Global Waste To Diesel Market

Market Size in USD Million

USD

691.53 Million

USD

1,251.80 Million

2025

2033

USD

691.53 Million

USD

1,251.80 Million

2025

2033

| 2026 - 2033 | |

| USD 691.53 Million | |

| USD 1,251.80 Million | |

| % | |

|

What is the Global Waste to Diesel Market Size and Growth Rate?

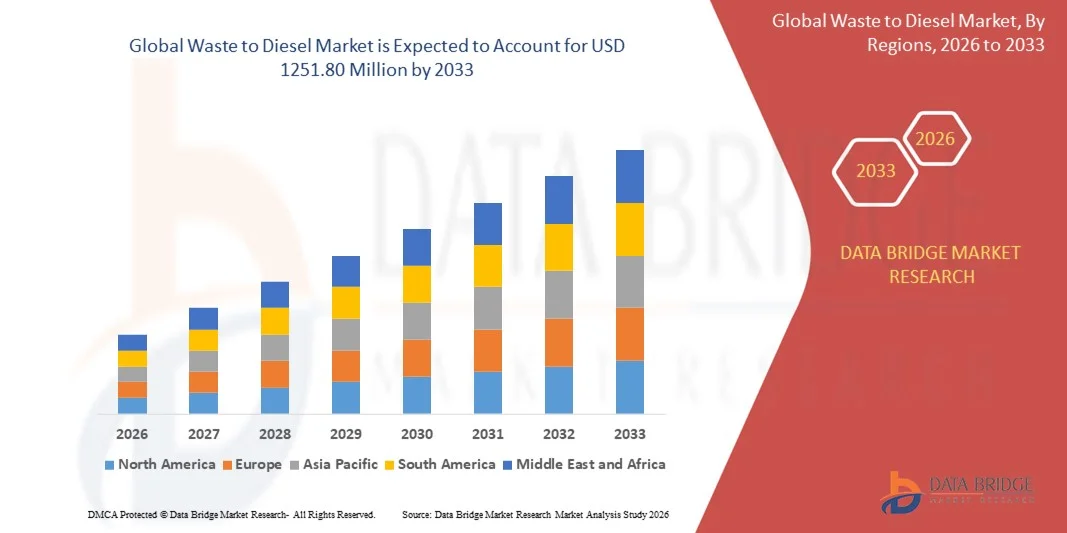

- The global waste to diesel market size was valued at USD 691.53 million in 2025 and is expected to reach USD 1251.80 million by 2033, at a CAGR of 7.70% during the forecast period

- The increasing demand from jet airways, transportation, construction and automotive sector has highly influenced growth of the waste to diesel market

- In line with this, the increasing application scope of diesel produced from waste in diesel boilers, tractors and trucks, ships, diesel power generators and construction machinery amongst others are also acting as a key determinant favoring the growth of the waste to diesel market

What are the Major Takeaways of Waste to Diesel Market?

- Escalating development of the automotive sector across countries as well as an increasing concern over waste management are also positively impacting the growth of the waste to diesel market

- The major factor accountable for the growth of the market is the stringent government policies on waste control and recycling of garbage. Beside this, the rising R&D so as to reduce the costs coupled with the installation of processing plants is also flourishing the growth of the waste to diesel market

- Europe dominated the waste to diesel market with the largest revenue share of 43.6% in 2025, driven by strong waste-management infrastructure, well-established renewable fuel policies, and rapid adoption of circular-economy practices

- North America is projected to witness the fastest CAGR of 10.2% during 2026–2033, driven by strong adoption of renewable fuels in transportation, logistics, and heavy-duty industrial sectors. The region benefits from advanced waste-processing infrastructure, rising landfill diversion initiatives, and increasing federal and state-level incentives for sustainable diesel production

- The Plastic Waste segment dominated the market with a revenue share of 48.7% in 2025, owing to the massive global accumulation of single-use plastics, strong demand for circular fuel solutions, and the high conversion efficiency of plastics into synthetic diesel through pyrolysis and depolymerization

Report Scope and Waste to Diesel Market Segmentation

|

Attributes |

Waste to Diesel Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Waste to Diesel Market?

Growing Adoption of Advanced Thermochemical and Catalytic Technologies

- The waste to diesel market is experiencing a major trend toward adopting advanced thermochemical conversion, catalytic depolymerization, and pyrolysis technologies to produce high-quality diesel from plastic, municipal waste, and biomass. This shift is driven by stricter emission norms, rising waste accumulation, and the growing push for circular economy models across global industries

- For instance, Klean Industries and Nexus Fuels expanded their deployment of catalytic pyrolysis units in 2025 to convert mixed plastic waste into ultra-low sulfur diesel, enabling large-scale commercialization of circular fuel

- Increasing government mandates for renewable fuels, waste reduction, and low-carbon transportation are accelerating investments in integrated waste-to-fuel plant

- Industries such as logistics, marine transport, and off-road machinery are increasingly adopting waste-derived diesel to reduce lifecycle emissions and fuel dependence

- Continuous innovations in catalysts, reactor designs, and feedstock preprocessing are boosting diesel yield, quality, and operational efficiency

- As global sustainability commitments strengthen, waste to diesel solutions is emerging as a crucial trend, supporting decarbonization and waste management goals across major market

What are the Key Drivers of Waste to Diesel Market?

- Rising demand for low-carbon, renewable, and circular fuels is a major driver of the waste to diesel market, as industries seek sustainable alternatives to conventional fossil diesel

- For instance, in 2025, OMV and Agilyx expanded their waste-to-fuel collaboration to convert post-consumer plastics into synthetic diesel for transportation and industrial applications

- Increasing global waste generation—particularly plastic, municipal solid waste, and industrial waste—is encouraging governments to adopt waste-to-energy and waste-to-fuel strategies

- Supportive policies such as low-carbon fuel standards, renewable energy mandates, and tax incentives are accelerating project implementation across the U.S., Europe, and Asia

- Technological advancements in pyrolysis, gasification, and Fischer–Tropsch synthesis are enabling higher diesel output, stable operations, and improved plant scalability

- As demand for renewable fuels rises across transport, power generation, and industrial sectors, the Waste to Diesel market is expected to register strong and steady growth globall

Which Factor is Challenging the Growth of the Waste to Diesel Market?

- High capital investment requirements, complex plant construction, and expensive catalytic systems pose significant challenges to large-scale waste-to-diesel deployment

- For instance, during 2024–2025, plastic waste supply volatility and feedstock contamination affected operational efficiencies for several pyrolysis-based diesel facilities

- Stringent regulatory approval processes for waste-derived fuels, combined with varying fuel quality standards across regions, increase compliance complexity

- Limited consumer acceptance and lack of awareness in emerging markets regarding the benefits and performance of waste-derived diesel hinder adoption

- Competition from other renewable fuel technologies such as biodiesel, renewable diesel (HVO), and green hydrogen creates pressure on pricing and market expansion

- To address these constraints, companies are investing in advanced feedstock preparation, improved catalysts, long-term supply agreements, and government partnerships to ensure consistent, high-quality diesel productio

How is the Waste to Diesel Market Segmented?

The market is segmented on the basis of source and technology type.

- By Source

On the basis of source, the waste to diesel market is segmented into Municipal Waste, Oil and Fat Waste, and Plastic Waste. The Plastic Waste segment dominated the market with a revenue share of 48.7% in 2025, owing to the massive global accumulation of single-use plastics, strong demand for circular fuel solutions, and the high conversion efficiency of plastics into synthetic diesel through pyrolysis and depolymerization. Plastic-derived diesel offers high calorific value and low sulfur content, making it suitable for industrial and transportation applications.

The Municipal Waste segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising investments in waste-to-energy facilities, government mandates for solid waste reduction, and increasing adoption of integrated waste management systems. Continuous advancements in sorting, feedstock preprocessing, and thermochemical technologies further support municipal waste’s expanding contribution to waste-derived diesel production across global markets.

- By Technology Type

On the basis of technology type, the waste to diesel market is segmented into Pyrolysis, Incineration, Gasification, and Depolymerization. The Pyrolysis segment dominated the market with a revenue share of 52.4% in 2025, attributed to its proven efficiency in converting plastic, municipal, and biomass waste into high-quality diesel, along with lower emissions and cost-effective scalability compared to traditional incineration. Pyrolysis plants offer modular deployment, high diesel yield, and compatibility with mixed waste streams, making them the most widely adopted technology worldwide.

The Depolymerization segment is expected to witness the fastest CAGR during 2026–2033, propelled by its ability to break down complex plastic polymers into high-purity liquid hydrocarbons suitable for refining into diesel. Growing global emphasis on plastic circularity, rising investments in chemical recycling, and advancements in catalytic systems are accelerating depolymerization adoption. As the need for ultra-low-carbon synthetic fuels increases, advanced catalytic and molecular recycling technologies will continue to shape future market growth.

Which Region Holds the Largest Share of the Waste to Diesel Market?

- Europe dominated the waste to diesel market with the largest revenue share of 43.6% in 2025, driven by strong waste-management infrastructure, well-established renewable fuel policies, and rapid adoption of circular-economy practices. Countries such as Germany, the U.K., France, and the Netherlands are leading investments in advanced waste conversion technologies to reduce landfill dependency and carbon emissions. Rising demand for sustainable diesel alternatives across transportation, logistics, and industrial sectors further supports Europe’s leadership

- The region is witnessing accelerated deployment of thermochemical and catalytic conversion facilities, supported by EU directives promoting renewable fuels and waste valorization. Increasing public-private partnerships, funding for waste-to-fuel innovations, and corporate sustainability commitments are strengthening Europe’s dominance in the global market

- Favorable regulatory frameworks such as the Renewable Energy Directive (RED II), decarbonization targets, and financial incentives for green fuel production continue to position Europe as the global leader in the Waste to Diesel market

Germany Waste to Diesel Market Insight

Germany represents the largest contributor to Europe’s Waste to Diesel market, supported by strong waste-recycling infrastructure, advanced R&D capabilities, and aggressive carbon-reduction targets. The country’s focus on expanding biofuel production, combined with growing investments in circular fuel technologies, is fostering large-scale Waste to Diesel projects. Strategic collaborations between technology providers, energy companies, and government bodies are accelerating deployment of high-efficiency conversion facilities across the country.

U.K. Waste to Diesel Market Insight

The U.K. is witnessing steady growth in the Waste to Diesel market driven by rising emphasis on clean transportation, expansion of waste-conversion pilot facilities, and enhanced governmental commitments toward renewable fuels. Manufacturers are adopting advanced catalytic and thermochemical processes to convert municipal and commercial waste into high-quality diesel substitutes. Regulatory support, sustainability mandates, and increasing corporate demand for low-carbon fuels are strengthening long-term market development.

North America Waste to Diesel Market Insight

North America is projected to witness the fastest CAGR of 10.2% during 2026–2033, driven by strong adoption of renewable fuels in transportation, logistics, and heavy-duty industrial sectors. The region benefits from advanced waste-processing infrastructure, rising landfill diversion initiatives, and increasing federal and state-level incentives for sustainable diesel production. Growing demand for circular-economy solutions and decarbonized fuels is further accelerating Waste to Diesel facility installations across the region.

U.S. Waste to Diesel Market Insight

The U.S. is the largest contributor to the North American Waste to Diesel market, supported by strong technology innovation, large-scale waste-to-fuel pilot projects, and increasing adoption of renewable diesel across shipping, aviation, and trucking sectors. Federal initiatives promoting greenhouse-gas reduction, coupled with rising investments from energy and waste-management companies, are driving significant capacity expansion. Strategic collaborations and advancements in pyrolysis, gasification, and synthetic fuel upgrading continue to strengthen the country’s market position.

Canada Waste to Diesel Market Insight

Canada contributes consistently to the regional Waste to Diesel market due to rising clean-energy adoption, growing waste-conversion research, and supportive federal programs for renewable fuel development. Increasing investments in pilot plants, collaborations with technology innovators, and nationwide efforts to reduce landfill dependency are fostering the development of Waste to Diesel facilities. The country’s focus on sustainable transportation and circular-economy initiatives enhances its long-term market potential.

Which are the Top Companies in Waste to Diesel Market?

The waste to diesel industry is primarily led by well-established companies, including:

- Covanta Holding Corporation (U.S.)

- Biofuels Digest (U.S.)

- PolyCycl Private Limited (India)

- Plastic2Oil, Inc. (U.S.)

- Valero Energy Corporation (U.S.)

- Klean Industries (Canada)

- Nexus Fuels (U.S.)

- Agilyx, Inc. (U.S.)

- Plastic Advanced Recycling Corp. (U.S.)

- OMV Aktiengesellschaft (Austria)

- MK Aromatics Limited (India)

- Clariant (Switzerland)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Waste To Diesel Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Waste To Diesel Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Waste To Diesel Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.