Middle East And Africa Ready To Drink High Strength Premixes Market

Market Size in USD Billion

USD

41.41 Billion

USD

56.24 Billion

2025

2033

USD

41.41 Billion

USD

56.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 41.41 Billion | |

| USD 56.24 Billion | |

| % | |

|

Middle East and Africa Ready to Drink/High Strength Premixes Market Overview

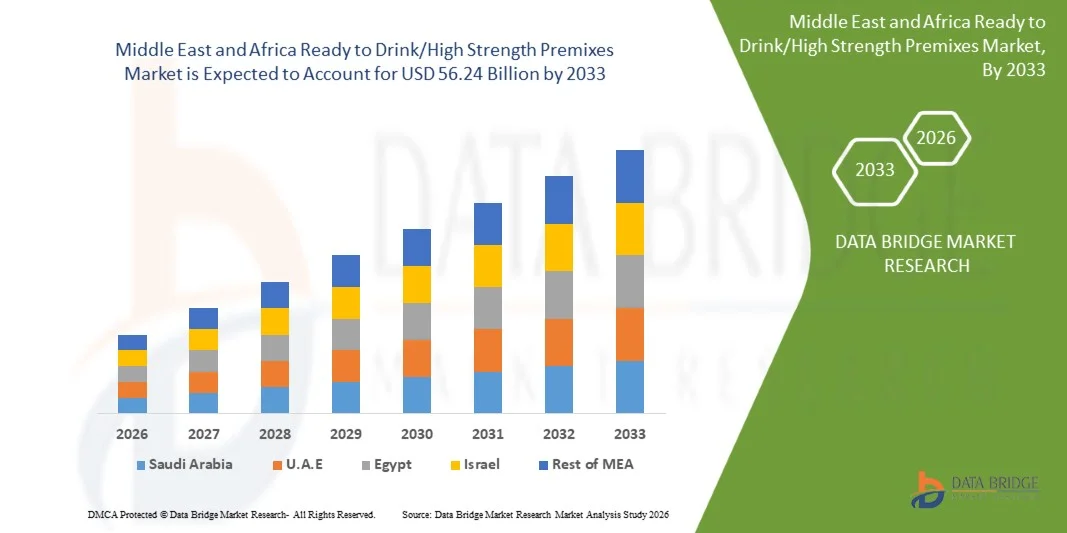

The Middle East and Africa ready to drink/high strength premixes market was valued at USD 41.41 billion in 2025 and is projected to reach USD 56.24 billion by 2033, growing at a CAGR of 3.90% from 2026 to 2033. 2025 and is projected to reach USD 56.24 billion by 2033, growing at a CAGR of 3.90% from 2026 to 2033. The market is experiencing steady growth driven by changing consumer lifestyles, increasing demand for convenient beverage formats, expanding urban populations, and the growing popularity of flavored alcoholic and non-alcoholic ready-to-consume products across key markets in the region.

Rising disposable incomes, increasing exposure to international beverage trends, and the expansion of modern retail channels are encouraging consumers to shift toward premium and innovative premixed beverages. Manufacturers are introducing a wider variety of flavors, low-sugar formulations, and premium ready-to-drink offerings to attract younger consumers seeking convenience and consistent product quality. In addition, the growth of tourism, hospitality, and entertainment sectors across countries such as the U.A.E., South Africa, and Saudi Arabia is supporting product visibility and consumption. The increasing adoption of ready-to-drink beverage formats through supermarkets, convenience stores, and online retail platforms is further strengthening market expansion by providing consumers with easy access to diverse beverage options for both social and personal consumption occasions.

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa ready to drink/high strength premixes market with the largest revenue share in 2025, supported by strong demand for premium beverages, rapid urbanization, high disposable income levels, and expansion of modern retail and hospitality infrastructure.

- U.A.E. is expected to be the fastest-growing region, recording a CAGR of from 2026 to 2033. Growth is driven by rising tourism activity, strong expatriate population base, rapid development of nightlife and hospitality sectors, increasing premium beverage consumption, and continuous expansion of retail and on-trade distribution channels.

- The Spirit Based RTDs segment held the largest market revenue share of approximately 46.2% in 2025 driven by strong demand in urban nightlife, hospitality venues, and tourism-heavy economies such as the U.A.E. and South Africa, where cocktail-style ready to drink beverages are widely consumed. Spirit based variants are preferred due to their premium positioning, wider flavor innovation, and strong presence in licensed retail channels.

- The Malt Based RTDs segment is projected to register the fastest growth at a CAGR of 5.1% from 2026 to 2033, driven by increasing acceptance of low-alcohol beverages, rising youth population consumption, and expanding availability in retail and convenience stores across emerging African economies.

- The Blended segment held the largest market revenue share of approximately 58.7% in 2025 driven by increasing consumer preference for multi-flavor combinations and consistent taste profiles across mass-market and premium beverage categories. Blended formulations are widely used by manufacturers to enhance product differentiation and improve shelf appeal in competitive retail environments.

- The Single Compound segment is expected to register the fastest growth at a CAGR of 4.6% from 2026 to 2033 driven by rising demand for clean-label beverages and simpler ingredient formulations among health-conscious consumers.

- The Male segment accounted for the largest market revenue share of approximately 62.4% in 2025 driven by higher consumption rates of alcoholic ready to drink products and stronger participation in nightlife and on-trade consumption channels across urban centers.

- The Female segment is projected to register the fastest growth at a CAGR of 5.3% from 2026 to 2033 driven by increasing adoption of low-alcohol, flavored, and functional beverage options aligned with lifestyle and wellness trends.

- The Cans segment held the largest market revenue share of approximately 49.6% in 2025 driven by portability, affordability, and strong usage across convenience stores and outdoor consumption occasions. Cans are widely preferred for ready to drink beverages due to ease of storage and strong branding surfaces.

- The Bottle segment is expected to register the fastest growth at a CAGR of 4.4% from 2026 to 2033 driven by premium product positioning and increasing demand in hospitality and fine dining environments

- The Off-Trade segment held the largest market revenue share of approximately 55.8% in 2025 driven by strong supermarket penetration, expanding retail chains, and growing consumer preference for at-home consumption.

- The On-Trade segment is expected to register the fastest growth at a CAGR of 4.9% from 2026 to 2033 driven by expansion of hotels, bars, restaurants, and tourism-driven hospitality consumption across key Middle Eastern destinations and African urban hubs.

Market Size & Forecast

- Market Value (2025): USD 41.41 Billion

- Expected Market Value (2033): USD 56.24 Billion

- Forecast CAGR (2026–2033): 3.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Middle East and Africa Ready to Drink/High Strength Premixes Market Segmentation

|

Attributes |

Middle East and Africa Ready to Drink/High Strength Premixes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

• Almarai (Saudi Arabia) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Ready to Drink/High Strength Premixes Market Trends

Trend: Growth In Premiumization And Functional Ready To Drink Beverage Consumption

Increasing demand for convenient, premium, and ready to consume beverage formats across urban populations in the Middle East and Africa, driven by shifting lifestyles, rising disposable incomes, and expanding hospitality and tourism sectors. Traditional beverage consumption patterns are gradually shifting toward packaged, consistent-quality, and innovative flavored products, particularly in fast-growing urban centers such as Dubai, Riyadh, Johannesburg, and Lagos.

In modern retail ecosystems, manufacturers are expanding ready to drink portfolios, For instance in flavored alcoholic beverages, energy-based premixes, and low-sugar functional drinks, to cater to younger consumers seeking convenience and variety while aligning with global health and wellness trends. In the hospitality sector, hotels, restaurants, and entertainment venues are increasingly integrating premium premixed beverages into their offerings to enhance customer experience and reduce preparation time while maintaining consistent taste quality.

The rapid expansion of modern retail formats and e-commerce beverage delivery platforms is also increasing product accessibility across emerging markets, particularly in the U.A.E. and South Africa, where organized retail penetration exceeded 60% in major urban areas in 2025. In addition, increasing tourism inflows, which surpassed 30 million visitors in the GCC region in 2024, continue to strengthen demand for standardized, high-quality beverage experiences. Growing product innovation through sugar-free, vitamin-enriched, and energy-enhanced premixes is further accelerating adoption across health-conscious consumer segments in Africa and the Middle East.

Global Middle East And Africa Ready To Drink/High Strength Premixes Market Dynamics

Key Market Driver: Rising Urbanization And Premium Beverage Consumption

The increasing urban population, expanding middle-class income groups, and changing consumer preferences toward convenient beverage formats are significantly driving the demand for ready to drink and high strength premixed beverages across the Middle East and Africa. Rapid lifestyle changes in metropolitan areas are encouraging consumers to shift from traditional beverages to packaged and on-the-go drink options with consistent taste and higher convenience.

In modern consumption environments, beverage manufacturers are expanding portfolios across alcoholic and non-alcoholic premixes, For instance flavored malt-based drinks, energy-infused beverages, and ready-to-serve cocktails, to cater to evolving consumer preferences in urban retail and hospitality channels. In major markets such as the U.A.E. and South Africa, increasing penetration of supermarkets, convenience stores, and licensed beverage outlets is enhancing product visibility and accessibility, while tourism-driven demand in cities such as Dubai and Cape Town is further boosting consumption across hospitality venues and entertainment sectors.

Key Restraint/Challenge: Regulatory Restrictions And Cultural Consumption Barriers

Stringent regulatory frameworks governing alcohol distribution, import policies, and product licensing across several countries in the Middle East and parts of Africa continue to restrict market expansion for alcoholic premixed beverages. Cultural and religious sensitivities in key economies also limit consumption potential, creating uneven market penetration across the region.

In addition, complex taxation structures, import duties, and distribution restrictions increase operational costs for manufacturers and limit pricing flexibility in competitive markets. For instance, alcohol-related products face strict retail licensing requirements in countries such as Saudi Arabia and Kuwait, which significantly constrain market accessibility compared to more liberal markets like the U.A.E. and South Africa. These regulatory and cultural limitations collectively slow down large-scale commercialization despite rising urban demand.

Key Market Opportunity: Expansion Of Premium And Functional Beverage Segments

The growing demand for premium, health-oriented, and functional beverage options presents significant opportunities for ready to drink and high strength premix manufacturers across the Middle East and Africa. Consumers are increasingly seeking low-sugar, vitamin-enriched, and energy-boosting beverages that align with wellness-focused lifestyles while maintaining convenience.

In response, beverage companies are introducing innovative product lines, For instance alcohol-free mocktails, electrolyte-based premixes, and fortified energy drinks designed for fitness-conscious and young urban consumers. The expansion of tourism infrastructure, with GCC countries attracting over 30 million international visitors in 2024, is further driving demand for standardized premium beverage experiences in hotels, resorts, and entertainment venues. In addition, rapid growth in e-commerce beverage delivery platforms and digital retail channels across Africa is creating new distribution opportunities, enabling brands to reach untapped consumer bases in both urban and semi-urban markets.

Middle East and Africa Ready to Drink/High Strength Premixes Market Scope

The market is segmented on the basis of model, type, functionality, offering, and end-use application

• By Type

On the basis of type, the Middle East and Africa ready to drink/high strength premixes market is segmented into Malt Based RTDs, Spirit Based RTDs, Wine Based RTDs, and Others. The Spirit Based RTDs segment held the largest market revenue share of approximately 46.2% in 2025 driven by strong demand in urban nightlife, hospitality venues, and tourism-heavy economies such as the U.A.E. and South Africa, where cocktail-style ready to drink beverages are widely consumed. Spirit based variants are preferred due to their premium positioning, wider flavor innovation, and strong presence in licensed retail channels.

The Malt Based RTDs segment is projected to register the fastest growth at a CAGR of 5.1% from 2026 to 2033, driven by increasing acceptance of low-alcohol beverages, rising youth population consumption, and expanding availability in retail and convenience stores across emerging African economies.

• By Processing Type

On the basis of processing type, the market is segmented into Single Compound and Blended. The Blended segment held the largest market revenue share of approximately 58.7% in 2025 driven by increasing consumer preference for multi-flavor combinations and consistent taste profiles across mass-market and premium beverage categories. Blended formulations are widely used by manufacturers to enhance product differentiation and improve shelf appeal in competitive retail environments.

The Single Compound segment is expected to register the fastest growth at a CAGR of 4.6% from 2026 to 2033 driven by rising demand for clean-label beverages and simpler ingredient formulations among health-conscious consumers.

• By Gender

On the basis of gender, the market is segmented into Male and Female. The Male segment accounted for the largest market revenue share of approximately 62.4% in 2025 driven by higher consumption rates of alcoholic ready to drink products and stronger participation in nightlife and on-trade consumption channels across urban centers.

The Female segment is projected to register the fastest growth at a CAGR of 5.3% from 2026 to 2033 driven by increasing adoption of low-alcohol, flavored, and functional beverage options aligned with lifestyle and wellness trends.

• By Packaging Type

On the basis of packaging type, the market is segmented into Bottle, Cans, and Others. The Cans segment held the largest market revenue share of approximately 49.6% in 2025 driven by portability, affordability, and strong usage across convenience stores and outdoor consumption occasions. Cans are widely preferred for ready to drink beverages due to ease of storage and strong branding surfaces.

The Bottle segment is expected to register the fastest growth at a CAGR of 4.4% from 2026 to 2033 driven by premium product positioning and increasing demand in hospitality and fine dining environments

• By Trade

On the basis of trade, the market is segmented into Off-Trade and On-Trade. The Off-Trade segment held the largest market revenue share of approximately 55.8% in 2025 driven by strong supermarket penetration, expanding retail chains, and growing consumer preference for at-home consumption.

The On-Trade segment is expected to register the fastest growth at a CAGR of 4.9% from 2026 to 2033 driven by expansion of hotels, bars, restaurants, and tourism-driven hospitality consumption across key Middle Eastern destinations and African urban hubs.

Middle East and Africa Ready to Drink/High Strength Premixes Market Regional Analysis

Saudi Arabia Ready To Drink/High Strength Premixes Market Insight

Saudi Arabia dominated the Middle East and Africa ready to drink/high strength premixes market with the largest revenue share in 2025, supported by rapid expansion of premium hospitality infrastructure, rising tourism activities under Vision 2030 initiatives, and growing demand for modern beverage formats in urban centers such as Riyadh and Jeddah. Increasing preference for flavored and convenient drink options in licensed hospitality venues and luxury hotels is further strengthening market penetration.

U.A.E. Ready To Drink/High Strength Premixes Market Insight

U.A.E. is expected to be the fastest-growing country in the Middle East and Africa ready to drink/high strength premixes market from 2026 to 2033, driven by strong tourism inflows, expansion of high-end nightlife and entertainment sectors, and rising expatriate population. Growth is further supported by increasing availability of innovative beverage products across premium retail and on-trade channels, along with continued investments in hospitality and event tourism infrastructure in Dubai and Abu Dhabi.

Middle East and Africa Ready to Drink/High Strength Premixes Market Share

The Middle East and Africa Ready to Drink/High Strength Premixes industry is primarily led by well-established companies, including:

• Almarai (Saudi Arabia)

• MenaBev (Saudi Arabia)

• National Beverage Company (Palestine)

• East African Breweries Limited (Kenya)

• Distell Group Holdings (South Africa)

• Castel Group (France)

• Delta Beverages (Zimbabwe)

• Al Ahram Beverages Company (Egypt)

• United National Breweries (South Africa)

• Ethiopian Brewing Company (Ethiopia)

• Heineken Beverages Africa (South Africa)

• The Beverage Company (South Africa)

• KEO plc (Cyprus)

• Namibia Breweries Limited (Namibia)

• Nile Breweries Limited (Uganda)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East And Africa Ready To Drink High Strength Premixes Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East And Africa Ready To Drink High Strength Premixes Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East And Africa Ready To Drink High Strength Premixes Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.