Middle East And Africa White Goods Market

Market Size in USD Billion

USD

33.54 Billion

USD

50.55 Billion

2024

2032

USD

33.54 Billion

USD

50.55 Billion

2024

2032

| 2025 - 2032 | |

| USD 33.54 Billion | |

| USD 50.55 Billion | |

| % | |

|

White Goods Market Analysis

The white goods market is experiencing robust growth, driven by inclination towards advanced model of refrigerators. As the Middle East and Africa white goods industry continues to expand, the consumption of washing machines in medical facilities is growing. Government initiatives towards energy efficient home appliances and rapidly emerging electronic brands with new technologies are providing opportunities for the market. Market dynamics are also influenced by high maintenance and service cost of refrigerators. Overall, the market is expected to continue expanding, with a focus on innovation and sustainability to meet evolving industrial demands.

White Goods Market Size

The Middle East and Africa White Goods Market size was valued at USD 33.54 billion in 2024 and is projected to reach USD 50.55 billion by 2032, with a CAGR of 5.26% during the forecast period of 2025 to 2032. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

White Goods Market Trends

“Rising Shares of Organized Retail Stores”

Increase in the retail outlet has made it possible for consumers to easily access the product everywhere and anytime. Consumers can directly reach to their nearest retail outlet and enquire for the specific product which they wish to buy. Retail acts as a mode of promotion for the products. Brands usually put big hoardings at the retail as a method to attract the consumers. Since, retail outlets are increasing in the number means market share of particular product is increasing which suggests more sale of that product. Also, market players are coming with more retail outlets in order to cover the large share of market. Instead of retail outlet of single brand, retailers are adopting new strategy by selling products of different brands from the same retail outlet. As it gives more option to the customers and chances of buying increases as if any customer doesn’t gets satisfied from the product of one brand, then they can shift to the other brand. For instance, In October, 2024 according to an article published by Forbes Middle East, the Middle East retail industry has thrived on robust economic growth and rising consumer incomes, though it now faces maturity, with many global retailers experiencing flat or negative growth. As technology reshapes consumer expectations, major retailers are enhancing their digital presence through e-commerce investments. The region's retail landscape is diverse yet concentrated, dominated by a few family-owned companies that hold franchises for international brands, especially in the luxury segment. This article highlights the largest retail chains, considering factors like employee numbers, geographical reach, brand diversity, and store space

Moreover, growing awareness, changing lifestyle and easily access to the products have made customers to reach out to retail outlets. Thus, increased share of organized retail is increasing the sales of white goods and hence is expected to propel the growth of the Middle East and Africa white goods market.

Report Scope and White Goods Market Segmentation

|

Attributes |

White Goods Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Saudi Arabia, U.A.E., Egypt, Qatar, Kuwait, Oman, Algeria, Morocco, Tunisia, Libya, and Rest of Middle East and Africa |

|

Key Market Players |

SAMSUNG (South Korea), LG Electronics (South Korea), Whirlpool Corporation (U.S.), Haier Group (China), Robert Bosch GmbH (Germany), AB Electrolux (Sweden), Nikai Group (U.A.E), Super General (U.A.E), Mitsubishi Electric Corporation (Japan), The Middleby Corporation (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

White Goods Market Definition

White goods refer to large household appliances primarily designed for daily use in domestic settings. These typically include refrigerators, washing machines, ovens, dishwashers, and air conditioners. Named for their traditional white enamel finish, these appliances play a crucial role in enhancing convenience, efficiency, and comfort in homes. White goods are generally characterized by their larger size and capacity compared to smaller appliances, often requiring permanent installation. They contribute significantly to modern lifestyles by automating tasks such as food preservation, laundry, and cooking. In recent years, the definition has expanded to include energy-efficient and smart appliances that integrate technology for improved functionality and user experience. Overall, white goods are essential components of contemporary household life.

White Goods Market Dynamics

Drivers

- Inclination towards Advanced Model of Refrigerators

Technological awareness in the refrigerators has increased the market of advanced models of refrigerators. Advance models of refrigerators include modern features such as automatic temperature controls, chiller, door style and sensors for lighting, among others. The market is inclining towards advanced model due to rise in buying power, technological advancement and smart refrigerators which can be controlled by smart phones and Wi-Fi.

In recent years, refrigerators are modified in such a way that they consume less electricity and save power for customers. In other words, power efficient models are highly in demand as they are cost effective and consume less energy. Moreover, smart refrigerators have inclined the market towards advanced refrigerators which are installed with the Wi-Fi feature and can be controlled through smart devices such as smart phones and laptops. Smart refrigerators are highly in demand as it can be controlled from any location through the mobile and only thing which it requires is an internet connection.

Other than Wi-Fi, refrigerators are installed with the sensing devices. Sensor devices used in the refrigerators, perform various functions such as finger print sensor allows anyone to open the gate of refrigerator just by a touch and heat sensor decreases the temperature when required. Also, anti-microbial refrigeration is one more important characteristic of advanced refrigerators which is inclining the market towards advanced model of refrigerators. The edges of refrigerators are coated with the silver line so that microbes entering during the continuous opening and closing of refrigerators would not harm the organic food inside the refrigerators.

For instance,

In May 2024, according to an article published by Hindustan Times, modern refrigerators are transforming food storage with advanced features like dual cooling systems and air purification technologies. Unlike traditional models, these innovative designs offer separate cooling zones for optimal freshness. Configurations such as French door refrigerators combine style and functionality, featuring spacious refrigerator compartments and convenient pull-out freezers. With adjustable shelves and smart connectivity, they cater to larger families or those seeking a high-end appliance. These refrigerators not only maximize storage but also enhance the kitchen's aesthetic, making them ideal for those who value convenience and elegance

Therefore, the automation and advancement in the refrigerator models has increased the demand for white goods and is expected to propel the growth of the Middle East and Africa white goods market.

- Growing Consumption of Washing Machines in Medical Facilities

Washing machines are used to get the dirt out of the clothes. In hospitals, laundry service is important from the healthcare point of view. Hospitals receive hundreds of patients everyday who suffer from different diseases. Their clothes get infected from the bacterial effects and diseases they carry with them.

In general, hospitals use washing machines that are designed for high temperature water. Generally, clothes are washed around 60-to-70-degree temperature to get rid of the bacteria and diseases. The clothes are usually left for at least 10 minutes in the washing machine for the washing purpose.

Washing machines help in the control of infectious diseases which can transfer from individual to others. Washing machines are required to maintain the standard of hygiene in the hospitals. Special detergents are used which can kill the bacteria such as Methicillin-resistant Staphylococcus aureus and microbes during the cleaning of the clothes to avoid the risk of cross infection.

Disposing off the infected clothes is not possible every time. Throwing of clothes with infectious diseases will also contaminate the surrounding, resulting in soil and air pollution. Washing clothes is primarily a suitable option for all these possible problems. Hence, demand of washing machines is increasing in the hospitals.

For instance,

In May 2022, according to an article published by DANUBE INTERNATIONAL, All rights reserved., In hospitals, maintaining high hygiene standards is crucial, making the installation of efficient laundry equipment essential to prevent infections from linens and clothing. Properly designed laundry facilities optimize water and energy use, influencing management decisions. Key considerations include sensitivity to contamination, the selection of appropriate fabrics, and effective management of laundry operations. Scheduling tasks ensures daily cleanliness, while advanced machines like washer extractors and barrier washers enhance efficiency and minimize germ contact. Overall, the choice of laundry equipment must align with the facility's hygiene requirements and operational needs

In conclusion, the rise in the number of patients and hospitals around the region and countries also acts as one the factors for the growing consumption of washing machines in hospitals and is thus is expected to drive the growth of the Middle East and Africa white goods market.

Opportunities

- Government Initiatives towards Energy Efficient Home Appliances

Smart home appliances include advanced home and kitchen automation technology that improves the way governments monitor and control machinery, heating, cooling, and lighting systems in residential places across the countries, increasing the efficiency of these systems. In recent years, various research activities and investments have been done by the governments of the Middle East and African countries to develop innovative and advanced home and kitchen appliances such as smart refrigerators, which would be more energy efficient in the long run.

The smart home initiative allows governments to make a real difference by implementing innovative technologies and identifying opportunities to save energy. Through the smart home initiative, the government is continuously adopting several measures to improve energy performance management in both residential and commercial buildings. This will lead to a reduction in environmental footprint and energy costs through the implementation of intelligent kitchen and home automation systems.

Energy efficiency involves efficient utilization of energy resources which promotes sustainable development. Against the backdrop of growing economies and a concurrent income growth in Middle east and Africa, the real estate sector of the region has undergone a drastic transformation in the past few years. The government policies of the countries of MEA have been at the crux, providing vital stimulus for the growth of the industry along with encouraging small and medium stake holders to invest in the real estate sector.

For instance,

In June, 2021 according to an article published by Zawya., countries in the Middle East are implementing national action plans to promote a greener economy, focusing on energy efficiency. Initiatives like Egypt Vision 2030 and Saudi Vision 2030 aim to combat climate change and enhance energy efficiency

Moreover, the developmental investments towards sustainability to manufacture home and kitchen appliances that would generate fewer emissions are further contributing to the increased demand for white goods. This, in turn, is expected to provide opportunity for growth of the Middle East and Africa white goods market.

- Rapidly Emerging Electronic Brands with New Technologies

The electronics sector is typically divided between consumer electronics, electric utilities, and general electronics, where, the consumer electronics drive most of the growth in the sector which mainly includes smart home and kitchen appliances. The rising demand for smartphones, artificial intelligence, and voice recognition technology, and growing replacement cycles of old and manual appliances have encouraged the consumption of smart electronic devices.

The highly competitive and mature home appliance industry has long focused on product innovation. Exaggeration in new product development accelerates product innovation that in turn facilitates branding. Product innovations are effective in the changing the electronic industry environment and invent new brands according to current consumer demand patterns. Within the consumer electronics sector, companies that focus on emerging technology are driving significant growth for the white goods market.

Brand innovation trends in the smart home appliance industry are seen as one of the most competitive and mature corporate strategies that provide growth opportunities. Especially in the exceedingly competitive market, various electronic goods production units encounter many emerging counterfeit brands. As demand changes, new brands of different consumer electronics will come together to open up new opportunities throughout the whole consumer electronic industry, including the white goods market.

For instance,

In September, 2023 according to an article published by Evolute, the electronics manufacturing services (EMS) sector is rapidly evolving due to emerging technologies that enhance product design and production. Key innovations include the Internet of Things (IoT), artificial intelligence (AI), robotics, 5G, augmented and virtual reality, 3D printing, and sustainable manufacturing practices. These advancements enable EMS providers to produce more efficient, miniaturized components, improve quality control, and adopt eco-friendly practices. Additionally, technologies like blockchain and advanced materials are enhancing supply chain transparency and product functionality. As these trends continue, EMS companies are positioned to lead innovation in the electronics industry.

Furthermore, rising e-commerce activities and advanced technology development in manufacturing electronic goods in the smart home appliance industry have increased the demand for white goods. This, in turn, is expected to enhance the growth of the Middle East and Africa white goods market.

Restraints/Challenges

- Low Replacement Rate due to Life Span of Refrigerators

Refrigerators are built to last, typically functioning well for 10 to 15 years. This durability means consumers are less likely to replace them frequently. In the MEA region, many households prioritize the longevity of their appliances, focusing on repairs rather than replacements when issues arise. This trend slows market turnover, as a stable inventory of working refrigerators means fewer new sales.

Moreover, economic conditions in MEA countries significantly influence consumer behavior. In many African nations, a large portion of the population is price-sensitive, often due to lower disposable incomes and economic instability. As a result, consumers tend to repair their existing refrigerators instead of buying new ones, as repairs are usually more affordable than the cost of a new appliance. This preference is common in both urban centers and rural areas, where economic constraints dictate household spending.

Cultural attitudes toward consumption also impact replacement rates. In many MEA societies, there is a strong inclination to hold onto household items for extended periods, valuing reliability and durability over trends. This cultural preference results in a slower adoption of new refrigerator models, as consumers may view replacing appliances as unnecessary, especially if their current units still function adequately.

The low replacement rate creates challenges and opportunities for the white goods market. A stagnant replacement cycle can limit revenue growth for manufacturers, as fewer new units are sold. However, this situation also opens up opportunities for businesses focused on maintenance and repair services. Companies that offer extended warranties, service contracts, or parts for aging models may find a lucrative market among consumers reluctant to upgrade, ensuring steady revenue from service rather than new sales.

To counteract the effects of low replacement rates, manufacturers can adopt strategies centered on innovation and sustainability. Introducing energy-efficient models with advanced features can motivate consumers to upgrade. Modern refrigerators that promise lower electricity bills, better food preservation, and smart technology may appeal to consumers looking for long-term value. Effective marketing strategies that highlight these benefits can help shift consumer attitudes towards newer models, encouraging more frequent replacements.

For instance,

According to an article published by Truearth, refrigerators are essential household appliances, and maximizing their lifespan is crucial for making the most of your investment. Typically, refrigerators last between 10 to 20 years, with most averaging 14 to 17 years. To extend their durability, choose high-quality, energy-efficient models, perform regular maintenance, and maintain optimal temperature settings. Managing door seals, avoiding overloa, and inspecting components can also help. Be mindful of your refrigerator's condition; signs like frequent repairs or inefficient cooling may indicate it's time for a replacement. Proactive care ensures your fridge remains energy-efficient and long-lasting

The low replacement rate of refrigerators in the MEA region significantly impacts the growth of white goods market. This phenomenon poses challenges to sales growth, as fewer new units are purchased, limiting revenue potential for manufacturers. Additionally, the extended lifespan of these appliances, influenced by economic factors and cultural attitudes, contributes to a stagnant replacement cycle. Understanding these dynamics is essential for stakeholders in the market, as they must navigate a landscape shaped by unique consumer behaviors and preferences. The ongoing trends highlight the complexity of engaging consumers in a market where longevity often outweighs the desire for new purchases.

- Difficulties in Recycling Waste Materials

The Middle East and Africa white goods market faces significant challenges in recycling waste materials, particularly as the demand for household appliances continues to rise. This growth is accompanied by an increase in electronic waste (e-waste), with white goods such as refrigerators, washing machines, and ovens contributing substantially to the environmental burden.

One of the primary challenges is the lack of structured waste management systems across many MEA countries. Inadequate infrastructure means that e-waste is often improperly disposed of, leading to environmental pollution and health risks. Many nations lack dedicated recycling facilities for white goods, resulting in appliances ending up in landfills, where hazardous materials can leach into the soil and water systems. The informal waste collection sector often dominates, complicating the ability to ensure that materials are recycled effectively and safely.

Technical complexities also hinder recycling efforts. White goods are made from various materials, including metals, plastics, and refrigerants, each requiring specialized processes for extraction and recycling. Many local recycling facilities in the MEA region lack the technology and expertise needed to handle these materials properly. Consequently, valuable resources remain unrecovered, while harmful substances pose risks to both the environment and public health.

Economic factors further complicate the recycling landscape. Establishing and maintaining recycling facilities can be prohibitively expensive, deterring investment in proper waste management solutions. Additionally, the market for recycled materials is underdeveloped, providing minimal financial incentives for businesses to engage in recycling operations. This lack of economic motivation undermines efforts to create a circular economy where materials are reused and recycled effectively.

Regulatory frameworks regarding waste management and recycling are often weak or non-existent in many MEA countries. Without robust regulations and enforcement mechanisms, there is little accountability for manufacturers and consumers regarding the disposal of white goods. While some governments are starting to recognize the need for policies that promote responsible recycling and waste management, progress varies significantly across the region.

For instance,

In April, 2022 according to an article published by Colorado, recycling is often seen as a straightforward solution to plastic waste, but the industry faces several challenges that consumers can help alleviate. Many people lack knowledge about what can be recycled, leading to contamination of recyclable materials. Workers in the recycling sector face safety hazards, and some cities lack the resources for effective recycling services. Additionally, low market demand for recycled materials makes it less appealing for businesses to invest in recycling. However, recycling remains crucial for addressing plastic pollution, and individuals can contribute by educating themselves and supporting products made from recycled materials

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

White Goods Market Scope

The market is segmented on the basis of product. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Product

- Refrigerator

- Air Conditioners

- Washing Machines

- Cooker

- Ovens

- Dishwashing Machines

- Water Dispenser/RO System

- Fans

- Electric & Gas Heaters

- Freezers

- Personal Care

- Smart Medical Device

- Others

White Goods Market Regional Analysis

The market is analysed and market size insights and trends are provided by country and product as referenced above.

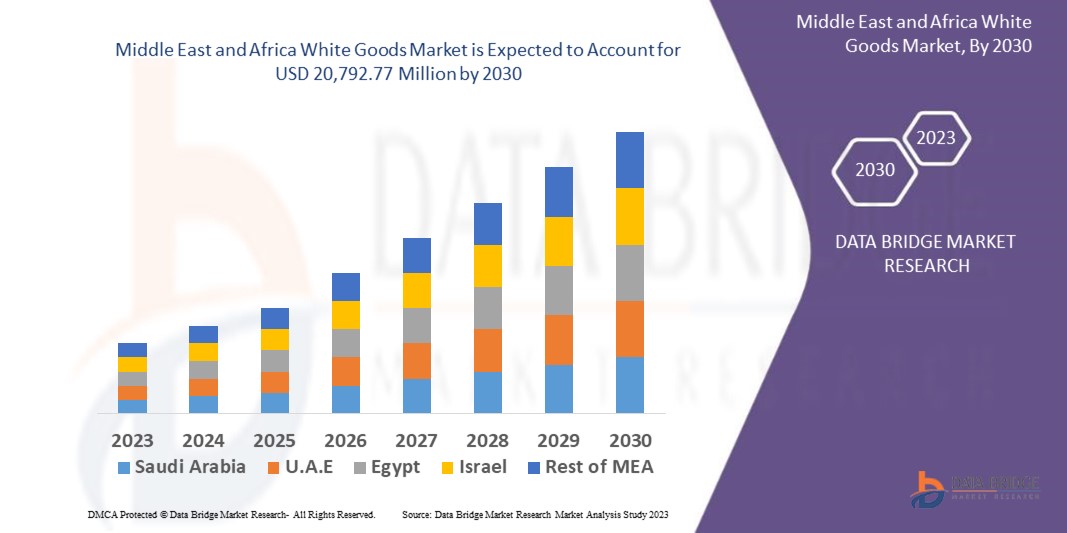

The countries covered in the market report are Saudi Arabia, U.A.E., Egypt, Qatar, Kuwait, Oman, Algeria, Morocco, Tunisia, Libya, and Rest of Middle East and Africa.

Saudi Arabia is expected to dominate the market due to growing demand for soaring temperature and humidity levels have increased the demand of air conditioners, and rising shares of organized retail stores.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points such as down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

White Goods Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

White Goods Market Leaders Operating in the Market Are:

- SAMSUNG (South Korea)

- LG Electronics (South Korea)

- Whirlpool Corporation (U.S.)

- Haier Group (China)

- Robert Bosch GmbH (Germany)

- AB Electrolux (Sweden)

- Nikai Group (U.A.E)

- Super General (U.A.E)

- Mitsubishi Electric Corporation (Japan)

- The Middleby Corporation (U.S.)

Latest Developments in White Goods Market

- In May 2024, LG Electronics unveiled its latest home entertainment lineup for the Middle East and Africa (MEA) region, showcasing cutting-edge technology and innovative features. The new range includes OLED TVs with enhanced picture quality, immersive audio experiences, and AI-driven capabilities that elevate the viewing experience. LG's commitment to sustainability is also evident, as the company incorporates eco-friendly practices in its production processes. This new lineup is designed to meet the evolving demands of consumers in the MEA region, positioning LG as a leader in the home entertainment sector

- In September 2024, LG Electronics launched its innovative WashTower in Qatar, revolutionizing laundry convenience with a compact and space-saving design. The WashTower combines a high-efficiency washer and dryer in a single vertical unit, allowing for seamless laundry management without compromising performance. Equipped with advanced technology such as AI DD™ for optimized washing and drying cycles, the WashTower enhances user experience while ensuring optimal fabric care. This launch underscores LG's commitment to meeting the diverse needs of consumers in the Middle East, offering innovative solutions that adapt to modern lifestyles

- In April 2024, Arçelik has completed the acquisition of Whirlpool's subsidiaries in Morocco and the UAE, along with its operations in the MENA region. This move is part of Arçelik's strategy to expand its presence and strengthen its market position in the home appliances sector. The acquisition is expected to enhance Arçelik’s portfolio and operational capabilities in these key markets

- In March 2023, LG Electronics Middle East and Africa (MEA) launched a unique range of innovative home appliance products designed to meet the diverse needs of consumers in the region. This new lineup includes advanced technologies such as AI-powered washing machines and energy-efficient refrigerators, aimed at enhancing convenience and sustainability in daily household tasks. LG emphasizes smart features that integrate seamlessly into modern lifestyles, offering users greater control and efficiency. This initiative reflects LG’s commitment to innovation and consumer satisfaction in the home appliance market, further solidifying its position as a leader in the region

- In June 2022, Samsung announced an extended warranty policy for its home appliances in the UAE, offering a three-year warranty for all customers. This initiative reflects Samsung's commitment to enhancing customer satisfaction and ensuring confidence in the durability and reliability of its products

- In September 2021, GE Appliances unveiled the GE Profile UltraFresh System dishwasher with Microban Antimicrobial Technology, which helps reduce the growth of bacteria inside and on the dishwasher

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.