Global Viral Gastroenteritis Market

Market Size in USD Billion

USD

2.27 Billion

USD

3.10 Billion

2024

2032

USD

2.27 Billion

USD

3.10 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.27 Billion | |

| USD 3.10 Billion | |

| % | |

|

Viral Gastroenteritis Market Size

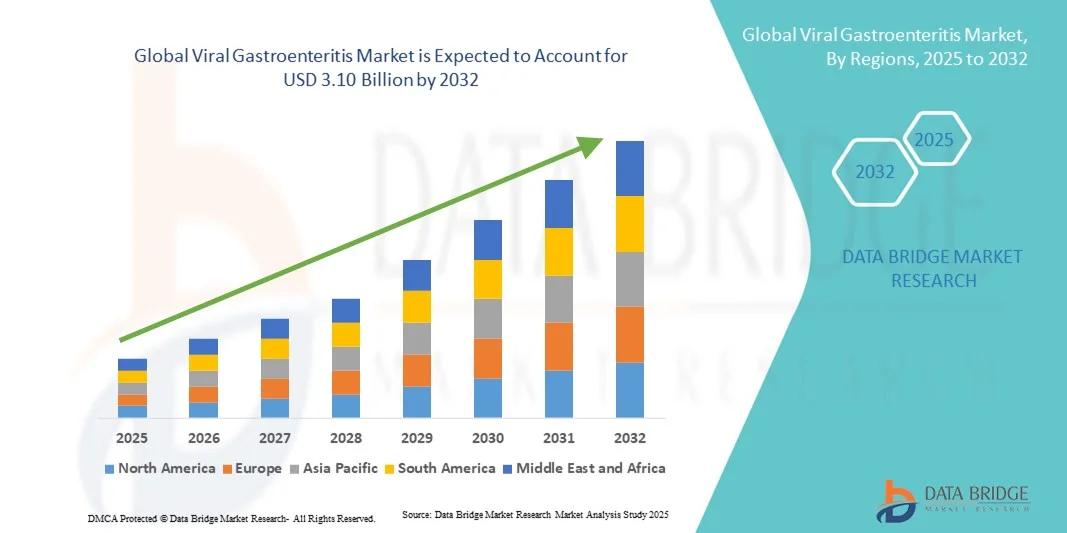

- The global viral gastroenteritis market size was valued at USD 2.27 billion in 2024 and is expected to reach USD 3.10 billion by 2032, at a CAGR of 3.99% during the forecast period

- The market growth is largely fueled by the increasing global burden of gastrointestinal infections, rising awareness about early diagnosis, and the widespread implementation of diagnostic screening programs in both developed and developing regions.

- Furthermore, the demand for rapid, accurate, and multiplex testing solutions for pathogens such as norovirus, rotavirus, and bacterial agents is pushing technological advancements and adoption rates. These dynamics are reinforcing the critical role of gastroenteritis testing in public health surveillance and clinical diagnosis, thereby accelerating overall market expansion

Viral Gastroenteritis Market Analysis

- Viral gastroenteritis, commonly known as the stomach flu, is a prevalent gastrointestinal infection caused by viruses such as norovirus, rotavirus, and adenovirus. It remains a significant public health concern worldwide, leading to increased healthcare utilization and economic burden

- The escalating demand for viral gastroenteritis management is primarily fueled by the rising incidence of viral infections, advancements in diagnostic technologies, and heightened awareness regarding gastrointestinal health

- North America dominated the viral gastroenteritis market with the largest revenue share of 40.6% in 2024, characterized by robust healthcare infrastructure, widespread availability of diagnostic services, and a high prevalence of viral gastroenteritis cases

- Asia-Pacific is expected to be the fastest-growing region in the viral gastroenteritis market during the forecast period due to increasing urbanization, improving healthcare access, and rising awareness about gastrointestinal health

- The norovirus segment dominated the viral gastroenteritis market with a market share of 42% in 2024, driven by its high transmissibility and frequent outbreaks in community settings such as schools and cruise ships

Report Scope and Viral Gastroenteritis Market Segmentation

|

Attributes |

Viral Gastroenteritis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Viral Gastroenteritis Market Trends

Advancements in Rapid Diagnostics and Multiplex Testing

- A significant and accelerating trend in the global viral gastroenteritis market is the growing adoption of rapid diagnostic tests and multiplex pathogen detection systems, enabling early and accurate identification of viral agents such as norovirus and rotavirus

- For instance, the BioFire FilmArray Gastrointestinal Panel allows simultaneous detection of multiple viral and bacterial pathogens, offering healthcare providers faster results and improved clinical decision-making

- Advancements in point-of-care testing and home-based diagnostic kits facilitate timely intervention and reduce the spread of infections, particularly in high-risk environments such as childcare centers, hospitals, and cruise ships

- The integration of diagnostic solutions with digital reporting platforms and cloud-based health systems allows centralized monitoring of outbreak trends and epidemiological data, enhancing public health surveillance

- This trend towards faster, more comprehensive, and connected diagnostic solutions is reshaping expectations in healthcare management, prompting companies such as Quidel and Cepheid to develop multiplex tests with automated reporting and user-friendly interfaces

- The demand for rapid, accurate, and multiplex diagnostic solutions is growing steadily across both clinical and community healthcare settings, as stakeholders prioritize timely detection and outbreak prevention

Viral Gastroenteritis Market Dynamics

Driver

Increasing Incidence of Gastroenteritis and Rising Awareness

- The rising prevalence of viral gastroenteritis infections globally, coupled with growing awareness of gastrointestinal health, is a significant driver for the heightened demand for diagnostic and preventive solutions

- For instance, in 2023, Quidel launched updated norovirus testing kits to expand early detection capabilities in hospitals and clinics, reflecting the market’s focus on rapid response

- As healthcare providers and caregivers recognize the importance of timely diagnosis and outbreak management, viral gastroenteritis testing and monitoring become integral to public health strategies

- Furthermore, increasing media coverage, educational campaigns, and awareness programs are making preventive measures, such as hygiene practices and vaccination, more widely adopted in both developed and developing regions

- The growing emphasis on community health, infection control in hospitals, and early diagnostic intervention is driving the adoption of advanced testing solutions and vaccines in high-risk populations

Restraint/Challenge

Limited Access in Developing Regions and High Cost of Advanced Solutions

- Limited access to modern diagnostic tools and vaccines in low-income regions poses a significant challenge to broader market penetration, slowing efforts to reduce disease burden

- For instance, reports indicate that regions in Sub-Saharan Africa and Southeast Asia still face challenges in distributing rotavirus vaccines and advanced testing kits to rural populations

- Addressing logistical issues, supply chain gaps, and affordability is crucial for expanding market reach. Companies such as BioFire and Cepheid emphasize collaborative programs with governments and NGOs to enhance accessibility

- In addition, the relatively high cost of multiplex diagnostic tests and advanced vaccines compared to traditional methods can be a barrier for budget-constrained healthcare systems

- While ongoing initiatives aim to subsidize or streamline testing and vaccination programs, the perceived premium and infrastructure limitations continue to hinder widespread adoption in certain regions

Viral Gastroenteritis Market Scope

The market is segmented on the basis of type, treatment, diagnosis, indication, dosage, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the viral gastroenteritis market is segmented into norovirus, rotavirus, and others. The norovirus segment dominated the market with the largest revenue share of 42% in 2024, driven by its high transmissibility and frequent outbreaks in community settings such as schools, hospitals, and cruise ships. Norovirus infections are highly contagious, prompting increased testing, hospital visits, and preventive interventions, which boosts market demand. The high prevalence in developed regions, combined with continuous monitoring by public health agencies, ensures steady market consumption. Norovirus-focused diagnostic kits and preventive solutions are widely adopted in both clinical and non-clinical settings. The segment’s dominance is also supported by increased awareness campaigns emphasizing hygiene and sanitation. Furthermore, research and development efforts targeting norovirus detection and treatment continue to enhance product offerings.

The rotavirus segment is expected to witness the fastest growth at a CAGR of 5.6% from 2025 to 2032, driven by the rising adoption of rotavirus vaccination programs in developing countries. Government-led immunization initiatives, coupled with the increasing awareness of childhood gastroenteritis prevention, fuel demand for rotavirus vaccines and rapid diagnostic tests. Hospitals and pediatric clinics are actively incorporating rotavirus testing in routine screenings, accelerating market penetration. The segment benefits from technological advancements in vaccine formulations and cold-chain distribution, ensuring accessibility in remote regions. Increasing global focus on child health and preventive care underpins rotavirus segment growth. The expansion of public health programs in Asia-Pacific and Africa further contributes to faster adoption rates.

- By Treatment

On the basis of treatment, the viral gastroenteritis market is segmented into intravenous fluids, antimotility agents, electrolytes, antiemetic drugs, antidiarrheal drugs, and others. The intravenous fluids segment dominated the market in 2024, primarily due to its critical role in managing dehydration caused by severe gastroenteritis cases. Hospitals and clinics heavily rely on IV therapy to stabilize patients, particularly children and the elderly, who are more susceptible to fluid loss. IV fluids ensure rapid rehydration, restore electrolyte balance, and reduce the risk of complications. The segment’s demand is further supported by the high frequency of hospital admissions during seasonal outbreaks. Healthcare providers prioritize IV fluids for severe or prolonged infections, making it a standard treatment approach. Clinical guidelines recommend IV administration as an essential first-line treatment in acute cases, sustaining market revenue.

The antiemetic drugs segment is expected to witness the fastest growth during the forecast period, driven by increasing demand for symptom management in outpatient and home-care settings. Antiemetic medications, which alleviate nausea and vomiting, improve patient comfort and reduce hospital readmissions. Rising awareness among caregivers and healthcare professionals about managing viral gastroenteritis symptoms at early stages boosts adoption. Innovations in oral and injectable formulations enhance patient compliance and market potential. The segment is also supported by expanding over-the-counter availability in developed markets, facilitating faster access to treatment.

- By Diagnosis

On the basis of diagnosis, the viral gastroenteritis market is segmented into physical examination, rapid stool tests, and others. The rapid stool test segment dominated in 2024 due to its ability to deliver quick, accurate, and multiplex detection of viral pathogens. Hospitals, laboratories, and point-of-care facilities widely prefer rapid stool tests for norovirus, rotavirus, and adenovirus detection. These tests help in timely clinical decision-making, outbreak management, and infection control measures. Integration with digital reporting platforms enhances epidemiological monitoring and reduces transmission rates. The segment benefits from continuous technological improvements, increasing sensitivity, and ease of use. The growing focus on early diagnosis and public health monitoring ensures consistent demand.

The physical examination segment is expected to witness the fastest growth from 2025 to 2032 as awareness campaigns emphasize early clinical evaluation in resource-limited settings. Physical assessments allow healthcare providers to quickly identify dehydration signs and prioritize treatment, especially where laboratory facilities are scarce. Integration with telemedicine platforms and mobile health applications is improving diagnostic reach. Clinics and small healthcare facilities increasingly adopt standardized clinical evaluation protocols. Growth is also supported by training programs for healthcare professionals on recognizing gastroenteritis symptoms. Early detection through physical examination reduces complications and hospitalizations, driving adoption.

- By Indication

On the basis of indication, the viral gastroenteritis market is segmented into abdominal pain, dizziness, diarrhea, nausea, vomiting, headache, chills, loss of appetite, fever, joint stiffness, sweating, muscle pain, weight loss, and others. The diarrhea segment dominated in 2024, as it is the most common and severe symptom of viral gastroenteritis that directly affects patient hydration and electrolyte balance. Healthcare providers prioritize treatment strategies targeting diarrhea, leading to higher adoption of IV fluids, antidiarrheal drugs, and rehydration therapies. Diarrhea cases significantly contribute to hospital admissions, particularly among children and the elderly. Public health campaigns focus on diarrhea prevention and treatment, supporting market growth. Rapid detection and symptom-targeted therapies further reinforce the segment’s revenue contribution. Continuous research on anti-diarrheal medications enhances effectiveness, sustaining demand.

The vomiting segment is expected to witness the fastest growth during the forecast period due to its prevalence across all age groups and the increasing focus on symptom management. Vomiting leads to dehydration and nutritional loss, necessitating prompt medical intervention. The segment benefits from the rising use of antiemetic drugs and supportive care solutions in both outpatient and inpatient settings. Awareness of symptom alleviation and patient comfort drives adoption in home-care and clinical settings. Technological advancements in oral, injectable, and pediatric-friendly formulations further expand the market. Increasing patient preference for non-invasive symptom management supports faster growth.

- By Dosage

On the basis of dosage, the viral gastroenteritis market is segmented into tablet, injection, and others. The injection segment dominated in 2024 due to its role in delivering intravenous fluids, electrolytes, and injectable medications for severe cases of gastroenteritis. Injectable treatments ensure rapid bioavailability and are crucial for hospitalized patients requiring immediate symptom control. Hospitals and emergency care centers rely heavily on injectable dosage forms for critical interventions. The segment is further strengthened by high adoption in pediatric and geriatric care settings, where rapid intervention is necessary. Clinical guidelines recommend injection therapy for severe dehydration or complicated cases, sustaining market revenue.

The tablet segment is expected to witness the fastest growth from 2025 to 2032, driven by the rising preference for convenient, home-based symptom management. Tablets for antidiarrheal, antiemetic, and electrolyte supplementation allow patients to self-administer treatment with ease. OTC availability in developed regions accelerates adoption. The segment is also supported by pediatric-friendly and chewable tablet formulations, enhancing compliance. Awareness campaigns promoting early intervention increase tablet consumption. Growing home-care trends and telemedicine guidance further drive the segment’s growth.

- By Route of Administration

On the basis of route of administration, the viral gastroenteritis market is segmented into oral, intravenous, and others. The intravenous segment dominated in 2024 due to its critical role in managing severe dehydration, restoring electrolytes, and ensuring rapid symptom control. Hospitals and emergency care units extensively use IV administration for acute gastroenteritis cases. This route provides quick therapeutic outcomes, which is vital for pediatric, geriatric, and immunocompromised patients. Clinical protocols prioritize IV rehydration in moderate to severe cases, sustaining high market revenue. The segment’s dominance is reinforced by hospital reliance during seasonal outbreaks. Advanced IV formulations with balanced electrolytes enhance efficacy and adoption.

The oral segment is expected to witness the fastest growth during the forecast period due to increasing demand for home-based management and ease of use. Oral rehydration salts, antidiarrheal, and antiemetic medications are widely used in outpatient care and home settings. Growth is supported by rising awareness of preventive and supportive care measures. Pediatric and adult-friendly oral formulations further increase adoption. Telemedicine guidance and OTC availability boost oral treatment consumption. Convenience, safety, and accessibility are key drivers of segment growth.

- By End-Users

On the basis of end-users, the viral gastroenteritis market is segmented into clinics, hospitals, and others. The hospitals segment dominated in 2024 due to high patient influx during viral gastroenteritis outbreaks and the need for inpatient care. Hospitals provide comprehensive treatment options including IV fluids, injections, and rapid diagnostics. They also serve as primary centers for outbreak management and public health surveillance. High adoption of advanced testing kits, preventive solutions, and vaccines in hospitals sustains revenue. Specialized gastroenterology units in hospitals contribute further to market dominance. Government and insurance support enhances hospital treatment adoption.

The clinics segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing demand for early diagnosis and outpatient care. Clinics are adopting rapid diagnostic tests and oral treatment solutions to provide efficient care. Home-care integration, telemedicine, and preventive healthcare initiatives contribute to faster adoption. Clinics in urban and semi-urban regions are expanding gastroenteritis treatment services. Growing awareness and preference for quick symptom management drive the segment. Cost-effective treatment options in clinics further support adoption.

- By Distribution Channel

On the basis of distribution channel, the viral gastroenteritis market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated in 2024, as hospitals remain the primary point for treatment, diagnostics, and preventive care solutions. High patient visits during gastroenteritis outbreaks ensure consistent demand. Hospital pharmacies supply IV fluids, injections, and oral medications, supporting continuous revenue. Integration with hospital protocols and insurance coverage further strengthens adoption. The segment’s dominance is bolstered by frequent seasonal peaks in gastroenteritis prevalence. Hospital pharmacies also provide specialized counseling and guidance for treatment compliance.

The online pharmacy segment is expected to witness the fastest growth during the forecast period due to the rising preference for convenient home delivery of medicines and diagnostics. Online platforms offer easy access to oral medications, OTC products, and diagnostic kits. Increasing digital literacy, smartphone adoption, and e-commerce penetration support growth. Telemedicine recommendations for home treatment enhance online pharmacy utilization. Convenience, contactless delivery, and competitive pricing accelerate adoption. Expanding regional reach and marketing initiatives further contribute to rapid growth.

Viral Gastroenteritis Market Regional Analysis

- North America dominated the viral gastroenteritis market with the largest revenue share of 40.6% in 2024, characterized by robust healthcare infrastructure, widespread availability of diagnostic services, and a high prevalence of viral gastroenteritis cases

- Consumers and healthcare providers in the region prioritize rapid, reliable diagnostic tools, with widespread adoption of molecular and multiplex testing platforms in hospitals, diagnostic labs, and outpatient settings

- This strong market position is further reinforced by favorable reimbursement policies, growing awareness of infectious disease control, and continuous innovation by regional diagnostic companies, making North America a key hub for advanced gastroenteritis testing solutions in both clinical and public health applications

U.S. Viral Gastroenteritis Market Insight

The U.S. gastroenteritis testing market captured the largest revenue share of 79% in 2024 within North America, driven by the high incidence of gastrointestinal infections, widespread implementation of routine diagnostic testing, and advanced molecular diagnostic capabilities. The demand for rapid and accurate pathogen detection tools is growing, particularly in hospitals, urgent care centers, and public health labs. Continued investment in healthcare infrastructure and R&D, along with proactive government surveillance programs, further supports market growth. The presence of leading diagnostic firms and their focus on multiplex and point-of-care testing solutions significantly contribute to the U.S. market’s expansion.

Europe Gastroenteritis Testing Market Insight

The Europe gastroenteritis testing market is projected to expand at a substantial CAGR throughout the forecast period, fueled by stringent infectious disease regulations and an increased emphasis on early and precise diagnosis. Rising foodborne illness cases and hospital-acquired infections are prompting the adoption of advanced diagnostic tools. The region’s focus on universal healthcare access and public health initiatives is boosting the demand for comprehensive testing solutions across hospitals and laboratories. Multiplex PCR and automated systems are gaining traction across both public and private healthcare facilities.

U.K. Gastroenteritis Testing Market Insight

The U.K. gastroenteritis testing market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the country’s commitment to infection control and widespread adoption of modern diagnostic technologies. National surveillance programs and NHS investments in pathogen detection platforms are key growth drivers. The rising prevalence of norovirus outbreaks, especially in schools and care homes, is increasing demand for rapid diagnostics. Furthermore, the U.K.'s centralized healthcare system ensures consistent testing protocols, supporting efficient outbreak tracking and treatment.

Germany Gastroenteritis Testing Market Insight

The Germany gastroenteritis testing market is expected to expand at a considerable CAGR during the forecast period, driven by a strong healthcare infrastructure, high diagnostic awareness, and growing demand for molecular testing solutions. Germany’s focus on public health, food safety, and hygiene practices fosters the widespread use of diagnostic tools across hospitals, research institutes, and public labs. The country is also investing in innovations such as real-time PCR and sequencing for precise pathogen identification, which is increasing the adoption of high-end testing solutions.

Asia-Pacific Gastroenteritis Testing Market Insight

The Asia-Pacific gastroenteritis testing market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by rising gastrointestinal disease prevalence, improved healthcare access, and technological advancements in countries such as China, Japan, and India. Government-led healthcare modernization and disease surveillance initiatives are expanding diagnostic capacities. Increasing awareness about food and waterborne infections, coupled with rising healthcare expenditure and urbanization, is driving the adoption of accurate and rapid testing platforms across the region.

Japan Gastroenteritis Testing Market Insight

The Japan gastroenteritis testing market is gaining momentum due to its advanced healthcare system, aging population, and increasing use of automated and multiplex diagnostic platforms. The country’s strong focus on infection prevention and early intervention encourages widespread testing, particularly in hospitals and elderly care facilities. High demand for compact, efficient diagnostic tools compatible with Japan’s tech-driven healthcare infrastructure is supporting market expansion. Public health campaigns targeting hygiene and food safety are also boosting awareness and testing rates.

India Gastroenteritis Testing Market Insight

The India gastroenteritis testing market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by the country’s large population, improving healthcare infrastructure, and rising awareness of infectious disease diagnostics. The government’s initiatives to combat diarrheal diseases and enhance primary care services have accelerated the deployment of diagnostic tools in public health centers. Affordable test kits and rising penetration of point-of-care solutions are enabling broader access across urban and rural areas. Additionally, the local manufacturing of testing kits and the growth of private diagnostics chains are further propelling market expansion in India.

Viral Gastroenteritis Market Share

The Viral Gastroenteritis industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- GSK plc (U.K.)

- Moderna, Inc. (U.S.)

- Vaxart, Inc. (U.S.)

- HilleVax, Inc. (U.S.)

- INDIANA UNIVERSITY (U.S.)

- GIVAX, Inc. (U.S.)

- Serum Institute of India Pvt. Ltd. (India)

- Bharat Biotech (India)

- Biological E. Limited (India)

- Shantha Biotechnics Ltd. (India)

- Aridis Pharmaceuticals, Inc. (U.S.)

- Fundação Butantan (Brazil)

- Center for Research and Production of Vaccines (Vietnam)

- Lanzhou Institute of Biological Products (China)

- University of Texas at Austin (U.S.)

- Emory University (U.S.)

- Johns Hopkins University (U.S.)

What are the Recent Developments in Global Viral Gastroenteritis Market?

- In June 2025, researchers at the University of Texas at Austin published a study in Science Translational Medicine demonstrating that an experimental oral norovirus vaccine, VXA-G1.1-NN, effectively triggered antibodies capable of neutralizing a wide range of norovirus strains. This advancement holds promise for a broadly protective vaccine against norovirus, a leading cause of acute gastroenteritis worldwide

- In June 2025, Emory University and Micron Biomedical announced the commencement of a clinical trial for CC24, a novel rotavirus vaccine delivered via dissolvable microarray technology. This trial represents the first-ever CDC-sponsored clinical trial of a vaccine delivered via patch technology, potentially offering a pain-free and innovative method for immunization

- In May 2025, a phase 2 placebo-controlled study published in Science Translational Medicine revealed that an oral tablet norovirus vaccine generated mucosal immunity and reduced viral shedding in participants. This development signifies a step forward in creating effective oral vaccines for norovirus, potentially simplifying administration and enhancing accessibility

- In March 2025, the Ministry of Health and UNICEF launched a media campaign in Vietnam aimed at educating parents and caregivers about the importance of rotavirus vaccination. The campaign successfully increased awareness and vaccine confidence, particularly among caregivers in remote and ethnic minority communities, contributing to higher vaccination rates

- In October 2024, a groundbreaking phase 3 clinical trial commenced in the UK, evaluating the world's first mRNA vaccine against norovirus. The trial, named Nova 301, involves 25,000 adult participants across 27 NHS sites. Developed by Moderna in collaboration with the UK government, the vaccine aims to protect against three major norovirus strains by instructing cells to produce their protein coats

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.