Middle East And Africa Bacteriophages Therapy Market

Market Size in USD Million

USD

1.37 Million

USD

1.88 Million

2025

2033

USD

1.37 Million

USD

1.88 Million

2025

2033

| 2026 - 2033 | |

| USD 1.37 Million | |

| USD 1.88 Million | |

| % | |

|

What is the Middle East and Africa Bacteriophages Therapy Size and Growth Rate?

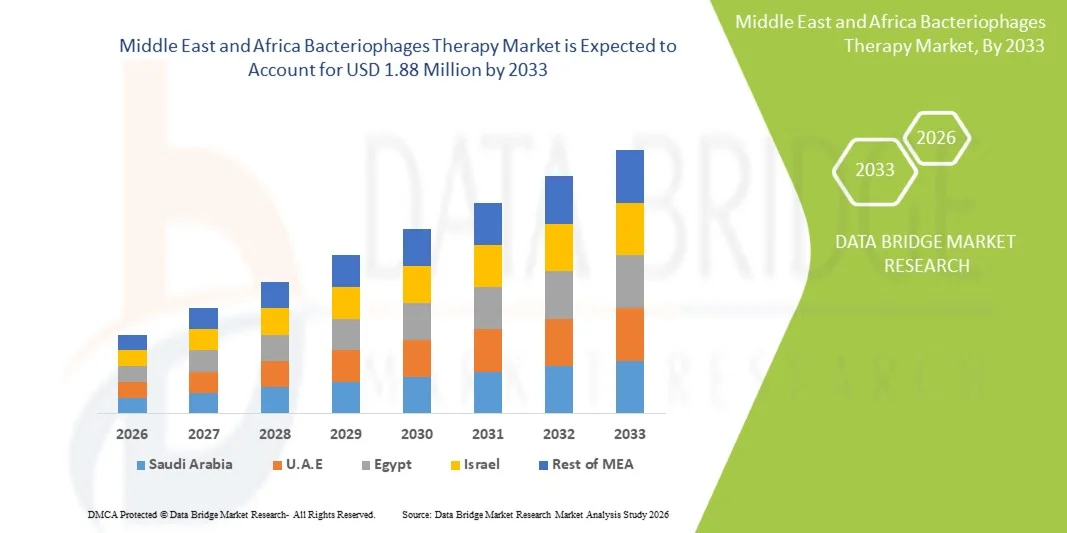

- As per Data Bridge Market Research Analysis the Middle East and Africa Bacteriophages Therapy Market size was valued at USD 1.37 Million in 2025 and is expected to reach USD 1.88 Million by 2033, at a CAGR of 4.10% during the forecast period

- The market growth is largely fueled by the increasing global burden of antibiotic-resistant infections and rapid advancements in phage research, personalized medicine, and genomic engineering. The rising shift from traditional antibiotics toward precision-based antimicrobial therapies is significantly accelerating the adoption of bacteriophage-based solutions across clinical, veterinary, and agricultural settings

- Furthermore, growing consumer and healthcare provider demand for safe, effective, and targeted antimicrobial alternatives is positioning bacteriophage therapy as a promising next-generation treatment option. These converging factors are accelerating the uptake of Bacteriophages Therapy solutions, thereby significantly boosting the industry’s growth

Market Size & Forecast

- Global Market Value (2025): USD 1.37 Million in 2025

- Expected Market Value (2033): USD 1.88 Million by 2033

- Forecast CAGR (2026–2033): 4.10%

Middle East and Africa Bacteriophages Therapy Market Analysis

- Bacteriophage therapy, offering highly targeted and precision-based antimicrobial action against specific bacterial pathogens, is becoming an essential component of next-generation infectious disease treatment in both hospital and clinical research settings due to its ability to combat antibiotic-resistant infections, reduce side effects, and preserve healthy microbiota

- The escalating demand for bacteriophage therapy is primarily fueled by the global rise in antimicrobial resistance (AMR), increasing investments in phage biotechnology, and the expanding adoption of personalized medicine approaches. In addition, growing clinical trials, supportive regulatory pathways, and emerging biotechnology startups are accelerating the uptake of Bacteriophages Therapy solutions

- Saudi Arabia dominated the Middle East and Africa Bacteriophages Therapy Market with the largest revenue share of 27.4% in 2025, supported by strong government investment in advanced healthcare technologies, expansion of infectious disease research capabilities, and strategic initiatives under Saudi Vision 2030 to strengthen biomedical innovation. The country’s increasing adoption of innovative therapeutic modalities across major hospitals further enhances its leadership position in the Middle East

- The U.A.E. is expected to be the fastest-growing country in the Middle East and Africa Bacteriophages Therapy Market during the forecast period, driven by rapid healthcare modernization, expansion of clinical research infrastructure, rising prevalence of antibiotic-resistant infections, and strong government focus on adopting cutting-edge biotherapeutics in both public and private healthcare sectors

- The Sterile Broth Culture segment dominated the largest market revenue share of 62.1% in 2025, due to stability, ease of production, and suitability for clinical use

Report Scope and Middle East and Africa Bacteriophages Therapy Market Segmentation

|

Attributes |

Bacteriophages Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Middle East and Africa Bacteriophages Therapy?

“Growing Shift Toward Precision, Personalized, and Synthetic Bacteriophage Engineering”

- A major and rapidly strengthening trend in the Middle East and Africa Bacteriophages Therapy Market is the transition from traditional, naturally-isolated phages toward precision-engineered, genetically optimized, and personalized phage therapies. This shift is driven by increasing antimicrobial resistance (AMR), the limitations of broad-spectrum antibiotics, and the clinical need for highly targeted antibacterial solutions

- For instance, companies such as Adaptive Phage Therapeutics (APT) are advancing personalized phage therapy platforms that match patient-specific bacterial strains with corresponding phages from continuously expanding phage libraries. Similarly, BiomX is leveraging synthetic biology and microbiome-targeted phages to treat chronic infections and inflammatory conditions

- Engineered phages enable features such as improved host range expansion, enhanced bacterial killing efficiency, resistance-circumvention traits, and removal of undesirable genes, which significantly increases therapeutic reliability and clinical outcomes. In addition, the ability to rapidly update phage cocktails helps maintain effectiveness against evolving bacterial mutations

- The growing adoption of CRISPR-enhanced phage design and bioinformatics-led phage selection supports the development of precision treatments for infections where conventional antibiotics fail. Start-ups and research institutions are increasingly collaborating to create automated phage-matching platforms capable of rapid bacterial identification and phage pairing

- The integration of synthetic biology tools is also allowing manufacturers to develop modular, programmable bacteriophages with predictable behavior and enhanced safety profiles. For example, Pherecydes Pharma is advancing tailored phage cocktails specifically targeted toward multidrug-resistant (MDR) pathogens like Pseudomonas aeruginosa and Staphylococcus aureus

- This expanding trend toward personalized and engineered bacteriophage therapies is fundamentally reshaping treatment expectations for drug-resistant infections. As a result, companies across the U.S., Europe, and Asia-Pacific are increasingly investing in phage engineering, phage banks, and automated phage manufacturing platforms to meet growing clinical demand

- Demand for precision-based bacteriophage therapies is rising rapidly across hospital, research, and biotechnology settings as healthcare providers look for safer, more effective alternatives to antibiotics, especially for chronic, recurrent, and antibiotic-resistant infections

Middle East and Africa Bacteriophages Therapy Market Dynamics

Driver

“Growing Antibiotic Resistance and Increasing Clinical Acceptance of Phage-Based Therapeutics”

- The global rise in antimicrobial resistance (AMR) and the declining effectiveness of conventional antibiotics are key drivers accelerating the demand for bacteriophage therapy. Hospitals and clinicians are increasingly seeking alternative treatment approaches for life-threatening infections that no longer respond to available antibiotics

- For instance, in January 2024, Adaptive Phage Therapeutics expanded its clinical trial program for MDR Staphylococcus aureus infections under FDA oversight, demonstrating growing institutional and regulatory recognition of phage-based therapeutics. Such advancements are expected to drive strong market expansion in the coming years

- As awareness increases regarding MDR pathogens such as E. coli, Klebsiella pneumoniae, and Pseudomonas aeruginosa, healthcare providers are rapidly adopting phage therapies for severe wound infections, bone infections, diabetic foot ulcers, and chronic respiratory illnesses

- Bacteriophage therapies offer crucial advantages such as high specificity, reduced toxicity, minimal impact on beneficial microbiota, and the ability to replicate at infection sites, which makes them superior to broad-spectrum antibiotics in many clinical cases

- The rise of hospital-acquired infections (HAIs) and the increasing prevalence of immunocompromised patients further elevate the need for highly targeted therapeutic strategies. The ability to combine phage therapy with traditional antibiotics for synergistic effects enhances treatment effectiveness and broadens adoption

- Furthermore, improved regulatory support, compassionate-use approvals, and expanding clinical trial pipelines are strengthening global acceptance of phage therapy, particularly in the U.S., Europe, and South Korea. The increasing availability of scalable GMP phage manufacturing platforms continues to boost commercial feasibility

- Collectively, these factors strongly propel market growth by encouraging hospitals, government programs, and biotechnology firms to incorporate phage-based solutions into routine treatment pathways for complex bacterial infections

Restraint/Challenge

“Regulatory Complexity, Limited Standardization, and High Production Constraints”

- Despite rising interest, the Middle East and Africa Bacteriophages Therapy Market faces significant challenges due to regulatory uncertainty, lack of global standardization, and complexities in developing consistent, scalable phage manufacturing processes. These issues continue to hinder rapid market penetration

- For instance, varying approval pathways across regions — with the U.S. relying on investigational IND routes and Europe moving toward adaptive regulatory frameworks — create delays and inconsistencies in clinical adoption and commercialization

- Phages’ biological diversity and rapid evolution make it difficult to establish universal quality benchmarks, potency testing methods, and long-term stability standards. These scientific challenges lead to extended development timelines and increased production costs for manufacturers

- In addition, the process of isolating, sequencing, purifying, and producing high-quality, contaminant-free bacteriophages requires sophisticated bioprocessing infrastructure and skilled personnel, contributing to high manufacturing and R&D expenses

- Public awareness remains limited, and some clinicians remain hesitant to adopt phage therapy due to insufficient long-term clinical data and concerns regarding regulatory acceptance

- Furthermore, the need for personalized phage cocktails in some cases increases logistical complexity, as real-time phage matching, bacterial isolation, and customized formulation require coordination between laboratories and clinical centers

- To overcome these challenges, the industry must prioritize harmonized regulatory frameworks, standardized manufacturing guidelines, improved stability testing, and expanded clinical trial evidence. Achieving these goals will be essential for enabling large-scale commercialization and wider therapeutic adoption of bacteriophage-based treatments

Middle East and Africa Bacteriophages Therapy Market Scope

The Middle East and Africa Bacteriophages Therapy Market is segmented on the basis of target, type, base, application, route of administration, end-user, and distribution channel.

• By Target

On the basis of target, the Middle East and Africa Bacteriophages Therapy Market is segmented into Escherichia coli, Staphylococcus, Streptococcus, Pseudomonas, Salmonella, and Others. The Escherichia coli segment dominated the largest market revenue share of 36.4% in 2025, driven by the high prevalence of E. coli-related gastrointestinal infections and growing antibiotic resistance. Hospitals and specialty clinics increasingly prefer phage therapy due to its targeted action and minimal side effects. E. coli phages are supported by ongoing clinical trials validating their safety and efficacy. The segment benefits from research funding and government initiatives promoting alternative therapies. Rising awareness among patients and healthcare professionals accelerates adoption. Phage therapy for E. coli infections reduces dependence on broad-spectrum antibiotics. The commercial availability of well-characterized E. coli phages ensures reliable clinical use. Continuous technological advancements in phage formulation enhance stability and shelf-life. Increasing incidence of multidrug-resistant strains further strengthens demand. This segment remains crucial in both developed and developing regions.

The Staphylococcus segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, driven by increasing cases of MRSA and other resistant Staphylococcus infections. The rising urgency for effective alternatives to conventional antibiotics fuels research and commercial interest. Hospitals and specialty clinics are rapidly adopting Staphylococcus-targeted phages for infection control. Academic research institutes are actively developing engineered phages to improve therapeutic efficacy. Clinical trials are expanding the evidence base for safe and targeted treatment. Phage therapy offers rapid bacterial clearance with minimal disruption to normal microbiota. The integration of phage therapy with standard care enhances outcomes for chronic and post-operative infections. Rising awareness among physicians and patients boosts prescription rates. Government and private funding support new product development and commercialization. Growing prevalence of skin and soft tissue infections amplifies market demand. Regulatory approvals in key markets strengthen adoption and distribution. Expansion into emerging markets offers significant growth opportunities.

• By Type

On the basis of type, the market is segmented into Lytic and Lysogenic. The Lytic segment held the largest market revenue share of 58.7% in 2025, owing to its rapid bactericidal action and effectiveness against multi-drug-resistant strains. Hospitals and clinics prefer lytic phages for acute infections due to their immediate effect. The segment benefits from a well-established safety profile and clinical evidence. Lytic phages reduce bacterial load quickly, minimizing complications and hospitalization duration. Their predictable pharmacokinetics allow precise dosing and treatment planning. Adoption is supported by rising cases of gastrointestinal and skin infections. Pharmaceutical companies invest in large-scale production for clinical use. Integration with standard antibiotic therapy enhances therapeutic outcomes. Research is expanding formulation stability for broader applications. Patient compliance improves due to shorter treatment duration. Lytic phages are compatible with various delivery formats including oral and dermal applications. Their commercial availability strengthens market penetration.

The Lysogenic segment is expected to witness the fastest CAGR of 16.3% from 2026 to 2033, driven by research on engineered lysogenic phages and their potential in long-term infection control. Academic and clinical research is increasing due to their ability to integrate into host genomes. Lysogenic phages offer prolonged antibacterial activity and microbiome modulation. Growing interest in chronic infection management drives market growth. Technological advancements allow safer and more predictable therapeutic applications. Clinical trials are validating efficacy against resistant bacterial strains. The segment benefits from funding and collaborative projects between research institutes and biotech companies. Lysogenic phages are gaining attention for personalized therapy applications. Regulatory acceptance is gradually improving with positive trial results. Their integration with other treatment modalities enhances versatility. Patient-specific formulations are being explored for targeted therapy. Expansion in emerging markets offers significant opportunities. Increasing awareness among healthcare providers supports adoption.

• By Base

On the basis of base, the market is segmented into Sterile Broth Culture and Water-Soluble Jelly Base. The Sterile Broth Culture segment dominated the largest market revenue share of 62.1% in 2025, due to stability, ease of production, and suitability for clinical use. Hospitals and research labs widely use broth cultures for reliable results. The segment benefits from standardized manufacturing protocols ensuring consistent quality. Sterile broth culture allows precise dosing and maintains phage viability. Adoption is supported by clinical evidence and regulatory compliance. The format is suitable for both oral and parenteral applications. Pharmaceutical companies prefer broth cultures for mass production and commercialization. Integration with hospital protocols ensures safe administration. The segment sees high usage in gastrointestinal and systemic infections. Continuous R&D enhances efficacy and shelf-life. Broth cultures are compatible with automated distribution systems. Growing awareness and clinical adoption drive market dominance.

The Water-Soluble Jelly Base segment is expected to witness the fastest CAGR of 18.5% from 2026 to 2033, driven by demand in topical applications, wound care, and patient-friendly formulations. The segment benefits from growing use in post-operative wound infections and skin treatments. Jelly-based phages allow localized therapy, minimizing systemic side effects. Rising adoption in hospitals and specialty clinics supports growth. Clinical research demonstrates improved patient compliance with topical delivery. Technological advancements enhance stability and shelf-life in jelly formulations. Growing preference for non-invasive therapies accelerates adoption. Rising awareness among physicians and patients strengthens market potential. E-commerce and distribution channels expand accessibility. Integration with modern wound care products boosts market acceptance. Targeted therapy in dermatology increases segment relevance. Government initiatives for alternative therapies support expansion. Emerging markets present new growth opportunities.

• By Application

On the basis of application, the market is segmented into Bacterial Dysentery, Infections of Skin and Nasal Mucosa, Suppurative Skin Infection, Lung and Pleural Infections, Postoperative Wound Infections, and Others. The Bacterial Dysentery segment accounted for the largest market revenue share of 40.6% in 2025, driven by high prevalence in developing regions and resistance to conventional antibiotics. Hospitals and clinics prefer phage therapy due to its specificity and rapid action. Research supports the efficacy of phages in gastrointestinal infections. Government health programs and NGOs promote adoption. Patient awareness and physician recommendation boost market penetration. Clinical trials reinforce safety and efficacy profiles. Integration into public health strategies enhances treatment accessibility. Commercial availability of standardized phages ensures reliability. Technological advances improve stability and storage. Rising prevalence of pediatric cases drives demand. Supportive reimbursement policies aid adoption. Continuous R&D ensures improvement in formulations.

The Postoperative Wound Infections segment is expected to witness the fastest CAGR of 21.2% from 2026 to 2033, driven by increasing surgical procedures and antibiotic-resistant infections. Hospitals adopt phage therapy for wound management and infection control. Topical and dermal phage formulations are gaining preference. Clinical evidence supports faster healing and reduced infection recurrence. Research focuses on combining phages with conventional antibiotics. Patient compliance improves due to ease of application. Government and private healthcare programs encourage adoption. Integration into hospital protocols enhances operational efficiency. Technological advancements allow better formulation and stability. Rising awareness among surgeons and nurses boosts usage. Emerging markets show growing acceptance. Collaborations between biotech companies and hospitals expand reach. Expansion in surgical centers provides significant growth opportunities.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Parenteral, Rectal, Dermal, and Others. The Oral segment held the largest market revenue share of 47.9% in 2025, due to convenience, effectiveness in gastrointestinal infections, and patient compliance. Oral phages allow targeted therapy without invasive procedures. Hospitals and clinics prefer oral administration for outpatient care. Clinical evidence supports safety and rapid action. Pharmaceutical manufacturers favor scalable oral formulations. Integration with routine treatment enhances outcomes. Stability and shelf-life improvements strengthen adoption. Commercial availability ensures reliable supply. Research focuses on encapsulation techniques for better bioavailability. Public health programs promote oral phage therapy. Awareness campaigns drive adoption among patients and physicians. Oral delivery supports widespread use in emerging markets. Regulatory approvals reinforce credibility.

The Dermal segment is expected to witness the fastest CAGR of 20.5% from 2026 to 2033, driven by demand in skin infections, burns, and post-operative wounds. Topical therapy allows localized treatment and reduces systemic exposure. Hospitals and specialty clinics adopt dermal phages for patient-friendly care. Clinical studies demonstrate rapid healing and infection control. Technological advancements improve gel and cream formulations. Integration with wound dressings enhances therapeutic efficacy. Academic research supports new delivery systems. Rising awareness among dermatologists and surgeons boosts adoption. Patient compliance improves due to non-invasive application. Regulatory approvals enable market expansion. E-commerce and distributors increase accessibility. Emerging markets show growing preference for dermal therapy. Private and public healthcare programs encourage use.

• By End-User

On the basis of end-user, the market is segmented into Hospitals, Specialty Clinics, Academic Research and Institutes, and Others. The Hospitals segment accounted for the largest market revenue share of 53.3% in 2025, driven by high patient inflow, infection control protocols, and access to clinical-grade phages. Hospitals prefer standardized phage formulations for reliability and safety. Integration into infection management programs enhances adoption. Commercial availability and distribution networks ensure supply. Continuous training and awareness programs support usage. Hospitals conduct in-house studies to validate efficacy. Rising incidence of resistant infections increases demand. Technological advancements enable efficient administration. Hospital adoption is supported by government health initiatives. Patient trust in hospital-administered therapy strengthens market position. Regulatory compliance ensures quality and safety. Hospitals provide a platform for large-scale clinical trials.

The Academic Research and Institutes segment is expected to witness the fastest CAGR of 22.0% from 2026 to 2033, driven by increasing research funding, clinical trials, and collaborations. Academic institutions focus on engineering phages for targeted therapy. Research expands into chronic and rare infections. Government grants and private investments support innovation. Collaboration with biotech companies accelerates commercialization. Publication of clinical results boosts awareness and adoption. Training programs develop skilled professionals for phage therapy. Academic research contributes to regulatory approvals and guidelines. Laboratory-scale production enables experimental applications. Conferences and seminars drive knowledge exchange. Emerging markets show increased research activity. Patenting of phage products enhances market value. Academic findings influence hospital adoption.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender and Third-Party Distributors. The Direct Tender segment dominated the largest market revenue share of 61.5% in 2025, due to bulk procurement by hospitals, government programs, and research institutions. Direct tendering ensures quality control, regulatory compliance, and steady supply. Hospitals and institutions prefer direct procurement for critical therapies. Government health initiatives support adoption through tenders. Standardized supply chains enhance reliability. Long-term contracts secure consistent availability. Pharmaceutical companies maintain direct sales teams for hospital engagement. Clinical and research requirements drive bulk purchases. Market dominance is strengthened by regulatory oversight. Cost efficiency and transparency support tender adoption. Direct tenders facilitate access in emerging markets. Strong distribution networks ensure timely delivery.

The Third-Party Distributors segment is expected to witness the fastest CAGR of 19.4% from 2026 to 2033, driven by e-commerce growth, regional distribution networks, and expanding reach to semi-urban and rural healthcare facilities. Distributors provide smaller-scale supply to clinics and research labs. Flexible logistics enable timely delivery and inventory management. E-pharmacy platforms increase accessibility for end-users. Partnerships with local distributors enhance market penetration. Awareness campaigns boost adoption in remote regions. Regulatory guidance ensures safe distribution. Distributors support hospitals with quick replenishment. Marketing and educational support facilitate product understanding. Growth in specialty clinics drives demand for distributed products. Regional customization improves acceptance. Expansion in developing regions offers high growth potential.

Middle East and Africa Bacteriophages Therapy Market Regional Analysis

- The Middle East & Africa Middle East and Africa Bacteriophages Therapy Market is projected to grow significantly throughout the forecast period, driven by rising antibiotic-resistant infections, increasing investment in advanced infectious disease management, and growing awareness of precision antibacterial therapies

- Governments across the region are strengthening healthcare infrastructure, expanding research capabilities, and promoting the adoption of innovative biologics, all of which are accelerating the demand for bacteriophage-based treatments

- In addition, rising collaborations between regional healthcare providers and global biotech firms are supporting the introduction of clinically validated phage therapies in both hospital and research settings

Saudi Arabia Middle East and Africa Bacteriophages Therapy Market Insight

Saudi Arabia Middle East and Africa Bacteriophages Therapy Market dominated the Middle East and Africa Bacteriophages Therapy Market with the largest revenue share of 27.4% in 2025, supported by strong government investment in advanced healthcare technologies, expansion of infectious disease research capabilities, and strategic initiatives under Saudi Vision 2030 to strengthen biomedical innovation. The country’s increasing adoption of innovative therapeutic modalities across major hospitals further enhances its leadership position in the Middle East.

U.A.E. Middle East and Africa Bacteriophages Therapy Market Insight

The U.A.E. Middle East and Africa Bacteriophages Therapy Market is expected to be the fastest-growing country in the Middle East and Africa Bacteriophages Therapy Market during the forecast period, driven by rapid healthcare modernization, expansion of clinical research infrastructure, rising prevalence of antibiotic-resistant infections, and strong government focus on adopting cutting-edge biotherapeutics in both public and private healthcare sectors. The nation’s commitment to integrating next-generation therapies and fostering biotechnology development positions it as a key growth hotspot in the region.

Which are the Top Companies in Middle East and Africa Bacteriophages Therapy?

The Bacteriophages Therapy industry is primarily led by well-established companies, including:

- Intralytix Inc. (U.S.)

- Armata Pharmaceuticals (U.S.)

- PhagePro Inc. (U.S.)

- Micreos (Netherlands)

- Proteon Pharmaceuticals (Poland)

- Phagelux (China)

- Technophage (Portugal)

- Eligo Bioscience (France)

- Pherecydes Pharma (France)

- PhageLab (Chile)

- Locus Biosciences (U.S.)

- Genpharm (U.S.)

- Phage International (U.S.)

- Aptorum Group (Hong Kong)

- Viralytics (Australia)

- iNtRON Biotechnology (South Korea)

Latest Developments in Middle East and Africa Bacteriophages Therapy Market

- In February 2021, Locus Biosciences announced the successful completion of a Phase 1b clinical trial of its CRISPR-Cas3–enhanced bacteriophage therapy (LBP-EC01), targeting Escherichia coli. The trial showed that the engineered phage was safe, well-tolerated, and led to a reduction in E. coli levels in patients, marking a major proof-of-concept for their precision phage platform

- In May 2022, Adaptive Phage Therapeutics (APT) reported dosing of the first patient in its “DANCE” Phase 1/2 trial in Diabetic Foot Osteomyelitis (DFO), using its PhageBank approach. This was a key clinical milestone, as APT uses a library of phages matched to patient infections to target antibiotic-resistant infections

- In January 2024, Locus Biosciences received a $23.9 million funding tranche from BARDA (the U.S. Biomedical Advanced Research and Development Authority) to support Part 2 of its ELIMINATE Phase 2 trial of LBP-EC01 for drug-resistant E. coli urinary tract infections. This non-dilutive support underscores strong governmental commitment to advanced phage therapies

- In August 2024, Locus Biosciences announced positive results from Part 1 (open-label) of its ELIMINATE Phase 2 trial of LBP-EC01. The data, published in The Lancet Infectious Diseases, reaffirmed safety and tolerability in patients, providing a strong foundation for the blinded, placebo-controlled Part 2 of the study

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.