Global Virtual Client Computing Market

Market Size in USD Billion

USD

33.00 Billion

USD

70.74 Billion

2024

2032

USD

33.00 Billion

USD

70.74 Billion

2024

2032

| 2025 - 2032 | |

| USD 33.00 Billion | |

| USD 70.74 Billion | |

| % | |

|

Virtual Client Computing Market Size

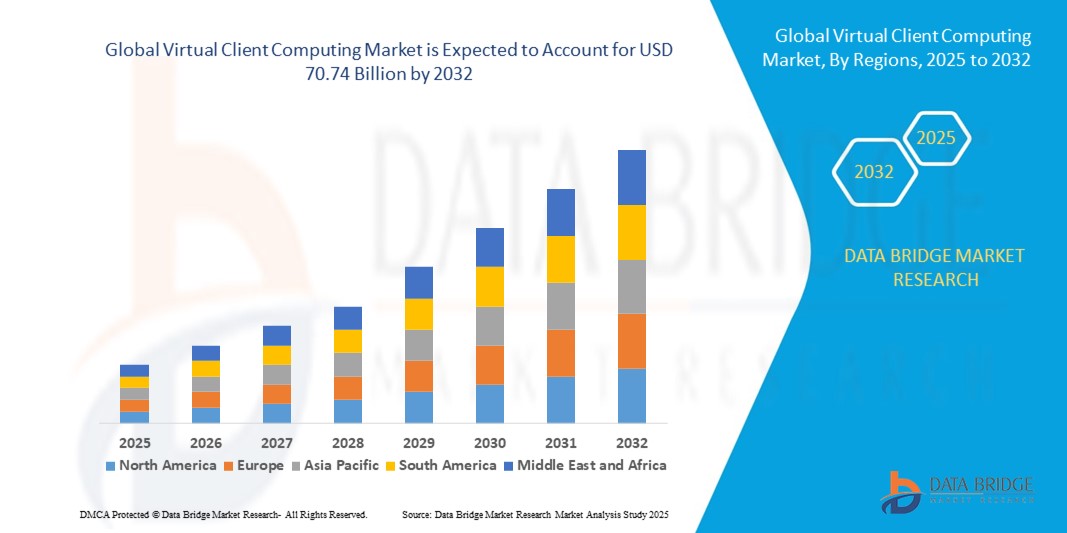

- Global virtual client computing market size was valued at USD 33.00 Billion in 2024 and is projected to reach USD 70.74 Billion by 2032, with a CAGR of 10.00% during the forecast period of 2025 to 2032

- This growth is driven by increasing demand for secure, centralized IT infrastructures, remote working solutions, and cost-effective virtualization technologies across various industries

- The virtual client computing market is experiencing steady growth, driven by the increasing demand for centralized management, enhanced security, and cost efficiency in IT infrastructure. Virtual client computing allows organizations to host desktop environments, applications, and data on centralized servers, enabling employees to access their work environments from any device, anywhere

Virtual Client Computing Market Analysis

- Virtual client computing (VCC), which enables centralized management and deployment of desktop environments across various endpoints, is a critical technology in modern enterprise IT infrastructure, offering enhanced data security, reduced hardware dependency, and simplified management through virtualization and cloud integration

- The growing demand for virtual client computing is primarily driven by the widespread adoption of remote and hybrid work models, increasing concerns over data security, and the need for scalable, cost-efficient IT solutions that support business continuity and workforce mobility

- North America dominated the virtual client computing (VCC) market with the largest revenue share of 41.5% in 2024, driven by rapid adoption of cloud technologies, digital workplace transformation, and a strong emphasis on data security

- The Asia-Pacific region is expected to grow at the fastest CAGR 9.32% from 2025 to 2032, fueled by rapid digitalization, expanding IT infrastructure, and increasing adoption of cloud services in emerging markets such as China, India, Japan, and Australia

- The on-premises segment dominated the market with the largest revenue share of 58.6% in 2024, supported by enterprises requiring complete control, data sovereignty, and compliance with strict regulatory frameworks

Report Scope and Global Virtual Client Computing Market Segmentation

|

Atrributes |

Global Virtual client computing Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Virtual Client Computing Market Trends

Rise of Remote Work

- A pivotal trend driving the virtual client computing (VCC) market is the widespread adoption of remote work, which has significantly reshaped organizational operations. Initially accelerated by the COVID-19 pandemic, this shift continues to be sustained by advancements in technology and evolving employee expectations around workplace flexibility

- In response, businesses rapidly implemented remote work strategies to ensure business continuity and protect workforce well-being—leading to a surge in demand for VCC solutions

- These technologies provide secure, consistent access to corporate resources from any location and across multiple devices, including laptops, tablets, and smartphones. By enabling seamless collaboration among distributed teams, VCC enhances productivity, employee satisfaction, and workforce agility

- Moreover, it allows organizations to expand recruitment efforts globally, no longer limited by geographic boundaries. As remote and hybrid work models become the norm, companies are increasingly investing in robust virtual client computing infrastructure to support long-term operational resilience, cybersecurity, and digital transformation goals

Virtual Client Computing Market Dynamics

Drive

Rising Demand for Remote Work Solutions and Centralized IT Management

- The surge in remote and hybrid work models across enterprises globally is a major driver for the virtual client computing (VCC) market, as organizations seek secure, scalable, and easily manageable IT infrastructures to support distributed workforces

- For instance, in March 2024, Citrix (a business unit of Cloud Software Group) introduced enhanced features in its DaaS offerings, enabling more efficient remote access and improved performance monitoring, aiming to support the growing demands of hybrid work environments

- VCC solutions allow IT teams to centrally manage desktops, applications, and user environments, enhancing data security, reducing hardware dependency, and streamlining updates and troubleshooting processes

- Furthermore, the shift towards cloud-based IT infrastructure and the increasing adoption of virtualization technologies are reinforcing the demand for VCC, as businesses aim to reduce operating costs and improve flexibility

- The ability to deliver consistent desktop experiences across various devices and locations, while ensuring compliance and data protection, makes VCC an attractive solution for industries such as healthcare, finance, and education. As digital transformation initiatives accelerate, the role of virtual client computing in enabling seamless and secure remote operations continues to expand

Restraint/Challenge

Complex Deployment and Data Privacy Concerns

- Despite its benefits, virtual client computing faces challenges related to complex deployment processes and growing concerns over data privacy, particularly when integrating with legacy systems or transitioning from traditional desktop environments

- For instance, small and mid-sized enterprises (SMEs) often struggle with the technical and financial demands of implementing full-scale VDI or DaaS solutions, especially without dedicated IT support. In addition, storing and managing sensitive data on centralized servers or cloud environments introduces privacy and compliance risks, especially in sectors governed by strict regulations such as healthcare (HIPAA) or finance (GDPR, PCI DSS)

- Concerns about data breaches, unauthorized access, and compliance violations can deter some organizations from adopting VCC solutions, particularly in regions with limited cybersecurity infrastructure or data protection frameworks

- Addressing these concerns requires robust encryption, secure access protocols, regular security audits, and compliance with regional data laws. Leading vendors such as VMware and Microsoft emphasize zero-trust architectures and secure endpoint management to mitigate these risks

- Furthermore, the upfront investment in infrastructure and the need for skilled personnel to manage and maintain VCC systems can act as additional barriers, particularly for resource-constrained organizations. Educating businesses on long-term ROI and simplifying deployment through managed services and cloud-hosted options will be essential for broader adoption

Virtual Client Computing Market Scope

The market is segmented on the basis of deployment type, end user, component, type of virtualization, user type, and access mode.

- By Deployment Type

On the basis of deployment type, the virtual client computing market is segmented into on-premises and cloud-based. The on-premises segment dominated the market with the largest revenue share of 58.6% in 2024, supported by enterprises requiring complete control, data sovereignty, and compliance with strict regulatory frameworks. Large organizations in sectors such as banking and government often prefer on-premises deployment to manage sensitive data securely. Moreover, legacy system integration and high customization needs continue to strengthen the dominance of on-premises virtualization solutions.

The cloud-based segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the rapid shift toward hybrid and multi-cloud strategies. Cloud virtualization provides scalability, cost efficiency, and flexibility, making it attractive to SMEs and enterprises undergoing digital transformation. With rising demand for subscription-based models and reduced infrastructure costs, cloud-based deployment is anticipated to reshape the future growth of the virtualization market.

- By End User

On the basis of end user, the virtual client computing market is segmented into healthcare, education, IT & telecom, BFSI, and manufacturing. The IT & telecom segment accounted for the largest revenue share of 34.7% in 2024, driven by the sector’s reliance on virtualization to optimize data centers, reduce operational costs, and ensure seamless workload management. Rapid adoption of 5G networks and cloud-native applications further increases demand for virtualized infrastructure in IT & telecom.

The healthcare sector is anticipated to witness the fastest growth rate from 2025 to 2032, supported by rising adoption of electronic health records (EHRs), telemedicine, and secure data storage requirements. Virtualization enables healthcare providers to consolidate servers, improve disaster recovery, and ensure HIPAA-compliant patient data management. As digital health expands, healthcare providers are increasingly investing in virtualized systems to enhance efficiency, scalability, and security. This trend positions healthcare as a strong driver of future virtualization market expansion.

- By Component

On the basis of component, the virtual client computing market is segmented into software and hardware. The software segment dominated the market with a revenue share of 61.4% in 2024, as software solutions form the backbone of virtualization by enabling hypervisors, virtual machines (VMs), and workload automation. Enterprises prioritize virtualization software for workload optimization, security, and cloud integration, with vendors continuously innovating to improve performance and reduce complexity.

The hardware segment is projected to record the fastest growth from 2025 to 2032, driven by the need for advanced servers, storage, and networking components to support highly virtualized environments. Hardware innovations, including GPU virtualization and high-performance computing, are further propelling adoption. With the rise of edge computing and AI workloads, demand for hardware designed for virtualized infrastructures is accelerating, particularly in large-scale enterprises and data centers, positioning hardware as the fastest-growing component of the market.

- By Type of Virtualization

On the basis of type, the virtual client computing market is segmented into desktop virtualization, application virtualization, and data virtualization. Desktop virtualization dominated with the largest revenue share of 46.1% in 2024, supported by enterprises seeking centralized management, cost efficiency, and improved security for remote workforces. Virtual desktop infrastructure (VDI) solutions became essential as organizations expanded work-from-home and hybrid work models.

Data virtualization is expected to witness the fastest CAGR from 2025 to 2032, fueled by the growing need to access, integrate, and analyze large volumes of data without replication. Businesses across industries are leveraging data virtualization to enhance real-time analytics, streamline business intelligence, and enable decision-making agility. Application virtualization continues to see steady adoption, but the rapid digital transformation trend is making data virtualization a top priority for enterprises investing in AI, big data, and real-time data integration solutions.

- By User Type

On the basis of user type, the virtual client computing market is segmented into large enterprises and small & medium enterprises (SMEs). Large enterprises dominated with a revenue share of 67.8% in 2024, driven by their significant investments in IT infrastructure, need for scalability, and demand for centralized management of virtual environments. These organizations often deploy advanced virtualization strategies to optimize data centers, support global operations, and ensure compliance with security regulations.

The SME segment is expected to record the fastest growth from 2025 to 2032, fueled by rising awareness of cost savings, simplified IT operations, and improved disaster recovery enabled by virtualization. Cloud-based solutions and subscription pricing models make virtualization increasingly accessible for SMEs. As smaller firms embrace digital transformation and remote working, virtualization adoption is expected to rise significantly, bridging the technology gap between SMEs and large enterprises.

- By Access Mode

On the basis of access mode, the virtual client computing market is segmented into remote access and local access. The remote access segment dominated the market with the largest revenue share of 59.2% in 2024, driven by the global adoption of hybrid work models and the demand for secure access to virtual desktops and applications from any location. Enterprises across industries prioritize remote access solutions to ensure workforce productivity, data security, and flexibility.

Local access is projected to witness the fastest growth from 2025 to 2032, supported by specific use cases in manufacturing plants, education institutions, and localized IT environments where high performance and low latency are critical. As edge computing expands, local access virtualization will play a pivotal role in enabling real-time data processing and localized workload management, particularly in industries requiring instant response and high efficiency.

Virtual Client Computing Market Regional Analysis

- North America dominated the virtual client computing (VCC) market with the largest revenue share of 41.5% in 2024, driven by rapid adoption of cloud technologies, digital workplace transformation, and a strong emphasis on data security

- Enterprises in the region prioritize scalable and secure virtual desktop infrastructure (VDI) and desktop-as-a-service (DaaS) solutions to support hybrid work models and reduce IT complexity. The U.S. leads the region’s growth, benefiting from robust IT investments and early adoption of advanced virtual client computing solutions by industries such as BFSI, healthcare, and government

- High disposable incomes, a mature cloud ecosystem, and a significant presence of key virtual client computing vendors such as VMware, Citrix, and Microsoft further bolster the market. In addition, growing demand for remote access and centralized IT management supports widespread VCC adoption across both large enterprises and SMEs

U.S. Virtual Client Computing Market Insight

The U.S. holds the largest share within North America at 83% in 2024, propelled by extensive cloud adoption and remote workforce expansion. The country’s enterprises rapidly deploy VDI and DaaS platforms to maintain productivity and secure sensitive data amid increasing cyber threats. The proliferation of hybrid work policies, coupled with advancements in AI-powered virtual desktops and zero-trust security frameworks, is accelerating growth. Leading providers continuously innovate to enhance user experience and reduce IT overhead, making the U.S. a key market for virtual client computing technologies.

Europe Virtual Client Computing Market Insight

Europe’s virtual client computing market is expected to grow steadily, supported by stringent data protection regulations such as GDPR and increased digital transformation initiatives across government and private sectors. Countries such as the UK and Germany are notable contributors, driven by investments in cloud infrastructure and secure virtual workplace solutions. The region benefits from a focus on compliance, data sovereignty, and secure remote access, especially in finance, healthcare, and public administration, which increasingly rely on VCC to meet regulatory demands and operational efficiency.

U.K. Virtual Client Computing Market Insight

The U.K. virtual client computing market is projected to witness strong growth due to expanding remote work adoption and government-backed digital modernization programs. Organizations seek to enhance cybersecurity and employee productivity through secure virtual desktop environments. The country’s advanced IT infrastructure and growing cloud services ecosystem facilitate easier VCC implementation. Increasing adoption among SMEs, alongside large enterprises, supports a dynamic market landscape focused on hybrid cloud deployments and cost-effective IT management.

Germany Virtual Client Computing Market Insight

Germany’s virtual client computing market is marked by a strong emphasis on data security, privacy, and regulatory compliance, fueling demand for on-premise and hybrid VCC solutions. The country’s industrial and manufacturing sectors, alongside financial institutions, are key users of VCC technology to maintain operational continuity while safeguarding sensitive data. Germany’s focus on innovation and digital transformation also drives adoption, with growing integration of virtual client computing into smart factory and Industry 4.0 initiatives.

Asia-Pacific Virtual Client Computing Market Insight

The Asia-Pacific region is expected to grow at the fastest CAGR 9.32% from 2025 to 2032, fueled by rapid digitalization, expanding IT infrastructure, and increasing adoption of cloud services in emerging markets such as China, India, Japan, and Australia. Governments’ push for smart city projects and digital workplaces accelerates virtual client computing uptake. Rising demand for secure, flexible remote work solutions and cost-effective IT management drives growth, particularly among SMEs and public sector organizations. The region also benefits from competitive pricing and increasing awareness of VCC advantages.

Japan Virtual Client Computing Market Insight

Japan’s virtual client computing market is growing steadily, supported by the country’s advanced technology ecosystem and focus on workforce productivity. Remote work policies and the need for secure access to corporate applications drive virtual client computing adoption, especially in IT, manufacturing, and healthcare sectors. Integration with AI and automation enhances virtual desktop efficiency, meeting Japan’s high standards for reliability and security. Aging workforce demographics also encourage the adoption of user-friendly, remote desktop technologies.

China Virtual Client Computing Market Insight

China holds the largest market share in Asia-Pacific due to rapid urbanization, growing cloud adoption, and government-led digital transformation initiatives. Enterprises across banking, e-commerce, and education increasingly deploy virtual client computing to enable remote working and enhance data security. The country’s vast IT ecosystem and domestic providers offering affordable VCC solutions contribute to robust market growth. China’s focus on building smart cities and digital government services further accelerates virtual client computing adoption across public and private sectors.

Virtual Client Computing Market Share

Virtual Client Computing Market Leaders Operating in the Market Are:

- VMware, Inc. (U.S.)

- Citrix Systems, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services (AWS) (U.S.)

- Nutanix, Inc. (U.S.)

- Google Cloud (U.S.)

- Dell Technologies (U.S.)

- IBM Corporation (U.S.)

- Parallels, Inc. (U.S.)

- HP Inc. (U.S.)

- Ericom Software (U.S.)

- Centrify Corporation (U.S.)

- IGEL Technology (Germany)

- Rackspace Technology (U.S.)

- Fujitsu Limited (Japan)

Latest Developments in the Global Virtual Client Computing Market

- In April 2023, VMware, a leader in virtualization and cloud infrastructure, launched its VMware Horizon 8 Update to enhance virtual desktop and application delivery with improved performance, security, and cloud integration. This update focuses on supporting hybrid work environments by providing seamless access to virtual desktops across devices, reinforcing VMware’s position as a key innovator in the virtual client computing space.

- In March 2023, Citrix Systems introduced Citrix Workspace Premium, a new service tier offering enhanced AI-driven analytics and automation to optimize virtual desktop experiences and IT management. This development underscores Citrix’s commitment to improving user productivity and security while simplifying IT operations in complex VCC deployments across enterprises worldwide.

- In February 2023, Microsoft expanded its Windows 365 Cloud PC service by integrating advanced endpoint security features and AI-powered performance optimization. These enhancements aim to provide organizations with secure, scalable virtual desktops that support hybrid workforces, emphasizing Microsoft’s strategic focus on cloud-based client computing.

- In January 2023, Amazon Web Services (AWS) announced the launch of Amazon WorkSpaces Web, a cloud-based virtual desktop service designed to simplify secure access to internal applications via browsers without requiring VPNs. This innovation highlights AWS’s drive to provide cost-effective, easy-to-manage VCC solutions for remote and distributed workforces.

- In January 2023, Nutanix unveiled Nutanix Xi Frame V2, an upgraded platform for virtual desktop and app delivery featuring enhanced multi-cloud support and simplified management tools. This release strengthens Nutanix’s presence in the VCC market by enabling enterprises to deploy virtual workspaces flexibly across public and private clouds.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Virtual Client Computing Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Virtual Client Computing Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Virtual Client Computing Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.