Middle East And Africa Ehealth Market

Market Size in USD Billion

USD

1.13 Billion

USD

4.76 Billion

2025

2033

USD

1.13 Billion

USD

4.76 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.13 Billion | |

| USD 4.76 Billion | |

| % | |

|

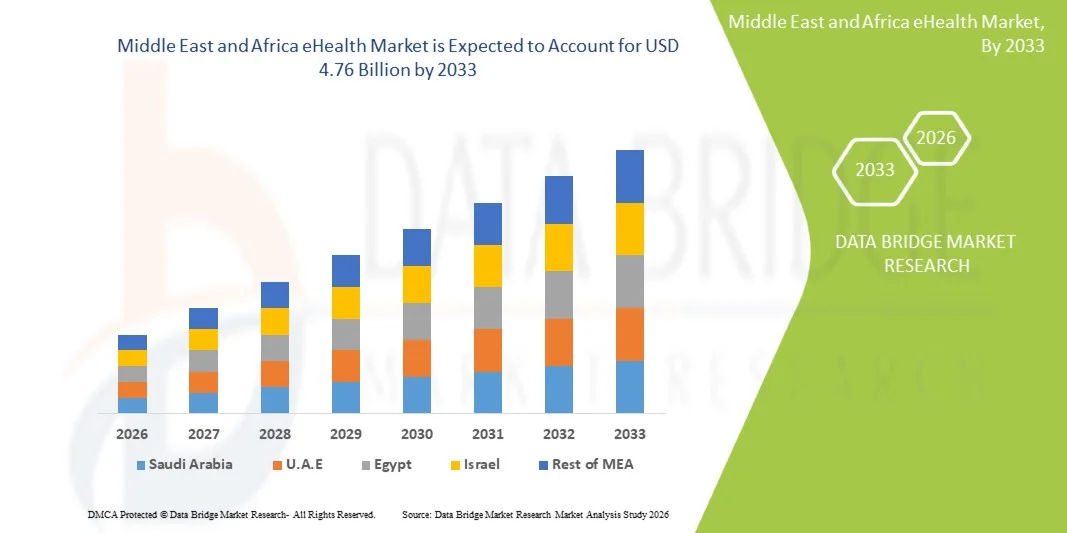

Middle East and Africa eHealth Market Size

- The Middle East and Africa eHealth market size was valued at USD 1.13 billion in 2025 and is expected to reach USD 4.76 billion by 2033, at a CAGR of 19.7% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital healthcare solutions, expansion of telemedicine services, and government initiatives aimed at improving healthcare infrastructure and accessibility across both urban and rural areas

- Furthermore, rising demand for efficient, patient-centric, and integrated healthcare systems, along with growing investments in electronic health records (EHR), remote monitoring, and healthcare IT solutions, is driving the adoption of eHealth platforms, thereby significantly boosting the industry's growth

Middle East and Africa eHealth Market Analysis

- eHealth solutions, including electronic health records (EHR), telemedicine platforms, and healthcare information systems, are becoming increasingly vital components of modern healthcare delivery in countries across the Middle East and Africa due to their ability to enhance care coordination, improve patient outcomes, and enable efficient management of healthcare data across providers and institutions

- The escalating demand for eHealth is primarily driven by government-led digital health initiatives, rising investments in healthcare infrastructure, increasing burden of chronic diseases, and the growing need for accessible, cost-effective, and patient-centric healthcare services across the region

- United Arab Emirates dominated the eHealth market with the largest revenue share of 32.5% in 2025, characterized by advanced healthcare infrastructure, strong governmental support for digital transformation programs, and rapid adoption of telemedicine and electronic health record systems

- South Africa is expected to be the fastest growing country in the eHealth market during the forecast period due to expanding mobile connectivity, improving internet penetration, and increasing deployment of mobile health (mHealth) and telehealth solutions to address gaps in healthcare access

- Cloud segment dominated the eHealth market with a significant market share of 46.8% in 2025, driven by its scalability, cost-effectiveness, ease of deployment, and growing preference among healthcare organizations for centralized, interoperable, and secure digital healthcare platforms

Report Scope and Middle East and Africa eHealth Market Segmentation

|

Attributes |

Middle East and Africa eHealth Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa eHealth Market Trends

“Expansion of Telemedicine and Digital Health Integration”

- A significant and accelerating trend in the Middle East and Africa eHealth market is the rapid expansion of telemedicine platforms and their integration with electronic health records and broader digital healthcare ecosystems such as mobile health applications and hospital information systems, enhancing accessibility and continuity of care

- For instance, telehealth platforms integrated with EHR systems enable healthcare providers to conduct virtual consultations while simultaneously accessing patient histories, improving diagnostic efficiency and care coordination across facilities

- The integration of digital health technologies enables features such as remote patient monitoring, AI-assisted diagnostics, and real-time health data tracking, allowing providers to deliver more proactive and personalized care, particularly for chronic disease management

- The seamless interoperability between telemedicine platforms, wearable devices, and centralized healthcare databases facilitates unified healthcare delivery, enabling clinicians to manage patient information, appointments, and treatment plans through a single connected interface

- This trend toward more connected, data-driven, and patient-centric healthcare systems is reshaping expectations for healthcare delivery, with organizations such as Seha Virtual Hospital in Saudi Arabia implementing advanced digital platforms to support large-scale virtual care services

- The increasing adoption of cloud-based eHealth platforms and mobile applications is further enabling scalable deployment of healthcare services, improving accessibility in remote and underserved areas

- The demand for integrated eHealth solutions is growing rapidly across both public and private healthcare sectors, as governments and providers increasingly prioritize efficient, scalable, and technology-enabled healthcare delivery models

Middle East and Africa eHealth Market Dynamics

Driver

“Growing Need Due to Rising Healthcare Demand and Digital Transformation Initiatives”

- The increasing burden of chronic diseases and rising healthcare demand, coupled with government-led digital transformation initiatives, is a significant driver for the heightened adoption of eHealth solutions across countries in the Middle East and Africa

- For instance, in April 2025, several national healthcare authorities expanded digital health programs aimed at strengthening telemedicine infrastructure and electronic health record adoption to improve service delivery and accessibility

- As healthcare systems seek to improve efficiency and patient outcomes, eHealth solutions offer advanced capabilities such as remote consultations, digital patient records, and real-time health monitoring, providing a strong alternative to traditional care models

- Furthermore, the growing penetration of smartphones and internet connectivity is enabling broader access to digital health services, making eHealth platforms an integral part of modern healthcare ecosystems in both urban and rural areas

- The convenience of remote healthcare access, reduced hospital congestion, and the ability to connect patients with specialists across geographies are key factors propelling the adoption of eHealth solutions in both public and private healthcare sectors

- Increasing investments from international organizations and technology providers are also supporting the deployment of advanced digital health infrastructure across developing healthcare systems

- The rising focus on improving healthcare accessibility in underserved populations is encouraging the adoption of mobile health and telemedicine solutions at a national level

Restraint/Challenge

“Cybersecurity Risks and Infrastructure Limitations”

- Concerns surrounding data privacy, cybersecurity vulnerabilities, and the protection of sensitive patient information pose a significant challenge to broader eHealth adoption across the Middle East and Africa

- For instance, incidents involving breaches of healthcare databases and cyberattacks on hospital systems have increased caution among healthcare providers and patients regarding the adoption of fully digital health platforms

- Addressing these cybersecurity concerns through robust encryption, secure cloud architectures, and strict regulatory compliance frameworks is essential for building trust and ensuring safe deployment of eHealth systems

- In addition, limited digital infrastructure, uneven internet penetration, and lack of standardized healthcare IT systems in certain countries create barriers to seamless implementation and interoperability of eHealth solutions

- While investments in healthcare IT are increasing, the relatively high implementation costs and the need for skilled personnel to manage digital systems can hinder adoption, particularly in resource-constrained settings

- Lack of awareness and digital literacy among healthcare professionals and patients further slows the adoption and effective utilization of eHealth technologies. Fragmented regulatory frameworks across different countries in the region also create challenges for standardization and cross-border interoperability of digital health systems

- Overcoming these challenges through strengthened cybersecurity measures, infrastructure development, regulatory support, and increased investment in digital health capabilities will be vital for sustained growth of the eHealth market in the region

Middle East and Africa eHealth Market Scope

The market is segmented on the basis of offering, deployment, enterprise size, functionality, technology, and end user.

- By Offering

On the basis of offering, the eHealth market is segmented into solutions and services. The solutions segment dominated the market with the largest market revenue share in 2025, driven by the increasing adoption of electronic health records (EHR), telemedicine platforms, and healthcare information systems across hospitals and clinics. Healthcare providers prefer integrated digital solutions that streamline operations, improve patient data management, and enhance care coordination. The rising need for centralized data platforms and interoperability between systems further strengthens the dominance of solutions. In addition, growing investments in digital health infrastructure and government-led digitization initiatives are accelerating the deployment of comprehensive eHealth software solutions across the region. The ability of these solutions to support real-time data access and analytics also contributes to their widespread adoption. The services segment is witnessing strong demand due to the need for implementation, integration, maintenance, and consulting support for eHealth systems.

The services segment is expected to witness the fastest growth rate during the forecast period, driven by increasing complexity of healthcare IT systems and the rising need for technical expertise to manage and optimize digital health platforms. Healthcare organizations are increasingly relying on third-party vendors for cloud migration, system integration, cybersecurity management, and ongoing support services. The growing adoption of outsourced IT services allows providers to focus on core healthcare delivery while ensuring efficient system performance. Furthermore, continuous upgrades, training requirements, and regulatory compliance needs are fueling the demand for professional and managed services in the eHealth ecosystem.

- By Deployment

On the basis of deployment, the eHealth market is segmented into cloud and on-premises. The cloud segment dominated the market with the largest market revenue share of 46.8% in 2025, driven by its scalability, cost-effectiveness, and ability to enable real-time data access across multiple healthcare facilities. Cloud-based eHealth solutions allow seamless integration of electronic health records, telemedicine platforms, and analytics tools, making them highly suitable for modern healthcare delivery. Healthcare providers prefer cloud deployment due to reduced infrastructure costs, easier updates, and improved interoperability. The increasing adoption of SaaS-based healthcare platforms and growing reliance on remote access to patient data are further strengthening the dominance of cloud solutions. In addition, cloud platforms support disaster recovery, data backup, and enhanced collaboration among healthcare professionals.

The on-premises segment is expected to witness the fastest growth rate during the forecast period, primarily driven by healthcare organizations with strict data security, privacy, and regulatory compliance requirements. Certain hospitals and government institutions prefer on-premises deployment to maintain full control over sensitive patient data and IT infrastructure. The need for customized system configurations and concerns regarding data sovereignty also contribute to the adoption of on-premises solutions. Furthermore, legacy systems in established healthcare facilities continue to rely on on-premises infrastructure, leading to gradual modernization and hybrid deployment models.

- By Enterprise Size

On the basis of enterprise size, the eHealth market is segmented into large enterprises and small and medium enterprises (SMEs). The large enterprises segment dominated the market with the largest revenue share in 2025, driven by their higher financial capacity to invest in advanced eHealth infrastructure, including integrated hospital management systems and AI-powered analytics platforms. Large healthcare providers and hospital networks are early adopters of digital health technologies due to their need for efficient patient management and operational scalability. These organizations also benefit from economies of scale and have dedicated IT teams to implement and maintain complex systems. Government hospitals and large private healthcare chains are increasingly deploying enterprise-wide digital solutions to improve service delivery and patient outcomes.

The small and medium enterprises segment is expected to witness the fastest growth rate during the forecast period, driven by increasing affordability of cloud-based eHealth solutions and growing awareness of digital healthcare benefits. SMEs, including small clinics and diagnostic centers, are adopting subscription-based models that require lower upfront investment. The availability of user-friendly and modular eHealth platforms is enabling smaller healthcare providers to digitize operations without extensive IT infrastructure. In addition, government initiatives supporting digital healthcare adoption among smaller providers are contributing to the rapid growth of this segment.

- By Functionality

On the basis of functionality, the eHealth market is segmented into content management system, group messaging, dashboard, video sessions, social support, and others. The video sessions segment dominated the market with the largest revenue share in 2025, driven by the widespread adoption of telemedicine and virtual consultations across the region. Video-based consultations enable real-time interaction between patients and healthcare professionals, improving accessibility, especially in remote and underserved areas. The growing demand for remote healthcare services, coupled with the convenience of virtual appointments, has made video sessions a core functionality of eHealth platforms. Integration with EHR systems and scheduling tools further enhances the effectiveness of video consultations.

The artificial intelligence (AI)-enabled functionalities segment, particularly under “others,” is expected to witness the fastest growth rate during the forecast period, driven by increasing use of AI for diagnostics, predictive analytics, and personalized treatment recommendations. AI-powered chatbots and decision-support systems are improving patient engagement and reducing the workload on healthcare professionals. The growing adoption of data-driven healthcare and real-time analytics is further accelerating the integration of advanced functionalities into eHealth platforms.

- By Technology

On the basis of technology, the eHealth market is segmented into Internet of Things (IoT), chatbots, artificial intelligence, blockchain, big data, and others. The artificial intelligence segment dominated the market with the largest revenue share in 2025, driven by its widespread application in diagnostics, patient monitoring, predictive analytics, and clinical decision support systems. AI technologies enable healthcare providers to analyze large volumes of patient data, identify patterns, and improve treatment outcomes. The increasing adoption of AI-powered tools in telemedicine and hospital management systems is strengthening its dominance. In addition, AI enhances operational efficiency and supports automation in healthcare workflows.

The Internet of Things (IoT) segment is expected to witness the fastest growth rate during the forecast period, driven by the rising adoption of connected medical devices, wearable health trackers, and remote monitoring systems. IoT enables continuous tracking of patient health parameters, allowing healthcare providers to monitor conditions in real time and respond proactively. The integration of IoT with cloud platforms and analytics tools is further enhancing its utility in chronic disease management and preventive healthcare.

- By End User

On the basis of end user, the eHealth market is segmented into healthcare providers, payers, healthcare consumers, pharmacies, and others. The healthcare providers segment dominated the market with the largest revenue share in 2025, driven by the widespread adoption of digital solutions by hospitals, clinics, and diagnostic centers to improve patient care and operational efficiency. Healthcare providers are the primary users of EHR systems, telemedicine platforms, and hospital management software, making them the key contributors to market demand. The need for efficient patient data management, workflow automation, and regulatory compliance further supports this segment’s dominance.

The healthcare consumers segment is expected to witness the fastest growth rate during the forecast period, driven by increasing awareness of digital health solutions, rising smartphone penetration, and growing demand for convenient access to healthcare services. Patients are increasingly using mobile health apps, teleconsultation platforms, and wearable devices to monitor their health and access medical services remotely. The shift toward patient-centric care and self-management of health conditions is accelerating the adoption of consumer-facing eHealth solutions across the region.

Middle East and Africa eHealth Market Regional Analysis

- United Arab Emirates dominated the eHealth market with the largest revenue share of 32.5% in 2025, characterized by advanced healthcare infrastructure, strong governmental support for digital transformation programs, and rapid adoption of telemedicine and electronic health record systems

- Healthcare providers and patients in the country highly value the convenience, efficiency, and integrated care capabilities offered by eHealth solutions such as electronic health records, telemedicine platforms, and AI-enabled health services

- This widespread adoption is further supported by high internet penetration, strong investment in healthcare IT, a technologically advanced population, and the growing preference for remote consultations and connected healthcare systems, establishing eHealth as a key component of the UAE’s modern healthcare ecosystem

The United Arab Emirates eHealth Market Insight

The United Arab Emirates eHealth market captured the largest revenue share in the Middle East and Africa in 2025, driven by strong government-led digital transformation initiatives and well-established healthcare infrastructure. The country has been at the forefront of adopting advanced digital health technologies, including telemedicine platforms, electronic health records, and AI-enabled healthcare systems. Healthcare providers and patients in the country highly value the convenience, efficiency, and seamless connectivity offered by integrated eHealth solutions. The widespread adoption is further supported by high internet penetration, strong investments in healthcare IT, and a technologically advanced population, along with increasing preference for remote consultations and data-driven healthcare services. This has positioned eHealth as a critical component of the UAE’s modern healthcare ecosystem.

Saudi Arabia eHealth Market Insight

The Saudi Arabia eHealth market is anticipated to grow at a substantial CAGR during the forecast period, driven by the country’s Vision 2030 initiatives aimed at digitalizing healthcare services and improving healthcare accessibility. The increasing focus on building smart hospitals, expanding telemedicine services, and implementing national electronic health record systems is significantly supporting market growth. Rising demand for efficient healthcare delivery, coupled with government support for digital transformation, is encouraging widespread adoption of eHealth solutions. In addition, the integration of advanced technologies such as AI, cloud computing, and IoT into healthcare systems is enhancing patient care and operational efficiency across healthcare institutions.

South Africa eHealth Market Insight

The South Africa eHealth market is expected to grow at a considerable CAGR during the forecast period, driven by increasing efforts to improve healthcare accessibility and infrastructure development. The country’s growing adoption of mobile health (mHealth) and telemedicine solutions is addressing challenges related to geographic disparities and limited access to healthcare services. Healthcare providers and consumers are increasingly leveraging digital platforms for remote consultations, patient monitoring, and health information management. Furthermore, rising awareness of digital healthcare benefits, improving internet connectivity, and government support for healthcare digitization are contributing to the expansion of the eHealth market in the country.

Nigeria eHealth Market Insight

The Nigeria eHealth market is expected to witness notable growth during the forecast period, driven by increasing demand for improved healthcare access in underserved and rural areas. The adoption of mobile-based health platforms and telemedicine services is gaining traction as a practical solution to bridge gaps in healthcare delivery. Healthcare providers are increasingly leveraging digital tools to enhance patient outreach, manage health records, and deliver remote consultations. In addition, growing smartphone penetration, expanding internet connectivity, and support from public-private partnerships are facilitating the adoption of eHealth solutions. Efforts to strengthen healthcare infrastructure and promote digital health awareness are further contributing to the market’s growth in the country.

Middle East and Africa eHealth Market Share

The Middle East and Africa eHealth industry is primarily led by well-established companies, including:

- Tencent Holdings Limited (China)

- Alibaba Health Information Technology Limited (China)

- WeDoctor Holdings Limited (China)

- JD Health International Inc (China)

- Practo Technologies Pvt. Ltd (India)

- HealthifyMe (India)

- mFine (India)

- Halodoc (Indonesia)

- MyDoc Pte. Ltd (Singapore)

- Samsung Electronics Co. Ltd (South Korea)

- Koninklijke Philips N.V. (Netherlands)

- Cisco Systems, Inc. (U.S.)

- IBM Corporation (U.S.)

- Epic Systems Corporation (U.S.)

- Allscripts Healthcare, LLC (U.S.)

- McKesson Corporation (U.S.)

- AT&T Inc. (U.S.)

- QSI Management, LLC (U.S.)

- Vodafone Group Plc (U.K.)

What are the Recent Developments in Middle East and Africa eHealth Market?

- In January 2026, discussions at regional healthcare IT forums focused on owning digital health’s future in the Middle East, urging countries to scale up local digital health innovations and workforce capabilities to support long-term eHealth growth and reduce dependence on imported technologies

- In August 2025, MedQuick, a UAE-based health tech innovator, expanded its digital health ecosystem by launching a new telemedicine app alongside MedLink, a portable tele-diagnostic and lab diagnostic bag designed to modernize healthcare delivery and improve patient access across the Middle East region

- In December 2024, Arab Health 2025 was announced to spotlight how AI, telemedicine, and robotics are transforming healthcare delivery across the Middle East, highlighting digital healthcare innovations and their role in improving patient care and operational efficiency in countries such as the UAE, Saudi Arabia, and Qatar

- In October 2024, the rise of telemedicine and virtual care in the MENA region was documented, showing a significant transformation in healthcare delivery driven by telehealth platforms that expand access to care and support remote consultations across the Middle East and North Africa

- In March 2023, the MENA Telehealth Conference 2023 concluded in Dubai, bringing together healthcare regulators, telemedicine service providers, and technology leaders to showcase rapid progress in telehealth adoption and digital health solutions across the Middle East and North Africa region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.