Global Vernal Keratoconjunctivitis Treatment Market

Market Size in USD Million

USD

491.40 Million

USD

672.51 Million

2025

2033

USD

491.40 Million

USD

672.51 Million

2025

2033

| 2026 - 2033 | |

| USD 491.40 Million | |

| USD 672.51 Million | |

| % | |

|

Vernal Keratoconjunctivitis Treatment Market Size

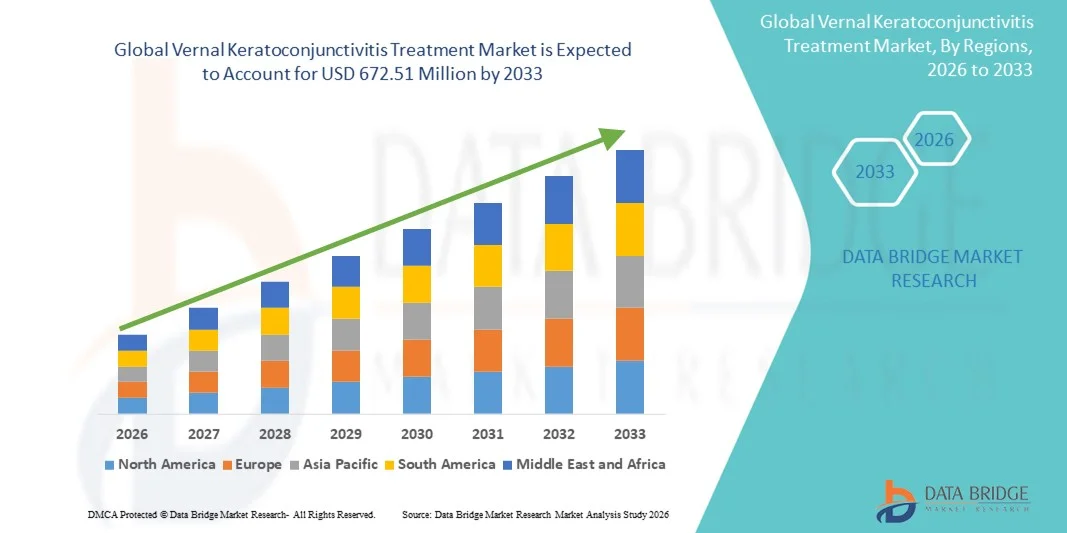

- The global vernal keratoconjunctivitis treatment market size was valued at USD 491.40 million in 2025 and is expected to reach USD 672.51 million by 2033, at a CAGR of 4.00% during the forecast period

- The market growth is largely fueled by increasing diagnosis and treatment of allergic ocular conditions, especially among children and young adults, coupled with rising awareness among healthcare professionals and patients

- Furthermore, development of advanced therapies, including immunomodulators and biologics, along with expanding ophthalmic and allergy-care infrastructure in emerging markets, is establishing VKC treatments as a preferred approach for ocular allergy management. These converging factors are accelerating the adoption of VKC therapies, thereby significantly boosting the industry's growth

Vernal Keratoconjunctivitis Treatment Market Analysis

- Vernal Keratoconjunctivitis treatments, offering management of this chronic ocular allergic condition often affecting children and young adults, are increasingly vital components of modern ophthalmology due to their need for safe, long‑term therapies, steroid‑sparing options, and improved patient adherence

- The escalating demand for VKC therapies is primarily fueled by the growing prevalence of ocular allergic conditions, rising awareness among healthcare professionals and patients of potential complications, and a rising preference for more targeted, convenient, and safer treatment options

- North America dominated the VKC treatment market with the largest revenue share of 36.9% in 2024, characterized by strong healthcare infrastructure, higher per‑capita healthcare spending, and active innovation and regulatory approvals, with the U.S. experiencing substantial adoption of advanced therapies, particularly in pediatric and chronic cases

- Asia‑Pacific is expected to be the fastest growing region in the VKC market during the forecast period due to increasing allergy prevalence, expanding ophthalmic care infrastructure, and rising disposable incomes in emerging countries

- The mast‑cell stabilizer segment dominated the VKC treatment market with a market share of 37.9% in 2024, driven by its established safety profile for long‑term management and effectiveness in pediatric patients, supporting the shift away from sole corticosteroid use

Report Scope and Vernal Keratoconjunctivitis Treatment Market Segmentation

|

Attributes |

Vernal Keratoconjunctivitis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Vernal Keratoconjunctivitis Treatment Market Trends

Shift Toward Biologics and Immunomodulatory Therapies

- A significant and accelerating trend in the global VKC treatment market is the growing adoption of immunomodulatory and biologic therapies that target underlying immune mechanisms, offering safer and more effective long-term management in children and severe cases

- For instance, the approval and increasing use of Verkazia (cyclosporine ophthalmic emulsion) demonstrates the market’s move beyond traditional antihistamines and corticosteroids toward targeted therapies

- Personalized formulations such as gels, ointments, and lower-dose regimens are enhancing patient adherence and comfort, particularly for pediatric populations. For instance, improved retention formulations reduce dosing frequency and irritation compared to conventional drops

- The integration of tele-ophthalmology and remote monitoring platforms enables early diagnosis, continuous treatment adjustments, and patient follow-up, particularly in regions with limited access to eye specialists

- This trend toward patient-centric, convenient, and targeted VKC therapies is reshaping clinician and patient expectations. Consequently, companies such as Santen and Eyevance are developing therapies with improved safety profiles, reduced steroid dependency, and enhanced pediatric compliance

- The demand for therapies that offer convenience, targeted action, and long-term safety is growing rapidly across both pediatric and adult populations, as patients and healthcare providers prioritize effective and safer treatment options

Vernal Keratoconjunctivitis Treatment Market Dynamics

Driver

Rising Allergy Burden and Growing Awareness Among Clinicians

- The increasing prevalence of VKC, driven by rising allergy incidence, urbanization, and environmental factors in tropical and subtropical regions, is a significant driver of market growth

- For instance, higher allergy burdens among children and adolescents in Asia-Pacific and Latin America are increasing the demand for effective VKC-specific therapies

- Growing awareness among ophthalmologists and allergists regarding long-term complications of untreated VKC, such as corneal scarring and vision impairment, is promoting earlier diagnosis and treatment adoption

- Regulatory approvals and inclusion of newer therapies in clinical guidelines across multiple geographies are expanding accessibility and supporting treatment uptake. For instance, multiple countries have recently approved cyclosporine-based therapies for pediatric VKC management

- Expansion of eye-care infrastructure, increased specialist availability, and better access to pediatric ophthalmology in emerging markets are supporting broader treatment adoption and regional market growth

- The increasing focus on early intervention, safer therapy options, and long-term management of VKC continues to drive demand for advanced treatment solutions in both developed and emerging regions

Restraint/Challenge

Diagnostic Variability and High Treatment Costs

- The absence of universally accepted diagnostic criteria and standardized grading of VKC severity remains a significant challenge, limiting consistent diagnosis and treatment initiation

- For instance, mild or atypical VKC cases often go undiagnosed due to heterogeneity in symptoms and lack of biomarkers, reducing therapy uptake potential

- High costs of advanced therapies and limited reimbursement coverage in many emerging markets hinder patient access and restrict market growth. For instance, biologics and immunomodulators remain expensive relative to conventional antihistamines or corticosteroids

- Continued reliance on corticosteroids and older therapies, despite potential side effects such as glaucoma and cataract, creates reluctance among patients and clinicians to adopt newer therapies

- Pediatric-focused VKC populations introduce ethical and regulatory challenges for conducting clinical trials, which can delay the introduction of new therapies into the market

- Overcoming these challenges through improved diagnostics, cost-effective therapies, and awareness programs will be vital for sustained growth of the global VKC treatment market

Vernal Keratoconjunctivitis Treatment Market Scope

The market is segmented on the basis of treatment, dosage form, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the VKC treatment market is segmented into mast cell stabilizers, antihistamines, nonsteroidal anti-inflammatory drugs (NSAIDs), topical corticosteroids, cyclosporine, tacrolimus, and others. The Mast Cell Stabilizers segment dominated the VKC treatment market with the largest market revenue share of 37.9% in 2024, driven by their effectiveness in preventing allergic reactions and providing long-term symptom management. For instance, medications such as cromolyn sodium and lodoxamide are widely prescribed to reduce itching, redness, and ocular inflammation in both children and adults. Their favorable safety profile compared to corticosteroids makes them the preferred choice for chronic VKC management, particularly in pediatric patients. Growth is supported by the increasing adoption of dual-action formulations combining antihistamine and mast cell stabilization for faster symptomatic relief. Mast cell stabilizers are also compatible with other VKC therapies, enabling combination treatment strategies that improve patient outcomes. Rising awareness among clinicians and caregivers about steroid-sparing approaches further reinforces the dominance of this segment.

The Topical Corticosteroids segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the need for rapid control of acute VKC flare-ups. For instance, ophthalmologists prescribe low- to medium-potency corticosteroids for short-term relief of severe inflammation and corneal complications. The segment benefits from innovations in safer formulations that reduce the risk of glaucoma and cataract associated with long-term use. Corticosteroids also provide synergistic effects when combined with mast cell stabilizers or cyclosporine, enhancing overall treatment efficacy. Growing awareness of controlled, monitored steroid therapy in pediatric patients supports faster adoption. The development of patient-friendly topical drops and gels with precise dosing further accelerates market growth.

- By Dosage Form

On the basis of dosage form, the VKC treatment market is segmented into solution, tablet, and syrup. The Solution segment dominated the market with a market share of 71.3% in 2024, driven by targeted delivery to the ocular surface and rapid relief of symptoms. For instance, topical drops allow fast relief of redness, itching, and corneal irritation with minimal systemic exposure, which is crucial in pediatric patients. Patient compliance is higher with eye drops compared to systemic forms, enhancing treatment adherence. Innovative formulations, such as preservative-free and gel-based drops, further reinforce the dominance of ophthalmic products. Systemic forms such as tablets or syrups are less preferred due to lower efficacy at the ocular surface, keeping topical forms dominant. Clinicians rely on topical administration as first-line therapy for both acute and maintenance treatment, maintaining its large market share.

The Tablets segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by convenience and longer-acting formulations supporting chronic management. For instance, gels with better ocular adhesion reduce dosing frequency and improve patient adherence. Tablets and syrups provide systemic support or adjunctive therapy in older children and adults. Emerging markets with limited ophthalmic specialist access are adopting systemic forms for easier administration. Novel dosage forms tailored for pediatric compliance are being developed, supporting faster market growth. Increased awareness of maintenance therapy needs is driving demand for these non-traditional dosage forms.

- By Route of Administration

On the basis of route of administration, the VKC treatment market is segmented into oral, ophthalmic, and others. The Ophthalmic segment dominated the market with 71% share in 2024, reflecting the ocular surface as the primary treatment site. For instance, topical eye drops and gels deliver direct therapy to conjunctiva and cornea, minimizing systemic exposure. Approved therapies, including mast cell stabilizers and cyclosporine emulsions, are primarily ophthalmic, reinforcing this dominance. Standard care guidelines recommend topical administration as first-line therapy, securing the majority share. Oral or parenteral routes are used only for refractory cases, contributing to their smaller market share. Pediatric patient preference for non-invasive methods further strengthens ophthalmic route dominance.

The Oral segment is anticipated to witness the fastest CAGR from 2026 to 2033, driven by the use of systemic therapy in chronic or refractory VKC cases. For instance, systemic antihistamines or immunomodulators are increasingly used as adjunct therapy for older children and adults. Growth is supported by expansion in home-based care and easier access in regions lacking ophthalmic specialists. Pipeline therapies in systemic immunomodulators and biologics are increasing adoption outside traditional ophthalmic routes. Sustained-release systemic formulations and home-administered therapy options drive further growth. Parenteral or combination routes are used in severe VKC with corneal involvement, representing a niche but expanding segment.

- By End-Users

On the basis of end-users, the VKC treatment market is segmented into clinic, hospital, and others. The Hospitals segment dominated the market with the largest market share in 2025, driven by diagnosis, prescription, and follow-up management for severe cases. For instance, ophthalmology outpatient units and pediatric allergy centers handle most VKC patients requiring specialized therapy. Advanced therapies, including immunomodulators, are first launched and predominantly used in hospital or clinic settings. Hospitals provide monitoring for corticosteroid therapy to mitigate side effects, maintaining their central role. Expansion of hospital infrastructure in emerging regions supports their continued dominance. Pediatric-focused treatment protocols are primarily administered in hospital or clinic settings, reinforcing this segment.

The Home-care segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by ambulatory care, home-based management, and tele-ophthalmology platforms supporting VKC patients outside hospitals. For instance, online consultations and prescription delivery allow long-term management without frequent hospital visits. Specialty allergy or immunology clinics are increasingly managing VKC patients, supporting faster growth of this segment. Outpatient and home-care adoption improves convenience and compliance, especially for pediatric patients. Remote monitoring platforms in emerging markets facilitate early intervention and treatment adherence. Parental preference for less hospital-dependent care drives adoption in these alternative end-user channels.

- By Distribution Channel

On the basis of distribution channel, the VKC treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market with 47.4% share in 2024, driven by in-clinic prescription and dispensing of therapies. For instance, advanced therapies such as cyclosporine and tacrolimus are primarily dispensed through hospital pharmacies. Hospital pharmacies provide direct access to specialist-recommended therapies and monitor patient adherence. Reimbursement policies often favour hospital-dispensed medications, supporting dominance of this channel. Hospitals have integrated ophthalmology and pediatric departments, strengthening the distribution network. High patient volumes in hospitals ensure steady demand, consolidating hospital pharmacy dominance.

The Online Pharmacy segment is anticipated to witness the fastest CAGR from 2026 to 2033, fueled by digital adoption and home-delivery of VKC therapies. For instance, caregivers of children with chronic VKC can refill prescriptions conveniently without clinic visits. Remote regions benefit from e-pharmacy access, expanding treatment reach beyond traditional channels. Telehealth integration accelerates growth of online pharmacies for VKC medication delivery. Manufacturers partner with e-pharmacy platforms to increase reach, fueling faster adoption. Convenience, cost-effectiveness, and support for long-term therapy contribute to rapid growth of this channel.

Vernal Keratoconjunctivitis Treatment Market Regional Analysis

- North America dominated the VKC treatment market with the largest revenue share of 36.9% in 2024, characterized by strong healthcare infrastructure, higher per‑capita healthcare spending, and active innovation and regulatory approvals, with the U.S. experiencing substantial adoption of advanced therapies, particularly in pediatric and chronic cases

- For instance, patients and caregivers in the region prioritize early diagnosis and access to specialized ophthalmology and allergy clinics, leading to higher adoption of mast cell stabilizers, corticosteroids, and immunomodulators

- This widespread adoption is further supported by strong healthcare reimbursement policies, availability of advanced therapies, and a growing preference for steroid-sparing long-term treatment strategies

U.S. Vernal Keratoconjunctivitis Treatment Market Insight

The U.S. Vernal Keratoconjunctivitis (VKC) Treatment Market captured the largest revenue share of 35% in 2025 within North America, fueled by high prevalence of pediatric allergic eye disorders and the presence of advanced healthcare infrastructure. Patients and caregivers are increasingly prioritizing early diagnosis and effective management through mast cell stabilizers, corticosteroids, and immunomodulators. The growing adoption of steroid-sparing therapies, along with increased awareness of chronic VKC management, further propels market growth. Moreover, the widespread availability of ophthalmologists and specialized pediatric eye clinics is significantly contributing to the market’s expansion. Rising healthcare expenditure and insurance coverage for ocular therapies also support higher adoption rates.

Europe Vernal Keratoconjunctivitis (VKC) Treatment Market Insight

The Europe Vernal Keratoconjunctivitis (VKC) Treatment Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of pediatric eye care and growing adoption of novel therapies such as cyclosporine and tacrolimus. The rise in urbanization, coupled with well-developed healthcare infrastructure, is fostering greater access to VKC treatments. Patients and caregivers are drawn to safe, long-term therapies that minimize steroid-related complications. The region is experiencing significant growth across both public and private healthcare settings, with VKC treatments being integrated into standard pediatric ophthalmology protocols. Government initiatives promoting eye care and preventive management further support market expansion.

U.K. Vernal Keratoconjunctivitis (VKC) Treatment Market Insight

The U.K. Vernal Keratoconjunctivitis (VKC) Treatment Market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of ocular allergies, the desire for effective symptom management, and high adoption of safe, long-term therapies. Concerns regarding chronic complications and corneal damage are encouraging parents and clinicians to choose mast cell stabilizers and immunomodulators for pediatric patients. The U.K.’s robust healthcare system, combined with high patient compliance and access to specialty care, is expected to continue to stimulate market growth. In addition, tele-ophthalmology and online prescription services are improving accessibility for chronic VKC management.

Germany Vernal Keratoconjunctivitis (VKC) Treatment Market Insight

The Germany Vernal Keratoconjunctivitis (VKC) Treatment Market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of pediatric eye health and the demand for safe, effective therapies. Germany’s advanced healthcare infrastructure and emphasis on early diagnosis and preventive care promote adoption of mast cell stabilizers, corticosteroids, and cyclosporine. The integration of VKC treatment protocols in ophthalmology and allergy clinics is becoming increasingly prevalent. Patients and caregivers show a strong preference for treatments with minimal long-term side effects, aligning with national health guidelines. Continuous innovations in topical formulations and patient-friendly dosing further support market growth.

Asia-Pacific Vernal Keratoconjunctivitis (VKC) Treatment Market Insight

The Asia-Pacific Vernal Keratoconjunctivitis (VKC) Treatment Market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing prevalence of allergic eye disorders, rising pediatric population, and improving healthcare access in countries such as China, Japan, and India. The region’s growing inclination towards early diagnosis and long-term disease management is driving the adoption of mast cell stabilizers and immunomodulators. Government initiatives promoting pediatric eye care and digital health solutions are further accelerating market growth. In addition, increasing awareness among parents and caregivers about steroid-sparing therapies is supporting faster adoption. Expansion of ophthalmology clinics and telemedicine platforms is improving accessibility in urban and semi-urban areas.

Japan Vernal Keratoconjunctivitis (VKC) Treatment Market Insight

The Japan Vernal Keratoconjunctivitis (VKC) Treatment Market is gaining momentum due to high prevalence of allergic conjunctivitis, advanced healthcare infrastructure, and increasing focus on pediatric eye health. Patients and caregivers prioritize safe and effective therapies such as mast cell stabilizers and cyclosporine for long-term management. The integration of VKC management protocols in specialty eye clinics and hospitals is fueling growth. Moreover, the increasing use of tele-ophthalmology and home-based care options is enhancing accessibility. Japan’s aging population also drives demand for easier-to-use treatment solutions suitable for all age groups. The strong emphasis on preventive care and chronic disease management supports sustained market expansion.

India Vernal Keratoconjunctivitis (VKC) Treatment Market Insight

The India Vernal Keratoconjunctivitis (VKC) Treatment Market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s growing pediatric population, rising awareness of allergic eye disorders, and improving healthcare access. India stands as one of the largest markets for ophthalmic therapies, with mast cell stabilizers, corticosteroids, and immunomodulators becoming increasingly popular in both urban and semi-urban areas. The push towards improving pediatric eye care, alongside affordable therapy options and expanding healthcare facilities, are key factors propelling the market in India. Government initiatives to strengthen preventive eye care and tele-ophthalmology services further support adoption. Rapid urbanization and increasing healthcare literacy among parents are accelerating the uptake of VKC treatments.

Vernal Keratoconjunctivitis Treatment Market Share

The Vernal Keratoconjunctivitis Treatment industry is primarily led by well-established companies, including:

- Santen Pharmaceutical Co., Ltd (Japan)

- Alcon (U.S.)

- Bausch Health Companies Inc. (Canada)

- Novartis AG (Switzerland)

- Sun Pharmaceutical Industries Ltd (India)

- Senju Pharmaceutical Co., Ltd (Japan)

- Akari Therapeutics (U.K.)

- Allakos Inc. (U.S.)

- SATELLOS (U.S.)

- Viatris Inc. (U.S.)

- Aldeyra Therapeutics, Inc. (U.S.)

- Laboratoires Thea S.A.S (France)

- Astellas Pharma Inc. (Japan)

- Abbott (U.S.)

- AbbVie Inc. (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Meda Pharmaceuticals (Sweden)

- Teva Pharmaceutical Industries Ltd (Israel)

- iCo Therapeutics Inc. (Canada)

What are the Recent Developments in Global Vernal Keratoconjunctivitis Treatment Market?

- In March 2025, a comprehensive review on the evolving role of Cyclosporine in VKC management was published in Frontiers in Ophthalmology, detailing improved ocular bioavailability, unpreserved formulations, expanded age‑indication, and global licensing efforts for CsA as a steroid‑sparing standard in VKC

- In August 2024, a review article titled Management of Vernal Keratoconjunctivitis: Navigating a Moving Therapeutic Landscape detailed the evolving treatment paradigm emphasizing immunomodulators, dual‑action topical agents and tailored maintenance regimens as standard practice

- In April 2024, a prospective paediatric study published in The Egyptian Journal of Hospital Medicine demonstrated that topical 0.03% tacrolimus ointment in children with VKC produced significant improvement in visual acuity and clinical signs (hyperemia, Tranta’s dots, papillary hypertrophy) with no cataract or infectious keratitis over six‑month follow‑up

- In June 2023, a study published in the journal I OVS presented early real‑world outcomes of 0.1% cationic‑emulsion Cyclosporine A 0.1% Cationic Emulsion (CsA CE) in children and adolescents with VKC, showing improved corneal fluorescein staining, reduced need for rescue steroids, and favourable safety profile. The real‑world data bolster earlier clinical‑trial findings and reinforce CsA CE’s position as a steroid‑sparing cornerstone in VKC management

- In December 2021, Japanese researchers reported that prolonged treatment with topical 0.1% Tacrolimus Ophthalmic Suspension in patients with VKC and atopic keratoconjunctivitis achieved remission in 92 % of cases by the 2‑year mark, demonstrating both efficacy and a steroid‑sparing effect. This study is significant because it shows that immunomodulators such as tacrolimus can move from adjunctive to core therapies for VKC, potentially changing the long‑term management paradigm

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.