Middle East And Africa Health Insurance Market

Market Size in USD Billion

CAGR :

%

USD

160.90 Billion

USD

215.17 Billion

2025

2033

USD

160.90 Billion

USD

215.17 Billion

2025

2033

| 2026 –2033 | |

| USD 160.90 Billion | |

| USD 215.17 Billion | |

| % | |

|

Middle East and Africa Health Insurance Market Size

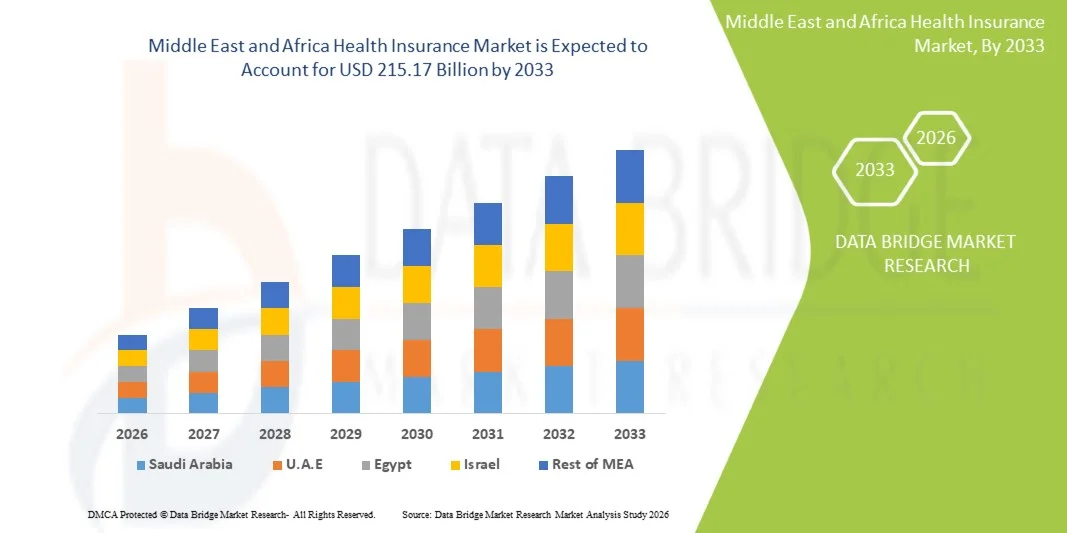

- The Middle East and Africa health insurance market size was valued at USD 160.90 billion in 2025 and is expected to reach USD 215.17 billion by 2033, at a CAGR of 3.70% during the forecast period

- The market growth is largely fueled by increasing awareness of health coverage, rising healthcare costs, and government initiatives promoting insurance penetration across the region, leading to higher adoption of health insurance solutions in both urban and rural populations

- Furthermore, growing demand for comprehensive, affordable, and digitally-enabled health insurance plans is driving insurers to innovate and expand their offerings. These converging factors are accelerating the uptake of health insurance products, thereby significantly boosting the industry's growth

Middle East and Africa Health Insurance Market Analysis

- Health insurance, providing financial coverage for medical expenses and access to healthcare services, is becoming increasingly critical across Middle East and Africa due to rising healthcare costs, expanding private healthcare facilities, and growing awareness of the benefits of insurance in mitigating out-of-pocket expenditures

- The accelerating demand for health insurance is primarily driven by government initiatives to expand coverage, increasing prevalence of chronic diseases, and rising consumer preference for comprehensive, affordable, and digitally-enabled insurance solutions

- United Arab Emirates dominated the Middle East and Africa health insurance market with the largest revenue share of 38.5% in 2025, characterized by high healthcare spending, mandatory insurance regulations, and a strong presence of leading insurers, with significant growth in policy adoption due to mandatory health coverage for residents and corporate employees

- South Africa is expected to be the fastest-growing country in the health insurance market during the forecast period due to increasing government-backed insurance schemes, rising middle-class population, and improving healthcare infrastructure

- Private health insurance providers segment dominated the market with a share of 46.8% in 2025, driven by its comprehensive coverage options, flexibility, and growing partnerships between insurers and healthcare providers

Report Scope and Middle East and Africa Health Insurance Market Segmentation

|

Attributes |

Middle East and Africa Health Insurance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Health Insurance Market Trends

“Digital Transformation and Telehealth Integration”

- A significant and accelerating trend in the Middle East and Africa health insurance market is the growing adoption of digital platforms and telehealth solutions, enabling policyholders to access healthcare services and insurance management remotely

- For instance, the UAE-based Daman Health integrates telemedicine consultations with its insurance plans, allowing members to receive virtual doctor visits and claim processing through a mobile app

- Digital health platforms enable insurers to analyze patient data, offer personalized wellness programs, and streamline claims management, enhancing user convenience and engagement. For instance, Discovery Health in South Africa leverages digital health tools to monitor chronic conditions and provide proactive health insights

- The integration of telehealth with insurance plans facilitates centralized management of health services, allowing policyholders to schedule appointments, track claims, and access preventive care resources through a single interface

- This trend toward more connected, technology-driven, and patient-centric insurance services is reshaping consumer expectations, prompting insurers to develop app-based platforms with AI-enabled health assessments and virtual care options

- The demand for health insurance solutions that offer seamless digital access and telehealth integration is growing rapidly across both individual and corporate sectors, as consumers increasingly prioritize convenience and comprehensive healthcare management

- Expansion of cloud-based claims processing and AI-powered underwriting is enabling faster approvals and customized coverage, improving overall customer experience. For instance, AXA Gulf utilizes AI-driven platforms to streamline claims and policy issuance for corporate clients

Middle East and Africa Health Insurance Market Dynamics

Driver

“Increasing Healthcare Costs and Awareness of Insurance Benefits”

- The rising cost of healthcare services across Middle East and Africa, coupled with growing awareness of insurance benefits, is a key driver fueling the adoption of health insurance products

- For instance, in March 2025, Saudi Arabia’s Council of Cooperative Health Insurance launched awareness campaigns highlighting mandatory insurance coverage for residents and expatriates, boosting policy uptake

- As consumers seek to mitigate out-of-pocket expenses and secure access to quality care, health insurance plans offer financial protection, wellness programs, and coverage for chronic disease management

- Furthermore, government regulations and incentives promoting insurance enrollment are encouraging individuals and companies to adopt health coverage, integrating it into employee benefits packages and family health plans

- The convenience of digital enrollment, flexible coverage options, and partnerships with hospitals and clinics are key factors driving market growth across both urban and rural populations

- Increasing demand from the growing expatriate workforce in GCC countries is pushing insurers to offer tailored corporate health plans that meet diverse employee needs. For instance, multinational companies in UAE and Qatar are mandating comprehensive health coverage for foreign staff

- Rising incidence of lifestyle diseases such as diabetes and cardiovascular disorders is prompting individuals to seek preventive and comprehensive insurance solutions. For instance, insurers in South Africa are introducing chronic disease management programs within their plans

Restraint/Challenge

“Limited Insurance Penetration and Regulatory Fragmentation”

- Low insurance penetration in several countries and fragmented regulatory frameworks present significant challenges to the expansion of health insurance in the Middle East and Africa

- For instance, reports indicate that in parts of Sub-Saharan Africa, only a small percentage of the population has formal health insurance, limiting market growth opportunities

- Inconsistent regulations across countries create compliance complexities for insurers operating regionally, affecting product standardization and cross-border expansion. For instance, insurers entering Nigeria face diverse state-level requirements that complicate uniform policy offerings

- Affordability remains a barrier, as high premiums can deter low-income households from purchasing coverage, especially in countries without government subsidies or employer-sponsored plans

- Overcoming these challenges through regulatory harmonization, targeted awareness campaigns, and development of low-cost, accessible insurance products will be essential for sustained market growth

- Limited digital literacy in rural and semi-urban areas hampers adoption of app-based and telehealth insurance solutions. For instance, some rural communities in Kenya struggle to navigate online enrollment and claims processes

- Political instability and economic fluctuations in certain countries can disrupt insurance operations, reduce consumer confidence, and delay expansion plans. For instance, insurers in parts of North Africa face challenges during periods of economic uncertainty

Middle East and Africa Health Insurance Market Scope

The market is segmented on the basis of type, services, level of coverage, service providers, health insurance plans, demographics, coverage type, end user, and distribution channel.

- By Type

On the basis of type, the market is segmented into products and solutions. The products segment dominated the market in 2025 due to widespread adoption of standalone health insurance policies offering financial coverage for hospitalization, outpatient care, and chronic disease management. Consumers prefer products for their structured coverage, transparency in premiums, and ease of understanding, especially in GCC countries with high awareness of insurance benefits. Regulatory frameworks in countries such as UAE and Saudi Arabia have standardized these products, making them widely trusted. Insurers also bundle additional services such as wellness programs, telemedicine access, and emergency medical support, further enhancing appeal. Corporates and individuals increasingly rely on product-based insurance for predictable coverage and budget management. Product-based policies also benefit from strong marketing and brand recognition, contributing to market dominance.

The solutions segment is expected to witness the fastest growth from 2026 to 2033, driven by rising demand for integrated healthcare and insurance services. These solutions combine insurance coverage with digital health platforms, AI-enabled health assessments, and preventive care programs. Consumers and corporates increasingly seek personalized solutions that address both financial protection and proactive health management. App-based platforms and telemedicine integration enhance convenience and accessibility, particularly in urban areas. Health insurers are innovating with solutions that monitor patient health, provide reminders for check-ups, and offer chronic disease management support. Rising digital literacy and smartphone penetration are further accelerating adoption of solution-based insurance offerings in the region.

- By Services

On the basis of services, the market is segmented into inpatient treatment, outpatient treatment, medical assistance, and others. The inpatient treatment segment dominated in 2025 due to the high costs associated with hospitalization, surgeries, and emergency care. Consumers in UAE, Saudi Arabia, and South Africa prefer plans covering hospital stays and critical care, minimizing out-of-pocket payments. Mandatory insurance regulations for expatriates and employees in GCC countries drive large-scale adoption. Insurers often include value-added services such as hospital network access, room upgrades, and pre-authorization support to enhance attractiveness. Inpatient coverage remains essential for financial protection against severe health events. This segment contributes significantly to overall revenue due to higher premiums and broader utilization.

The outpatient treatment segment is expected to witness the fastest growth during the forecast period, driven by rising demand for consultations, diagnostics, and minor procedures. Telemedicine adoption and preventive care programs are fueling growth, particularly in urban areas. Outpatient coverage appeals to policyholders seeking affordable and convenient day-to-day healthcare. Insurers are increasingly including wellness programs, vaccination coverage, and routine health check-ups to attract customers. Digital platforms that provide remote consultation and e-prescriptions enhance the segment’s adoption. Corporates offering outpatient benefits for employees also support rapid growth in this segment.

- By Level of Coverage

On the basis of level of coverage, the market is segmented into bronze, silver, gold, and platinum. The gold segment dominated in 2025 due to its balanced premium affordability and comprehensive benefits, including hospitalization, outpatient care, and wellness programs. Corporates often adopt gold-tier plans for employees, while high-income individuals prefer them for family coverage. Gold plans also include telemedicine and chronic disease management benefits, making them attractive across demographics. Insurers actively promote gold plans digitally and through corporate tie-ups. International coverage options in gold-tier plans further enhance adoption in GCC countries. The combination of affordability and comprehensive benefits ensures dominance of this segment.

The platinum segment is expected to witness the fastest growth from 2026 to 2033, driven by demand for premium, all-inclusive insurance coverage among high-net-worth individuals and expatriates. Platinum plans provide global coverage, concierge healthcare services, and advanced telehealth options. Rising affluence and medical tourism in GCC countries increase adoption. Platinum policies appeal to individuals seeking maximum protection with minimal out-of-pocket expenses. Insurers are marketing these plans with additional wellness and preventive benefits to attract premium customers. Growth is also fueled by corporates offering elite plans for top executives and international staff.

- By Service Providers

On the basis of service providers, the market is segmented into public health insurance providers and private health insurance providers. The private providers segment dominated in 2025 with a market share of 46.8% due to a wide range of plan options, faster claim processing, and value-added services such as telemedicine and wellness programs. Private insurers cater to both corporates and individuals, offering flexible coverage across multiple healthcare facilities. Countries such as UAE and South Africa have strong private insurer presence, boosting market share. Private insurers are more agile in product innovation and digital adoption, enhancing customer satisfaction. Their partnerships with hospitals and clinics ensure better service accessibility, supporting dominance. Marketing and brand visibility also contribute to widespread adoption.

The public providers segment is expected to witness the fastest growth from 2026 to 2033, due to government initiatives expanding insurance coverage to underserved populations. Programs in Saudi Arabia, Kenya, and other countries aim to increase enrollment through mandatory policies and subsidies. Public insurance schemes focus on affordability, accessibility, and inclusivity, helping low-income and rural populations. Digital enrollment platforms and mobile-based services are enhancing adoption. Partnerships with private insurers for networked service delivery are also expanding reach. Rising government spending on health and insurance awareness campaigns drives this segment’s rapid growth.

- By Health Insurance Plans

On the basis of plans, the market is segmented into POS, EPOS, Indemnity, HSA, QSEHRAs, PPO, HMO, and others. The HMO segment dominated in 2025 due to its structured network of providers, cost efficiency, and preventive care coverage. Corporates in UAE and GCC countries frequently adopt HMO plans for employee benefits. Coordinated care, centralized claims processing, and inclusion of telemedicine enhance its appeal. HMOs also provide chronic disease management and wellness programs, increasing their attractiveness. Wide hospital and clinic networks strengthen adoption. Policyholders value predictability of costs and services, consolidating dominance.

The PPO segment is expected to witness the fastest growth from 2026 to 2033, due to flexibility in choosing healthcare providers and facilities. Expatriates and high-income individuals prefer PPOs for freedom of provider choice. Insurers enhance PPO offerings with telemedicine, wellness, and international coverage. Increasing awareness of personalized healthcare drives adoption. PPO plans also attract corporate clients looking for employee satisfaction and mobility. Digital platforms facilitate easy claims and network access, accelerating growth.

- By Demographics

On the basis of demographics, the market is segmented into adults, minors, and senior citizens. The adults segment dominated in 2025 due to higher awareness of health risks, disposable income, and responsibility for family coverage. Adults, particularly working professionals, are primary policy purchasers. Corporate plans contribute to dominance. Insurance policies for adults often include outpatient, inpatient, and preventive services. The segment benefits from both individual and family coverage. Awareness campaigns and regulatory requirements support widespread adoption.

The senior citizens segment is expected to witness the fastest growth from 2026 to 2033, due to aging populations, rising chronic disease prevalence, and higher healthcare expenditure. Specialized plans for seniors cover age-related conditions, home healthcare, and preventive care. Insurers in UAE and South Africa are targeting seniors with tailored products. Digital platforms and concierge services enhance accessibility. Rising life expectancy drives long-term insurance demand. Government and private schemes increasingly focus on senior coverage, accelerating adoption.

- By Coverage Type

On the basis of coverage type, the market is segmented into lifetime coverage and term coverage. The term coverage segment dominated in 2025 due to affordability, flexible durations, and suitability for corporates and individuals. Term policies appeal to young adults seeking coverage for specific periods or projects. Short-term and renewable plans allow easy management of premiums. Policyholders benefit from predictable costs and simple claims. Term coverage is popular in mandatory corporate insurance schemes. Market familiarity and ease of purchase further support dominance.

The lifetime coverage segment is expected to witness the fastest growth from 2026 to 2033, driven by long-term financial protection needs and post-retirement healthcare security. Insurers offer lifetime policies with wellness and chronic disease management benefits. High-net-worth individuals prefer lifetime coverage for comprehensive security. Aging populations in GCC and South Africa drive demand. Insurers are enhancing digital tools for claims and policy management. Growth is also fueled by increasing awareness of long-term health risks.

- By End User

On the basis of end user, the market is segmented into corporates, individuals, and others. The corporates segment dominated in 2025 due to employer-mandated insurance, rising workforce health needs, and inclusion of benefits in compensation packages. Large organizations negotiate group policies, driving high market revenue. Corporates also benefit from cost predictability and streamlined claims. Employee wellness programs further support adoption. Insurers actively target corporate clients through digital and direct sales. Regulatory mandates in GCC countries reinforce corporate adoption.

The individuals segment is expected to witness the fastest growth from 2026 to 2033, due to increasing health awareness, digital insurance platforms, and expanding middle-class populations. Individuals prefer personal plans offering flexibility and tailored benefits. Smartphone apps and online portals make purchase and claim processes convenient. Health-conscious consumers seek preventive care coverage. Digital marketing and telemedicine integration are fueling rapid adoption. Policies for freelancers and small business owners also drive growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct sales, financial institutions, e-commerce, hospitals, clinics, and others. The direct sales segment dominated in 2025 due to strong insurer-client relationships, personalized advisory services, and customized corporate offerings. Insurers actively engage with both individual and corporate clients, improving penetration. Direct sales teams explain complex policy terms and coverage benefits, enhancing trust. High-value clients often prefer face-to-face interactions. Marketing campaigns reinforce brand visibility. Accessibility of agents and brokers contributes to segment dominance.

The e-commerce segment is expected to witness the fastest growth from 2026 to 2033, due to rising digital adoption, mobile-based policy purchases, and online claim management. Insurers are investing in easy-to-use digital platforms that provide instant quotes, policy comparison, and claims processing. Urban populations increasingly prefer online channels for convenience. App-based enrollment simplifies access to coverage for tech-savvy consumers. Telemedicine integration with e-commerce platforms enhances value. Digital adoption trends in GCC and South Africa accelerate segment growth.

Middle East and Africa Health Insurance Market Regional Analysis

- United Arab Emirates dominated the Middle East and Africa health insurance market with the largest revenue share of 38.5% in 2025, characterized by high healthcare spending, mandatory insurance regulations, and a strong presence of leading insurers, with significant growth in policy adoption due to mandatory health coverage for residents and corporate employees

- Consumers in the UAE increasingly value comprehensive coverage, access to private healthcare networks, and integrated wellness programs offered by health insurance providers. Corporate-sponsored policies and employer-mandated coverage further enhance adoption

- This widespread uptake is supported by strong government initiatives, rising healthcare costs, and increasing demand for digital insurance solutions, establishing health insurance as a critical financial and healthcare planning tool for both individuals and corporates in the UAE

The UAE Health Insurance Market Insight

The UAE health insurance market captured the largest revenue share of 38.5% in 2025 within the Middle East and Africa region, fueled by mandatory health insurance regulations for residents and expatriates, rising healthcare costs, and growing awareness of insurance benefits. Consumers are increasingly prioritizing comprehensive coverage, access to private healthcare networks, and integrated wellness programs. The growing trend of corporate-sponsored insurance and digitally-enabled policy management further propels the market. Moreover, the UAE government’s initiatives to expand healthcare access and promote insurance adoption are significantly contributing to market growth.

Saudi Arabia Health Insurance Market Insight

The Saudi Arabia health insurance market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by mandatory cooperative health insurance for employees and residents, increasing urbanization, and rising private healthcare infrastructure. Consumers are drawn to comprehensive plans covering hospitalization, outpatient care, and chronic disease management. Digital platforms for claims processing and policy management are fostering adoption. The demand is also growing across corporate, individual, and expatriate segments. In addition, ongoing healthcare reforms and investments in medical facilities are stimulating market expansion.

Egypt Health Insurance Market Insight

The Egypt health insurance market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising healthcare awareness, government-led insurance initiatives, and increasing private sector participation. Concerns regarding high out-of-pocket medical expenses are encouraging individuals and families to adopt health insurance. The government’s introduction of social health insurance programs and partnerships with private insurers enhances accessibility. Urban populations show a higher preference for digital enrollment and cashless claim facilities. The growth of corporate insurance coverage and voluntary health plans is also contributing to market development.

South Africa Health Insurance Market Insight

The South Africa health insurance market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing private healthcare demand, rising chronic disease prevalence, and growing awareness of insurance benefits. South African consumers value plans offering extensive hospital networks, preventive care, and wellness programs. Corporate-sponsored group schemes are widely adopted across industries. Digital and mobile-enabled policy management is becoming prevalent, supporting faster enrollment and claims processing. The integration of health insurance with telemedicine and chronic care management programs is further driving adoption. Sustainability and affordability initiatives by insurers are attracting a broader customer base.

Middle East and Africa Health Insurance Market Share

The Middle East and Africa Health Insurance industry is primarily led by well-established companies, including:

- Bupa Arabia (Saudi Arabia)

- The National Insurance Company (UAE)

- Abu Dhabi National Insurance Company (UAE)

- Qatar Insurance Group (Qatar)

- Sanlam Limited (South Africa)

- Allianz Group (Germany)

- Iran Insurance Company (Iran)

- Orient Insurance PJSC (UAE)

- AXA (France)

- Cigna Healthcare Middle East (UAE)

- Aetna Inc. (U.S.)

- Now Health International (Hong Kong)

- Centene Corporation (U.S.)

- Anthem Insurance Companies, Inc. (U.S.)

- Broadstone Corporate Benefits Limited (U.K.)

- Vitality (U.K.)

- International Medical Group, Inc. (U.S.)

- Vhi Group (Ireland)

- The Company for Cooperative Insurance (Saudi Arabia)

What are the Recent Developments in Middle East and Africa Health Insurance Market?

- In October 2025, Vitalls and MSH MENA signed a Memorandum of Understanding (MoU) in Dubai to collaborate on integrated administrative health solutions that enhance cross‑border health insurance services for expatriates, multinational corporations, and global citizens

- In May 2025, the WHO Foundation signed its first corporate partnership in the GCC region with Tawuniya, Saudi Arabia’s largest insurer, to advance health innovation and digital healthcare delivery across the Eastern Mediterranean. The agreement focuses on leveraging AI, digital platforms, and evidence‑based strategies to improve care delivery and health outcomes

- In November 2023, Cigna Healthcare announced a strategic partnership with AAR Insurance Kenya to deliver expanded and innovative health insurance services in East Africa, blending global insurance expertise with local market knowledge to improve access to care

- In July 2023, the Egyptian government greenlit the first phase of its Comprehensive Health Insurance System, backed by a US$1.09 billion investment in health infrastructure that will include hundreds of facilities and expand insured services at primary, secondary, and tertiary levels

- In June 2023, Esaal (an online health and wellness platform) and Allianz Insurance Egypt launched an exclusive partnership to integrate mental health and nutrition consultations into health insurance offerings expanding holistic care services available to policyholders in Egypt and across the MENA region

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.