Global Vitreoretinal Disorders Market

Market Size in USD Billion

USD

2.17 Billion

USD

4.01 Billion

2025

2033

USD

2.17 Billion

USD

4.01 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.17 Billion | |

| USD 4.01 Billion | |

| % | |

|

Vitreoretinal Disorders Market Size

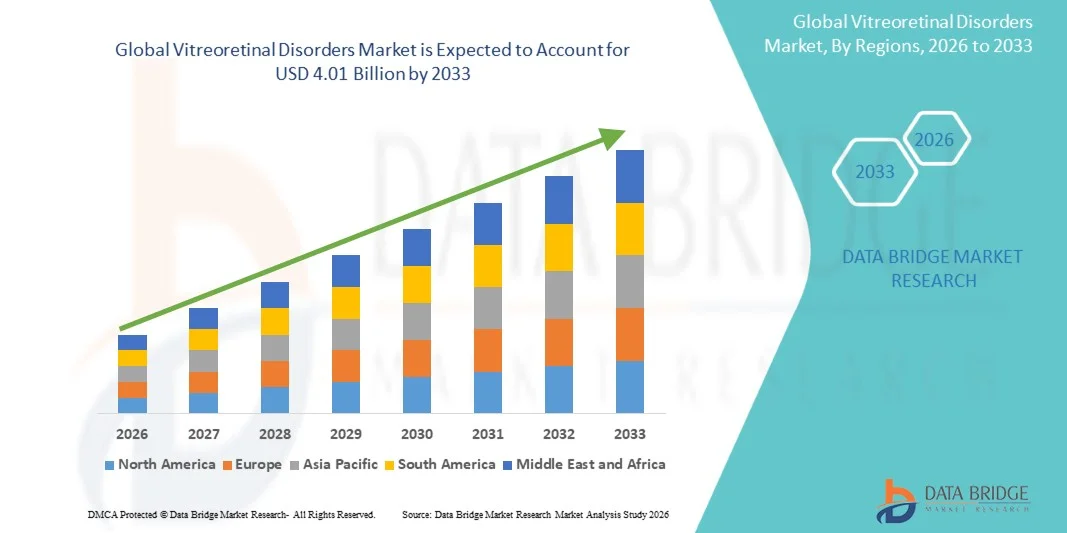

- The global vitreoretinal disorders market size was valued at USD 2.17 billion in 2025 and is expected to reach USD 4.01 billion by 2033, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the rising prevalence of retinal diseases such as diabetic retinopathy, age-related macular degeneration, and retinal vein occlusion, along with the increasing aging population worldwide, leading to greater demand for advanced ophthalmic treatments

- Furthermore, growing advancements in diagnostic imaging technologies, minimally invasive surgical procedures, and targeted drug therapies are driving improved patient outcomes, thereby establishing vitreoretinal treatments as a critical component of modern ophthalmic care and significantly boosting the market’s growth

Vitreoretinal Disorders Market Analysis

- Vitreoretinal disorders, encompassing a range of conditions affecting the retina and vitreous body such as diabetic retinopathy, macular degeneration, retinal detachment, and macular hole, are increasingly critical areas within ophthalmology due to their significant impact on vision and the growing need for timely diagnosis and treatment across both hospital and specialty eye care settings

- The escalating demand for vitreoretinal treatments is primarily fueled by the rising global burden of diabetes, increasing geriatric population, and heightened awareness regarding early eye disease detection, along with continuous advancements in retinal imaging technologies such as optical coherence tomography and angiography techniques

- North America dominated the vitreoretinal disorders market with the largest revenue share of 40.01% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative diagnostic modalities, and a strong presence of leading ophthalmic companies, with the U.S. witnessing significant growth in retinal procedures supported by favorable reimbursement policies and technological innovations

- Asia-Pacific is expected to be the fastest growing region in the vitreoretinal disorders market during the forecast period due to increasing healthcare expenditure, expanding access to eye care services, and a rapidly growing diabetic population

- Diabetic retinopathy segment dominated the vitreoretinal disorders market with a market share of 43.2% in 2025, driven by its high global prevalence, strong association with rising diabetes cases, and increasing demand for both diagnostic and therapeutic interventions

Report Scope and Vitreoretinal Disorders Market Segmentation

|

Attributes |

Vitreoretinal Disorders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Vitreoretinal Disorders Market Trends

“Advancements in Retinal Imaging and Targeted Therapies”

- A significant and accelerating trend in the global vitreoretinal disorders market is the increasing adoption of advanced diagnostic imaging technologies and targeted treatment approaches for conditions such as Diabetic Retinopathy and Macular Degeneration. This integration of technologies is significantly enhancing early detection and treatment precision

- For instance, optical coherence tomography (OCT) systems and fundus imaging devices are widely used for high-resolution retinal assessment, enabling clinicians to diagnose diseases at earlier stages and monitor disease progression more effectively. Similarly, advanced angiography techniques provide detailed visualization of retinal vasculature, supporting improved clinical decision-making

- Technological advancements in vitreoretinal care enable features such as real-time imaging, minimally invasive surgical guidance, and personalized treatment planning based on disease severity. For instance, some modern imaging platforms incorporate AI to assist in identifying retinal abnormalities and predicting disease progression, thereby enhancing diagnostic accuracy and efficiency. Furthermore, targeted drug delivery systems offer improved therapeutic outcomes with reduced treatment burden for patients

- The seamless integration of diagnostic tools with treatment planning systems facilitates a more coordinated approach to patient care. Through unified ophthalmic platforms, clinicians can manage diagnosis, treatment, and follow-up within a single ecosystem, improving workflow efficiency and patient outcomes

- This trend towards more precise, efficient, and technology-driven retinal care is fundamentally reshaping clinical practices in ophthalmology. Consequently, companies are developing advanced imaging systems and therapeutic solutions with enhanced accuracy, automation, and patient-centric features

- The demand for advanced vitreoretinal diagnostic and treatment solutions is growing rapidly across both developed and emerging healthcare markets, as providers increasingly prioritize early detection and improved management of retinal disorders

- The growing adoption of teleophthalmology and remote retinal screening programs is expanding access to eye care services, particularly in underserved and rural regions, thereby supporting early diagnosis and intervention

Vitreoretinal Disorders Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Retinal Diseases and Aging Population”

- The increasing prevalence of retinal disorders and the rapidly growing aging population are significant drivers for the heightened demand for vitreoretinal treatments and diagnostic solutions

- For instance, in March 2025, leading ophthalmic companies introduced next-generation retinal imaging devices and therapeutic solutions aimed at improving early diagnosis and treatment outcomes for patients with chronic retinal conditions. Such strategies by key companies are expected to drive the vitreoretinal disorders market growth in the forecast period

- As the global burden of diabetes and age-related eye diseases rises, patients are increasingly seeking early diagnosis and effective treatment options, creating strong demand for advanced vitreoretinal care

- Furthermore, the growing awareness regarding vision health and the importance of regular eye examinations are encouraging early detection and timely intervention, thereby improving clinical outcomes

- The availability of advanced treatment options, including minimally invasive surgeries and pharmacological therapies, along with improved access to ophthalmic care services, are key factors propelling the adoption of vitreoretinal solutions across healthcare settings. The expansion of specialized eye care centers and increasing investment in healthcare infrastructure further contribute to market growth

- Government initiatives and public health programs aimed at reducing vision impairment and blindness are further accelerating the adoption of screening and treatment services

- Increasing collaborations between research institutions and pharmaceutical companies are fostering innovation and accelerating the development of novel therapies for retinal diseases

Restraint/Challenge

“High Treatment Costs and Limited Access to Advanced Care”

- The high cost associated with advanced diagnostic imaging systems, surgical procedures, and long-term treatment regimens poses a significant challenge to the widespread adoption of vitreoretinal care solutions

- For instance, the cost of repeated intravitreal injections and advanced imaging procedures can be substantial, limiting accessibility for patients in low- and middle-income regions

- Addressing these cost-related challenges is crucial for improving patient access to care. Healthcare providers and companies are focusing on developing cost-effective solutions and expanding reimbursement coverage to reduce the financial burden on patients. In addition, limited availability of specialized ophthalmologists and advanced healthcare facilities in rural or underserved areas further restricts access to timely diagnosis and treatment

- While advancements in technology continue to improve treatment outcomes, disparities in healthcare infrastructure and affordability remain key barriers to market growth

- The complexity of treatment regimens, including frequent follow-ups and long-term therapy adherence, can lead to patient non-compliance and suboptimal outcomes

- Regulatory challenges and lengthy approval timelines for advanced therapies, including biologics and gene therapies, can delay market entry and limit the availability of innovative treatment options

- Overcoming these challenges through increased healthcare investment, improved insurance coverage, and the development of affordable diagnostic and treatment options will be vital for sustained market expansion

Vitreoretinal Disorders Market Scope

The market is segmented on the basis of type, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the vitreoretinal disorders market is segmented into retinal tear, retinal detachment, Diabetic Retinopathy, Macular Degeneration, macular hole, and others. The diabetic retinopathy segment dominated the market with the largest market revenue share of 43.2% in 2025, driven by its strong association with the rising global prevalence of diabetes and increasing screening initiatives for early detection. The condition requires continuous monitoring and long-term management, leading to sustained demand for diagnostic and therapeutic solutions. In addition, growing awareness regarding diabetic eye complications and improved access to ophthalmic care further contribute to segment dominance. The availability of multiple treatment options, including medications and surgical interventions, also supports its high market share. Increasing healthcare investments and government-led screening programs are further strengthening this segment’s position.

The macular degeneration segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rapidly aging global population and increasing life expectancy. Age-related macular degeneration is a leading cause of vision loss among elderly individuals, significantly driving demand for advanced therapies and diagnostic tools. Continuous advancements in imaging technologies and targeted treatments are enhancing disease management outcomes. Furthermore, rising awareness and early diagnosis initiatives are accelerating patient inflow for treatment. The development of novel therapies and ongoing clinical research are also contributing to the rapid expansion of this segment.

- By Diagnosis

On the basis of diagnosis, the vitreoretinal disorders market is segmented into digital fluorescein angiography, optical coherence tomography, Heidelberg retinal tomography, indocyanine green angiography, and others. The optical coherence tomography segment dominated the market with the largest market revenue share in 2025, driven by its high-resolution imaging capabilities and non-invasive nature. OCT is widely adopted for early detection, diagnosis, and monitoring of various retinal conditions, making it a standard tool in ophthalmology practices. Its ability to provide real-time cross-sectional images of the retina significantly improves diagnostic accuracy. The growing availability of advanced OCT devices and integration with AI-based analytics further strengthen its dominance. Increasing investments in ophthalmic diagnostic infrastructure also contribute to its widespread use.

The indocyanine green angiography segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its superior capability in visualizing deeper retinal and choroidal blood vessels. This technique is increasingly used in complex retinal disease diagnosis where conventional imaging methods may be insufficient. Growing demand for precise and detailed vascular imaging is accelerating its adoption. Technological advancements and improved imaging systems are enhancing its clinical utility. In addition, rising cases of retinal vascular disorders are further supporting the growth of this segment.

- By Treatment

On the basis of treatment, the vitreoretinal disorders market is segmented into surgery, medication, and others. The medication segment dominated the market with the largest market revenue share in 2025, driven by the widespread use of pharmacological therapies for managing chronic retinal conditions. Medications offer less invasive treatment options and are often preferred for long-term disease management. The increasing availability of targeted therapies and sustained-release drug formulations is enhancing treatment effectiveness. In addition, the rising number of patients requiring ongoing therapy contributes to consistent demand. Improved patient compliance and advancements in drug delivery systems further support segment growth.

The surgery segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by advancements in minimally invasive vitreoretinal surgical techniques. Surgical interventions are increasingly required for severe conditions such as retinal detachment and macular hole. Technological innovations in surgical equipment and improved success rates are encouraging adoption. The growing number of specialized ophthalmic centers is also supporting procedural volumes. Furthermore, increasing awareness and accessibility to surgical treatments are driving rapid growth in this segment.

- By Route of Administration

On the basis of route of administration, the vitreoretinal disorders market is segmented into oral, parenteral, ocular, and others. The ocular segment dominated the market with the largest market revenue share in 2025, driven by its direct delivery of drugs to the eye, ensuring higher efficacy and targeted treatment. Ocular administration methods, such as intravitreal injections, are widely used for managing retinal disorders. These approaches minimize systemic side effects while maximizing therapeutic outcomes. Increasing adoption of advanced ocular drug delivery systems is further supporting this segment. The rising prevalence of chronic retinal diseases also contributes to its dominance.

The parenteral segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the growing use of injectable therapies for effective disease management. Parenteral administration ensures rapid drug action and precise dosing, making it suitable for severe retinal conditions. Advancements in biologics and injectable formulations are boosting segment growth. In addition, increasing clinical adoption of injectable treatments is further supporting demand. The expansion of healthcare infrastructure and treatment accessibility also contributes to its rapid growth.

- By End-Users

On the basis of end-users, the vitreoretinal disorders market is segmented into hospitals, specialty clinics, and others. The hospitals segment dominated the market with the largest market revenue share in 2025, driven by the availability of advanced diagnostic and surgical facilities. Hospitals serve as primary centers for complex retinal procedures and comprehensive patient care. The presence of skilled ophthalmologists and access to cutting-edge technologies further strengthen this segment. Increasing patient inflow for diagnosis and treatment also contributes to its dominance. Government support and healthcare investments are enhancing hospital capabilities.

The specialty clinics segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising number of dedicated eye care centers. These clinics offer focused and efficient ophthalmic services, attracting a growing patient base. Shorter waiting times and personalized care are key factors driving their popularity. Increasing investments in specialized eye care infrastructure are supporting segment expansion. Furthermore, the growing trend toward outpatient care is accelerating the adoption of specialty clinics.

- By Distribution Channel

On the basis of distribution channel, the vitreoretinal disorders market is segmented into hospital pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated the market with the largest market revenue share in 2025, driven by the high volume of prescriptions generated within hospital settings. Hospital pharmacies ensure the availability of specialized medications required for retinal treatments. The integration of pharmacy services within hospitals enhances patient convenience and treatment adherence. Increasing hospitalization rates for retinal conditions further support this segment. In addition, strong supply chain networks in hospitals contribute to its dominance.

The retail pharmacy segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing accessibility and convenience for patients requiring ongoing medication. Retail pharmacies play a crucial role in dispensing maintenance therapies and follow-up prescriptions. The expansion of pharmacy networks and improved availability of ophthalmic drugs are boosting segment growth. Rising patient preference for easily accessible healthcare services further supports this trend. In addition, the growth of e-pharmacy platforms is enhancing the reach of retail distribution channels.

Vitreoretinal Disorders Market Regional Analysis

- North America dominated the vitreoretinal disorders market with the largest revenue share of 40.01% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative diagnostic modalities, and a strong presence of leading ophthalmic companies

- Patients and healthcare providers in the region highly value advanced diagnostic imaging technologies, specialized retinal treatments, and well-established ophthalmology infrastructure, which enable effective disease management and improved visual outcomes

- This widespread adoption is further supported by high healthcare expenditure, strong insurance coverage, and a technologically advanced medical ecosystem, along with the presence of leading ophthalmic companies and continuous innovation in retinal therapies, establishing the region as a key hub for vitreoretinal disorder management

U.S. Vitreoretinal Disorders Market Insight

The U.S. vitreoretinal disorders market captured the largest revenue share of 81% in North America in 2025, fueled by the high prevalence of retinal diseases such as Diabetic Retinopathy and Age-related Macular Degeneration, along with strong adoption of advanced ophthalmic diagnostic and treatment solutions. Consumers are increasingly prioritizing early detection and effective management of vision-threatening conditions through advanced retinal imaging and therapeutic interventions. The growing preference for technologically advanced ophthalmic care, combined with robust demand for minimally invasive procedures and innovative biologics, further propels the market. Moreover, the increasing integration of technologies such as optical coherence tomography and anti-VEGF therapies is significantly contributing to market expansion.

Europe Vitreoretinal Disorders Market Insight

The Europe vitreoretinal disorders market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising aging population, increasing burden of retinal diseases, and growing demand for early diagnosis and preventive eye care. The increase in urbanization, coupled with the demand for advanced ophthalmic services, is fostering the adoption of vitreoretinal treatments and diagnostic technologies. European patients are also drawn to the effectiveness and precision offered by modern retinal imaging systems and minimally invasive procedures. The region is experiencing significant growth across hospitals and specialty eye clinics, with advanced diagnostic tools and therapies being incorporated into both new and existing healthcare infrastructures.

U.K. Vitreoretinal Disorders Market Insight

The U.K. vitreoretinal disorders market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating prevalence of diabetes-related retinal complications and a strong focus on early diagnosis and treatment. In addition, concerns regarding vision loss and increasing awareness of eye health are encouraging patients and healthcare providers to opt for advanced retinal care solutions. The UK’s robust public healthcare system and expanding ophthalmology services are expected to continue to stimulate market growth.

Germany Vitreoretinal Disorders Market Insight

The Germany vitreoretinal disorders market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of retinal diseases and demand for advanced, technology-driven ophthalmic solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on medical innovation and precision diagnostics, promotes the adoption of vitreoretinal treatments. The integration of retinal imaging technologies with hospital systems is also becoming increasingly prevalent, with a strong preference for high-quality, patient-centric eye care solutions aligning with local healthcare expectations.

Asia-Pacific Vitreoretinal Disorders Market Insight

The Asia-Pacific vitreoretinal disorders market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by increasing prevalence of diabetes, rising geriatric population, and rapid improvements in ophthalmic healthcare access. The region's growing inclination towards advanced eye care, supported by government initiatives promoting healthcare modernization, is driving the adoption of vitreoretinal diagnostic and treatment solutions. Furthermore, as APAC emerges as a major hub for healthcare expansion, the affordability and availability of ophthalmic care are increasing across a wider patient base.

Japan Vitreoretinal Disorders Market Insight

The Japan vitreoretinal disorders market is gaining momentum due to the country’s rapidly aging population, high healthcare standards, and strong demand for advanced retinal disease management. The Japanese market places a significant emphasis on precision medicine and early diagnosis, driving the adoption of advanced imaging technologies and minimally invasive procedures. Moreover, integration of ophthalmic solutions with digital healthcare systems and increasing focus on improving quality of life for elderly patients are further supporting market growth.

India Vitreoretinal Disorders Market Insight

The India vitreoretinal disorders market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the rapidly growing diabetic population, increasing awareness of eye health, and expanding access to ophthalmic care services. India stands as one of the fastest-growing markets for eye care solutions, and vitreoretinal treatments are becoming increasingly important in both urban and semi-urban regions. The push towards improving healthcare infrastructure, alongside rising affordability of diagnostic and treatment options, are key factors propelling market growth.

Vitreoretinal Disorders Market Share

The Vitreoretinal Disorders industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche AG (Switzerland)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Alcon Inc. (Switzerland)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- Bausch + Lomb Corporation (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- AbbVie Inc. (U.S.)

- Carl Zeiss Meditec AG (Germany)

- Topcon Corporation (Japan)

- NIDEK CO., LTD. (Japan)

- Ocular Therapeutix, Inc. (U.S.)

- EyePoint Pharmaceuticals, Inc. (U.S.)

- Genentech, Inc. (U.S.)

- Apellis Pharmaceuticals, Inc. (U.S.)

- Kodiak Sciences Inc. (U.S.)

- Clearside Biomedical, Inc. (U.S.)

- Alimera Sciences, Inc. (U.S.)

- STAAR Surgical Company (U.S.)

What are the Recent Developments in Global Vitreoretinal Disorders Market?

- In December 2025, a ranibizumab biosimilar (Nufymco) received FDA approval as an interchangeable therapy for retinal diseases, increasing affordability and access to treatments for diabetic retinopathy and macular degeneration

- In November 2025, the FDA approved Eylea HD® (aflibercept 8 mg) for retinal vein occlusion-related macular edema, expanding high-dose anti-VEGF treatment options and improving long-interval dosing for retinal disorder management

- In May 2025, the US FDA approved Susvimo® (ranibizumab implant) for diabetic retinopathy, marking a breakthrough in continuous drug delivery for retinal diseases and significantly reducing injection burden for patients with chronic vitreoretinal conditions

- In March 2025, regulatory advancements in sustained ocular drug delivery and next-generation retinal therapies continued, with multiple pipeline innovations and expanded approvals improving long-term treatment outcomes for vitreoretinal diseases

- In March 2025, the FDA approved Encelto (revakinagene taroretcel), the first encapsulated cell-based gene therapy for macular telangiectasia type 2, marking a major milestone in sustained retinal drug delivery for degenerative vitreoretinal diseases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.