Global Vitamin D Testing Market

Market Size in USD Million

USD

950.20 Million

USD

1,447.23 Million

2025

2033

USD

950.20 Million

USD

1,447.23 Million

2025

2033

| 2026 - 2033 | |

| USD 950.20 Million | |

| USD 1,447.23 Million | |

| % | |

|

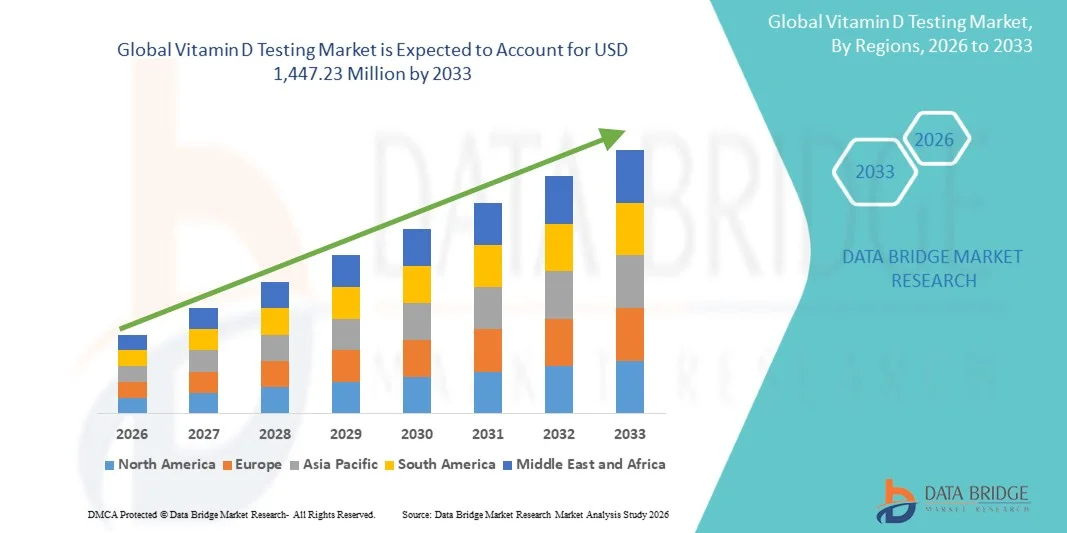

Vitamin D Testing Market Size

- The global Vitamin D testing market size was valued at USD 950.20 million in 2025and is expected to reach USD 1,447.23 million by 2033, at a CAGR of 5.40% during the forecast period

- The market growth is primarily driven by the rising prevalence of vitamin D deficiency across all age groups, coupled with increasing awareness regarding preventive healthcare and the importance of early nutritional assessment in managing chronic diseases and bone health

- Furthermore, growing adoption of advanced diagnostic technologies, expanding routine health screening programs, and increasing demand for accurate laboratory testing solutions are positioning vitamin D testing as an essential component of modern clinical diagnostics. These combined factors are significantly supporting the expansion of the global vitamin D testing industry during the forecast period

Vitamin D Testing Market Analysis

- Vitamin D testing, used to measure vitamin D levels in the body for the diagnosis and monitoring of nutritional deficiencies and related health conditions, is becoming an increasingly important component of preventive healthcare and routine clinical diagnostics due to the growing awareness regarding bone health, immune function, and chronic disease management

- The rising demand for vitamin D testing is primarily driven by the increasing prevalence of vitamin D deficiency worldwide, growing geriatric population, and expanding adoption of preventive health screening programs among healthcare providers and consumers

- North America dominated the vitamin D testing market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, high awareness regarding nutritional deficiencies, and strong adoption of routine diagnostic testing, with the U.S. witnessing substantial demand due to increasing cases of osteoporosis, obesity, and chronic disorders requiring regular vitamin D assessment

- Asia-Pacific is expected to be the fastest growing region in the vitamin D testing market during the forecast period due to improving healthcare access, rising health awareness, and increasing government initiatives promoting preventive diagnostics and wellness monitoring

- 25 -Hydroxy Vitamin D Testing segment dominated the vitamin D testing market with a market share of 46.3% in 2025, driven by its widespread clinical use as the standard and most accurate method for evaluating overall vitamin D status in patients

Report Scope and Vitamin D Testing Market Segmentation

|

Attributes |

Vitamin D Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· The growing integration of vitamin D testing into personalized nutrition and preventive healthcare programs · Increasing adoption of at-home sample collection kits and digital health platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Vitamin D Testing Market Trends

“Rising Adoption of Preventive Healthcare and At-Home Testing Solutions”

- A significant and accelerating trend in the global vitamin D testing market is the increasing adoption of preventive healthcare practices and the growing availability of convenient at-home vitamin D testing solutions. This combination of trends is significantly improving early deficiency detection and consumer engagement in personal health management

- For instance, Everlywell and LetsGetChecked offer at-home vitamin D testing kits that enable consumers to collect samples conveniently and access digital results remotely. Similarly, Quest Diagnostics and Labcorp continue expanding preventive wellness testing panels that include vitamin D assessment services

- The integration of advanced diagnostic technologies in vitamin D testing enables faster turnaround times, improved test accuracy, and streamlined laboratory workflows. For instance, automated immunoassay analyzers and LC-MS/MS systems are increasingly being utilized to enhance precision and support high-volume vitamin D testing across healthcare facilities. Furthermore, digital health platforms provide users with convenient access to reports, physician consultations, and long-term wellness monitoring services

- The seamless incorporation of vitamin D testing into routine health checkups and preventive screening programs facilitates broader patient access to nutritional assessment services. Through integrated healthcare systems, providers can monitor vitamin D levels alongside other biomarkers, supporting comprehensive disease prevention and personalized treatment planning

- This trend toward more accessible, accurate, and consumer-focused diagnostic services is fundamentally reshaping expectations for preventive healthcare testing. Consequently, companies such as Roche are developing advanced automated vitamin D assays designed to improve efficiency, scalability, and clinical reliability across laboratories and healthcare institutions

- The growing use of artificial intelligence and data analytics in diagnostic laboratories is further enhancing vitamin D testing efficiency by supporting automated result interpretation, predictive health assessments, and optimized patient management strategies across healthcare systems

- The demand for vitamin D testing solutions that offer convenience, rapid results, and integration with preventive healthcare services is growing rapidly across hospitals, diagnostic laboratories, and home healthcare settings, as consumers increasingly prioritize proactive wellness management and early disease prevention

Vitamin D Testing Market Dynamics

Driver

“Increasing Prevalence of Vitamin D Deficiency and Preventive Health Awareness”

- The rising prevalence of vitamin D deficiency among all age groups, coupled with increasing awareness regarding preventive healthcare and nutritional monitoring, is a significant driver for the heightened demand for vitamin D testing services

- For instance, in March 2025, Quest Diagnostics announced the expansion of its preventive wellness testing portfolio, including enhanced vitamin deficiency screening services aimed at supporting early diagnosis and chronic disease management. Such strategies by key companies are expected to drive the vitamin D testing industry growth in the forecast period

- As healthcare providers and consumers become more focused on early disease detection and preventive care, vitamin D testing offers critical insights for managing conditions such as osteoporosis, immune disorders, and cardiovascular diseases, making it an essential diagnostic tool in modern healthcare practices

- Furthermore, the growing adoption of routine health screening programs and personalized healthcare approaches is increasing the integration of vitamin D testing into standard wellness assessments, enabling healthcare professionals to provide targeted nutritional and therapeutic interventions

- The convenience of advanced automated testing systems, expanding availability of at-home sample collection kits, and increasing access to digital health platforms are key factors propelling the adoption of vitamin D testing across hospitals, diagnostic laboratories, and home healthcare settings. The trend toward preventive healthcare monitoring and rising awareness campaigns regarding nutritional deficiencies further contribute to market growth

- Increasing government initiatives promoting nutritional deficiency screening and chronic disease prevention programs are further supporting the adoption of vitamin D testing services across public healthcare systems and community wellness programs

- The expanding geriatric population, which is more vulnerable to osteoporosis, bone disorders, and vitamin deficiencies, is also contributing significantly to the growing demand for routine vitamin D monitoring and diagnostic testing services worldwide

Restraint/Challenge

“High Testing Costs and Limited Awareness in Developing Regions”

- Concerns surrounding the relatively high cost of advanced vitamin D testing procedures and limited awareness regarding nutritional deficiency screening in certain developing regions pose a significant challenge to broader market expansion. As advanced testing technologies require sophisticated laboratory infrastructure and skilled professionals, affordability and accessibility remain key concerns among underserved populations

- For instance, inadequate healthcare infrastructure and limited reimbursement support for preventive diagnostic testing in several low- and middle-income countries have restricted the widespread adoption of vitamin D testing services

- Addressing these accessibility concerns through affordable diagnostic solutions, expanded reimbursement coverage, and public health awareness initiatives is crucial for improving patient adoption rates. Companies such as Abbott and Siemens Healthineers continue emphasizing automated and cost-efficient testing systems to improve operational efficiency and reduce laboratory costs. In addition, variability in testing standards and inconsistencies in result interpretation across laboratories can create challenges for clinicians and healthcare providers seeking standardized diagnostic outcomes

- While technological advancements are gradually improving affordability and testing accuracy, the perceived non-essential nature of routine vitamin D screening among certain patient groups can still hinder broader adoption, particularly in cost-sensitive healthcare markets or regions with limited preventive healthcare infrastructure

- Overcoming these challenges through enhanced healthcare awareness initiatives, improved access to affordable diagnostic services, and the development of standardized testing protocols will be vital for sustaining long-term market growth

- Limited availability of advanced diagnostic laboratories and trained healthcare professionals in rural and underserved regions further restricts timely access to accurate vitamin D testing and preventive healthcare services

- Variations in regulatory guidelines and clinical recommendations regarding routine vitamin D screening across different countries may also create inconsistencies in testing adoption and reimbursement policies, thereby impacting overall market expansion

Vitamin D Testing Market Scope

The market is segmented on the basis of product, application, technique, patient, indication, and end user.

- By Product

On the basis of product, the vitamin D testing market is segmented into 25-Hydroxy Vitamin D Testing, 1,25-Dihydroxy Vitamin D Testing, and 24,25-Dihydroxy Vitamin D Testing. The 25-Hydroxy Vitamin D Testing segment dominated the market with the largest market revenue share of 46.3% in 2025, driven by its widespread clinical adoption as the standard diagnostic method for evaluating overall vitamin D status in patients. Healthcare providers commonly prefer this test due to its high reliability, clinical accuracy, and ability to detect vitamin D deficiencies effectively. The growing prevalence of osteoporosis, bone disorders, and chronic diseases has significantly increased demand for routine 25-hydroxy vitamin D testing across hospitals and diagnostic laboratories. In addition, increasing awareness regarding preventive healthcare and nutritional monitoring continues to support the segment’s expansion globally. The availability of automated analyzers and standardized testing procedures further strengthens the dominance of this segment in the global market.

The 1,25-Dihydroxy Vitamin D Testing segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing use in specialized clinical investigations related to kidney disorders, endocrine abnormalities, and metabolic bone diseases. This test plays a critical role in evaluating active vitamin D hormone levels in patients with complex medical conditions requiring advanced diagnostic assessment. Growing advancements in laboratory technologies and rising adoption of personalized medicine approaches are supporting the demand for specialized vitamin D testing solutions. Furthermore, increasing research activities related to chronic kidney disease and parathyroid disorders are contributing to segment growth. Expanding healthcare infrastructure and rising awareness regarding advanced diagnostic testing are also expected to accelerate adoption rates during the forecast period.

- By Application

On the basis of application, the vitamin D testing market is segmented into clinical testing and research testing. The Clinical Testing segment dominated the market with the largest market revenue share in 2025, driven by the growing number of routine health screenings and increasing prevalence of vitamin D deficiency worldwide. Hospitals, diagnostic laboratories, and healthcare providers widely utilize clinical vitamin D testing for diagnosing osteoporosis, immune disorders, and nutritional deficiencies. Rising patient awareness regarding preventive healthcare and chronic disease management continues to support strong demand for clinical testing services. In addition, increasing physician recommendations for regular vitamin D assessment among geriatric and at-risk populations further strengthen segment growth. The expansion of automated laboratory systems and standardized testing protocols also contributes significantly to the segment’s market leadership.

The Research Testing segment is expected to witness the fastest CAGR from 2026 to 2033, driven by growing scientific research focused on the relationship between vitamin D levels and chronic diseases such as cancer, diabetes, and cardiovascular disorders. Academic institutions, biotechnology companies, and pharmaceutical organizations are increasingly investing in vitamin D-related clinical studies and biomarker research activities. The rising emphasis on precision medicine and nutritional genomics is further supporting demand for research-based vitamin D testing solutions. Furthermore, technological advancements in analytical instruments and biomarker analysis methods are enhancing research capabilities across healthcare institutions. Increasing government and private funding for healthcare research programs is also anticipated to accelerate segment growth during the forecast period.

- By Technique

On the basis of technique, the vitamin D testing market is segmented into Radioimmunoassay, ELISA, HPLC, LC-MS, and Others. The ELISA segment dominated the market with the largest market revenue share in 2025, driven by its cost-effectiveness, high sensitivity, and widespread adoption across diagnostic laboratories and healthcare facilities. ELISA-based vitamin D testing methods are commonly preferred due to their ability to process large sample volumes efficiently while maintaining reliable diagnostic accuracy. The growing demand for automated and high-throughput laboratory testing solutions continues to support segment growth globally. In addition, increasing prevalence of vitamin D deficiency and expansion of preventive healthcare programs are fueling adoption of ELISA testing techniques. The ease of implementation and compatibility with routine clinical workflows further strengthen the segment’s dominance in the market.

The LC-MS segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its superior analytical accuracy, specificity, and capability to simultaneously measure multiple vitamin D metabolites. Healthcare providers and research institutions are increasingly adopting LC-MS techniques for advanced clinical diagnostics and specialized testing applications. Rising demand for precise biomarker analysis and personalized treatment approaches is significantly contributing to segment expansion. Furthermore, technological advancements in mass spectrometry instruments and laboratory automation systems are improving operational efficiency and testing reliability. Growing investments in advanced diagnostic infrastructure and research laboratories are also expected to drive rapid adoption of LC-MS techniques during the forecast period.

- By Patient

On the basis of patient, the vitamin D testing market is segmented into adult and paediatric. The Adult segment dominated the market with the largest market revenue share in 2025, driven by the high prevalence of vitamin D deficiency, osteoporosis, and chronic disorders among the adult and geriatric populations. Adults frequently undergo vitamin D testing as part of routine preventive healthcare assessments and chronic disease monitoring programs. Increasing awareness regarding bone health, immune support, and nutritional wellness continues to support strong testing demand within this patient group. In addition, sedentary lifestyles, limited sun exposure, and changing dietary habits are contributing to rising vitamin D deficiency rates among adults globally. The growing adoption of preventive diagnostics and wellness screening services further strengthens segment growth across healthcare facilities.

The Paediatric segment is expected to witness the fastest CAGR from 2026 to 2033, driven by rising awareness regarding childhood nutritional deficiencies and increasing focus on early disease prevention. Healthcare providers are increasingly recommending vitamin D testing for infants and children to support healthy bone development and immune function. The growing prevalence of pediatric rickets and malnutrition in developing regions is further contributing to segment expansion. Furthermore, increasing government healthcare initiatives promoting maternal and child nutrition are supporting adoption of pediatric vitamin D screening services. Expanding pediatric healthcare infrastructure and rising parental awareness regarding preventive healthcare are also expected to accelerate growth during the forecast period.

- By Indication

On the basis of indication, the vitamin D testing market is segmented into osteoporosis, rickets, thyroid disorders, malabsorption, vitamin d deficiency, and others. The Vitamin D Deficiency segment dominated the market with the largest market revenue share in 2025, driven by the growing global burden of nutritional deficiencies and increasing awareness regarding preventive health screening. Vitamin D deficiency testing is widely utilized across hospitals, diagnostic laboratories, and wellness clinics for routine health assessments and chronic disease prevention programs. Rising prevalence of sedentary lifestyles, inadequate dietary intake, and limited sunlight exposure continue to increase testing demand worldwide. In addition, growing physician recommendations for routine nutritional monitoring among at-risk populations further support segment dominance. Expanding healthcare access and increasing awareness campaigns regarding vitamin deficiency management also contribute significantly to market growth.

The Osteoporosis segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising geriatric population and increasing incidence of bone-related disorders globally. Healthcare professionals frequently recommend vitamin D testing as part of osteoporosis diagnosis, treatment monitoring, and fracture prevention strategies. The growing focus on healthy aging and preventive bone healthcare is significantly contributing to demand for osteoporosis-related vitamin D testing services. Furthermore, increasing adoption of advanced diagnostic screening programs for postmenopausal women and elderly patients is supporting segment expansion. Rising healthcare expenditures and expanding awareness regarding bone health management are also expected to accelerate growth during the forecast period.

- By End User

On the basis of end user, the vitamin D testing market is segmented into hospitals, diagnostic laboratories, home care, point-of-care, and others. The Diagnostic Laboratories segment dominated the market with the largest market revenue share in 2025, driven by the increasing volume of routine vitamin D screening procedures and widespread availability of advanced laboratory testing infrastructure. Diagnostic laboratories are highly preferred for vitamin D testing due to their ability to deliver accurate results, high sample processing capacity, and access to automated analytical technologies. The growing prevalence of chronic diseases and preventive health screening programs continues to support rising patient testing volumes globally. In addition, strong collaborations between healthcare providers and laboratory service organizations further strengthen segment growth. The expansion of centralized laboratory networks and digital diagnostic platforms also contributes significantly to the dominance of this segment.

The Point-of-Care segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing demand for rapid diagnostic solutions and decentralized healthcare services. Point-of-care vitamin D testing enables faster clinical decision-making and improved patient convenience through near-patient testing capabilities. Healthcare providers are increasingly adopting portable diagnostic devices to support immediate nutritional assessment in outpatient settings and remote healthcare environments. Furthermore, technological advancements in compact testing devices and digital healthcare integration are improving testing accessibility and operational efficiency. Rising adoption of home healthcare services and growing emphasis on personalized preventive care are also expected to accelerate segment growth during the forecast period.

Vitamin D Testing Market Regional Analysis

- North America dominated the vitamin D testing market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, high awareness regarding nutritional deficiencies, and strong adoption of routine diagnostic testing

- Patients and healthcare providers in the region highly value the accuracy, convenience, and clinical reliability offered by advanced vitamin D testing solutions integrated with modern diagnostic laboratory systems and preventive healthcare programs

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, and the growing preference for early disease detection and wellness monitoring, establishing vitamin D testing as an essential component of preventive diagnostics across hospitals, laboratories, and home healthcare settings

U.S. Vitamin D Testing Market Insight

The U.S. vitamin D testing market captured the largest revenue share of 79% in 2025 within North America, fueled by the growing prevalence of vitamin D deficiency and the increasing focus on preventive healthcare and wellness monitoring. Patients and healthcare providers are increasingly prioritizing routine nutritional screening and early diagnosis of chronic conditions through advanced laboratory testing services. The growing adoption of preventive health checkups, combined with strong demand for accurate and automated diagnostic solutions, further propels the vitamin D testing industry. Moreover, the increasing integration of digital healthcare platforms, at-home testing services, and personalized wellness programs is significantly contributing to the market's expansion.

Europe Vitamin D Testing Market Insight

The Europe vitamin D testing market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness regarding bone health and the increasing burden of nutritional deficiencies across the region. The growth in preventive healthcare initiatives, coupled with the demand for advanced diagnostic services, is fostering the adoption of vitamin D testing. European consumers are also increasingly focused on wellness management and early disease prevention through routine health screening programs. The region is experiencing significant growth across hospitals, diagnostic laboratories, and home healthcare applications, with vitamin D testing being incorporated into both routine clinical assessments and specialized disease management programs.

U.K. Vitamin D Testing Market Insight

The U.K. vitamin D testing market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness regarding vitamin deficiency-related disorders and a rising emphasis on preventive healthcare services. In addition, growing concerns regarding osteoporosis, immune health, and chronic disease management are encouraging both patients and healthcare providers to adopt routine vitamin D screening solutions. The U.K.’s expanding digital healthcare infrastructure, alongside its strong diagnostic laboratory network and healthcare accessibility, is expected to continue to stimulate market growth.

Germany Vitamin D Testing Market Insight

The Germany vitamin D testing market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of nutritional health and the demand for technologically advanced diagnostic solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on clinical accuracy and preventive care, promotes the adoption of vitamin D testing, particularly across hospitals and specialized diagnostic laboratories. The integration of advanced automated testing systems within healthcare facilities is also becoming increasingly prevalent, with a strong preference for reliable and standardized diagnostic services aligning with local healthcare expectations.

Asia-Pacific Vitamin D Testing Market Insight

The Asia-Pacific vitamin D testing market is poised to grow at the fastest CAGR of 22.8% during the forecast period of 2026 to 2033, driven by increasing healthcare awareness, rising disposable incomes, and expanding access to diagnostic services in countries such as China, Japan, and India. The region's growing focus on preventive healthcare, supported by government initiatives promoting nutritional health and disease prevention, is driving the adoption of vitamin D testing services. Furthermore, as APAC emerges as a rapidly expanding healthcare and diagnostic services market, the affordability and accessibility of vitamin D testing solutions are increasing across a broader patient population.

Japan Vitamin D Testing Market Insight

The Japan vitamin D testing market is gaining momentum due to the country’s advanced healthcare infrastructure, aging population, and growing demand for preventive wellness monitoring. The Japanese market places a significant emphasis on healthy aging and chronic disease prevention, and the adoption of vitamin D testing is driven by the increasing prevalence of osteoporosis and nutritional deficiencies among elderly populations. The integration of vitamin D testing with routine health screening programs and advanced laboratory technologies is fueling growth. Moreover, Japan's increasing focus on personalized healthcare and nutritional management is likely to spur demand for accurate and convenient vitamin D testing services across healthcare institutions and wellness centers.

India Vitamin D Testing Market Insight

The India vitamin D testing market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's large population base, rising awareness regarding nutritional deficiencies, and rapidly expanding healthcare infrastructure. India stands as one of the fastest growing markets for preventive diagnostics, and vitamin D testing is becoming increasingly popular across hospitals, diagnostic laboratories, and wellness clinics. The growing focus on preventive healthcare programs and increasing availability of affordable diagnostic services, alongside strong expansion of organized laboratory networks, are key factors propelling the market in India.

Vitamin D Testing Market Share

The Vitamin D Testing industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Danaher (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- Quest Diagnostics Incorporated (U.S.)

- BIOMÉRIEUX (France)

- DiaSorin S.p.A. (Italy)

- Thermo Fisher Scientific Inc. (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Tosoh Corporation (Japan)

- Bio-Rad Laboratories, Inc. (U.S.)

- Randox Laboratories Ltd. (U.K.)

- EUROIMMUN Medizinische Labordiagnostika AG (Germany)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- NanoEnTek Inc. (South Korea)

- Qualigen Therapeutics, Inc. (U.S.)

- DIAsource ImmunoAssays SA (Belgium)

- Gold Standard Diagnostics Corporation (U.S.)

- OmegaQuant Analytics, LLC (U.S.)

- SpectraCell Laboratories, Inc. (U.S.)

What are the Recent Developments in Global Vitamin D Testing Market?

- In September 2025, Roche Diagnostics announced that its Ionify® 25-Hydroxy Vitamin D total assay became the first mass spectrometry-based vitamin D test to receive CLIA “Moderate Complexity” categorization in the U.S. The development expands access to advanced vitamin D testing for a broader range of clinical laboratories through Roche’s automated cobas® Mass Spec solution. The launch highlights the growing adoption of highly standardized and automated vitamin D diagnostic technologies across healthcare facilities

- In February 2025, Technavio highlighted the increasing integration of AI-driven technologies in the vitamin D testing market, emphasizing the growing role of advanced analytics and automation in improving testing efficiency and diagnostic workflows. The report also noted rising awareness regarding vitamin D’s role in immunity and chronic disease prevention as a major factor accelerating demand for testing services globally

- In December 2024, Technavio reported significant advancements in AI-powered vitamin D testing market evolution, with increasing adoption of automated laboratory systems and digital diagnostic solutions across hospitals and diagnostic laboratories. The report emphasized that growing technological innovation is improving testing accessibility and operational efficiency within preventive healthcare services

- In February 2023, Hurdle Health announced the launch of its at-home Vitamin D Test, designed to provide consumers with lab-quality vitamin D results from the comfort of their homes. The new solution was introduced to improve accessibility to nutritional deficiency testing and support preventive healthcare initiatives through convenient remote diagnostic services. This launch reflects the increasing consumer demand for home-based wellness and vitamin deficiency testing solutions

- In April 2022, Medisure Canada Inc. announced the launch of its Health Canada-approved at-home vitamin D testing kit, enabling consumers to monitor vitamin D deficiency through self-testing solutions. The company reported strong early demand from pharmacies and online distribution channels, highlighting the expanding adoption of convenient home healthcare diagnostics and preventive wellness testing services

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.