Middle East And Africa Self Injections Market

Market Size in USD Billion

USD

9.22 Billion

USD

17.58 Billion

2024

2032

USD

9.22 Billion

USD

17.58 Billion

2024

2032

| 2025 - 2032 | |

| USD 9.22 Billion | |

| USD 17.58 Billion | |

| % | |

|

Self-Injections Market Size

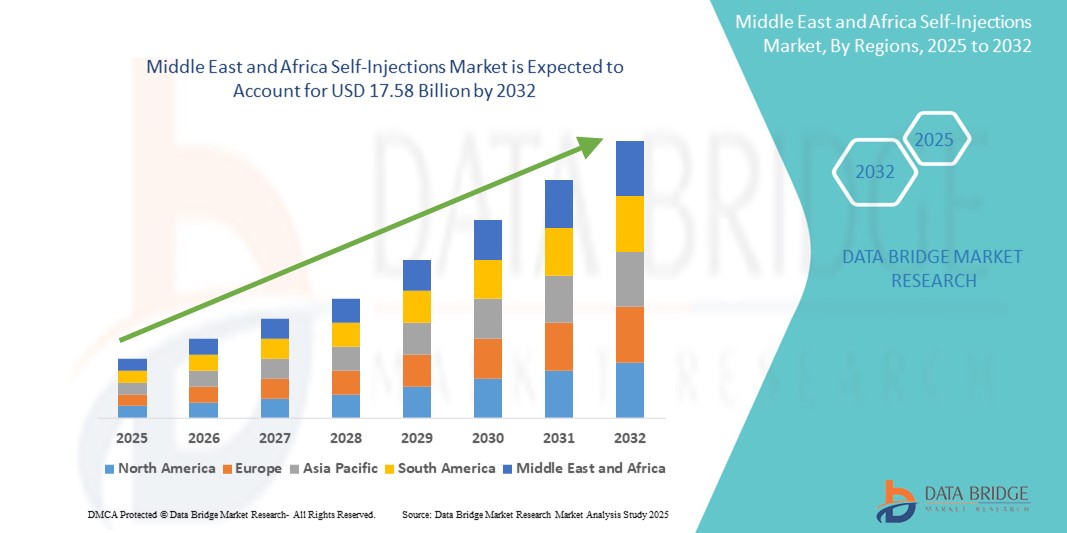

- The Middle East and Africa self-injections market size was valued at USD 9.22 billion in 2024 and is expected to reach USD 17.58 billion by 2032, at a CAGR of 8.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases such as diabetes, rheumatoid arthritis, and multiple sclerosis, which require long-term therapeutic regimens and have led to growing adoption of convenient drug delivery methods like self-injection systems. Technological advancements in drug delivery devices—such as auto-injectors and wearable injectors—are also contributing significantly to the rise of digital and connected healthcare environments across both home and clinical settings

- Furthermore, rising patient preference for self-administered therapies, coupled with healthcare providers’ emphasis on reducing hospital visits and improving medication adherence, is establishing self-injection systems as the preferred mode of drug delivery. These converging factors are accelerating the uptake of self-injection solutions, thereby significantly boosting the industry's growth across various therapeutic areas including oncology, hormonal disorders, and rare diseases

Self-Injections Market Analysis

- Self-injection devices, which allow patients to administer medication independently at home or in outpatient settings, are becoming essential components of modern healthcare systems due to their enhanced convenience, reduced need for clinic visits, and improved medication adherence

- The escalating demand for self-injections is primarily fueled by the increasing prevalence of chronic diseases such as diabetes, rheumatoid arthritis, and multiple sclerosis, growing patient preference for at-home care, and technological advancements in drug delivery systems

- Saudi Arabia dominated the Middle East and Africa self-injections market with a revenue share of 33.7% in 2024, driven by a surge in biologic drug utilization, supportive governmental health initiatives, a rapidly expanding pharmaceutical manufacturing sector, and increasing public awareness regarding chronic disease management

- Israel is projected to be the fastest-growing region in the Middle East and Africa self-injections market, expected to expand at a CAGR of 25.6% from 2025 to 2032, owing to its robust biotechnology ecosystem, growing adoption of innovative self-administration devices, and a strong focus on personalized medicine and remote care solutions

- The subcutaneous segment accounted for the largest share of 61.3% in the Middle East and Africa self-injections market in 2024, attributed to its compatibility with biologics, enhanced patient compliance, and broad applicability in chronic therapies such as insulin and monoclonal antibodies

Report Scope and Self-Injections Market Segmentation

|

Attributes |

Self-Injections Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Self-Injections Market Trends

“Rising Demand for Intelligent and User-Centric Solutions”

- A significant and accelerating trend in the Middle East and Africa self-injections market is the growing emphasis on intelligent and user-friendly solutions that enhance patient autonomy and medication adherence

- For instance, self-injection devices integrated with digital monitoring features and reminder systems are enabling real-time tracking of drug administration, helping patients and caregivers manage chronic conditions more effectively

- Pharmaceutical companies and medtech firms are incorporating smart technologies into auto-injectors and pen devices—such as sensors that detect injection completion or send refill alerts—to ensure better compliance and treatment outcomes

- The adoption of connected health platforms enables seamless synchronization between injection devices and mobile health apps, allowing patients to monitor injection history, receive dosage alerts, and communicate with healthcare providers from the comfort of home

- These developments align with the broader trend of personalized medicine and digital therapeutics, where treatment delivery is tailored to individual health profiles, supported by real-time data

- The demand for such advanced self-injection solutions is growing rapidly in Middle East and Africa, driven by increasing chronic disease prevalence, rising health literacy, and greater investment in remote patient monitoring and at-home care solutions

Self-Injections Market Dynamics

Driver

“Growing Need Due to Rising Chronic Disease Burden and Home-Based Care Adoption”

- The increasing prevalence of chronic conditions such as diabetes, multiple sclerosis, and rheumatoid arthritis, coupled with the accelerating adoption of home-based care solutions, is a significant driver for the heightened demand for self-injection devices

- For instance, in April 2024, Heron Therapeutics announced advancements in sustained-release drug delivery platforms aimed at enhancing post-surgical pain management via self-administered injections—an innovation expected to contribute significantly to the growth of the self-injections market during the forecast period

- As patients become more engaged in managing their own healthcare, self-injection devices offer advanced features such as pre-filled syringes, auto-injectors, and smart injectors with dose tracking and feedback alerts, providing a compelling alternative to hospital-based drug administration

- Furthermore, the growing popularity of telemedicine and the desire for remote, personalized treatment options are making self-injection systems an integral component of patient-centric care, offering convenience, adherence support, and reduced need for clinic visits

- The ease of use, improved patient autonomy, and the ability to administer biologics and specialty drugs at home are key factors propelling the adoption of self-injection systems across both developed and emerging markets. The trend towards digital health and the increasing availability of user-friendly self-injection options further contribute to market growth

Restraint/Challenge

“Concerns Regarding Safety, Training, and High Product Costs”

- Concerns surrounding the safe and accurate use of self-injection devices pose a significant challenge to broader market adoption. Users may lack confidence in their ability to properly administer medications without clinical supervision, particularly among elderly or visually impaired populations

- For instance, market reports have shown that training and education gaps remain a key concern, especially in low-resource settings, hindering effective self-injection practices and adherence

- Addressing these concerns through better instructional design, patient education programs, and intuitive device interfaces is crucial for building user confidence. Companies such as Amgen and Teva emphasize patient support tools and video guides in their device ecosystems to improve self-injection success rates

- In addition, the relatively high cost of biologics and associated self-injection systems—especially for therapies involving auto-injectors or wearable injectors—can be a barrier to access in price-sensitive markets

- While some cost reductions have been achieved through biosimilars and improved manufacturing efficiencies, the overall price point still limits widespread adoption, particularly for uninsured or underinsured populations

- Overcoming these challenges through improved product design, affordability, expanded reimbursement coverage, and targeted patient training will be vital for sustained growth of the self-injections market

Self-Injections Market Scope

The market is segmented on the basis of product type, dosage form, route of administration, application, age group, gender, and distribution channel.

- By Product Type

On the basis of product type, the Middle East and Africa self-injections market is segmented into self-injection devices and self-injection formulations. The self-injection devices segment held the largest market revenue share of 54.8% in 2024, driven by increasing patient preference for home-based treatments and technological advancements in autoinjectors and pen injectors.

The self-injection formulations segment is anticipated to witness the fastest growth rate of 22.3% CAGR from 2025 to 2032, owing to rising demand for ready-to-use biologics and specialty drug formulations for chronic diseases like diabetes, rheumatoid arthritis, and multiple sclerosis.

- By Dosage Form

On the basis of dosage form, the Middle East and Africa self-injections market is segmented into single dose and multi-dose. The single dose segment dominated the market with a revenue share of 59.6% in 2024, due to its convenience, reduced contamination risk, and ease of use.

The multi-dose segment is projected to register a strong CAGR of 21.1% during the forecast period, supported by increasing adoption in clinical and emergency settings.

- By Route of Administration

On the basis of route of administration, the Middle East and Africa self-injections market is segmented into subcutaneous, intramuscular, and others. The subcutaneous segment accounted for the largest share of 61.3% in 2024, due to its widespread usage in chronic disease management and better patient compliance.

The intramuscular segment is projected to grow at a CAGR of 20.5% from 2025 to 2032, particularly in the context of vaccines and hormone therapies that require deep tissue delivery.

- By Application

On the basis of application, the Middle East and Africa self-injections market is segmented into autoimmune diseases, pain management, emergency drugs, oncology, hormonal disorders, and others. The autoimmune diseases segment held the highest revenue share of 38.5% in 2024, driven by rising cases of conditions such as rheumatoid arthritis, psoriasis, and inflammatory bowel disease.

The oncology segment is expected to show the fastest CAGR of 23.4%, due to increasing availability of injectable cancer drugs and supportive therapy administered at home.

- By Age Group

On the basis of age group, the Middle East and Africa self-injections market is segmented into adult, geriatric, and pediatric. The adult segment dominated the market with 52.7% share in 2024, reflecting the higher prevalence of chronic diseases and lifestyle-related disorders in this group.

The geriatric segment is anticipated to experience a CAGR of 20.9%, due to increased adoption of self-administered therapies for conditions such as osteoporosis and diabetes.

- By Gender

On the basis of gender, the Middle East and Africa self-injections market is segmented into male and female. The female segment held a slightly higher market share of 50.8% in 2024, due to higher rates of autoimmune disorders and hormonal treatments that necessitate regular injections.

The male segment is growing at a CAGR of 19.6%, supported by rising demand in areas such as testosterone therapy and chronic pain management.

- By Distribution Channel

On the basis of distribution channel, the Middle East and Africa self-injections market is segmented into direct tender, hospital pharmacy, online pharmacy, and others. The hospital pharmacy segment captured the largest market share of 46.9% in 2024, attributed to the institutional buying of injectable medications and devices.

Meanwhile, the online pharmacy segment is projected to grow at the fastest CAGR of 24.2% from 2025 to 2032, owing to increasing digitalization, patient convenience, and widespread acceptance of e-pharmacy platforms in countries such as India, China, and Japan.

Self-Injections Market Regional Analysis

- Middle East and Africa accounted for a significant share of the global self-injections market in 2024 and is projected to grow at the fastest CAGR of 24% during 2025–2032

- driven by rising healthcare expenditure, expanding chronic disease prevalence, and increasing preference for self-care therapies

- Digital health acceleration, public awareness campaigns, and cost-effective access to injectable devices across urban and rural populations are key growth drivers

Saudi Arabia Self-Injections Market Insight

The Saudi Arabia self-injections market dominated the Middle East and Africa self-injections market with a market share of 31.6% in 2024, supported by growing investments in healthcare infrastructure, increased diagnosis of chronic conditions such as diabetes and autoimmune diseases, and strong government support for home-based treatment solutions. Local and international manufacturers are scaling operations to meet domestic demand for prefilled syringes and auto-injectors.

U.A.E. Self-Injections Market Insight

The U.A.E. self-injections market held a notable share of 17.4% in 2024 in the regional self-injections market, driven by high per capita healthcare spending, digital health adoption, and a focus on personalized treatment solutions. The increasing availability of biosimilars and digital health apps integrated with injectable therapy adherence tools is fostering market expansion.

South Africa Self-Injections Market Insight

The South Africa self-injections market accounted for 13.8% of the regional market share in 2024, benefiting from improved access to chronic disease management programs and national initiatives promoting home-based care. The rollout of biosimilar therapies and increased partnerships between pharmaceutical firms and private clinics are strengthening the market landscape.

Egypt Self-Injections Market Insight

Egypt’s self-injections market is gaining traction, holding a market share of 11.2% in 2024, backed by the Ministry of Health's focus on expanding outpatient care and early disease detection. Rising public sector procurement of biologic injectables and the introduction of affordable auto-injectors are supporting growth.

Self-Injections Market Share

The Middle East and Africa self-injections industry is primarily led by well-established companies, including:

- Bayer AG (Germany)

- UCB Pharma (Belgium)

- Ipsen Biopharmaceuticals, Inc. (France)

- Teva Pharmaceuticals Industries Ltd (Israel)

- Recipharm AB (Sweden)

- SCHOTT Pharma (Germany)

- Lilly (U.S.)

- AstraZeneca (U.K.)

- Takeda Pharmaceuticals Company Limited (Japan)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- AbbVie (U.S.)

- Biogen (U.S.)

- YPSOMED (Switzerland)

- Bausch Health Companies Inc. (Canada)

- Merck & Co. (U.S.)

- Amgen Inc. (U.S.

- Johnson & Johnson Services, Inc. (U.S.)

- PharmaJet (U.S.)

- Societe Industrielle de Sonceboz SA (Switzerland)

- Terumo Corporation (Japan)

- Haselmeier (Germany)

- Midas Pharma GmbH (Germany)

- BD (U.S.)

- Phillips-Medisize (U.S.)

- West Pharmaceutical Services (U.S.)

- Gerresheimer AG (Germany)

- Oval Medical Technologies Ltd. (SMC Limited) (U.K.)

- SHL Medical AG (Switzerland)

- Novo Nordisk A/S (Denmark)

- AptarGroup, Inc. (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GSK plc (U.K.)

Latest Developments in Middle East and Africa Self-Injections Market

- In September 2024, Evotec shares jumped 6% after announcing a technology development partnership with Novo Nordisk centered on cell therapy. The collaboration involves funding for development activities in Germany and Italy, along with upfront payments, potential milestone achievements, and royalty incentives. Dr. Cord Dohrmann, Evotec's Chief Scientific Officer, expressed optimism about creating innovative stem cell-based therapies through this partnership

- In September 2024, Tremfya (guselkumab) was FDA-approved for adults with moderately to severely active ulcerative colitis, in addition to its approvals for plaque psoriasis and psoriatic arthritis. It is the first dual-acting interleukin-23 inhibitor for this condition, showing significant remission rates in the QUASAR study. Administered as a 200 mg intravenous induction dose, it follows with subcutaneous maintenance doses of 100 mg every 8 weeks or 200 mg every 4 weeks. This approval highlights Johnson & Johnson's commitment to advancing treatments for inflammatory bowel disease

- In July 2024, Biogen has acquired Human Immunology Biosciences (HI-Bio), enhancing its immunology pipeline with felzartamab, a promising therapeutic candidate. The acquisition will advance felzartamab into Phase 3 trials for various indications. Positive interim results have been reported in Phase 2 studies for IgA nephropathy and antibody-mediated rejection

- In July 2024, Biogen has acquired Human Immunology Biosciences (HI-Bio), enhancing its immunology pipeline with felzartamab, a promising therapeutic candidate. The acquisition will advance felzartamab into Phase 3 trials for various indications. Positive interim results have been reported in Phase 2 studies for IgA nephropathy and antibody-mediated rejection

- In July 2024, AstraZeneca had successfully acquired Amolyt Pharma for up to USD 1.05 billion, enhancing its Alexion Rare Disease pipeline. This includes the Phase III peptide eneboparatide for hypoparathyroidism, expanding AstraZeneca's focus on rare endocrine diseases and calcium regulation treatments

- In June 2024, Aptar Digital Health partnered with SHL Medical to enhance connected device technologies by integrating its SaMD platform. This collaboration aimed to improve the patient experience during self-administration of injectable therapies, supporting better adherence and disease management for patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.