoption of advanced surgical techniques, and strong presence of leading medical device manufacturers, particularly in the U.S. where procedural volumes remain high

- Asia-Pacific is expected to be the fastest growing region during the forecast period due to rising healthcare investments, growing awareness of women’s health issues, and increasing access to surgical care in emerging economies

- Urological surgical devices segment dominates the uro-gynecological surgical devices market with a market share of 46.8% in 2024, driven by its widespread application in treating urinary incontinence and pelvic organ prolapse, along with continuous advancements in minimally invasive surgical tool

Report Scope and Uro-Gynecological Surgical Devices Market Segmentation

|

Attributes |

Uro-Gynecological Surgical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Uro-Gynecological Surgical Devices Market Trends

“Technological Advancements in Minimally Invasive and Robotic-Assisted Procedures”

- A significant and accelerating trend in the global uro-gynecological surgical devices market is the advancement of minimally invasive and robotic-assisted surgical technologies, which are transforming the landscape of pelvic floor disorder treatments by improving precision, reducing patient recovery times, and minimizing surgical complications

- For instance, Intuitive Surgical’s da Vinci system is increasingly utilized in uro-gynecological surgeries, offering enhanced dexterity and 3D visualization for complex procedures. Similarly, Olympus and Stryker continue to innovate with advanced endoscopic tools specifically designed for gynecologic applications

- Robotic and laparoscopic systems allow for more accurate procedures in treating conditions such as pelvic organ prolapse and urinary incontinence, while also supporting outpatient and ambulatory surgical settings. Manufacturers are introducing integrated platforms that combine visualization, diagnostics, and surgical intervention capabilities

- Furthermore, developments in surgical mesh materials with improved biocompatibility and reduced complication risks are gaining traction. These innovations support safer and more effective pelvic floor repairs

- The integration of these advanced technologies into routine gynecological practices enhances surgical outcomes and patient satisfaction. The adoption is further encouraged by the global trend towards outpatient procedures, increased healthcare efficiency, and evolving reimbursement models

- This trend towards precision-driven, minimally invasive uro-gynecological interventions is redefining clinical standards, with companies such as Medtronic, CooperSurgical, and Karl Storz leading the development of next-generation surgical tools tailored to these procedures

Uro-Gynecological Surgical Devices Market Dynamics

Driver

“Rising Prevalence of Pelvic Floor Disorders and Growing Geriatric Population”

- The increasing global prevalence of pelvic floor disorders, particularly urinary incontinence and pelvic organ prolapse among aging women, is a key driver for the uro-gynecological surgical devices market

- For instance, data from the World Health Organization highlights a steady rise in the geriatric female population, a demographic disproportionately affected by uro-gynecologic conditions, thereby increasing the need for surgical intervention

- In addition, rising awareness about women’s health, improved access to healthcare, and the availability of minimally invasive surgical treatments are encouraging more patients to seek timely care

- Reimbursement support for gynecological surgeries and broader acceptance of surgical solutions among healthcare providers are further contributing to the increasing demand for specialized uro-gynecological devices

- This rising clinical need, combined with demographic trends and healthcare infrastructure improvements, is positioning uro-gynecological surgical tools as essential components in women’s health services across the globe

Restraint/Challenge

“Regulatory Scrutiny and Litigation Over Surgical Mesh Implants”

- Regulatory and legal challenges, particularly involving transvaginal mesh implants, represent a major restraint to the uro-gynecological surgical devices market, affecting both manufacturer operations and end-user confidence

- For instance, past safety concerns and litigation in the U.S. and Europe have resulted in recalls and heightened regulatory scrutiny, with agencies such as the FDA enforcing stricter guidelines for the approval and marketing of pelvic mesh devices

- These legal developments have led to reputational challenges for several companies, as well as increased demand for transparent clinical data and long-term safety evidence for implantable devices

- In addition, the cost and complexity associated with regulatory compliance and post-market surveillance increase entry barriers for emerging players and slow down innovation in certain high-risk product categories

- To overcome these challenges, companies are focusing on developing safer non-mesh alternatives, investing in robust clinical validation, and improving surgeon education to ensure appropriate use and patient safety, which will be essential for regaining trust and sustaining market growth

Uro-Gynecological Surgical Devices Market Scope

The market is segmented on the basis of product type, disease-specific surgeries, and procedure.

- By Product Type

On the basis of product type, the uro-gynecological surgical devices market is segmented into urological surgical devices, trocars, and endoscopes. The urological surgical devices segment dominated the market with the largest market revenue share of 46.8% in 2024, driven by its extensive use in treating urinary incontinence and pelvic organ prolapse. These devices are widely utilized due to their effectiveness, ongoing technological improvements in minimally invasive solutions, and growing surgical volumes in both hospitals and ambulatory surgical centers. Increasing patient preference for less invasive interventions and faster recovery times further supports the demand for urological surgical tools.

The endoscopes segment is anticipated to witness the fastest growth rate from 2025 to 2032, propelled by advancements in visualization technologies and rising demand for diagnostic and operative hysteroscopy procedures. Enhanced imaging quality, ease of insertion, and integration with advanced surgical platforms make endoscopes a vital tool for precision gynecologic interventions.

- By Disease Specific Surgeries

On the basis of disease-specific surgeries, the uro-gynecological surgical devices market is segmented into pelvic organ prolapse, urinary incontinence, and others. The urinary incontinence segment led the market with the highest revenue share of 48.7% in 2024, owing to the high prevalence of stress, urge, and mixed incontinence among postmenopausal and elderly women. The increasing availability of surgical treatment options, including slings and artificial urinary sphincters, along with greater awareness and diagnosis rates, contributes to strong market demand in this segment.

The pelvic organ prolapse segment is projected to witness fastest growth during the forecast period, supported by innovations in prolapse repair devices and a growing number of women opting for surgical correction of prolapse conditions. Increased emphasis on quality of life and treatment outcomes is also fostering the adoption of advanced surgical interventions in this category.

- By Procedure

On the basis of procedure, the uro-gynecological surgical devices market is segmented into dilation and curettage procedure, uterine balloon therapy, hysteroscopy procedure, tubal ligation procedure, and myomectomy procedure. The hysteroscopy procedure segment dominated the uro-gynecological surgical devices market with the largest share of 34.9% in 2024, driven by its minimally invasive nature and wide application in both diagnostic and therapeutic settings. Hysteroscopy is increasingly used for conditions such as abnormal uterine bleeding, fibroid removal, and endometrial evaluation, offering high precision with reduced patient downtime.

The uterine balloon therapy segment is expected to grow at the fastest rate during the forecast period due to rising demand for non-resectoscopic endometrial ablation techniques. This procedure is particularly favored for its simplicity, cost-effectiveness, and favorable safety profile, making it a suitable outpatient solution for abnormal uterine bleeding management

Uro-Gynecological Surgical Devices Market Regional Analysis

- North America dominates the uro-gynecological surgical devices market with the largest revenue share of 39.2% in 2024, supported by a well-established healthcare infrastructure, early adoption of advanced surgical techniques, and strong presence of leading medical device manufacturers, particularly in the U.S. where procedural volumes remain high

- The region’s robust demand is fueled by increased awareness of women’s health issues, strong reimbursement frameworks, and the widespread availability of skilled surgeons and minimally invasive surgical platforms

- In addition, factors such as a growing geriatric female population, frequent uro-gynecologic procedures in outpatient settings, and a high level of investment in innovative surgical solutions reinforce North America’s position as the leading market for uro-gynecological surgical devices

U.S. Uro-Gynecological Surgical Devices Market Insight

The U.S. uro-gynecological surgical devices market captured the largest revenue share of 79.3% in North America in 2024, fueled by the high prevalence of pelvic floor disorders and advanced surgical infrastructure. A growing aging female population, along with the rapid adoption of robotic-assisted and minimally invasive gynecological procedures, supports market growth. Furthermore, strong reimbursement policies and widespread access to specialized healthcare professionals are enhancing procedural volumes, particularly in outpatient and ambulatory surgical centers across the country.

Europe Uro-Gynecological Surgical Devices Market Insight

The Europe uro-gynecological surgical devices market is projected to grow at a steady CAGR throughout the forecast period, driven by increasing awareness of women’s pelvic health and the rising demand for minimally invasive procedures. Enhanced healthcare accessibility, especially in countries such as Germany, France, and Italy, is fostering the uptake of advanced surgical tools. The region is also experiencing growth due to supportive public health policies, early diagnosis programs, and an expanding elderly female demographic, leading to more interventions for urinary incontinence and pelvic organ prolapse.

U.K. Uro-Gynecological Surgical Devices Market Insight

The U.K. uro-gynecological surgical devices market is expected to grow at a noteworthy CAGR during the forecast period, spurred by increased emphasis on women's health initiatives and improvements in surgical care quality. The National Health Service (NHS) initiatives promoting pelvic health awareness, combined with the rising number of uro-gynecologic consultations and surgical treatments, are driving demand. In addition, the adoption of advanced endoscopic and laparoscopic tools for less invasive interventions supports continued market expansion.

Germany Uro-Gynecological Surgical Devices Market Insight

The Germany uro-gynecological surgical devices market is projected to expand significantly over the forecast period, backed by the country’s robust healthcare infrastructure and high adoption of advanced surgical technologies. Increasing focus on clinical outcomes, patient comfort, and sustainable surgical innovations supports strong demand for minimally invasive tools. Germany’s emphasis on quality standards and patient safety is fostering the development and uptake of precision uro-gynecological devices across both public and private healthcare sectors.

Asia-Pacific Uro-Gynecological Surgical Devices Market Insight

The Asia-Pacific uro-gynecological surgical devices market is poised to grow at the fastest CAGR of 25.4% from 2025 to 2032, driven by rising awareness of pelvic health, increased access to healthcare facilities, and a rapidly growing elderly female population in countries such as China, Japan, and India. Government-led health reforms, greater investment in hospital infrastructure, and improved training of gynecologic surgeons are enhancing procedural volumes. The region also benefits from the growing availability of affordable, locally manufactured surgical devices and the expansion of women’s health services.

Japan Uro-Gynecological Surgical Devices Market Insight

The Japan uro-gynecological surgical devices market is gaining traction due to the country’s aging population, high medical standards, and preference for advanced, non-invasive treatment options. Japan’s strong focus on geriatric care and early diagnosis supports a rise in uro-gynecologic procedures. Integration of high-definition endoscopic and robotic-assisted systems is expanding, with hospitals increasingly adopting these technologies to meet patient demand for high-precision, low-recovery interventions.

India Uro-Gynecological Surgical Devices Market Insight

The India uro-gynecological surgical devices market accounted for the largest revenue share in Asia-Pacific in 2024, driven by growing healthcare awareness, urbanization, and the rising demand for surgical treatments for urinary incontinence and pelvic organ prolapse. India’s expanding middle class and increased government focus on maternal and women’s health are fostering greater access to gynecologic surgical care. In addition, domestic production of cost-effective devices and the development of specialized women’s health centers are accelerating market growth across both urban and semi-urban regions.

Uro-Gynecological Surgical Devices Market Share

The uro-gynecological surgical devices industry is primarily led by well-established companies, including:

- CooperSurgical, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Medtronic (Ireland)

- Olympus Corporation (Japan)

- Stryker (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Cook Medical LLC (U.S.)

- Coloplast A/S (Denmark)

- BD (U.S.)

- Teleflex Incorporated (U.S.)

- Laborie Medical Technologies Corp. (Canada)

- Hologic, Inc. (U.S.)

- Minerva Surgical, Inc. (U.S.)

- RocaMed (France)

- Caldera Medical, Inc. (U.S.)

- MedGyn Products, Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

What are the Recent Developments in Global Uro-Gynecological Surgical Devices Market?

- In April 2023, CooperSurgical, Inc. announced the expansion of its manufacturing facility in Denmark to scale up production of advanced surgical instruments for gynecologic and uro-gynecologic procedures. The expansion aims to meet rising global demand for minimally invasive solutions and reflects CooperSurgical’s strategic focus on innovation in women's health. This move strengthens the company’s global supply chain and enhances its ability to deliver high-quality surgical products for pelvic health treatments

- In March 2023, Intuitive Surgical, Inc. launched its next-generation robotic-assisted surgical platform for gynecologic applications, featuring enhanced visualization, smaller instrumentation, and improved ergonomic design for surgeons. This system supports complex uro-gynecologic procedures such as pelvic organ prolapse repair and hysterectomy, showcasing Intuitive’s commitment to advancing precision surgery and improving patient outcomes through cutting-edge technology

- In March 2023, Olympus Corporation introduced an updated range of hysteroscopes and operative instruments aimed at expanding its minimally invasive gynecology portfolio. These devices offer improved optics and reduced invasiveness, enabling more effective treatment of uterine conditions. The launch reinforces Olympus’s role in driving endoscopic innovation and aligns with the broader market trend towards less invasive, high-precision uro-gynecologic interventions

- In February 2023, Boston Scientific Corporation partnered with leading healthcare institutions in Europe to conduct clinical trials evaluating the long-term safety and efficacy of new implantable devices for stress urinary incontinence. This initiative reflects Boston Scientific’s continued focus on evidence-based innovation and regulatory compliance, supporting global trust in advanced uro-gynecologic devices

- In January 2023, Medtronic plc unveiled its expanded suite of energy-based surgical devices designed for precision cutting and coagulation during pelvic surgeries. Showcased at the Global Congress on Minimally Invasive Gynecology, these tools cater to procedures such as myomectomy and endometrial ablation. The launch demonstrates Medtronic’s investment in comprehensive, technology-driven surgical platforms that address the evolving needs of uro-gynecologic care providers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.