Middle East And Africa Sleep Apnea Devices Market

Market Size in USD Million

USD

400.98 Million

USD

806.59 Million

2025

2033

USD

400.98 Million

USD

806.59 Million

2025

2033

| 2026 - 2033 | |

| USD 400.98 Million | |

| USD 806.59 Million | |

| % | |

|

Middle East and Africa Sleep Apnea Devices Market Overview

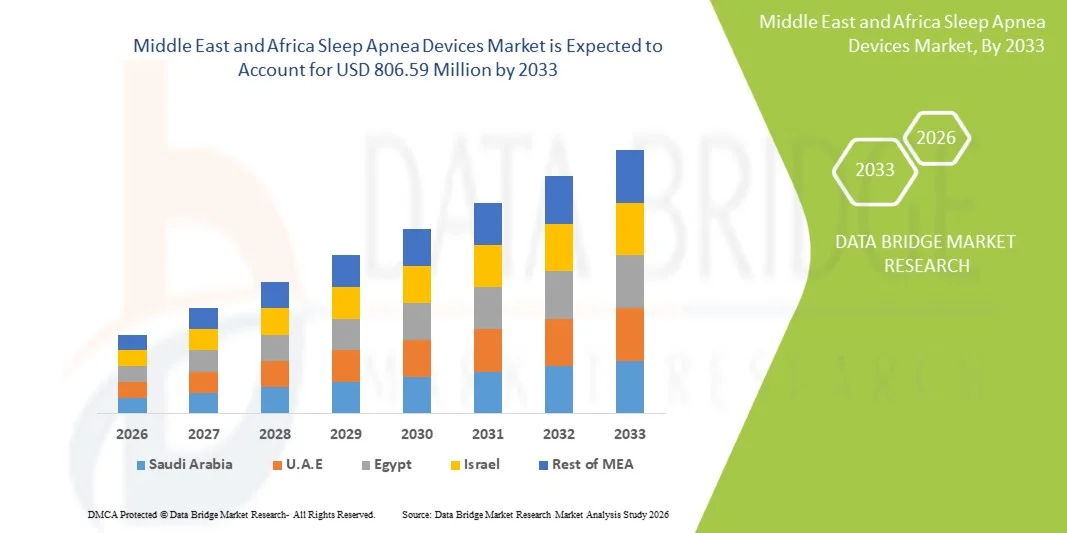

The Middle East and Africa sleep apnea devices market was valued at USD 400.98 Million in 2025 and is projected to reach USD 806.59 Million by 2033, growing at a CAGR of 9.5% from 2026 to 2033. The market is experiencing consistent growth driven by increasing prevalence of sleep-related breathing disorders, growing awareness of the health risks associated with untreated sleep apnea, and continuous advancements in diagnostic and therapeutic technologies. Sleep apnea devices play a crucial role in the detection, monitoring, and management of obstructive, central, and complex sleep apnea, helping improve sleep quality and overall patient health outcomes.

The market comprises a wide range of products, including positive airway pressure devices, oral appliances, sleep monitoring systems, home sleep testing devices, wearable technologies, and implantable therapeutic solutions. Technological innovations such as connected devices, remote patient monitoring, cloud-based data management, artificial intelligence-assisted diagnostics, and miniaturized equipment are transforming the sleep apnea care landscape.

Market Size & Forecast

- Middle East and Africa Market Value (2025): USD 400.98 Million

- Expected Market Value (2033): USD 806.59 Million

- Forecast CAGR (2026–2033): 9.5%

- Leading Country in 2025: Saudi Arabia

- Fastest Growing Country: Saudi Arabia

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa sleep apnea devices market with the largest revenue share of 25.80% in 2025, supported by a high prevalence of sleep apnea, strong awareness and diagnosis rates, widespread adoption of advanced sleep therapy devices, favorable reimbursement policies, and a well-established healthcare infrastructure.

- The devices segment led the market with a 58.42% share in 2025, driven by growing adoption of continuous positive airway pressure (CPAP), bilevel positive airway pressure (BiPAP), adaptive servo-ventilation (ASV), and oral appliance devices for the treatment of obstructive sleep apnea.

- Saudi Arabia is expected to be the fastest-growing region at a CAGR of11.0% from 2026 to 2033, fueled by a surging prevalence of obstructive sleep apnea (OSA) driven by rising obesity rates, sedentary lifestyles, and rapidly aging populations across key countries like China, India, and Japan. This growth is further accelerated by expanding healthcare infrastructure and rising disposable income, alongside a massive shift toward convenient, cost-effective home-based care.

- Oral appliances are the fastest-growing product type, projected to register a CAGR of 10.0%, reflecting the surge in demand for non-invasive, patient-friendly alternatives to traditional Continuous Positive Airway Pressure (CPAP) therapy. This growth is heavily propelled by low patient compliance with CPAP machines due to mask discomfort, noise, and bulkiness.

- The fixed machines segment dominates the machine type category with a 63.80% revenue share in 2025, led by their critical role in clinical settings and the high volume of initial therapeutic setups. Fixed machines, such as standard Continuous Positive Airway Pressure (CPAP) and Bi-level Positive Airway Pressure (BiPAP) devices, remain the gold standard of care for severe obstructive sleep apnea (OSA).

- The airway pressure segment in the function category accounts for 35.28% of the market, led by its undisputed standing as the gold standard for clinical efficacy in maintaining open airways.

- The portable machine segment is the fastest-growing machine type category, with a CAGR of 9.9%, driven by rapid expansion of the home healthcare sector and a massive shift in patient lifestyle preferences toward mobility and travel. Because traditional fixed sleep apnea devices are bulky and difficult to transport, patients with obstructive sleep apnea (OSA) are increasingly demanding lightweight, compact, and battery-powered alternatives that seamlessly integrate into their daily routines outside the bedroom.

Report Scope and Middle East and Africa Sleep Apnea Devices Market Segmentation

|

Attributes |

Sleep Apnea Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· ResMed Inc. (U.S.) · Philips Respironics (U.S.) · Inspire Medical Systems (U.S.) · Fisher & Paykel Healthcare (New Zealand) · BMC Medical (China) · Medtronic (Ireland) · Drive DeVilbiss Healthcare (U.S.) · Löwenstein Medical (Germany) · Breas Medical (Sweden) · Transcend (U.S.) · Apex Medical [now Wellell] (Taiwan) · Natus Medical (U.S.) · Zoll Medical (U.S.) · Compumedics (Australia) · Nihon Kohden (Japan) · Cadwell Industries (U.S.) · Ababil Medtech Innovations India Pvt Ltd (India) · OXYMED (China) · Beijing Aeonmed Co., Ltd. (China) · Hamilton Medical (Switzerland) · Hunan Beyond Medical (China) · BPL Medical Technologies (India) · Desco Medical Technologies (India) · Deck Mount (India) · Nidek Medical (U.S.) · NARANG MEDICAL (India) · React Health (U.S.) · Nareena Lifesciences Private Limited (India) · SEFAM (France) · InnAccel Technologies Pvt Ltd (India) · Advanced Brain Monitoring (U.S.) · SOMNOmedics America Inc. (Germany/U.S.) · Sunset Healthcare Solutions (U.S.) · Human Design Medical (U.S.) · Prosomnus sleep technologies (U.S.) · SomnoMed (Australia) |

|

Market Opportunities |

· Expansion of Telemedicine and Remote Sleep Apnea Diagnostics · Growing Adoption of Wearable and Non-Invasive Sleep Apnea Monitoring Solutions · Technological advancement in wearable and connected devices · Rising home care U.S.ge in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Sleep Apnea Devices Market Trends

Trend: Rising home care U.S.ge in emerging economies

Rising home care U.S.ge in emerging economies is creating significant opportunities across the healthcare ecosystem as patients increasingly prefer receiving medical support, chronic disease management, rehabilitation, and elderly care services within their homes. Rapid urbanization, growing middle-class populations, and increasing awareness of personalized healthcare are encouraging families to adopt home-based care solutions that offer convenience, comfort, and continuity of treatment. Healthcare providers are responding by expanding home nursing, remote monitoring, telehealth integration, and assisted living services, enabling patients to access quality care while reducing dependence on hospital-based settings.

For Instance,

-

In April 2025, according to PR Newswire, Geri Care Health Services launched its first assisted living centre in Bengaluru, India, establishing a 100-bed facility designed to provide round-the-clock geriatric care in a home-like environment. The expansion supports the company's broader strategy to strengthen home and elder care services across India.

-

In April 2025, according to Waud Capital Partners, the company announced that its home care platform Altocare acquired MedTec Healthcare, a provider of in-home care and adult day services. The acquisition was undertaken to expand home-based care capabilities and build a broader care delivery network serving both private-pay and Medicaid-supported patients

Middle East and Africa Sleep Apnea Devices Market Dynamics

Key Market Driver: Expanding Reimbursement Policies and Insurance Coverage

Expanding reimbursement policies and broader insurance coverage are significantly improving access to sleep apnea diagnosis and treatment worldwide. As sleep apnea becomes increasingly associated with serious health complications such as cardiovascular disease, diabetes, and other chronic conditions, healthcare systems are placing greater emphasis on early detection and long-term disease management. In response, public and private payers are extending coverage for diagnostic testing, positive airway pressure therapies, implantable devices, and ongoing patient care. Financial support is also expanding for home sleep testing, remote monitoring solutions, and alternative treatment options, making care more accessible and convenient for patients. These developments are reducing out-of-pocket costs, encouraging treatment initiation, and improving therapy adherence. At the same time, evolving reimbursement frameworks are supporting the adoption of innovative technologies and value-based care models, contributing to broader utilization of sleep apnea management solutions across diverse patient populations.

For instance,

-

According to Inspire Medical Systems in July 2024, the company announced the publication of nationwide reimbursement coverage for Inspire therapy in France. The reimbursement approval expanded patient access to Inspire’s obstructive sleep apnea treatment and supported broader adoption of advanced sleep apnea therapies through public healthcare funding mechanisms.

Key Restraint/Challenge: High Device Costs and Limited Reimbursement Policies

High device costs and limited reimbursement coverage remain major challenges for the adoption of sleep apnea diagnostic and treatment solutions. CPAP devices, oral appliances, home sleep testing systems, and advanced implantable therapies often require significant upfront spending, which can limit access for uninsured or underinsured patients. In many countries, reimbursement policies are restricted by stringent eligibility criteria, diagnostic requirements, and compliance monitoring rules, delaying treatment initiation. These financial barriers can contribute to underdiagnosis and inadequate management of sleep apnea, increasing the risk of cardiovascular, metabolic, and respiratory complications. In response, manufacturers are developing cost-effective home-based diagnostics, flexible treatment models, and reimbursement-friendly devices, while collaborating with payers and healthcare providers to expand coverage and improve patient access to long-term therapy.

For instance,

-

In March 2025, Signifier Medical Technologies introduced a new eXciteOSA configuration with a hardware remote control. The enhancement was designed to meet CMS reimbursement requirements and support broader insurance coverage. It aims to improve patient access to therapy by aligning with payer compliance standards.

-

In April 2025, ResMed launched NightOwl™, an FDA-cleared home sleep apnea test in the United States. The home-based diagnostic solution simplifies sleep apnea detection and reduces reliance on in-laboratory testing. It is intended to lower diagnostic costs and improve patient access to care.

Key Market Opportunity: Expansion of Telemedicine and Remote Sleep Apnea Diagnostics

The expansion of telemedicine and remote sleep apnea diagnostics is creating significant opportunities for healthcare providers and medical technology companies to improve patient access, accelerate diagnosis, and enhance long-term disease management. Traditional sleep studies often require overnight monitoring in specialized laboratories, which can be expensive, time-consuming, and inaccessible for patients living in remote or underserved regions. Telemedicine platforms and home sleep apnea testing solutions are helping overcome these barriers by enabling patients to undergo diagnostic evaluations from their homes while maintaining virtual consultations with sleep specialists. This shift is improving convenience, reducing waiting times, and encouraging earlier identification of sleep-related breathing disorders. Advancements in wearable technology, cloud-based diagnostic platforms, artificial intelligence, and remote patient monitoring are further strengthening the adoption of virtual sleep care models. Healthcare providers can now collect, analyze, and share sleep data in real time, allowing physicians to remotely assess patient conditions and optimize treatment plans without requiring frequent in-person visits. The integration of telehealth services with digital diagnostic tools is also supporting continuous patient engagement and therapy adherence, particularly for individuals using CPAP devices and other sleep apnea treatments. As healthcare systems increasingly emphasize decentralized care and digital health solutions, remote sleep apnea diagnostics are expected to play a larger role in expanding treatment accessibility and improving patient outcomes.

For instance,

-

In February 2024 according to Samsung Middle East and Africa Newsroom, Samsung Electronics received FDA authorization for its sleep apnea detection feature on Galaxy Watch devices. The feature helps users identify signs of moderate to severe obstructive sleep apnea through sleep monitoring. It supports earlier diagnosis using wearable health technology.

- In May 2024, according to Nox Medical, company launched Nox Connect, a cloud-based platform for home and in-lab sleep testing. The system centralizes patient data, diagnostics, and remote testing workflows. It enhances telemedicine-based sleep care and operational efficiency.

Middle East and Africa Sleep Apnea Devices Market Scope

The sleep apnea devices market is segmented on the basis of product type, machinery type, function, application, age group, end user, and distribution channel.

- By Product Type

On the basis of product type, the market is segmented into devices, consumables & accessories, oral appliances, and others. In 2026, the devices segment is expected to dominate the market with a market share of 58.40%, owing to the increasing prevalence of sleep apnea, growing adoption of CPAP, BiPAP, and adaptive servo-ventilation devices, and rising awareness regarding the health risks associated with untreated sleep disorders.

The oral appliances segment is projected to register the fastest growth at a CAGR of 10.0% from 2026 to 2033, driven by increasing patient preference for non-invasive and portable treatment options, rising awareness of obstructive sleep apnea, and growing acceptance of mandibular advancement devices as an alternative to CPAP therapy.

- By Machinery Type

On the basis of machinery type, the market is segmented into fixed machines and portable machines. In 2026, the fixed machines segment is expected to dominate the market with a market share of 63.69%, supported by their widespread use in clinical and home-based sleep apnea therapy, superior therapeutic effectiveness, advanced monitoring capabilities, and established adoption of fixed CPAP and BiPAP systems.

The portable machines segment is expected to experience the fastest growth at a CAGR of 9.9% from 2026 to 2033, driven by increasing demand for convenient and travel-friendly sleep apnea treatment solutions, rising adoption of home healthcare, and growing patient preference for compact, lightweight devices.

- By Function

On the basis of function, the market is segmented into airway pressure, data recording & connectivity, airway monitoring, oxygen therapy, humidification, apnea detection, alarm & alert systems, and others. In 2026, the airway pressure segment is expected to dominate the market with a market share of 35.37% due to its critical role in maintaining unobstructed airflow during sleep and its widespread use in CPAP, BiPAP, and other positive airway pressure therapies.

The data recording & connectivity segment is anticipated to witness the fastest CAGR of 10.0% from 2026 to 2033, driven by the increasing integration of digital health technologies, remote patient monitoring, and cloud-based data management solutions in sleep apnea therapy devices.

- By Application

On the basis of application, the market is segmented into obstructive sleep apnea, central sleep apnea, complex sleep apnea syndrome, and others. In 2026, the obstructive sleep apnea segment is expected to dominate the market with a market share of 71.66% due to its significantly higher prevalence compared to other sleep apnea types, increasing diagnosis rates, and the widespread adoption of CPAP, BiPAP, and oral appliance therapies for its treatment.

The complex sleep apnea syndrome segment is expected to witness the fastest CAGR of 10.0% from 2026 to 2033, driven by increasing recognition and diagnosis of mixed sleep apnea conditions that combine characteristics of both obstructive and central sleep apnea.

- By Age Group

On the basis of age group, the market is segmented into adult, geriatric, and pediatric. In 2026, the adult segment is expected to dominate the market with a market share of 63.10% due to the high prevalence of sleep apnea among the working-age population, increasing rates of obesity and lifestyle-related risk factors, and greater awareness and diagnosis of sleep disorders.

The geriatric segment is expected to witness the fastest CAGR of 9.9% from 2026 to 2033, this growth is driven by rapidly expanding elderly population worldwide, increasing prevalence of sleep apnea and other age-related respiratory disorders, and higher susceptibility to comorbidities such as cardiovascular diseases, hypertension, and diabetes.

- By End User

On the basis of end user, the market is segmented into hospitals, home care settings, sleep laboratories & clinics, ambulatory surgical centers, and others. In 2026, the home care settings segment is expected to dominate the market with a market share of 18.25% due to the growing preference for home-based sleep apnea diagnosis and treatment, increasing adoption of portable and user-friendly therapy devices, and the cost-effectiveness of home care compared to hospital-based treatment.

The home care settings segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing shift toward home-based healthcare, growing demand for convenient and cost-effective treatment options, and rising adoption of portable sleep apnea diagnostic and therapeutic devices.

- By Distribution Channel

On the basis of the distribution channel, the market is segmented into direct and indirect. In 2026, the direct segment is expected to dominate the market with a market share of 61.47% due to manufacturers' increasing focus on direct sales channels, stronger relationships with healthcare providers and sleep clinics, and greater control over pricing, product customization, and customer support.

The direct segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, driven by growing preference of manufacturers to engage directly with healthcare providers, sleep clinics, and end users, enabling improved customer experience and stronger brand loyalty.

Middle East and Africa Sleep Apnea Devices Market Regional Analysis

Saudi Arabia dominated the Middle East and Africa sleep apnea devices market with the largest revenue share of 46.79% in 2025, supported by a high prevalence of sleep apnea, strong awareness and diagnosis rates, widespread adoption of advanced sleep therapy devices, favorable reimbursement policies, and a well-established healthcare infrastructure.

Saudi Arabia Sleep Apnea Devices Market Insight

The Saudi Arabia sleep apnea devices market is expected to grow significantly, supported by rising awareness of sleep-related breathing disorders, increasing healthcare spending, and improvements in diagnostic and treatment infrastructure. The high prevalence of obesity, diabetes, and cardiovascular risk factors is contributing to a greater incidence of sleep apnea cases. Expansion of sleep clinics, increasing availability of polysomnography and home sleep testing, and growing adoption of CPAP and other positive airway pressure devices are driving market growth. Additionally, healthcare transformation initiatives under Vision 2030 are improving access to advanced respiratory care and supporting the adoption of home-based sleep apnea management solutions.

UAE Sleep Apnea Devices Market Insight

The UAE sleep apnea devices market is witnessing steady growth due to increasing awareness of sleep disorders, rising obesity prevalence, and strong healthcare infrastructure development. The country’s focus on preventive healthcare, early diagnosis, and advanced medical technologies is encouraging greater adoption of sleep apnea diagnostic and therapeutic devices. Demand for CPAP, APAP, and BiPAP devices is increasing as patients and healthcare providers recognize the risks associated with untreated sleep apnea, including cardiovascular complications and reduced quality of life. Furthermore, the expansion of private healthcare facilities, telemedicine services, and home healthcare solutions is supporting market growth.

Egypt Sleep Apnea Devices Market Insight

The Egypt sleep apnea devices market is expected to expand due to growing awareness of sleep disorders, increasing prevalence of obesity, and gradual improvements in healthcare accessibility. Although diagnosis rates remain relatively low compared with developed markets, rising recognition among healthcare professionals and patients is creating demand for sleep apnea testing and treatment devices. The development of specialized sleep centers, increasing availability of CPAP therapy, and government efforts to strengthen healthcare services are contributing to market expansion. Egypt is emerging as a promising market in the Middle East and Africa region due to its large population base and increasing focus on respiratory health.

Middle East and Africa Sleep Apnea Devices Market Share

The sleep apnea devices industry is primarily led by well-established companies, including:

- ResMed Inc. (U.S.)

- Philips Respironics (U.S.)

- Inspire Medical Systems (U.S.)

- Fisher & Paykel Healthcare (New Zealand)

- BMC Medical (China)

- Medtronic (Ireland)

- Drive DeVilbiss Healthcare (U.S.)

- Löwenstein Medical (Germany)

- Breas Medical (Sweden)

- Transcend (U.S.)

- Apex Medical [now Wellell] (Taiwan)

- Natus Medical (U.S.)

- Zoll Medical (U.S.)

- Compumedics (Australia)

- Nihon Kohden (Japan)

- Cadwell Industries (U.S.)

- Ababil Medtech Innovations India Pvt Ltd (India)

- OXYMED (China)

- Beijing Aeonmed Co., Ltd. (China)

- Hamilton Medical (Switzerland)

- Hunan Beyond Medical (China)

- BPL Medical Technologies (India)

- Desco Medical Technologies (India)

- Deck Mount (India)

- Nidek Medical (U.S.)

- NARANG MEDICAL (India)

- React Health (U.S.)

- Nareena Lifesciences Private Limited (India)

- SEFAM (France)

- InnAccel Technologies Pvt Ltd (India)

- Advanced Brain Monitoring (U.S.)

- SOMNOmedics America Inc. (Germany/U.S.)

- Sunset Healthcare Solutions (U.S.)

- Human Design Medical (U.S.)

- Prosomnus sleep technologies (U.S.)

- SomnoMed (Australia)

Latest Developments in Middle East and Africa Sleep Apnea Devices Market

- In November 2025, Nihon Kohden Corporation announced that it has established a new technology development subsidiary in India to strengthen and accelerate the development of software for medical equipment and corporate IT systems, while also working to reduce related costs. The Company plans to gradually transfer and integrate the development and maintenance functions from Nihon Kohden Digital Health Solutions, LLC, Nihon Kohden America, LLC, and Nihon Kohden Corporation into this subsidiary by March 2029.

- In April 2026, Nihon Kohden announced it is expanding the reach of NomadAir with Connect, its established at-home sleep apnea diagnostic system, into dental sleep medicine. The expansion comes as growing collaboration between dentists and sleep physicians creates demand for a more connected, efficient approach to obstructive sleep apnea (OSA) diagnosis and treatment.

- In March 2026, BPL Medical Technologies announced the acquisition of Yozma BMtech Co, a company specialising in bone mineral density (BMD) diagnostic solutions. The acquisition adds to BPL MedTech’s imaging and diagnostics portfolio in preventive healthcare, bone health and women’s health.

- In June 2026, BPL Medical Technologies announced the launch of the BPL Vent 300, a new ICU ventilator developed to support critical care teams with advanced respiratory management across adult, paediatric, and infant patients. The launch comes at a time when hospitals across India are continuing to invest in stronger ICU preparedness, patient monitoring, and a dependable respiratory support system.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 DBMR VENDOR SHARE ANALYSIS

2.1 MARKET END USER COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES ANALYSIS

4.1.1 INTRODUCTION

4.1.2 INTENSITY OF COMPETITIVE RIVALRY HIGH

4.1.3 BARGAINING POWER OF BUYERS – MODERATE TO HIGH

4.1.4 THREAT OF NEW ENTRANTS – MODERATE TO LOW

4.1.5 THREAT OF SUBSTITUTE PRODUCTS – MODERATE

4.1.6 BARGAINING POWER OF SUPPLIERS – MODERATE

4.1.7 CONCLUSION

4.2 COMPANY EVALUATION QUADRANT

4.3 OPPORTUNITY MAP ANALYSIS

4.4 HEALTHCARE ECONOMY

4.4.1 HEALTHCARE EXPENDITURE

4.4.2 CAPITAL EXPENDITURE

4.4.3 CAPEX TRENDS

4.4.4 CAPEX ALLOCATION

4.4.5 FUNDING SOURCES

4.4.6 INDUSTRY BENCHMARKS

4.4.7 GDP RATIO IN OVERALL GDP

4.4.8 HEALTHCARE SYSTEM STRUCTURE

4.4.9 GOVERNMENT POLICIES

4.4.10 ECONOMIC DEVELOPMENT

4.4.11 CONCLUSION

4.5 REIMBURSEMENT FRAMEWORK

4.6 SUPPLY CHAIN ANALYSIS –

4.6.1 INTRODUCTION

4.6.2 RAW MATERIAL AND COMPONENT SOURCING

4.6.3 DEVICE MANUFACTURING & ASSEMBLY

4.6.4 SOFTWARE & TECHNOLOGY INTEGRATION

4.6.5 REGULATORY & QUALITY COMPLIANCE

4.6.6 DISTRIBUTION & LOGISTICS

4.6.7 HEALTHCARE PROVIDERS, HOMECARE PROVIDERS & END USERS

4.6.8 CONCLUSION

4.7 COST ANALYSIS BREAKDOWN

4.7.1 INTRODUCTION

4.7.2 RAW MATERIAL AND MANUFACTURING COSTS

4.7.3 PACKAGING AND LOGISTICS COSTS

4.7.4 RESEARCH, QUALITY, AND REGULATORY COMPLIANCE COSTS

4.7.5 ENVIRONMENTAL, ENERGY, AND SUSTAINABILITY COSTS

4.8 EPIDEMIOLOGY OF OBSTRUCTIVE SLEEP APNEA (OSA) –

4.8.1 MIDDLE EAST AND AFRICA BURDEN AND PREVALENCE OF OSA

4.8.2 REGIONAL DISTRIBUTION AND DIAGNOSIS GAP ANALYSIS

4.8.3 ASIA-PACIFIC OSA EPIDEMIOLOGY AND UNMET NEED

4.8.4 NORTH AMERICA OSA EPIDEMIOLOGY AND TREATMENT LANDSCAPE

4.8.5 EUROPE OSA EPIDEMIOLOGY AND HEALTHCARE ACCESS

4.8.6 SOUTH AMERICA AND MIDDLE EAST & AFRICA OSA EPIDEMIOLOGY

4.8.7 TREATMENT GAP AND FUTURE EPIDEMIOLOGICAL OUTLOOK

4.9 INDUSTRY INSIGHTS

4.9.1 MACRO AND MICRO ECONOMIC FACTORS

4.9.2 PENETRATION AND GROWTH PROSPECT MAPPING

4.9.3 KEY PRICING STRATEGIES

4.9.4 INTERVIEWS WITH SPECIALISTS

4.9.5 ANALYSIS AND RECOMMENDATION

4.9.5.1 MARKET ANALYSIS

4.9.5.2 STRATEGIC RECOMMENDATIONS

4.9.6 CONCLUSION

4.1 INNOVATION TRACKER AND STRATEGIC ANALYSIS –

4.10.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.10.1.1 JOINT VENTURES

4.10.1.2 MERGERS AND ACQUISITIONS

4.10.1.3 LICENSING AND PARTNERSHIP

4.10.1.4 TECHNOLOGY COLLABORATIONS

4.10.1.5 STRATEGIC DIVESTMENTS

4.10.2 NUMBER OF PRODUCTS IN DEVELOPMENT

4.10.3 STAGE OF DEVELOPMENT

4.10.4 TIMELINES AND MILESTONES

4.10.5 INNOVATION STRATEGIES AND METHODOLOGIES

4.10.6 RISK ASSESSMENT AND MITIGATION

4.10.7 FUTURE OUTLOOK

4.11 PATENT ANALYSIS

4.11.1 PATENT QUALITY AND STRENGTH

4.11.2 PATENT FAMILIES

4.11.3 LICENSING AND COLLABORATIONS

4.11.4 COMPETITIVE LANDSCAPE

4.11.5 IP STRATEGY AND MANAGEMENT

4.11.6 OTHER (EMERGING TRENDS AND INSIGHTS)

4.12 TECHNOLOGY ROADMAP– MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET

4.12.1 CURRENT TECHNOLOGY LANDSCAPE

4.12.2 NEAR-TERM DEVELOPMENTS (SHORT TERM: 2026–2029)

4.12.3 MID-TERM TECHNOLOGY EVOLUTION (MEDIUM TERM: 2030–2035)

4.12.4 LONG-TERM INNOVATION OUTLOOK (LONG TERM: 2035–2045)

4.12.5 ROLE OF DIGITAL HEALTH AND TELEMEDICINE

4.12.6 TECHNOLOGY ADOPTION CHALLENGES

5 TARIFFS & IMPACT ON THE MARKET –

5.1 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRY MARKETS

5.2 OUTLOOK: LOCAL PRODUCTION VS IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 RAW MATERIAL PROCUREMENT

5.4.2 MANUFACTURING AND PRODUCTION

5.4.3 LOGISTICS AND DISTRIBUTION

5.4.4 PRICE POSITIONING AND MARKET IMPACT

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 JOINT VENTURE ESTABLISHMENTS

5.6 REGULATORY INCLINATION

5.7 GEOPOLITICAL SITUATION

5.7.1 TRADE PARTNERSHIPS BETWEEN COUNTRIES

5.7.1.1 FREE TRADE AGREEMENTS

5.7.1.2 ALLIANCE ESTABLISHMENTS

5.7.2 STATUS ACCREDITATION (INCLUDING MFN)

6 REGULATORY COMPLIANCE

6.1 INTRODUCTION

6.2 REGULATORY AUTHORITIES

6.3 REGULATORY CLASSIFICATION

6.4 REGULATORY SUBMISSIONS

6.5 INTERNATIONAL HARMONIZATION

6.6 COMPLIANCE AND QUALITY MANAGEMENT SYSTEMS (QMS)

6.7 REGULATORY CHALLENGES AND STRATEGIES

6.8 RECOMMENDED REGULATORY STRATEGIES

6.9 CONCLUSION

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 RISING PREVALENCE OF OBSTRUCTIVE SLEEP APNEA (OSA)

7.1.2 INCREASING AWARENESS AND DIAGNOSTIC RATES

7.1.3 EXPANDING REIMBURSEMENT POLICIES AND INSURANCE COVERAGE

7.1.4 GROWING BURDEN OF COMORBIDITIES AND ASSOCIATED HEALTHCARE COSTS

7.2 RESTRAINTS

7.2.1 HIGH DEVICE COSTS AND LIMITED REIMBURSEMENT POLICIES

7.2.2 PATIENT NON-ADHERENCE AND COMFORT ISSUES

7.2.3 REGULATORY HURDLES AND PROLONGED APPROVAL TIMELINES

7.3 OPPORTUNITIES

7.3.1 EXPANSION OF TELEMEDICINE AND REMOTE SLEEP APNEA DIAGNOSTICS

7.3.2 GROWING ADOPTION OF WEARABLE AND NON-INVASIVE SLEEP APNEA MONITORING SOLUTIONS

7.3.3 TECHNOLOGICAL ADVANCEMENT IN WEARABLE AND CONNECTED DEVICES

7.3.4 RISING HOME CARE USAGE IN EMERGING ECONOMIES

7.4 CHALLENGES

7.4.1 STRINGENT REGULATORY APPROVALS AND COMPLIANCE COMPLEXITIES

7.4.2 LIMITED SPECIALIST AVAILABILITY IN LOW-INCOME REGIONS

7.4.3 SUPPLY CHAIN DISRUPTIONS AND COMPONENT SHORTAGES

8 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 DEVICES

8.3 CONSUMABLES & ACCESSORIES

8.4 ORAL APPLIANCES

8.5 OTHERS

8.6 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

8.6.1 DEVICES

8.6.2 CONSUMABLES & ACCESSORIES

8.6.3 ORAL APPLIANCES

8.6.4 OTHERS

8.7 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (ASP IN USD/UNIT)

8.7.1 DEVICES

8.7.2 CONSUMABLES & ACCESSORIES

8.7.3 ORAL APPLIANCES

8.7.4 OTHERS

8.8 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.8.1 POSITIVE AIRWAY PRESSURE (PAP) DEVICES

8.8.2 POLYSOMNOGRAPHY DEVICES

8.8.3 HOME SLEEP TESTING DEVICES

8.8.4 OTHERS

8.9 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.9.1 POSITIVE AIRWAY PRESSURE (PAP) DEVICES

8.9.2 POLYSOMNOGRAPHY DEVICES

8.9.3 HOME SLEEP TESTING DEVICES

8.9.4 OTHERS

8.1 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.10.1 POSITIVE AIRWAY PRESSURE (PAP) DEVICES

8.10.2 POLYSOMNOGRAPHY DEVICES

8.10.3 HOME SLEEP TESTING DEVICES

8.10.4 OTHERS

8.11 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.11.1 BY TYPE

8.11.2 BY MODALITY

8.12 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.12.1 CONTINUOUS POSITIVE AIRWAY PRESSURE (CPAP)

8.12.2 AUTOMATIC POSITIVE AIRWAY PRESSURE (APAP)

8.12.3 BILEVEL POSITIVE AIRWAY PRESSURE (BIPAP)

8.12.4 NASAL EXPIRATORY POSITIVE AIRWAY PRESSURE(NASAL EPAP) DEVICES

8.12.5 OTHERS

8.13 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.13.1 CONTINUOUS POSITIVE AIRWAY PRESSURE (CPAP)

8.13.2 AUTOMATIC POSITIVE AIRWAY PRESSURE (APAP)

8.13.3 BILEVEL POSITIVE AIRWAY PRESSURE (BIPAP)

8.13.4 NASAL EPAP DEVICES

8.13.5 OTHERS

8.14 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.14.1 CONTINUOUS POSITIVE AIRWAY PRESSURE (CPAP)

8.14.2 AUTOMATIC POSITIVE AIRWAY PRESSURE (APAP)

8.14.3 BILEVEL POSITIVE AIRWAY PRESSURE (BIPAP)

8.14.4 NASAL EPAP DEVICES

8.14.5 OTHERS

8.15 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (USD THOUSAND)

8.15.1 FIXED PAP DEVICES

8.15.2 AUTO-ADJUSTING PAP DEVICES

8.15.3 TRAVEL-SIZED PAP DEVICES

8.16 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (THOUSAND UNITS)

8.16.1 FIXED PAP DEVICES

8.16.2 AUTO-ADJUSTING PAP DEVICES

8.16.3 TRAVEL-SIZED PAP DEVICES

8.17 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.17.1 FULL IN-LAB PSG

8.17.2 PORTABLE PSG

8.17.3 PSG SENSORS & ELECTRODES

8.17.4 OTHERS

8.18 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.18.1 FULL IN-LAB PSG

8.18.2 PORTABLE PSG

8.18.3 PSG SENSORS & ELECTRODES

8.18.4 OTHERS

8.19 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.19.1 FULL IN-LAB PSG

8.19.2 PORTABLE PSG

8.19.3 PSG SENSORS & ELECTRODES

8.19.4 OTHERS

8.2 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.20.1 TYPE I

8.20.2 TYPE II

8.21 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.21.1 TYPE I

8.21.2 TYPE II

8.22 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.22.1 TYPE I

8.22.2 TYPE II

8.23 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.23.1 WEARABLE SENSORS

8.23.2 CONNECTED SLEEP MONITORS

8.23.3 OXIMETERS

8.24 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.24.1 WEARABLE SENSORS

8.24.2 CONNECTED SLEEP MONITORS

8.24.3 OXIMETERS

8.25 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.25.1 WEARABLE SENSORS

8.25.2 CONNECTED SLEEP MONITORS

8.25.3 OXIMETERS

8.26 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.26.1 FINGERTIP OXIMETERS

8.26.2 WRIST-WORN OXIMETERS

8.26.3 HANDHELD OXIMETERS

8.26.4 TABLETOP OXIMETERS

8.27 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.27.1 FINGERTIP OXIMETERS

8.27.2 WRIST-WORN OXIMETERS

8.27.3 HANDHELD OXIMETERS

8.27.4 TABLETOP OXIMETERS

8.28 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.28.1 FINGERTIP OXIMETERS

8.28.2 WRIST-WORN OXIMETERS

8.28.3 HANDHELD OXIMETERS

8.28.4 TABLETOP OXIMETERS

8.29 DEVICES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.29.1 NORTH AMERICA

8.29.2 EUROPE

8.29.3 ASIA-PACIFIC

8.29.4 SOUTH AMERICA

8.29.5 MIDDLE EAST AND AFRICA

8.3 DEVICES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

8.30.1 NORTH AMERICA

8.30.2 EUROPE

8.30.3 ASIA-PACIFIC

8.30.4 SOUTH AMERICA

8.30.5 MIDDLE EAST AND AFRICA

8.31 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.31.1 MASKS

8.31.2 PILLOWS

8.31.3 FILTERS & TUBING

8.31.4 BATTERY KITS

8.31.5 CHIN STRAPS

8.31.6 SENSORS

8.31.7 CANNULAS

8.31.8 TRAVEL CASES

8.31.9 BELTS

8.31.10 OTHERS

8.32 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.32.1 MASKS

8.32.2 PILLOWS

8.32.3 FILTERS & TUBING

8.32.4 BATTERY KITS

8.32.5 CHIN STRAPS

8.32.6 SENSORS

8.32.7 CANNULAS

8.32.8 TRAVEL CASES

8.32.9 BELTS

8.32.10 OTHERS

8.33 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.33.1 MASKS

8.33.2 PILLOWS

8.33.3 FILTERS & TUBING

8.33.4 BATTERY KITS

8.33.5 CHIN STRAPS

8.33.6 SENSORS

8.33.7 CANNULAS

8.33.8 TRAVEL CASES

8.33.9 BELTS

8.33.10 OTHERS

8.34 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.34.1 FULL FACE MASKS

8.34.2 NASAL MASKS

8.34.3 NASAL PILLOW MASKS

8.34.4 OTHERS

8.35 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.35.1 FULL FACE MASKS

8.35.2 NASAL MASKS

8.35.3 NASAL PILLOW MASKS

8.35.4 OTHERS

8.36 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

8.36.1 FULL FACE MASKS

8.36.2 NASAL MASKS

8.36.3 NASAL PILLOW MASKS

8.36.4 OTHERS

8.37 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.37.1 CERVICAL PILLOWS

8.37.2 WEDGE PILLOWS

8.38 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.38.1 CERVICAL PILLOWS

8.38.2 WEDGE PILLOWS

8.39 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

8.39.1 CERVICAL PILLOWS

8.39.2 WEDGE PILLOWS

8.4 CONSUMABLES & ACCESSORIES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.40.1 NORTH AMERICA

8.40.2 EUROPE

8.40.3 ASIA-PACIFIC

8.40.4 SOUTH AMERICA

8.40.5 MIDDLE EAST AND AFRICA

8.41 CONSUMABLES & ACCESSORIES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

8.41.1 NORTH AMERICA

8.41.2 EUROPE

8.41.3 ASIA-PACIFIC

8.41.4 SOUTH AMERICA

8.41.5 MIDDLE EAST AND AFRICA

8.42 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.42.1 MANDIBULAR ADVANCEMENT DEVICES

8.42.2 CUSTOMIZED ORAL APPLIANCES

8.42.3 TONGUE RETAINING DEVICES

8.42.4 NON-CUSTOMIZED ORAL APPLIANCES

8.42.5 OTHERS

8.43 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

8.43.1 MANDIBULAR ADVANCEMENT DEVICES

8.43.2 CUSTOMIZED ORAL APPLIANCES

8.43.3 TONGUE RETAINING DEVICES

8.43.4 NON-CUSTOMIZED ORAL APPLIANCES

8.43.5 OTHERS

8.44 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

8.44.1 MANDIBULAR ADVANCEMENT DEVICES

8.44.2 CUSTOMIZED ORAL APPLIANCES

8.44.3 TONGUE RETAINING DEVICES

8.44.4 NON-CUSTOMIZED ORAL APPLIANCES

8.44.5 OTHERS

8.45 ORAL APPLIANCES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.45.1 NORTH AMERICA

8.45.2 EUROPE

8.45.3 ASIA-PACIFIC

8.45.4 SOUTH AMERICA

8.45.5 MIDDLE EAST AND AFRICA

8.46 ORAL APPLIANCES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

8.46.1 NORTH AMERICA

8.46.2 EUROPE

8.46.3 ASIA-PACIFIC

8.46.4 SOUTH AMERICA

8.46.5 MIDDLE EAST AND AFRICA

8.47 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.47.1 NORTH AMERICA

8.47.2 EUROPE

8.47.3 ASIA-PACIFIC

8.47.4 SOUTH AMERICA

8.47.5 MIDDLE EAST AND AFRICA

8.48 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

8.48.1 NORTH AMERICA

8.48.2 EUROPE

8.48.3 ASIA-PACIFIC

8.48.4 SOUTH AMERICA

8.48.5 MIDDLE EAST AND AFRICA

9 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY MACHINERY TYPE

9.1 OVERVIEW

9.2 FIXED MACHINES

9.3 PORTABLE MACHINES

9.4 MIDDLE EAST AND AFRICA FIXED MACHINES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.4.1 HOMECARE MACHINES

9.4.2 HOSPITAL-GRADE MACHINES

9.5 FIXED MACHINES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.5.1 NORTH AMERICA

9.5.2 EUROPE

9.5.3 ASIA-PACIFIC

9.5.4 SOUTH AMERICA

9.5.5 MIDDLE EAST AND AFRICA

9.6 MIDDLE EAST AND AFRICA PORTABLE MACHINES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.6.1 WEARABLE DEVICES

9.6.2 MINIATURE TRAVEL DEVICES

9.7 PORTABLE MACHINES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.7.1 NORTH AMERICA

9.7.2 EUROPE

9.7.3 ASIA-PACIFIC

9.7.4 SOUTH AMERICA

9.7.5 MIDDLE EAST AND AFRICA

10 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY FUNCTION

10.1 OVERVIEW

10.1.1 AIRWAY PRESSURE

10.1.2 DATA RECORDING & CONNECTIVITY

10.1.3 AIRWAY MONITORING

10.1.4 OXYGEN THERAPY

10.1.5 HUMIDIFICATION

10.1.6 APNEA DETECTION

10.1.7 ALARM & ALERT SYSTEMS

10.1.8 OTHERS

10.2 AIRWAY PRESSURE IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.2.1 NORTH AMERICA

10.2.2 EUROPE

10.2.3 ASIA-PACIFIC

10.2.4 SOUTH AMERICA

10.2.5 MIDDLE EAST AND AFRICA

10.3 DATA RECORDING & CONNECTIVITY IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.3.1 NORTH AMERICA

10.3.2 EUROPE

10.3.3 ASIA-PACIFIC

10.3.4 SOUTH AMERICA

10.3.5 MIDDLE EAST AND AFRICA

10.4 AIRWAY MONITORING IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.4.1 NORTH AMERICA

10.4.2 EUROPE

10.4.3 ASIA-PACIFIC

10.4.4 SOUTH AMERICA

10.4.5 MIDDLE EAST AND AFRICA

10.5 OXYGEN THERAPY IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.5.1 NORTH AMERICA

10.5.2 EUROPE

10.5.3 ASIA-PACIFIC

10.5.4 SOUTH AMERICA

10.5.5 MIDDLE EAST AND AFRICA

10.6 HUMIDIFICATION IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.6.1 NORTH AMERICA

10.6.2 EUROPE

10.6.3 ASIA-PACIFIC

10.6.4 SOUTH AMERICA

10.6.5 MIDDLE EAST AND AFRICA

10.7 APNEA DETECTION IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.7.1 NORTH AMERICA

10.7.2 EUROPE

10.7.3 ASIA-PACIFIC

10.7.4 SOUTH AMERICA

10.7.5 MIDDLE EAST AND AFRICA

10.8 ALARM & ALERT SYSTEMS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.8.1 NORTH AMERICA

10.8.2 EUROPE

10.8.3 ASIA-PACIFIC

10.8.4 SOUTH AMERICA

10.8.5 MIDDLE EAST AND AFRICA

10.9 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.9.1 NORTH AMERICA

10.9.2 EUROPE

10.9.3 ASIA-PACIFIC

10.9.4 SOUTH AMERICA

10.9.5 MIDDLE EAST AND AFRICA

11 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY APPLICATION

11.1 OVERVIEW

11.2 OBSTRUCTIVE SLEEP APNEA

11.3 CENTRAL SLEEP APNEA

11.4 COMPLEX SLEEP APNEA SYNDROME

11.5 OTHERS

11.6 MIDDLE EAST AND AFRICA OBSTRUCTIVE SLEEP APNEA IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.6.1 DEVICES

11.6.2 CONSUMABLES & ACCESSORIES

11.6.3 ORAL APPLIANCE

11.6.4 OTHERS

11.7 OBSTRUCTIVE SLEEP APNEA IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.7.1 NORTH AMERICA

11.7.2 EUROPE

11.7.3 ASIA-PACIFIC

11.7.4 SOUTH AMERICA

11.7.5 MIDDLE EAST AND AFRICA

11.8 MIDDLE EAST AND AFRICA CENTRAL SLEEP APNEA IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.8.1 DEVICES

11.8.2 CONSUMABLES & ACCESSORIES

11.8.3 ORAL APPLIANCE

11.8.4 OTHERS

11.9 CENTRAL SLEEP APNEA IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.9.1 NORTH AMERICA

11.9.2 EUROPE

11.9.3 ASIA-PACIFIC

11.9.4 SOUTH AMERICA

11.9.5 MIDDLE EAST AND AFRICA

11.1 MIDDLE EAST AND AFRICA COMPLEX SLEEP APNEA SYNDROME IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.10.1 DEVICES

11.10.2 ORAL APPLIANCE

11.10.3 CONSUMABLES & ACCESSORIES

11.10.4 OTHERS

11.11 COMPLEX SLEEP APNEA SYNDROME IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.11.1 NORTH AMERICA

11.11.2 EUROPE

11.11.3 ASIA-PACIFIC

11.11.4 SOUTH AMERICA

11.11.5 MIDDLE EAST AND AFRICA

11.12 MIDDLE EAST AND AFRICA OTHERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.12.1 DEVICES

11.12.2 CONSUMABLES & ACCESSORIES

11.12.3 ORAL APPLIANCE

11.12.4 OTHERS

11.13 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.13.1 NORTH AMERICA

11.13.2 EUROPE

11.13.3 ASIA-PACIFIC

11.13.4 SOUTH AMERICA

11.13.5 MIDDLE EAST AND AFRICA

12 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY AGE GROUP

12.1 OVERVIEW

12.2 ADULT

12.3 GERIATRIC

12.4 PEDIATRIC

12.5 ADULT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.5.1 NORTH AMERICA

12.5.2 EUROPE

12.5.3 ASIA-PACIFIC

12.5.4 SOUTH AMERICA

12.5.5 MIDDLE EAST AND AFRICA

12.6 GERIATRIC IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.6.1 NORTH AMERICA

12.6.2 EUROPE

12.6.3 ASIA-PACIFIC

12.6.4 SOUTH AMERICA

12.6.5 MIDDLE EAST AND AFRICA

12.7 PEDIATRIC IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.7.1 NORTH AMERICA

12.7.2 EUROPE

12.7.3 ASIA-PACIFIC

12.7.4 SOUTH AMERICA

12.7.5 MIDDLE EAST AND AFRICA

13 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY END USER

13.1 OVERVIEW

13.2 HOSPITALS

13.3 HOME CARE SETTINGS

13.4 SLEEP LABORATORIES & CLINICS

13.5 AMBULATORY SURGICAL CENTERS

13.6 OTHERS

13.7 MIDDLE EAST AND AFRICA HOSPITALS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.7.1 PUBLIC

13.7.2 PRIVATE

13.8 HOSPITALS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.8.1 NORTH AMERICA

13.8.2 EUROPE

13.8.3 ASIA-PACIFIC

13.8.4 SOUTH AMERICA

13.8.5 MIDDLE EAST AND AFRICA

13.9 HOME CARE SETTINGS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.9.1 NORTH AMERICA

13.9.2 EUROPE

13.9.3 ASIA-PACIFIC

13.9.4 SOUTH AMERICA

13.9.5 MIDDLE EAST AND AFRICA

13.1 SLEEP LABORATORIES & CLINICS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.10.1 NORTH AMERICA

13.10.2 EUROPE

13.10.3 ASIA-PACIFIC

13.10.4 SOUTH AMERICA

13.10.5 MIDDLE EAST AND AFRICA

13.11 AMBULATORY SURGICAL CENTERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.11.1 NORTH AMERICA

13.11.2 EUROPE

13.11.3 ASIA-PACIFIC

13.11.4 SOUTH AMERICA

13.11.5 MIDDLE EAST AND AFRICA

13.12 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.12.1 NORTH AMERICA

13.12.2 EUROPE

13.12.3 ASIA-PACIFIC

13.12.4 SOUTH AMERICA

13.12.5 MIDDLE EAST AND AFRICA

14 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY DISTRIBUTION CHANNEL

14.1 OVERVIEW

14.2 INDIRECT

14.3 DIRECT

14.4 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (THOUSAND UNITS)

14.4.1 INDIRECT

14.4.2 DIRECT

14.5 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

14.5.1 ONLINE RETAILERS

14.5.2 OFFLINE RETAILERS

14.5.3 COMPANY OWNED WEBSITES

14.5.4 OTHERS

14.6 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

14.6.1 ONLINE RETAILERS

14.6.2 OFFLINE RETAILERS

14.6.3 COMPANY OWNED WEBSITES

14.6.4 OTHERS

14.7 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

14.7.1 NORTH AMERICA

14.7.2 EUROPE

14.7.3 ASIA-PACIFIC

14.7.4 SOUTH AMERICA

14.7.5 MIDDLE EAST AND AFRICA

14.8 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

14.8.1 NORTH AMERICA

14.8.2 EUROPE

14.8.3 ASIA-PACIFIC

14.8.4 SOUTH AMERICA

14.8.5 MIDDLE EAST AND AFRICA

14.9 DIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

14.9.1 NORTH AMERICA

14.9.2 EUROPE

14.9.3 ASIA-PACIFIC

14.9.4 SOUTH AMERICA

14.9.5 MIDDLE EAST AND AFRICA

14.1 DIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

14.10.1 NORTH AMERICA

14.10.2 EUROPE

14.10.3 ASIA-PACIFIC

14.10.4 SOUTH AMERICA

14.10.5 MIDDLE EAST AND AFRICA

15 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET BY REGION

15.1 MIDDLE EAST AND AFRICA

15.1.1 SAUDI ARABIA

15.1.2 SOUTH AFRICA

15.1.3 UNITED ARAB EMIRATES

15.1.4 EGYPT

15.1.5 ISRAEL

15.1.6 QATAR

15.1.7 KUWAIT

15.1.8 OMAN

15.1.9 BAHRAIN

15.1.10 REST OF MIDDLE EAST AND AFRICA

16 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET: COMPANY LANDSCAPE

16.1 MANUFACTURER COMPANY SHARE ANALYSIS: GLOBAL

17 SWOT ANALYSIS

18 COMPANY PROFILES

18.1 RESMED INC.

18.1.1 COMPANY SNAPSHOT

18.1.2 REVENUE ANALYSIS

18.1.3 COMPANY SHARE ANALYSIS

18.1.4 PRODUCT PORTFOLIO

18.1.5 RECENT UPDATES

18.2 PHILIPS RESPIRONICS (KONINKLIJKE PHILIPS N.V.)

18.2.1 COMPANY SNAPSHOT

18.2.2 REVENUE ANALYSIS

18.2.3 COMPANY SHARE ANALYSIS

18.2.4 PRODUCT PORTFOLIO

18.2.5 RECENT UPDATES

18.3 INSPIRE MEDICAL SYSTEMS

18.3.1 COMPANY SNAPSHOT

18.3.2 REVENUE ANALYSIS

18.3.3 COMPANY SHARE ANALYSIS

18.3.4 PRODUCT PORTFOLIO

18.3.5 RECENT UPDATES

18.4 FISHER & PAYKEL HEALTHCARE

18.4.1 COMPANY SNAPSHOT

18.4.2 REVENUE ANALYSIS

18.4.3 COMPANY SHARE ANALYSIS

18.4.4 PRODUCT PORTFOLIO

18.4.5 RECENT UPDATES

18.5 BMC MEDICAL CO., LTD.

18.5.1 COMPANY SNAPSHOT

18.5.2 REVENUE ANALYSIS

18.5.3 COMPANY SHARE ANALYSIS

18.5.4 PRODUCT PORTFOLIO

18.5.5 RECENT DEVELOPMENT

18.6 ABABIL MEDTECH INNOVATIONS INDIA PVT LTD

18.6.1 COMPANY SNAPSHOT

18.6.2 PRODUCT PORTFOLIO

18.6.3 RECENT DEVELOPMENT

18.7 ADVANCED BRAIN MONITORING, INC.

18.7.1 COMPANY SNAPSHOT

18.7.2 PRODUCT PORTFOLIO

18.7.3 RECENT DEVELOPMENT

18.8 BEIJING AEON MEDICAL SYSTEMS CO., LTD.

18.8.1 COMPANY SNAPSHOT

18.8.2 PRODUCT PORTFOLIO

18.8.3 RECENT DEVELOPMENT

18.9 BPL MEDICAL TECHNOLOGIES PRIVATE LIMITED

18.9.1 COMPANY SNAPSHOT

18.9.2 PRODUCT PORTFOLIO

18.9.3 RECENT DEVELOPMENT

18.1 BREAS MEDICAL

18.10.1 COMPANY SNAPSHOT

18.10.2 PRODUCT PORTFOLIO

18.10.3 RECENT DEVELOPMENT

18.11 CADWELL INDUSTRIES INC.

18.11.1 COMPANY SNAPSHOT

18.11.2 PRODUCT PORTFOLIO

18.11.3 RECENT DEVELOPMENT

18.12 COMPUMEDICS

18.12.1 COMPANY SNAPSHOT

18.12.2 REVENUE ANALYSIS

18.12.3 PRODUCT PORTFOLIO

18.12.4 RECENT DEVELOPMENT

18.13 DESCO MEDICAL INDIA

18.13.1 COMPANY SNAPSHOT

18.13.2 PRODUCT PORTFOLIO

18.13.3 RECENT DEVELOPMENT

18.14 DECKMOUNT

18.14.1 COMPANY SNAPSHOT

18.14.2 PRODUCT PORTFOLIO

18.14.3 RECENT DEVELOPMENT

18.15 DRIVE DEVILBISS HEALTHCARE

18.15.1 COMPANY SNAPSHOT

18.15.2 PRODUCT PORTFOLIO

18.15.3 RECENT UPDATES

18.16 HAMILTON MEDICAL

18.16.1 COMPANY SNAPSHOT

18.16.2 PRODUCT PORTFOLIO

18.16.3 RECENT DEVELOPMENT

18.17 HUNAN BEYOND MEDICAL TECHNOLOGY CO., LTD.

18.17.1 CO MPANY SNAPSHOT

18.17.2 PRODUCT PORTFOLIO

18.17.3 RECENT DEVELOPMENT

18.18 INNACCEL TECHNOLOGIES PVT LTD

18.18.1 COMPANY SNAPSHOT

18.18.2 PRODUCT PORTFOLIO

18.18.3 RECENT DEVELOPMENT

18.19 LOEWENSTEIN MEDICAL

18.19.1 COMPANY SNAPSHOT

18.19.2 PRODUCT PORTFOLIO

18.19.3 RECENT UPDATES

18.2 MEDTRONIC.

18.20.1 COMPANY SNAPSHOT

18.20.2 REVENUE ANALYSIS

18.20.3 PRODUCT PORTFOLIO

18.20.4 RECENT DEVELOPMENT

18.21 NARANG MEDICAL LIMITED

18.21.1 COMPANY SNAPSHOT

18.21.2 PRODUCT PORTFOLIO

18.21.3 RECENT DEVELOPMENT

18.22 NATUS MEDICAL INCORPORATED

18.22.1 COMPANY SNAPSHOT

18.22.2 PRODUCT PORTFOLIO

18.22.3 RECENT DEVELOPMENT

18.23 NAREENA LIFESCIENCES PRIVATE LIMITED

18.23.1 COMPANY SNAPSHOT

18.23.2 PRODUCT PORTFOLIO

18.23.3 RECENT DEVELOPMENT

18.24 NIDEK MEDICAL INDIA

18.24.1 COMPANY SNAPSHOT

18.24.2 PRODUCT PORTFOLIO

18.24.3 RECENT DEVELOPMENT

18.25 NIHON KOHDEN CORPORATION

18.25.1 COMPANY SNAPSHOT

18.25.2 REVENUE ANALYSIS

18.25.3 PRODUCT PORTFOLIO

18.25.4 RECENT DEVELOPMENT

18.26 OXYMED INDIA (PART OF - MEDEQUIP HEALTHCARE SOLUTIONS PVT LTD)

18.26.1 COMPANY SNAPSHOT

18.26.2 PRODUCT PORTFOLIO

18.26.3 RECENT DEVELOPMENT

18.27 PROSOMNUS SLEEP TECHNOLOGIES

18.27.1 COMPANY SNAPSHOT

18.27.2 PRODUCT PORTFOLIO

18.27.3 RECENT UPDATES

18.28 REACT HEALTH

18.28.1 COMPANY SNAPSHOT

18.28.2 PRODUCT PORTFOLIO

18.28.3 RECENT DEVELOPMENT

18.29 SEFAM

18.29.1 COMPANY SNAPSHOT

18.29.2 PRODUCT PORTFOLIO

18.29.3 RECENT DEVELOPMENT

18.3 SOMNOMEDICS AMERICA INC.

18.30.1 COMPANY SNAPSHOT

18.30.2 PRODUCT PORTFOLIO

18.30.3 RECENT DEVELOPMENT

18.31 SOMNOMED

18.31.1 COMPANY SNAPSHOT

18.31.2 REVENUE ANALYSIS

18.31.3 PRODUCT PORTFOLIO

18.31.4 RECENT UPDATES

18.32 SUNSET HEALTHCARE SOLUTIONS

18.32.1 COMPANY SNAPSHOT

18.32.2 PRODUCT PORTFOLIO

18.32.3 RECENT DEVELOPMENT

18.33 TRANSCEND, INC.

18.33.1 COMPANY SNAPSHOT

18.33.2 PRODUCT PORTFOLIO

18.33.3 RECENT UPDATES

18.34 WELLELL (APEX MEDICA)

18.34.1 COMPANY SNAPSHOT

18.34.2 REVENUE ANALYSIS

18.34.3 PRODUCT PORTFOLIO

18.34.4 RECENT UPDATES

18.35 ZOLL MEDICAL

18.35.1 COMPANY SNAPSHOT

18.35.2 PRODUCT PORTFOLIO

18.35.3 RECENT DEVELOPMENT

19 QUESTIONNAIRE

20 RELATED REPORTS

List of Table

TABLE 1 COST MODEL

TABLE 2 REGIONAL OSA EPIDEMIOLOGY COMPARISON (2025)

TABLE 3 PENETRATION BY PRODUCT CATEGORY

TABLE 4 TECHNOLOGY ROADMAP

TABLE 5 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 6 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 7 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 8 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 9 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 10 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 11 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 12 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 13 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 14 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 15 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (USD THOUSAND)

TABLE 16 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (THOUSAND UNITS)

TABLE 17 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 18 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 19 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 20 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 21 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 22 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 23 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 24 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 25 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 26 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 27 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 28 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 29 DEVICES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 30 DEVICES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 31 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 32 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 33 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 34 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 35 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 36 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

TABLE 37 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 38 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 39 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

TABLE 40 CONSUMABLES & ACCESSORIES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 41 CONSUMABLES & ACCESSORIES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 42 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 43 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 44 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 45 ORAL APPLIANCES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 46 ORAL APPLIANCES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 47 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 48 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 49 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY MACHINERY TYPE , 2018-2033 (USD THOUSAND)

TABLE 50 MIDDLE EAST AND AFRICA FIXED MACHINES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 51 FIXED MACHINES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 52 MIDDLE EAST AND AFRICA PORTABLE MACHINES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 53 PORTABLE MACHINES IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 54 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY FUNCTION , 2018-2033 (USD THOUSAND)

TABLE 55 AIRWAY PRESSURE IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 56 DATA RECORDING & CONNECTIVITY IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 57 AIRWAY MONITORING IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 58 OXYGEN THERAPY IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 59 HUMIDIFICATION IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 60 APNEA DETECTION IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 61 ALARM & ALERT SYSTEMS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 62 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 63 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 64 MIDDLE EAST AND AFRICA OBSTRUCTIVE SLEEP APNEA IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 65 OBSTRUCTIVE SLEEP APNEA IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 66 MIDDLE EAST AND AFRICA CENTRAL SLEEP APNEA IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 67 CENTRAL SLEEP APNEA IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 68 MIDDLE EAST AND AFRICA COMPLEX SLEEP APNEA SYNDROME IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 69 COMPLEX SLEEP APNEA SYNDROME IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 70 MIDDLE EAST AND AFRICA OTHERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 71 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 72 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY AGE GROUP, 2018-2033 (USD THOUSAND)

TABLE 73 ADULT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 74 GERIATRIC IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 75 PEDIATRIC IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 76 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 77 MIDDLE EAST AND AFRICA HOSPITALS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 78 HOSPITALS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 79 HOME CARE SETTINGS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 80 SLEEP LABORATORIES & CLINICS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 81 AMBULATORY SURGICAL CENTERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 82 OTHERS IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 83 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 84 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (THOUSAND UNITS)

TABLE 85 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 86 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 87 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 88 INDIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 89 DIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 90 DIRECT IN MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY REGION, 2018-2033 (THOUSAND UNITS)

TABLE 91 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 92 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 93 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 94 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 95 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 96 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 97 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 98 MIDDLE EAST AND AFRICA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 99 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 100 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 101 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 102 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (USD THOUSAND)

TABLE 103 MIDDLE EAST AND AFRICA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (THOUSAND UNITS)

TABLE 104 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 105 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 106 MIDDLE EAST AND AFRICA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 107 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 108 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 109 MIDDLE EAST AND AFRICA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 110 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 111 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 112 MIDDLE EAST AND AFRICA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 113 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 114 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 115 MIDDLE EAST AND AFRICA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 116 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 117 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 118 MIDDLE EAST AND AFRICA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 119 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 120 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 121 MIDDLE EAST AND AFRICA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

TABLE 122 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 123 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 124 MIDDLE EAST AND AFRICA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

TABLE 125 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 126 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 127 MIDDLE EAST AND AFRICA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 128 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY MACHINERY TYPE , 2018-2033 (USD THOUSAND)

TABLE 129 MIDDLE EAST AND AFRICA FIXED MACHINES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 130 MIDDLE EAST AND AFRICA PORTABLE MACHINES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 131 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY FUNCTION , 2018-2033 (USD THOUSAND)

TABLE 132 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 133 MIDDLE EAST AND AFRICA OBSTRUCTIVE SLEEP APNEA IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 134 MIDDLE EAST AND AFRICA CENTRAL SLEEP APNEA IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 135 MIDDLE EAST AND AFRICA COMPLEX SLEEP APNEA SYNDROME IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 136 MIDDLE EAST AND AFRICA OTHERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 137 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY AGE GROUP, 2018-2033 (USD THOUSAND)

TABLE 138 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 139 MIDDLE EAST AND AFRICA HOSPITALS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 140 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 141 MIDDLE EAST AND AFRICA SLEEP APNEA DEVICES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (THOUSAND UNITS)

TABLE 142 MIDDLE EAST AND AFRICA INDIRECT IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 143 MIDDLE EAST AND AFRICA INDIRECT IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 144 SAUDI ARABIA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 145 SAUDI ARABIA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 146 SAUDI ARABIA SLEEP APNEA DEVICES MARKET, BY PRODUCT TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 147 SAUDI ARABIA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 148 SAUDI ARABIA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 149 SAUDI ARABIA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 150 SAUDI ARABIA DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 151 SAUDI ARABIA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 152 SAUDI ARABIA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 153 SAUDI ARABIA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 154 SAUDI ARABIA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (USD THOUSAND)

TABLE 155 SAUDI ARABIA POSITIVE AIRWAY PRESSURE (PAP) DEVICES IN SLEEP APNEA DEVICES MARKET, BY MODALITY, 2018-2033 (THOUSAND UNITS)

TABLE 156 SAUDI ARABIA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 157 SAUDI ARABIA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 158 SAUDI ARABIA POLYSOMNOGRAPHY DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 159 SAUDI ARABIA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 160 SAUDI ARABIA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 161 SAUDI ARABIA PORTABLE PSG IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 162 SAUDI ARABIA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 163 SAUDI ARABIA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 164 SAUDI ARABIA HOME SLEEP TESTING DEVICES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 165 SAUDI ARABIA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 166 SAUDI ARABIA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 167 SAUDI ARABIA OXIMETERS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 168 SAUDI ARABIA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 169 SAUDI ARABIA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 170 SAUDI ARABIA CONSUMABLES & ACCESSORIES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 171 SAUDI ARABIA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 172 SAUDI ARABIA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 173 SAUDI ARABIA MASKS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

TABLE 174 SAUDI ARABIA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 175 SAUDI ARABIA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 176 SAUDI ARABIA PILLOWS IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD PER UNIT)

TABLE 177 SAUDI ARABIA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 178 SAUDI ARABIA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (THOUSAND UNITS)

TABLE 179 SAUDI ARABIA ORAL APPLIANCES IN SLEEP APNEA DEVICES MARKET, BY TYPE, 2018-2033 (ASP IN USD/UNIT)

TABLE 180 SAUDI ARABIA SLEEP APNEA DEVICES MARKET, BY MACHINERY TYPE , 2018-2033 (USD THOUSAND)