North America Cancer Biomarkers Market

Market Size in USD Billion

USD

25.18 Billion

USD

46.09 Billion

2025

2033

USD

25.18 Billion

USD

46.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 25.18 Billion | |

| USD 46.09 Billion | |

| % | |

|

North America Cancer Biomarkers Market Size

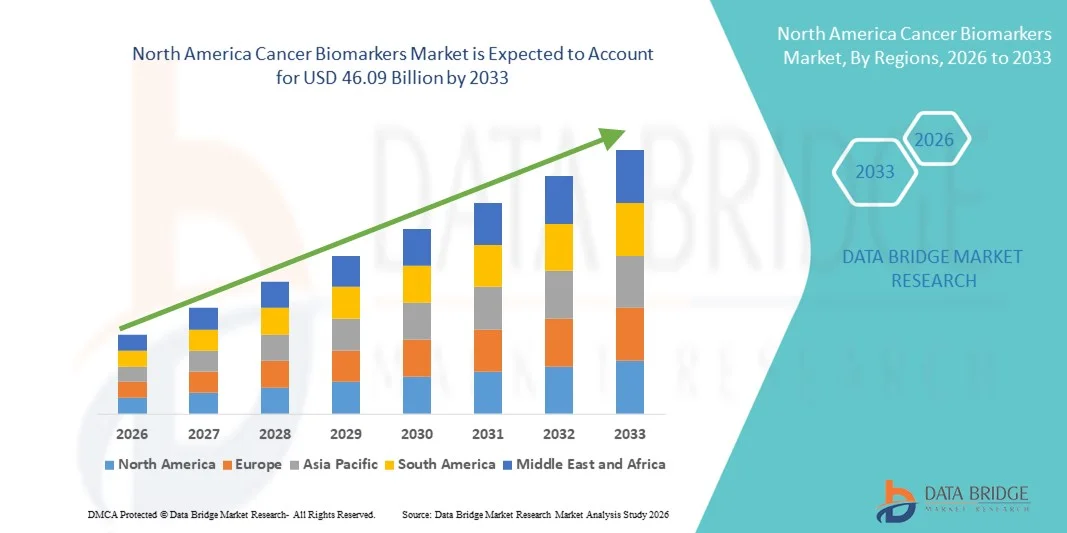

- The North America cancer biomarkers market size was valued at USD 25.18 billion in 2025 and is expected to reach USD 46.09 billion by 2033, at a CAGR of 7.85% during the forecast period

- The market growth is largely fueled by the increasing prevalence of various cancer types across the region, coupled with rising adoption of precision medicine and advanced molecular diagnostics technologies in clinical practice

- Furthermore, growing investments in oncology research, expanding applications of companion diagnostics, and the integration of genomics and proteomics into routine cancer screening and treatment decision-making are positioning cancer biomarkers as essential tools in modern oncology. These converging factors are accelerating the adoption of biomarker-based testing, thereby significantly boosting the industry's growth

North America Cancer Biomarkers Market Analysis

- Cancer biomarkers, which include genetic, proteomic, and molecular indicators used for cancer detection, prognosis, and therapy selection, are increasingly vital components of modern oncology care across hospitals, diagnostic laboratories, and research institutions due to their critical role in enabling early diagnosis, risk stratification, and personalized treatment planning

- The escalating demand for cancer biomarkers is primarily fueled by the rising incidence of cancer across North America, expanding adoption of precision medicine, and continuous advancements in genomic sequencing, liquid biopsy technologies, and companion diagnostics

- The United States dominated the cancer biomarkers market with the largest revenue share of 82.4% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, and significant investments in oncology research, with the country witnessing substantial growth in biomarker-based testing driven by pharmaceutical collaborations, increasing clinical trial activity, and regulatory support for targeted therapies

- Canada is expected to be the fastest growing country in the cancer biomarkers market during the forecast period, accounting for a revenue share of 17.6% in 2025, supported by increasing government funding for oncology research, expanding access to advanced molecular diagnostics, and rising implementation of nationwide precision medicine initiatives

- Genetic biomarkers segment dominated the cancer biomarkers market with a market share of 48.9% in 2025, driven by their widespread application in precision oncology, increasing use in companion diagnostics, and growing reliance on next-generation sequencing technologies for tailored cancer treatment strategies

Report Scope and North America Cancer Biomarkers Market Segmentation

|

Attributes |

North America Cancer Biomarkers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Cancer Biomarkers Market Trends

Advancement of Precision Oncology Through Genomic and AI Integration

- A significant and accelerating trend in the North America cancer biomarkers market is the deepening integration of next-generation sequencing (NGS), artificial intelligence (AI), and advanced bioinformatics platforms into oncology diagnostics. This convergence of technologies is significantly enhancing diagnostic accuracy and personalized treatment planning

- For instance, comprehensive genomic profiling panels are increasingly utilized across major cancer centers in the U.S. and Canada to identify actionable mutations, enabling clinicians to match patients with targeted therapies and immunotherapies more effectively

- AI integration in cancer biomarker platforms enables rapid interpretation of complex genomic datasets, identification of novel mutation patterns, and improved prediction of therapy response. For instance, certain molecular diagnostic laboratories utilize AI-driven algorithms to enhance variant classification accuracy and generate clinically actionable reports with reduced turnaround time. Furthermore, liquid biopsy technologies offer clinicians the ability to perform minimally invasive tumor profiling and monitor treatment response in real time

- The seamless integration of biomarker testing with electronic health records and clinical decision-support systems facilitates coordinated oncology care across hospitals and specialty clinics. Through centralized data platforms, physicians can align diagnostic findings with treatment protocols, clinical trial eligibility, and longitudinal patient monitoring, creating a more unified and data-driven oncology ecosystem

- This trend toward more precise, data-enabled, and personalized cancer management is fundamentally reshaping oncology practice standards across North America. Consequently, leading diagnostic and biotechnology companies are developing multi-omic biomarker solutions with expanded panels, higher sensitivity, and improved clinical utility

- The demand for advanced biomarker assays that offer comprehensive genomic insights and real-time disease monitoring is growing rapidly across academic institutions, community hospitals, and private diagnostic laboratories, as healthcare providers increasingly prioritize precision medicine approaches

- Collaborative partnerships between pharmaceutical companies and diagnostic developers to co-develop companion diagnostics alongside targeted therapies are further strengthening the role of biomarkers in accelerating drug approvals and optimizing patient stratification

North America Cancer Biomarkers Market Dynamics

Driver

Rising Cancer Incidence and Expanding Adoption of Personalized Medicine

- The increasing prevalence of cancer across North America, coupled with the accelerating adoption of personalized medicine frameworks, is a significant driver for the heightened demand for cancer biomarker testing

- For instance, leading oncology networks have expanded routine biomarker screening programs for lung, breast, and colorectal cancers to guide targeted therapy selection and improve survival outcomes. Such strategic expansions by healthcare providers are expected to drive the cancer biomarkers market growth during the forecast period

- As clinicians aim to optimize therapeutic efficacy and minimize adverse effects, biomarker-based diagnostics provide critical insights into tumor biology, genetic mutations, and predictive response to specific treatments, offering a substantial advancement over conventional diagnostic approaches

- Furthermore, growing pharmaceutical research and development activities in targeted therapies and immuno-oncology drugs are making companion diagnostics an integral component of drug development pipelines, ensuring that treatments are administered to appropriately selected patient populations

- The increasing availability of reimbursement coverage for molecular diagnostics, expansion of clinical trial activity, and collaborative initiatives between biotechnology firms and academic research centers are key factors propelling the adoption of cancer biomarker technologies across the region. The ongoing emphasis on early detection and preventive oncology further contributes to sustained market expansion

- Heightened awareness campaigns and national cancer control programs promoting early screening and molecular testing are also encouraging broader patient participation in biomarker-based diagnostics

- Advancements in automation and high-throughput laboratory technologies are reducing turnaround times and improving scalability of biomarker testing services, further accelerating clinical adoption

Restraint/Challenge

High Testing Costs and Regulatory & Reimbursement Complexities

- Concerns surrounding the high cost of advanced molecular diagnostic tests, including comprehensive genomic profiling and multi-gene panels, pose a significant challenge to broader market penetration. As biomarker testing often requires specialized laboratory infrastructure and skilled personnel, overall expenses can limit accessibility in certain healthcare settings

- For instance, variations in reimbursement policies across private insurers and public healthcare programs have created inconsistencies in patient access to advanced biomarker assays, leading some providers to hesitate in adopting comprehensive testing protocols

- Addressing cost and reimbursement challenges through value-based pricing models, standardized clinical guidelines, and expanded insurance coverage is crucial for improving equitable access. In addition, the complex and evolving regulatory landscape governing companion diagnostics and laboratory-developed tests can create compliance burdens for diagnostic manufacturers and laboratories

- While regulatory frameworks are designed to ensure test accuracy and patient safety, extended approval timelines and documentation requirements may delay market entry for innovative biomarker technologies, particularly for smaller biotechnology firms

- Data privacy concerns associated with large-scale genomic data collection and storage also present challenges, as healthcare providers must ensure compliance with stringent patient data protection regulations

- Limited access to advanced molecular diagnostic infrastructure in certain rural or underserved areas may restrict equitable adoption of biomarker testing services

- Overcoming these challenges through streamlined regulatory pathways, harmonized reimbursement structures, continued technological innovation to reduce testing costs, enhanced cybersecurity safeguards, and strengthened public–private collaboration will be vital for sustaining long-term market growth across North America

North America Cancer Biomarkers Market Scope

The market is segmented on the basis of type, product, cancer, technology, application, and end user.

- By Type

On the basis of type, the North America cancer biomarkers market is segmented into genetic biomarkers, protein biomarkers, and other cancer biomarkers. The genetic biomarkers segment dominated the market with the largest revenue share of 48.9% in 2025, driven by the widespread adoption of next-generation sequencing (NGS) and PCR-based molecular diagnostics across the United States and Canada. Genetic biomarkers play a critical role in identifying actionable mutations such as EGFR, KRAS, and BRCA, which guide targeted therapy selection in precision oncology. The growing use of companion diagnostics alongside immunotherapies and targeted drugs further strengthens this segment’s leadership. Increasing clinical trial activity focused on genomics-based stratification also supports revenue expansion. In addition, favorable reimbursement coverage for molecular testing and strong pharmaceutical–diagnostic collaborations contribute significantly to the segment’s dominance.

The protein biomarkers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption of immunoassay-based diagnostics and expanding applications in early cancer detection and monitoring. Protein-based markers such as PSA and HER-2 are widely utilized in routine screening and therapy response assessment. Technological advancements in multiplex immunoassays and high-sensitivity detection platforms are improving accuracy and scalability. Increasing demand for minimally invasive blood-based testing further accelerates segment growth. Growing research into novel circulating protein biomarkers for early-stage cancer detection also positions this segment for robust expansion.

- By Product

On the basis of product, the market is segmented into PSA, HER-2, EGFR, KRAS, and others. The PSA segment dominated the market in 2025 due to its long-standing clinical adoption in prostate cancer screening and monitoring across North America. PSA testing is widely integrated into routine preventive healthcare practices, especially among aging male populations. Strong physician familiarity, established reimbursement pathways, and high testing volumes contribute to sustained revenue generation. The large prevalence of prostate cancer in the region further supports segment leadership. Continuous improvements in assay sensitivity and specificity also enhance its clinical relevance.

The EGFR segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing incidence of lung cancer and expanding use of targeted EGFR inhibitors. EGFR mutation testing has become a standard component of non-small cell lung cancer (NSCLC) management. Advancements in liquid biopsy technologies are enabling non-invasive EGFR mutation detection, accelerating testing adoption. Pharmaceutical pipeline expansion in EGFR-targeted therapies further strengthens demand. Growing awareness of personalized treatment approaches significantly contributes to rapid segment growth.

- By Cancer

On the basis of cancer type, the market is segmented into breast cancer, lung cancer, prostate cancer, colorectal cancer, blood cancer, melanoma, ovarian cancer, liver cancer, stomach cancer, and others. The lung cancer segment dominated the market in 2025 due to the high disease burden and strong reliance on molecular biomarker testing for therapy selection. Biomarkers such as EGFR, ALK, and KRAS are routinely tested to guide targeted treatments. The shift toward precision oncology in lung cancer management drives high testing volumes. Significant R&D investment and clinical trial activity in immuno-oncology further reinforce segment leadership. Early detection initiatives and screening programs also support growth.

The breast cancer segment is projected to experience the fastest growth rate from 2026 to 2033, fueled by expanding use of HER-2, BRCA1/2, and multigene panel testing. Increasing awareness regarding hereditary cancer risk assessment is driving higher genetic screening rates. Advances in personalized hormone and targeted therapies require accurate biomarker identification. Rising survivorship rates necessitate ongoing monitoring through biomarker testing. Technological progress in multi-omic profiling further accelerates adoption in breast oncology.

- By Technology

On the basis of technology, the market is segmented into imaging technologies, omic technologies, and cytogenetic-based tests and immunoassays. The omic technologies segment dominated the market in 2025, driven by widespread adoption of genomics, proteomics, and transcriptomics platforms. Next-generation sequencing is increasingly utilized for comprehensive tumor profiling. The ability to analyze multiple mutations simultaneously enhances diagnostic efficiency. Strong integration of AI-powered bioinformatics tools supports accurate data interpretation. Growing investments in precision medicine initiatives further reinforce segment dominance.

The cytogenetic-based tests and immunoassays segment is expected to witness the fastest CAGR from 2026 to 2033, driven by improvements in fluorescence in situ hybridization (FISH) and advanced immunohistochemistry (IHC) techniques. These methods remain essential for validating genomic findings in clinical settings. Enhanced automation and standardization are increasing laboratory throughput. Rising adoption in community hospitals and diagnostic laboratories accelerates segment growth. Expanding applications in companion diagnostics further support rapid expansion.

- By Application

On the basis of application, the market is segmented into drug discovery and development, personalized medicine, diagnostics, and others. The diagnostics segment dominated the market in 2025, as biomarker testing is primarily utilized for cancer detection, prognosis, and treatment monitoring. Routine integration of biomarker assays into oncology workflows drives high test volumes. Expanding early cancer screening programs across North America further contribute to segment leadership. Increasing physician reliance on biomarker-driven decisions enhances demand. Established reimbursement frameworks also support sustained revenue generation.

The personalized medicine segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the growing emphasis on targeted and immuno-oncology therapies. Precision treatment strategies require comprehensive biomarker profiling prior to therapy initiation. Pharmaceutical companies are increasingly co-developing companion diagnostics alongside novel drugs. Advancements in multi-gene panel testing accelerate personalized treatment adoption. Rising patient preference for tailored therapy options further supports segment growth.

- By End User

On the basis of end user, the market is segmented into hospitals, academic and cancer research institutes, ambulatory surgical centers, and diagnostic laboratories. The hospitals segment dominated the market in 2025 due to high patient inflow, integrated oncology departments, and access to advanced molecular diagnostic infrastructure. Hospitals serve as primary centers for cancer diagnosis and treatment planning. Strong reimbursement support and multidisciplinary care teams further enhance adoption. Expansion of in-house molecular pathology laboratories strengthens segment revenue.

The diagnostic laboratories segment is projected to witness the fastest growth from 2026 to 2033, driven by increasing outsourcing of specialized biomarker testing services. Independent and reference laboratories offer high-throughput genomic analysis with advanced automation systems. Rising partnerships between hospitals and private labs accelerate test volumes. Cost-efficiency and rapid turnaround times make these facilities attractive for precision oncology testing. Growing demand for comprehensive genomic profiling further supports robust segment expansion.

North America Cancer Biomarkers Market Regional Analysis

- The United States dominated the cancer biomarkers market with the largest revenue share of 82.4% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, and significant investments in oncology research

- Healthcare providers in the region highly value the clinical accuracy, predictive capabilities, and treatment-guiding benefits offered by biomarker testing, particularly for targeted therapies and immuno-oncology applications across major cancer types

- This widespread adoption is further supported by advanced healthcare infrastructure, favorable reimbursement frameworks, substantial oncology research funding, and a strong presence of leading biotechnology and diagnostic companies, establishing cancer biomarkers as an essential component of modern oncology care across hospitals and research institutions

The U.S. Cancer Biomarkers Market Insight

The U.S. cancer biomarkers market captured the largest revenue share within North America in 2025, fueled by the high cancer incidence rate and strong adoption of precision oncology practices. Healthcare providers are increasingly prioritizing comprehensive genomic profiling and companion diagnostics to guide targeted therapy selection. The growing integration of next-generation sequencing, liquid biopsy technologies, and AI-driven bioinformatics platforms further propels market expansion. Moreover, robust federal research funding, active clinical trial pipelines, and the presence of leading biotechnology and pharmaceutical companies are significantly contributing to the market's continued growth.

Canada Cancer Biomarkers Market Insight

The Canada cancer biomarkers market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing government investments in cancer research and nationwide precision medicine initiatives. Rising awareness regarding early cancer detection and hereditary cancer screening is fostering broader biomarker adoption. Canadian healthcare systems are emphasizing evidence-based oncology practices supported by molecular diagnostics. The expansion of advanced laboratory infrastructure and collaborations between academic institutions and biotechnology firms are further accelerating market development across the country.

Mexico Cancer Biomarkers Market Insight

The Mexico cancer biomarkers market is expected to grow at a steady CAGR during the forecast period, driven by improving healthcare infrastructure and increasing focus on early cancer diagnosis. Rising cancer prevalence and expanding access to molecular diagnostic services are supporting biomarker adoption in major urban healthcare centers. Government-led health initiatives aimed at strengthening oncology care pathways are further contributing to market expansion. In addition, growing partnerships with international diagnostic companies and gradual integration of advanced genomic testing technologies are enhancing market penetration across both public and private healthcare institution

North America Cancer Biomarkers Market Share

The North America Cancer Biomarkers industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Myriad Genetics, Inc. (U.S.)

- Guardant Health, Inc. (U.S.)

- Foundation Medicine, Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Hologic, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- BD (U.S.)

- NeoGenomics, Inc. (U.S.)

- Adaptive Biotechnologies Corporation (U.S.)

- PerkinElmer, Inc. (U.S.)

- Cepheid (U.S.)

- Charles River Laboratories International, Inc. (U.S.)

- Quanterix Corporation (U.S.)

- Exact Sciences Corporation (U.S.)

- C-Biomex Ltd. (U.S.)

What are the Recent Developments in North America Cancer Biomarkers Market?

- In August 2025, Cizzle Bio a San Antonio biotech firm developed and validated DEX-G2, a new blood test that uses cell-free microRNAs and exosomal markers for early detection of gastric cancer, marking a significant milestone toward non-invasive cancer biomarker testing commercialization

- In August 2025, the U.S. Food and Drug Administration (FDA) cleared MI Cancer Seek, a comprehensive molecular test designed to enhance tumor profiling for precision oncology by identifying clinically relevant biomarkers (including companion diagnostic levels) from formalin-fixed, paraffin-embedded (FFPE) tissue, expanding options for biomarker-driven treatment decisions

- In June 2025, the U.S. FDA approved Nuvation Bio’s Ibtrozi, a ROS1 inhibitor targeting a genetic cancer driver mutation in ROS1-positive non-small cell lung cancer, underscoring the role of mutation-specific biomarkers in targeted therapy selection

- In April 2025, Thermo Fisher Scientific received U.S. FDA approval for its Oncomine Dx Express Test, a companion diagnostic for NSCLC patients with actionable EGFR exon 20 insertion mutations and broader solid tumor profiling across 46 genes—advancing genomic biomarker-guided therapy selection

- In April 2024, the US FDA approved Lumisight (pegulicianine) and the Lumicell Direct Visualization System as the first drug-device combination for intraoperative fluorescence imaging to detect residual breast cancer tissue during lumpectomy surgery, marking a significant advance in imaging biomarker-guided cancer detection

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.