Middle East And Africa Transplant Diagnostics Market

Market Size in USD Million

USD

298.17 Million

USD

430.56 Million

2025

2033

USD

298.17 Million

USD

430.56 Million

2025

2033

| 2026 - 2033 | |

| USD 298.17 Million | |

| USD 430.56 Million | |

| % | |

|

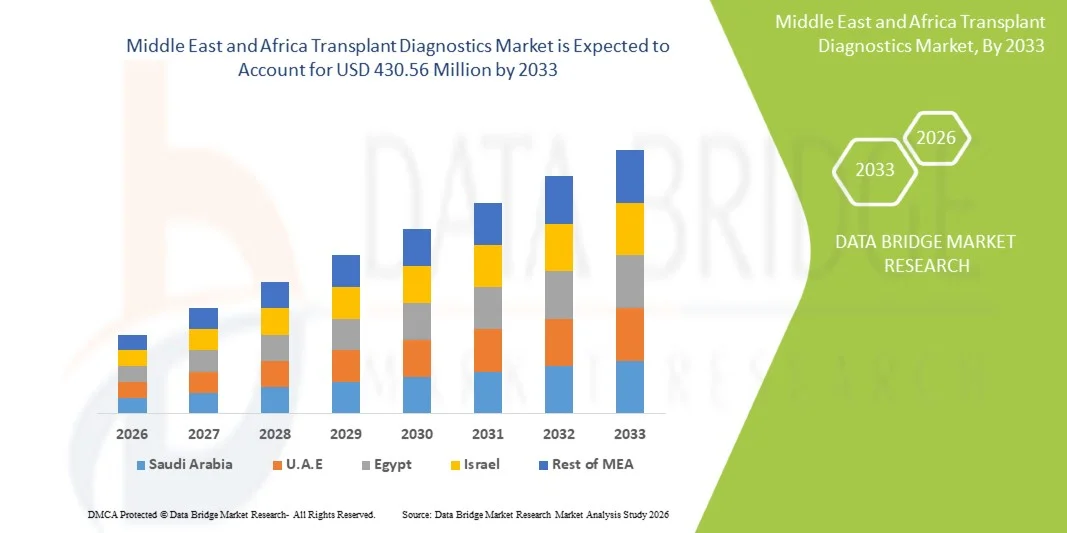

Middle East and Africa Transplant Diagnostics Market Size

- The Middle East and Africa transplant diagnostics market size was valued at USD 298.17 million in 2025 and is expected to reach USD 430.56 million by 2033, at a CAGR of 4.7% during the forecast period

- The market growth is largely driven by the rising prevalence of chronic diseases such as kidney failure and liver disorders, increasing demand for organ transplantation, and improving healthcare infrastructure across the region, leading to greater adoption of advanced diagnostic solutions

- Furthermore, growing awareness regarding early compatibility testing, advancements in molecular diagnostic technologies, and increasing government and private sector investments in transplant programs are establishing transplant diagnostics as a critical component in successful transplant procedures. These converging factors are accelerating the uptake of transplant diagnostic solutions, thereby significantly boosting the market growth

Middle East and Africa Transplant Diagnostics Market Analysis

- Transplant diagnostics, encompassing advanced testing methods such as molecular assays and histocompatibility testing to ensure donor-recipient compatibility, are becoming increasingly critical in modern healthcare systems across both public and private hospitals due to their role in improving transplant success rates and patient outcomes

- The escalating demand for transplant diagnostics is primarily fueled by the rising burden of chronic diseases leading to organ failure, increasing number of transplant procedures, and growing awareness about the importance of pre- and post-transplant monitoring

- Saudi Arabia dominated the market with the largest revenue share of 28.6% in 2025, characterized by improving healthcare infrastructure, higher healthcare expenditure, and expanding transplant programs, with the country witnessing significant growth driven by strong government initiatives and adoption of advanced diagnostic technologies

- South Africa is expected to be the fastest growing country in the Middle East and Africa transplant diagnostics market during the forecast period due to improving healthcare access, rising investments in medical infrastructure, and increasing focus on strengthening organ transplantation frameworks

- PCR-Based Molecular Assays segment dominated the transplant diagnostics market with a significant market share of 46.3% in 2025, driven by their high accuracy, sensitivity, and growing adoption in compatibility testing and post-transplant monitoring

Report Scope and Middle East and Africa Transplant Diagnostics Market Segmentation

|

Attributes |

Middle East and Africa Transplant Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Transplant Diagnostics Market Trends

“Advancement in Molecular and Precision-Based Diagnostic Technologies”

- A significant and accelerating trend in the Middle East and Africa transplant diagnostics market is the growing adoption of advanced molecular diagnostic techniques such as next-generation sequencing (NGS) and PCR-based assays, improving donor-recipient compatibility assessment and transplant success rates

- For instance, several transplant centers in Saudi Arabia and the UAE are increasingly utilizing NGS-based HLA typing platforms to enhance accuracy and reduce turnaround time in compatibility testing workflows

- Integration of molecular diagnostics enables earlier detection of transplant rejection risks and infectious complications, while improving post-transplant monitoring through more precise and data-driven insights

- The adoption of centralized laboratory networks and digital reporting systems is enabling better coordination between transplant centers and diagnostic laboratories, improving efficiency and standardization of testing processes

- This shift toward high-precision, technology-driven diagnostic solutions is transforming clinical decision-making, as healthcare providers increasingly rely on advanced tools for improved patient outcomes in transplant procedures

- Increasing collaboration between diagnostic companies and transplant centers to develop customized testing panels is further enhancing the adoption of tailored diagnostic solutions across complex transplant cases

Middle East and Africa Transplant Diagnostics Market Dynamics

Driver

“Rising Organ Failure Cases and Expansion of Transplant Programs”

- The increasing prevalence of chronic diseases such as kidney failure, diabetes, and liver disorders, coupled with the gradual expansion of organ transplantation programs, is a key driver for the growing demand for transplant diagnostics in the region

- For instance, in recent years, countries such as Saudi Arabia have expanded national transplant initiatives and registry systems to improve organ donation and transplantation rates, boosting the need for compatibility testing and related diagnostics

- As healthcare systems improve and awareness regarding organ donation increases, more patients are undergoing transplant procedures, requiring reliable and accurate diagnostic support before and after transplantation

- Furthermore, growing investments in healthcare infrastructure, establishment of specialized transplant centers, and increasing availability of skilled professionals are supporting the adoption of advanced diagnostic technologies

- The rising demand for early and precise donor-recipient matching, along with improved post-transplant monitoring, is significantly propelling the uptake of transplant diagnostic solutions across hospitals and laboratories

- Government-led awareness campaigns and public-private partnerships aimed at increasing organ donation rates are further strengthening the demand for transplant diagnostic services

Restraint/Challenge

“Limited Access to Advanced Infrastructure and High Cost of Diagnostic Procedures”

- Limited access to advanced laboratory infrastructure and uneven distribution of specialized transplant centers across certain countries in the Middle East and Africa poses a significant challenge to market growth

- For instance, many healthcare facilities in parts of Africa still rely on basic diagnostic capabilities, restricting the widespread adoption of advanced molecular and histocompatibility testing technologies

- High costs associated with transplant diagnostic tests, including molecular assays and HLA typing, can limit their accessibility, particularly in public healthcare systems and price-sensitive markets

- Furthermore, the shortage of trained laboratory professionals and lack of standardized diagnostic frameworks in some countries hinder the consistent implementation of advanced transplant diagnostic solutions

- Addressing these challenges through increased healthcare investments, expansion of diagnostic infrastructure, and cost-effective testing solutions will be critical for improving accessibility and supporting long-term market growth

- In addition, logistical constraints related to sample transportation and cold chain maintenance in remote areas further impact timely and reliable diagnostic testing outcomes

Middle East and Africa Transplant Diagnostics Market Scope

The market is segmented on the basis of product type, technology, transplant type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the transplant diagnostics market is segmented into transplant diagnostic instruments, transplant diagnostic software, and transplant diagnostic reagents. The transplant diagnostic reagents segment dominated the market with the largest market revenue share of 52.4% in 2025, driven by their recurring usage in laboratory testing procedures such as HLA typing, crossmatching, and molecular assays. Reagents are essential consumables in both routine and advanced transplant compatibility testing, ensuring consistent demand across diagnostic laboratories and hospitals. The increasing number of transplant procedures and repeated testing requirements for pre- and post-transplant monitoring further support the dominance of this segment. In addition, the availability of a wide range of standardized reagent kits tailored for different transplant applications enhances their adoption across healthcare facilities. The segment benefits from continuous replenishment cycles, making it a steady revenue generator for market players.

The transplant diagnostic software segment is anticipated to witness the fastest growth rate of 19.8% from 2026 to 2033, fueled by the growing need for data management, workflow automation, and integration of diagnostic results with hospital information systems. Software solutions enable efficient interpretation of complex molecular data, improve laboratory efficiency, and support decision-making in transplant compatibility assessments. Increasing adoption of digital pathology, AI-enabled analytics, and cloud-based platforms is further accelerating the uptake of software solutions in transplant diagnostics. Growing emphasis on interoperability and centralized data platforms is also contributing to the rapid expansion of this segment.

- By Technology

On the basis of technology, the transplant diagnostics market is segmented into PCR-based molecular assays and sequencing-based molecular assays. The PCR-based molecular assays segment held the largest market revenue share of 46.3% in 2025, driven by their widespread use in HLA typing, pathogen detection, and compatibility testing due to their cost-effectiveness, high sensitivity, and established clinical utility. PCR-based methods are widely adopted in laboratories across the region because of their relatively simpler workflow, faster turnaround time, and compatibility with existing laboratory infrastructure. Their proven reliability in routine transplant diagnostics continues to make them the preferred choice in many healthcare settings. In addition, lower operational complexity and availability of skilled technicians further strengthen their dominance. The segment also benefits from well-established regulatory acceptance and standardized protocols.

The sequencing-based molecular assays segment is expected to witness the fastest CAGR of 21.3% from 2026 to 2033, driven by the increasing adoption of next-generation sequencing (NGS) technologies for high-resolution HLA typing and comprehensive genetic analysis. Sequencing-based methods offer greater accuracy, deeper insights into genetic compatibility, and improved detection of rare alleles, making them highly suitable for complex transplant cases. Growing investments in advanced laboratory infrastructure and the shift toward precision medicine are further supporting the rapid growth of this segment. Rising demand for personalized transplant matching and improved graft survival outcomes is also accelerating adoption.

- By Transplant Type

On the basis of transplant type, the market is segmented into solid organ transplantation, stem cell transplantation, soft tissue transplantation, bone marrow transplantation, and others. The solid organ transplantation segment dominated the market with the largest revenue share of 48.9% in 2025, driven by the high prevalence of kidney, liver, and heart transplant procedures across the region. Rising incidence of chronic diseases such as renal failure and liver cirrhosis is significantly contributing to the demand for transplant diagnostics in solid organ procedures. These procedures require rigorous compatibility testing and continuous post-transplant monitoring, which further supports the dominance of this segment. Increasing availability of transplant centers and improved surgical outcomes are also boosting procedure volumes. The segment continues to benefit from strong clinical demand and established diagnostic protocols.

The stem cell transplantation segment is anticipated to witness the fastest growth rate of 18.6% from 2026 to 2033, fueled by increasing adoption of hematopoietic stem cell therapies for treating blood disorders such as leukemia and lymphoma. Advancements in donor matching techniques and growing awareness about stem cell therapies are encouraging more patients and healthcare providers to opt for these procedures. In addition, improvements in diagnostic techniques for immune compatibility and genetic profiling are enhancing the success rates of stem cell transplants, driving segment growth. Expanding clinical research and rising treatment accessibility are further supporting adoption.

- By Application

On the basis of application, the market is segmented into diagnostic applications and research applications. The diagnostic applications segment dominated the market with the largest revenue share of 68.1% in 2025, driven by the critical role of transplant diagnostics in pre-transplant compatibility testing, donor selection, and post-transplant monitoring. Hospitals and transplant centers heavily rely on diagnostic solutions to ensure accurate matching and reduce the risk of organ rejection. The increasing number of transplant procedures and rising need for precise and timely diagnostics further reinforce the dominance of this segment. Strong clinical demand and routine usage in patient care workflows also contribute to its leadership. The segment benefits from continuous utilization across all stages of the transplant process.

The research applications segment is expected to witness the fastest growth rate of 17.4% from 2026 to 2033, driven by increasing clinical research activities focused on improving transplant outcomes, immunology studies, and development of advanced diagnostic methods. Academic institutions and research laboratories are investing in innovative technologies to better understand transplant rejection mechanisms and enhance compatibility testing techniques. Growing collaborations between research organizations and diagnostic companies are also supporting advancements in this segment. Expanding funding for biomedical research and translational studies is further accelerating growth.

- By End User

On the basis of end user, the market is segmented into research laboratories and academic institutes, hospital and transplant centers, commercial service providers, and others. The hospital and transplant centers segment dominated the market with the largest revenue share of 61.7% in 2025, driven by the high volume of transplant procedures conducted in these facilities and their direct involvement in patient care. These centers require comprehensive diagnostic solutions for pre-transplant screening, donor matching, and post-operative monitoring, making them the primary consumers of transplant diagnostics. Increasing investments in specialized transplant centers and expansion of healthcare infrastructure further support the dominance of this segment. Availability of skilled professionals and integrated diagnostic workflows also enhance adoption. The segment remains central to clinical decision-making in transplantation.

The commercial service providers segment is expected to witness the fastest growth rate of 20.2% from 2026 to 2033, fueled by the rising outsourcing of diagnostic services to specialized laboratories. These providers offer advanced testing capabilities, cost efficiencies, and faster turnaround times, making them an attractive option for smaller hospitals and clinics. Increasing demand for centralized testing services and the growth of independent diagnostic laboratories are further contributing to the rapid expansion of this segment. Improved logistics, digital reporting, and scalable infrastructure are also supporting growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the market with the largest revenue share of 74.3% in 2025, driven by bulk procurement of diagnostic instruments, reagents, and software by hospitals, government institutions, and transplant centers through formal bidding processes. Direct tenders ensure standardized pricing, long-term supply agreements, and reliable access to critical diagnostic products, making them the preferred procurement method in institutional settings. Government-led healthcare initiatives and centralized purchasing systems further reinforce the dominance of this segment. Large-volume purchases and contractual supply arrangements also contribute to sustained revenue generation. The segment benefits from structured procurement frameworks across public healthcare systems.

The retail sales segment is anticipated to witness the fastest growth rate of 16.9% from 2026 to 2033, driven by increasing demand from smaller diagnostic laboratories, private clinics, and research facilities that procure products through distributors and online channels. Expanding distribution networks, improved product availability, and the growth of e-commerce platforms for laboratory supplies are contributing to the rising adoption of retail sales channels in the region. Greater accessibility and flexibility in purchasing options are also supporting segment expansion. Increasing penetration of third-party distributors further enhances market reach.

Middle East and Africa Transplant Diagnostics Market Regional Analysis

- Saudi Arabia dominated the market with the largest revenue share of 28.6% in 2025, characterized by improving healthcare infrastructure, higher healthcare expenditure, and expanding transplant programs, with the country witnessing significant growth driven by strong government initiatives and adoption of advanced diagnostic technologies

- Healthcare providers in the country highly value advanced molecular diagnostic technologies, standardized compatibility testing, and integrated laboratory systems to improve transplant success rates and patient outcomes

- This widespread adoption is further supported by rising healthcare expenditure, government-led initiatives to expand organ donation programs, and the growing availability of skilled professionals, establishing transplant diagnostics as a critical component of modern transplant care

The Saudi Arabia Transplant Diagnostics Market Insight

The Saudi Arabia transplant diagnostics market captured the largest revenue share in 2025 within the Middle East and Africa region, fueled by the rapid expansion of transplant programs and growing investments in advanced healthcare infrastructure. Healthcare providers are increasingly prioritizing precise compatibility testing through molecular diagnostics to improve transplant success rates and patient outcomes. The growing adoption of NGS-based HLA typing, along with well-established transplant centers, further supports market growth. In addition, government initiatives aimed at increasing organ donation awareness and strengthening national healthcare capabilities are significantly contributing to the expansion of transplant diagnostics in the country.

United Arab Emirates Transplant Diagnostics Market Insight

The United Arab Emirates transplant diagnostics market is experiencing strong growth due to the country’s advanced healthcare infrastructure and increasing focus on medical tourism. The UAE is witnessing rising adoption of state-of-the-art molecular diagnostic technologies to support organ transplantation procedures. High healthcare expenditure, along with the presence of internationally accredited hospitals and transplant centers, is further driving demand. In addition, government initiatives to enhance organ donation awareness and strengthen transplant frameworks are supporting the expansion of transplant diagnostics in the country.

Qatar Transplant Diagnostics Market Insight

The Qatar transplant diagnostics market is growing steadily, driven by increasing investments in healthcare infrastructure and the expansion of specialized medical facilities. The country is focusing on improving transplant care services by adopting advanced diagnostic technologies for accurate donor-recipient matching. Rising awareness about organ donation, along with government support for healthcare innovation, is contributing to market growth. Furthermore, the presence of well-equipped hospitals and collaborations with international healthcare providers are enhancing the adoption of transplant diagnostic solutions in Qatar.

South Africa Transplant Diagnostics Market Insight

The South Africa transplant diagnostics market is witnessing gradual growth, supported by improving healthcare infrastructure and increasing availability of specialized diagnostic laboratories. The country is focusing on expanding access to transplant procedures, particularly for kidney and bone marrow transplants, which is driving demand for compatibility testing and molecular diagnostics. Growing awareness about organ donation and rising participation from private healthcare providers are further contributing to market development. In addition, collaborations between public and private sectors are helping enhance diagnostic capabilities and improve transplant outcomes across the country.

Middle East and Africa Transplant Diagnostics Market Share

The Middle East and Africa Transplant Diagnostics industry is primarily led by well-established companies, including:

- QIAGEN (Netherlands)

- Thermo Fisher Scientific Inc. (U.S.)

- BIOMÉRIEUX (France)

- CareDx, Inc. (U.S.)

- Luminex Corporation (U.S.)

- BD (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Immucor Transplant Diagnostics, Inc. (U.S.)

- GenDx (Netherlands)

- Siemens Healthineers AG (Germany)

- Danaher (U.S.)

- Sysmex Corporation (Japan)

- Hologic, Inc. (U.S.)

- Bruker Corporation (U.S.)

- Werfen Group (Spain)

- Diasorin S.p.A. (Italy)

- Seegene, Inc. (South Korea)

What are the Recent Developments in Middle East and Africa Transplant Diagnostics Market?

- In March 2026, Dubai Health reported a 46% increase in kidney transplant procedures in 2025, highlighting rising awareness and expansion of organ donation and transplant services, which indirectly supports demand for transplant diagnostics and compatibility testing infrastructure in the UAE

- In February 2026, Medcare announced plans to expand with a new organ transplant centre in Sharjah, UAE, marking a strategic development in transplant care facilities in the region that will rely on enhanced diagnostic and compatibility testing services to support transplant procedures

- In December 2025, PureHealth launched the UAE’s largest AI-powered standalone diagnostic laboratory in Abu Dhabi, equipped to perform advanced histocompatibility testing for organ and bone marrow transplants as part of its comprehensive diagnostic services. This facility integrates AI, robotics, and automation to process millions of samples annually, significantly strengthening the UAE’s transplant diagnostics infrastructure

- In October 2025, a pioneering medical workshop in South Africa showcased machine perfusion technology that keeps donor organs viable longer, improving transplant outcomes and expanding the donor pool an advancement with implications for transplant diagnostics and patient matching protocols in the region

- In April 2025, the Organ Transplant Centre of Excellence (OTCoE) at King Faisal Specialist Hospital & Research Centre in Saudi Arabia won the ADGHW Innovation Award for its excellence in transplant care and advanced surgical milestones, reflecting growth in transplant-related clinical services and associated diagnostic needs

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.