Middle East And Africa Obsessive Compulsive Disorder Ocd Drug Market

Market Size in USD Million

USD

21.12 Million

USD

39.39 Million

2025

2033

USD

21.12 Million

USD

39.39 Million

2025

2033

| 2026 - 2033 | |

| USD 21.12 Million | |

| USD 39.39 Million | |

| % | |

|

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Size

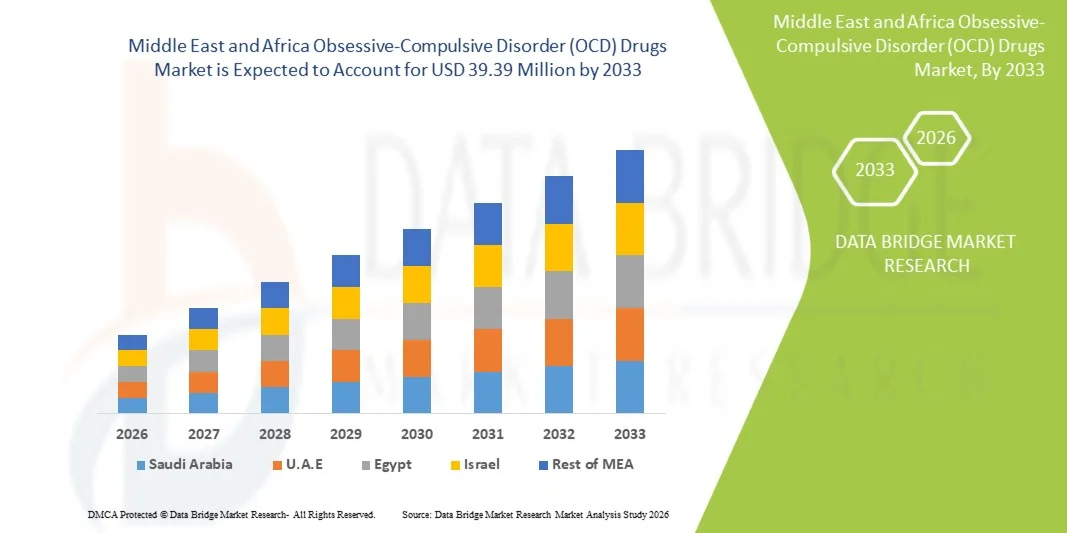

- The Middle East and Africa Obsessive-Compulsive Disorder (OCD) drugs market size was valued at USD 21.12 million in 2025 and is expected to reach USD 39.39 million by 2033, at a CAGR of 8.1% during the forecast period

- The market growth is largely fueled by increasing awareness of mental health conditions,grea ter healthcare investment in the region, and expanding availability of novel pharmacotherapies and supportive treatments in both community and institutional settings

- Furthermore, converging factors such as higher diagnosis rates of OCD, improved access to treatment services, and the development of more patient‑friendly, integrated mental‑health solutions are positioning OCD drug therapies as the modern standard for access control in mental‑health care in the MEA region. These combined factors are accelerating uptake of OCD drug treatments in the region, thereby significantly boosting the industry’s growth

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Analysis

- Obsessive‑Compulsive Disorder (OCD) drugs, including antidepressants, antipsychotics, and NMDA blockers, are increasingly vital components of mental health care in both hospital and outpatient settings in the Middle East & Africa (MEA) region due to their established efficacy, improved patient adherence, and integration with broader psychiatric care programs

- The escalating demand for OCD drugs is primarily fueled by rising prevalence of OCD, growing awareness of mental health disorders, and expanding access to healthcare infrastructure and specialist clinics across MEA countries

- Saudi Arabia dominated the MEA OCD drugs market with the largest revenue share of 35.1% in 2025, characterized by high healthcare expenditure, strong presence of key pharmaceutical players, and substantial adoption of OCD treatments in both urban hospitals and specialty clinics

- United Arab Emirates (UAE) is expected to be the fastest growing country in the MEA OCD drugs market during the forecast period due to improving mental health awareness, expansion of psychiatric care facilities, and rising patient affordability for prescription therapies

- Antidepressants segment dominated the MEA OCD drugs market with a market share of 60.5% in 2025, driven by their proven efficacy, safety profile, and strong physician preference as the first-line treatment option for OCD patients

Report Scope and Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Segmentation

|

Attributes |

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Trends

“Rising Adoption of Digital Therapeutics and Telepsychiatry”

- A significant and accelerating trend in the MEA OCD drugs market is the growing integration of digital therapeutics, telepsychiatry, and mobile health platforms with traditional pharmacological treatments. This approach enhances treatment adherence, patient monitoring, and overall therapy outcomes

- For instance, telepsychiatry programs in the UAE and Saudi Arabia allow patients to consult psychiatrists remotely while receiving prescriptions for OCD drugs, improving access for patients in remote areas

- Mobile health applications are increasingly being used to monitor medication schedules, track symptom severity, and provide cognitive behavioral therapy (CBT) support alongside prescribed drugs. For instance, digital CBT apps complement antidepressant therapy to improve patient adherence and outcomes

- The integration of telehealth and digital adherence platforms enables healthcare providers to remotely monitor patient responses to OCD drugs, make timely dose adjustments, and provide counseling, improving clinical effectiveness and patient satisfaction

- This trend towards combining digital solutions with traditional pharmacotherapy is reshaping treatment expectations and improving access, particularly in regions with limited specialist availability. For instance, platforms such as CuraCoach are being piloted to support OCD management in Saudi Arabia and UAE

- The demand for integrated digital and drug-based OCD therapies is rising rapidly across both urban and semi-urban populations, as patients increasingly prioritize convenience, accessibility, and comprehensive care solutions

- Partnerships between pharmaceutical companies and telehealth platforms are increasing in the MEA region to expand patient reach and deliver combined digital and drug-based therapy packages efficiently

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Dynamics

Driver

“Increasing Prevalence and Awareness of OCD Disorders”

- The increasing prevalence of OCD in the MEA region, coupled with growing awareness of mental health disorders, is a significant driver of heightened demand for OCD drugs

- For instance, in 2024, the Saudi Ministry of Health reported rising OCD diagnosis rates, prompting hospitals and clinics to expand psychiatric services and prescription access

- As patients and caregivers become more aware of OCD symptoms, demand for effective pharmacological interventions such as antidepressants and antipsychotics rises, offering a reliable treatment option

- Furthermore, government initiatives and NGO programs promoting mental health awareness are facilitating earlier diagnosis and treatment uptake, integrating both hospital-based and home-based care

- The increasing availability of specialist psychiatric clinics and mental health infrastructure across countries such as Saudi Arabia, UAE, and South Africa is enabling broader access to OCD therapies, thereby boosting drug adoption

- The adoption of evidence-based treatment guidelines, coupled with training for psychiatrists and general practitioners, is further reinforcing the use of OCD drugs across patient populations

- For instance, public-private collaborations are being implemented to improve access to OCD medications in underserved areas, particularly in North African countries

- Growing insurance coverage for mental health services in select MEA countries is improving affordability and driving higher uptake of OCD drugs among insured populations

Restraint/Challenge

“High Treatment Costs and Limited Mental Health Infrastructure”

- The high cost of prescription OCD drugs and the limited availability of specialized mental health infrastructure pose significant challenges to widespread market penetration in the MEA region

- For instance, imported antidepressants and antipsychotics often carry premium pricing in countries such as Saudi Arabia and UAE, making access difficult for lower-income patients

- Limited psychiatric workforce and uneven distribution of clinics across rural and semi-urban areas restrict patient access to diagnosis, consultation, and follow-up care

- In addition, cultural stigma and low awareness in certain MEA countries hinder early intervention and adherence to long-term OCD drug therapy. For instance, surveys in some North African countries indicate patients often delay seeking treatment due to social stigma

- Regulatory challenges, including lengthy drug approval processes and import restrictions, can further slow the introduction of newer or advanced pharmacotherapies in the region

- Overcoming these challenges through subsidy programs, increased psychiatric training, and public awareness campaigns will be critical to sustaining market growth and improving patient outcomes

- For instance, insufficient funding for mental health programs in some MEA countries limits expansion of OCD treatment centers, reducing accessibility for patients in remote regions

- Complex logistics and supply chain issues for importing specialty drugs create delays and inconsistencies in availability, particularly in sub-Saharan Africa, posing a challenge for continuous treatment adherence

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Scope

The market is segmented on the basis of severity, sub-type, drugs, route of administration, population type, end user, and distribution channel.

- By Severity

On the basis of severity, the MEA OCD drugs market is segmented into mild to moderate and moderate to severe. The Moderate to Severe segment dominated the market with the largest revenue share in 2025, driven by a higher prevalence of severe OCD cases in hospitals and specialty clinics. Patients in this segment often require combination therapies or higher dosages, increasing overall market value. Healthcare providers prioritize treatment for moderate to severe cases due to higher risk and symptom intensity. Delays in diagnosis or access to care in some MEA countries contribute to more patients presenting at advanced stages. Established treatment protocols and physician familiarity with severe cases further reinforce dominance. Therefore, the Moderate to Severe segment is the largest by revenue in the region.

The Mild to Moderate segment is expected to witness the fastest growth from 2026 to 2033, fueled by increased awareness, early screening programs, and telepsychiatry adoption. Patients with milder symptoms are now more such asly to seek treatment, expanding the target population. Community clinics and outpatient services provide accessible options for early-stage treatment. Public health initiatives promoting mental health awareness support adoption of pharmacotherapy in this segment. Pharmaceutical companies are introducing low-dose, outpatient-friendly medications to serve this patient pool. Consequently, Mild to Moderate is projected as the fastest-growing severity segment.

- By Sub-Type

On the basis of sub-type, the market is segmented into contamination obsessions with washing/cleaning compulsion, harm obsessions with checking compulsions, obsessions without visible compulsions, symmetry obsessions with ordering, arranging and counting compulsions, hoarding, and others. The Contamination Obsessions with Washing/Cleaning Compulsion segment dominated the market in 2025, due to higher patient awareness and the visible nature of compulsive behavior. Post-COVID hygiene awareness has increased recognition of this sub-type in both urban and semi-urban areas. Patients with contamination-related OCD often seek medical attention sooner, leading to higher drug adoption. Hospitals and specialty clinics report higher diagnosis and treatment rates for this sub-type. Physicians and pharma companies focus on established treatment guidelines, reinforcing market dominance. Consequently, this sub-type holds the largest revenue share in MEA.

The Hoarding sub-type is expected to witness the fastest growth from 2026 to 2033, as mental health literacy improves and underreported cases are increasingly diagnosed. Hoarding often requires combination therapy, which increases drug uptake. Urbanization and housing density amplify demand for treatment. Emerging telepsychiatry and digital therapy programs expand access to previously untreated patients. Awareness campaigns targeting hoarding-related OCD further accelerate adoption. Therefore, Hoarding is projected as the fastest-growing sub-type segment.

- By Drugs

On the basis of drugs, the market is segmented into antidepressants, antipsychotics, nmda blockers, and others. The Antidepressants segment dominated the market with the largest share of 60.5% in 2025, due to clinical guideline recommendations that designate them as first-line therapy for OCD. Generic availability increases accessibility across MEA countries. Physicians rely on antidepressants for both outpatient and inpatient cases. Hospitals and specialty clinics prioritize these drugs for moderate and severe OCD cases. Established safety profiles and long-standing physician familiarity support their dominant position. Consequently, antidepressants are the largest drug-type segment.

The NMDA Blockers segment is expected to witness the fastest growth from 2026 to 2033, driven by rising demand for treatment-resistant OCD therapies. Hospitals and specialty clinics are introducing NMDA blockers as adjunct therapy. Novel therapies and pipeline approvals provide a first-mover advantage in the region. Patients with severe or refractory OCD benefit from NMDA blockers, boosting adoption. Emerging clinical guidelines support integration with existing treatments. Therefore, NMDA blockers are projected as the fastest-growing drug sub-segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The Oral segment dominated the market in 2025, due to convenience, ease of self-administration, and outpatient treatment preference. Oral drugs are widely available in hospitals, retail, and specialty pharmacies. Patients show higher adherence with oral formulations. Regulatory approvals and established physician familiarity favor oral medications. Hospitals and clinics manage large volumes of oral prescriptions efficiently. Therefore, oral administration remains the largest route segment.

The Parenteral segment is expected to witness the fastest growth from 2026 to 2033, due to rising adoption in severe or treatment-resistant cases. Hospitals and specialty clinics provide parenteral therapies for rapid onset or controlled dosing. New injectable formulations entering MEA markets enhance adoption. Telemedicine and hospital-based monitoring support safe use of parenteral drugs. Growing clinical evidence supports parenteral use in complex cases. Hence, parenteral is projected as the fastest-growing administration route.

- By Population Type

On the basis of population type, the market is segmented into pediatrics and adults. The Adults segment dominated the market in 2025, as OCD prevalence is higher in adults compared to children. Hospitals and specialty clinics primarily focus on adult psychiatric care. Established dosing protocols and outpatient treatment options favor adults. Awareness campaigns and screening programs often target adult populations. Severe and moderate cases mostly present in adults, reinforcing dominance. Consequently, adults remain the largest population segment.

The Pediatrics segment is expected to witness the fastest growth from 2026 to 2033, driven by increased screening and early diagnosis in schools and clinics. Pediatric-specific formulations are being introduced in MEA markets. Parents and caregivers are more such asly to seek treatment for children with OCD. Telepsychiatry and home-based programs expand access to pediatric patients. Early treatment interventions improve outcomes and adherence. Therefore, pediatrics is projected as the fastest-growing population segment.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, home healthcare, and others. The Hospitals segment dominated the market in 2025, due to infrastructure, psychiatric departments, and ability to manage severe OCD cases. Hospitals provide initial treatment, monitoring, and dispensing of OCD drugs. Referral and tertiary care cases are concentrated in hospitals. Complex therapies and combination treatments are hospital-centric. Government and private hospitals in MEA control procurement and distribution. Consequently, hospitals remain the largest end-user segment.

The Home Healthcare segment is expected to witness the fastest growth from 2026 to 2033, driven by telepsychiatry, remote monitoring, and increasing preference for treatment at home. Outpatient and home-based programs expand patient access. E-prescription and delivery services support medication adherence. Home-based care improves convenience and privacy for patients. Community mental health initiatives also promote adoption. Therefore, home healthcare is projected as the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment dominated the market in 2025, as hospitals dispense specialty psychiatric medications and manage prescriptions. Hospital pharmacies serve both inpatient and outpatient cases. High-cost or complex therapies are usually hospital-dispensed. Regulatory frameworks favor hospital pharmacies. Close physician coordination ensures effective treatment delivery. Consequently, hospital pharmacy remains the largest distribution channel.

The Online Pharmacy segment is expected to witness the fastest growth from 2026 to 2033, due to increasing digital adoption, telehealth, and home delivery of OCD drugs. Patients in remote areas gain convenient access. E-pharmacy partnerships with hospitals and clinics facilitate market expansion. Regulatory liberalization in some MEA countries supports online drug sales. Home delivery and subscription models enhance adherence. Therefore, online pharmacy is projected as the fastest-growing distribution channel.

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Regional Analysis

- Saudi Arabia dominated the MEA OCD drugs market with the largest revenue share of 35.1% in 2025, characterized by high healthcare expenditure, strong presence of key pharmaceutical players, and substantial adoption of OCD treatments in both urban hospitals and specialty clinics

- Patients and healthcare providers in the region highly value the availability of guideline-based pharmacological treatments, easy access to hospitals and specialty clinics, and the integration of telepsychiatry services for monitoring and follow-up

- This widespread adoption is further supported by government initiatives promoting mental health awareness, rising private healthcare investment, and increasing demand for effective management of moderate to severe OCD cases, establishing pharmacotherapy as the preferred treatment option across both urban and semi-urban populations

The Saudi Arabia Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Insight

The Saudi Arabia OCD drugs market captured the largest revenue share of 35.1% in 2025 within the MEA region, driven by increasing mental health awareness, expansion of psychiatric services, and improved access to hospitals and specialty clinics. Patients and caregivers are prioritizing effective pharmacological treatments for moderate to severe OCD cases. The adoption of telepsychiatry services and outpatient management programs further propels market growth. Government initiatives supporting mental health, combined with private healthcare investments, are accelerating drug uptake. Moreover, hospitals and clinics are focusing on guideline-based therapies, establishing pharmacotherapy as the primary treatment option.

UAE Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Insight

The UAE OCD drugs market is projected to grow at a substantial CAGR during the forecast period, driven by rising awareness of mental health disorders and increasing healthcare infrastructure. Urbanization, higher disposable incomes, and a preference for modern psychiatric care are fostering the adoption of OCD drugs. Patients increasingly seek early diagnosis and treatment, and specialty clinics are integrating telemedicine solutions to enhance access. The UAE’s well-developed healthcare system and robust insurance coverage contribute to expanding treatment adoption. Furthermore, government-led mental health campaigns are encouraging proactive treatment-seeking behaviors.

Egypt Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Insight

The Egypt OCD drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by an increasing prevalence of OCD and growing recognition of psychiatric disorders. Rising patient awareness and better access to hospitals and specialty clinics are driving demand. Hospitals are focusing on standardized treatment protocols, supporting the prescription of antidepressants and antipsychotics. Expansion of outpatient services and telepsychiatry solutions further enhance drug accessibility. In addition, Egypt’s public and private healthcare initiatives are promoting mental health screening programs, which contribute to increasing adoption.

South Africa Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Insight

The South Africa OCD drugs market is expected to expand at a considerable CAGR during the forecast period, driven by the rising burden of mental health disorders and growing investments in healthcare infrastructure. Awareness programs, digital psychiatry, and improved hospital facilities are boosting treatment-seeking behavior. The availability of both generic and branded drugs ensures accessibility across urban and semi-urban populations. Specialty clinics are increasingly providing comprehensive care, integrating pharmacotherapy with counseling. Moreover, government initiatives supporting mental health awareness and insurance coverage for treatment are contributing to market expansion.

Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market Share

The Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs industry is primarily led by well-established companies, including:

- Pfizer Inc., (U.S.)

- GSK plc, (U.K.)

- H. Lundbeck A/S (Denmark)

- Sun Pharmaceutical Industries Ltd. (India)

- Eli Lilly and Company (U.S.)

- AbbVie (U.S.)

- Takeda Pharmaceutical Company Limited, (Japan)

- Novartis AG (Switzerland)

- Lupin (India)

- Dr. Reddy’s Laboratories Ltd., (India)

- Teva Pharmaceutical Industries Ltd., (Israel)

- Zydus Group (India)

- Aurobindo Pharma Limited (India)

- Alvogen (U.S.)

- Par Health Inc. (U.S.)

- Apotex Inc (Canada)

- Wockhardt (India)

- Amneal Pharmaceuticals LLC (U.S.)

- Sebela Pharmaceuticals Inc. (U.S.)

- Otsuka Pharmaceutical Co., Ltd., (Japan)

What are the Recent Developments in Middle East and Africa Obsessive-Compulsive Disorder (OCD) Drugs Market?

- In August 2025, a study on psychotropic medication trends in the Middle East revealed elevated prescribing rates for anxiety and OCD‑related conditions in the wake of the COVID‑19 pandemic, suggesting changing treatment patterns across MEA

- In January 2025, Boehringer Ingelheim signed a Memorandum of Understanding (MoU) with the Saudi Health Council (SHC) to jointly reassess mental health policies and enhance services across Saudi Arabia. The partnership is aimed at bringing global expertise into the Kingdom’s mental‑health ecosystem, improving awareness, access, and treatment practices a key enabler for drug therapy adoption for conditions including Obsessive‑Compulsive Disorder (OCD)

- In October 2024, a survey of medical students in Saudi Arabia found that 46.4% scored above the threshold for such asly obsessive‑compulsive symptoms (OCI‑R ≥ 21) across four major universities, indicating rising OCD burden and potential treatment demand in the region

- In October 2024, Burjeel Holdings introduced “Alkalma”, a digital mental‑health and wellness platform in Saudi Arabia designed to integrate preventive mental‑health care, risk‑management and outpatient services enhancing access to drug therapies for disorders such as OCD by bridging traditional hospital‑based care to digital/outpatient channels

- In September 2024, the Almoosa Health Group announced the opening of the “Rafa Mental Health Centre” within its rehabilitation hospital, offering comprehensive adult and child psychiatric services including treatment for OCD. This investment in infrastructure supports pharmacological and behavioural interventions for OCD and related disorders

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.