Middle East And Africa Point Of Care Diagnostics Market

Market Size in USD Billion

USD

1.63 Billion

USD

2.62 Billion

2024

2032

USD

1.63 Billion

USD

2.62 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.63 Billion | |

| USD 2.62 Billion | |

| % | |

|

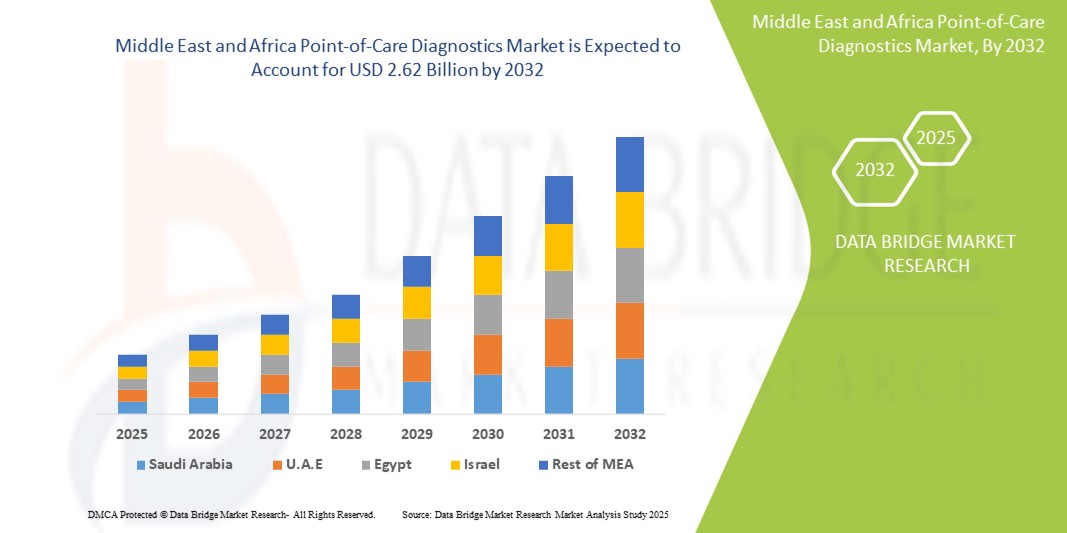

Middle East and Africa Point-of-Care Diagnostics Market Size

- The Middle East and Africa point-of-care diagnostics market size was valued at USD 1.63 billion in 2024 and is expected to reach USD 2.62 billion by 2032, at a CAGR of 6.1% during the forecast period

- The market growth is primarily driven by the rising burden of infectious and chronic diseases, coupled with the increasing need for rapid, accessible diagnostic solutions in remote and underserved areas across the region

- Moreover, growing investments in healthcare infrastructure, expanding government initiatives for early disease detection, and the rising adoption of portable and user-friendly testing devices are positioning point-of-care diagnostics as a vital tool for improving patient outcomes. These converging factors are accelerating the deployment of POC solutions, thereby significantly boosting the industry's growth

Middle East and Africa Point-of-Care Diagnostics Market Analysis

- Point-of-care (POC) diagnostics, enabling rapid medical testing at or near the site of patient care, are becoming crucial in the Middle East and Africa due to their ability to deliver timely results without the need for centralized laboratories, improving clinical decision-making and patient management in both urban and remote healthcare settings

- The growing demand for POC diagnostics is primarily fueled by the high prevalence of infectious diseases such as HIV, malaria, and tuberculosis, along with a rising need for chronic disease monitoring and increasing awareness around early disease detection

- Saudi Arabia dominated the Middle East and Africa point-of-care diagnostics market with the largest revenue share of 29.1% in 2024, supported by expanding healthcare infrastructure, government-led digital health initiatives under Vision 2030, and strategic investments to enhance diagnostic accessibility and quality

- Nigeria is expected to be the fastest growing country in the Middle East and Africa point-of-care diagnostics market during the forecast period, due to increasing international funding, improved supply chains, and the urgent need for rapid diagnostics to manage communicable and non-communicable diseases in underserved populations

- Infectious disease testing segment dominated the Middle East and Africa point-of-care diagnostics market with a market share of 47.8% in 2024, driven by targeted efforts to control epidemics and the need for fast, reliable testing in both clinical and community health environments

Report Scope and Middle East and Africa Point-of-Care Diagnostics Market Segmentation

|

Attributes |

Middle East and Africa Point-of-Care Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Point-of-Care Diagnostics Market Trends

“Expansion of Mobile Health and Decentralized Diagnostic Solutions”

- A key and accelerating trend in the MEA point-of-care diagnostics market is the widespread deployment of mobile health (mHealth) platforms and portable diagnostic devices aimed at decentralizing healthcare delivery. This trend is reshaping healthcare access by bringing diagnostics closer to patients, especially in rural and resource-limited settings

- For instance, m-PIMA HIV-1/2 VL by Abbott and the Cepheid GeneXpert platforms are being increasingly deployed across African countries such as Nigeria and Kenya through public health partnerships to deliver rapid results in the diagnosis of HIV, tuberculosis, and other infectious diseases

- Point-of-care solutions are being integrated with cloud-based health data systems, enabling healthcare providers to monitor and report cases in real-time. These digital integrations support national disease surveillance programs and ensure better treatment continuity. Devices such as LumiraDx and SD Biosensor are gaining traction for their portability, speed, and compatibility with mobile devices

- The rising penetration of smartphones and cellular networks in the region is driving innovation in connected diagnostic platforms that can transmit test results instantly to central systems for remote evaluation. This feature is particularly impactful in remote regions lacking fully equipped medical laboratories

- In addition, governments and NGOs across MEA are supporting this trend through initiatives that fund community health workers and equip them with mobile diagnostic kits to deliver frontline healthcare services

- This shift toward portable, connected, and rapid diagnostics is redefining the healthcare delivery model in the region, enabling more timely diagnosis and treatment and fostering growth in the point-of-care diagnostics market across both public and private health sectors

Middle East and Africa Point-of-Care Diagnostics Market Dynamics

Driver

“High Disease Burden and Government Focus on Decentralized Testing”

- The significant burden of communicable and non-communicable diseases in the MEA region, combined with limited access to centralized laboratory services, is a major driver for the growing adoption of point-of-care diagnostic solutions

- For instance, in February 2024, South Africa’s National Health Laboratory Service expanded its HIV viral load monitoring program by deploying new POC testing devices in mobile clinics across rural provinces

- As healthcare systems strive to achieve faster disease detection and treatment initiation, POC diagnostics offer timely results, ease of use, and the ability to reach underserved populations

- The increasing commitment from regional governments to strengthen primary healthcare and reduce patient turnaround times is further boosting market demand. This is supported by strategic collaborations with global health organizations such as WHO, UNICEF, and the Global Fund to introduce POC testing in immunization campaigns and disease eradication programs

- In countries such as Kenya, Egypt, and Saudi Arabia, the implementation of national health digitization plans and investments in community-level healthcare infrastructure are making POC diagnostics central to improving patient outcomes and optimizing clinical workflows

Restraint/Challenge

“Regulatory Gaps and Supply Chain Limitations”

- Despite growing adoption, the MEA point-of-care diagnostics market faces challenges due to fragmented regulatory frameworks and inconsistent product quality standards across countries, which hinder the timely approval and deployment of diagnostic devices

- For instance, the lack of harmonized policies across sub-Saharan Africa complicates the importation and certification of POC devices, leading to delays and underutilization in urgent care settings

- In addition, supply chain vulnerabilities—exacerbated by infrastructure deficits and political instability in certain regions—impede the consistent distribution and maintenance of POC equipment

- Ensuring device calibration, training healthcare workers, and maintaining a steady supply of consumables (such as test strips or cartridges) are recurring operational challenges

- Cost is also a barrier for certain advanced diagnostics, with limited funding in low-income countries preventing widespread adoption beyond pilot programs. Although donor-funded initiatives help offset these limitations, sustainable market penetration depends on improving affordability, local manufacturing, and regulatory harmonization

- Addressing these challenges will require capacity-building, public-private collaborations, and strengthened national frameworks to support the safe and effective integration of POC diagnostics into mainstream healthcare systems

Middle East and Africa Point-of-Care Diagnostics Market Scope

The market is segmented on the basis of product, prescription mode, platform, end user, and distribution channel.

- By Product

On the basis of product, the Middle East and Africa point-of-care diagnostics market is segmented into glucose monitoring products, infectious disease testing products, cardiometabolic testing products, pregnancy and fertility testing products, coagulation testing products, tumour/cancer marker testing products, cholesterol testing products, urinalysis testing products, haematology testing products, and other POC products. The infectious disease testing products segment dominated the market with the largest market revenue share of 47.8% in 2024, driven by the high prevalence of diseases such as HIV, malaria, tuberculosis, and respiratory infections. The widespread use of rapid diagnostic tests in public health programs and NGO-funded disease control initiatives has made this segment central to healthcare delivery in the region.

The glucose monitoring products segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the rising incidence of diabetes, increasing health awareness, and the growing availability of compact, affordable blood glucose monitors suitable for home and clinical use.

- By Prescription Mode

On the basis of prescription mode, the Middle East and Africa point-of-care diagnostics market is segmented into prescription-based testing and OTC testing. The prescription-based testing segment held the largest market revenue share in 2024, as most infectious disease and chronic condition diagnostics in the region are performed under physician supervision within professional healthcare settings. The segment is also supported by public health screenings and government programs.

The OTC testing segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing demand for self-diagnosis and the availability of home-use test kits for pregnancy, glucose, and cholesterol. The expansion of retail access and growing health awareness among consumers contribute to the segment's rapid growth.

- By Platform

On the basis of platform, the Middle East and Africa point-of-care diagnostics market is segmented into lateral flow assays/immunochromatography tests, molecular diagnostics, immunoassays, dipsticks, and microfluidics. The lateral flow assays/immunochromatography tests segment held the largest market revenue share in 2024, driven by its wide usage in infectious disease diagnostics and its suitability for low-resource environments. These tests offer affordability, portability, and minimal training requirements, making them highly effective for mass testing programs.

The molecular diagnostics segment is anticipated to witness the fastest growth rate from 2025 to 2032, supported by increasing use in early disease detection and the growing need for high-sensitivity testing methods. Platforms such as PCR and isothermal amplification are being increasingly adopted in urban healthcare facilities for HIV viral load monitoring and COVID-19 detection.

- By End User

On the basis of end user, the Middle East and Africa point-of-care diagnostics market is segmented into professional diagnostic centers, home care, research laboratories, and other end users. The professional diagnostic centers segment dominated the market with the largest market revenue share in 2024, driven by widespread use of point-of-care diagnostics in hospitals, clinics, and community health centers across the region. These centers often serve as the first point of contact for diagnostics in rural and peri-urban areas.

The home care segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the increasing adoption of home-use diagnostic kits, aging populations, and the demand for remote monitoring solutions. The shift toward patient-centric healthcare delivery models supports growth in this segment, especially in urban areas with higher access to retail pharmacies and digital health platforms.

- By Distribution Channel

On the basis of distribution channel, the Middle East and Africa point-of-care diagnostics market is segmented into direct tender and retail pharmacies. The direct tender segment held the largest market revenue share in 2024, owing to government procurement initiatives, public-private partnerships, and donor-funded programs that facilitate the bulk purchase and distribution of diagnostic tools to health centers and mobile clinics.

The retail pharmacies segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing demand for over-the-counter diagnostic products, greater accessibility in urban areas, and increasing consumer preference for self-testing kits available at commercial outlets.

Middle East and Africa Point-of-Care Diagnostics Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa point-of-care diagnostics market with the largest revenue share of 29.1% in 2024, supported by expanding healthcare infrastructure, government-led digital health initiatives under Vision 2030, and strategic investments to enhance diagnostic accessibility and quality

- Healthcare providers and patients in the country highly value the speed, portability, and ease-of-use offered by point-of-care diagnostics, particularly for managing infectious diseases and chronic conditions outside of centralized laboratory settings

- This strong adoption is further supported by rising healthcare expenditures, public-private partnerships, and digital health integration, positioning point-of-care diagnostics as a key enabler of efficient, patient-centered care across Saudi Arabia’s evolving healthcare landscape

The Saudi Arabia Point-of-Care Diagnostics Market Insight

The Saudi Arabia point-of-care diagnostics market captured the largest revenue share in the region in 2024, driven by the government's Vision 2030 healthcare reforms and significant investment in diagnostic infrastructure. The rising prevalence of chronic and infectious diseases, coupled with strong adoption of decentralized healthcare models, is fueling demand for rapid diagnostic tools. Increasing deployment of mobile health clinics and integration of digital platforms for health monitoring further support the growth of the POC diagnostics market in the country.

South Africa Point-of-Care Diagnostics Market Insight

The South Africa point-of-care diagnostics market is projected to grow at a substantial CAGR throughout the forecast period, primarily supported by public health programs targeting HIV, tuberculosis, and other infectious diseases. Government and NGO-led initiatives continue to drive widespread adoption of POC testing, especially in rural and underserved regions. In addition, the push for early detection and community-level healthcare access is strengthening demand across both public and private sectors.

United Arab Emirates Point-of-Care Diagnostics Market Insight

The UAE point-of-care diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for fast, accurate testing solutions in both clinical and non-clinical settings. The country’s advanced healthcare infrastructure and focus on digital health innovation promote adoption of POC technologies. The growing prevalence of lifestyle-related conditions such as diabetes and cardiovascular diseases is also contributing to the market's steady expansion.

Nigeria Point-of-Care Diagnostics Market Insight

The Nigeria point-of-care diagnostics market is expected to expand at a considerable CAGR during the forecast period, fueled by high disease burden, particularly in malaria, HIV, and tuberculosis. With limited access to centralized labs in many areas, POC diagnostics play a critical role in improving healthcare delivery. Support from international health agencies and increased deployment of mobile testing units are enhancing diagnostic reach, especially in rural communities.

Middle East and Africa Point-of-Care Diagnostics Market Share

The Middle East and Africa point-of-care diagnostics industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Siemens Healthineers AG (Germany)

- Danaher Corporation (U.S.)

- BD (U.S.)

- BIOMÉRIEUX (France)

- QuidelOrtho Corporation (U.S.)

- Chembio Diagnostic Systems, Inc. (U.S.)

- Trivitron Healthcare Pvt. Ltd. (India)

- EKF Diagnostics Holdings plc (U.K.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- SD Biosensor, Inc. (South Korea)

- Cepheid (U.S.)

- Nova Biomedical Corporation (U.S.)

- Instrumentation Laboratory Company (U.S.)

- POC Medical Systems, Inc. (U.S.)

- Biopanda Reagents Ltd. (U.K.)

- Meril Life Sciences Pvt. Ltd. (India)

- MicroLine Diagnostics Ltd. (Israel)

What are the Recent Developments in Middle East and Africa Point-of-Care Diagnostics Market?

- In june 2024, abbott laboratories expanded its footprint in africa by partnering with the nigerian ministry of health to deploy its m-pima™ hiv-1/2 vl platform across remote regions for rapid hiv viral load testing. this initiative aims to enhance access to decentralized diagnostics and strengthen national efforts in hiv monitoring and treatment, aligning with global 95-95-95 targets for hiv control

- in may 2024, roche diagnostics launched a mobile diagnostic initiative in kenya in collaboration with the clinton health access initiative (chai), introducing portable molecular testing platforms in underserved counties. this move is part of roche’s broader strategy to support disease surveillance and improve early diagnosis of tuberculosis and hepatitis in low-resource environments

- in april 2024, south africa's national health laboratory service (nhls) integrated cepheid’s genexpert® systems into its mobile health units as part of a national strategy to combat tuberculosis and drug-resistant infections. the deployment focuses on enabling rapid molecular testing in rural provinces, enhancing detection accuracy and reducing diagnostic delays

- in march 2024, sd biosensor and the uae’s ministry of health and prevention entered a strategic agreement to provide point-of-care covid-19 and flu testing devices across airports, schools, and community health centers. the agreement reinforces the uae's commitment to resilient healthcare infrastructure and pandemic preparedness

- in january 2024, siemens healthineers partnered with the egyptian ministry of health to introduce clinitest® rapid covid-19 antigen tests as part of a broader point-of-care diagnostics campaign. targeted at high-traffic areas such as transport hubs and government offices, the initiative supports egypt’s efforts in ensuring accessible and fast testing solutions during peak seasonal outbreaks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.