North America Down Syndrome Market

Market Size in USD Billion

USD

1.16 Billion

USD

3.34 Billion

2024

2032

USD

1.16 Billion

USD

3.34 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.16 Billion | |

| USD 3.34 Billion | |

| % | |

|

North America Down Syndrome Market Size

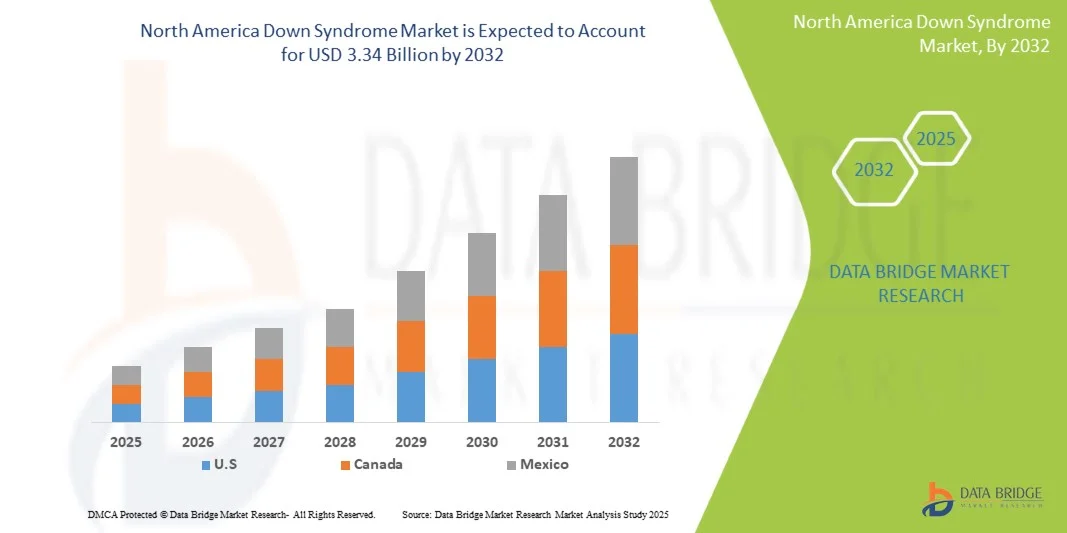

- The North America Down Syndrome market size was valued at USD 1.16 billion in 2024 and is expected to reach USD 3.34 billion by 2032, at a CAGR of 14.1% during the forecast period

- The market growth is primarily driven by the rising prevalence of Down syndrome, increasing awareness regarding early diagnosis, and expanding access to advanced genetic testing and prenatal screening technologies across the region

- Moreover, supportive government initiatives, growing investments in therapeutic research, and improved healthcare infrastructure are enhancing the management and treatment landscape. These combined factors are fostering significant advancements and strengthening the overall growth of the North America Down Syndrome market

North America Down Syndrome Market Analysis

- Down syndrome, a genetic disorder caused by the presence of an extra chromosome 21, is increasingly recognized as a focus area for early diagnosis, therapeutic interventions, and supportive care due to its impact on cognitive and physical development in affected individuals

- The growing market is primarily driven by rising awareness among healthcare providers and caregivers, expanding availability of advanced prenatal screening and diagnostic technologies, and increasing investments in research and development for therapies and management solutions

- The United States dominated the North America Down Syndrome market with the largest revenue share of 81.6% in 2024, characterized by advanced healthcare infrastructure, well-established genetic testing facilities, and strong government and non-government support programs

- Canada is expected to be the fastest-growing country in the North America Down Syndrome market during the forecast period due to increasing healthcare awareness, rising prenatal screening adoption, and supportive reimbursement policies

- Therapy segment dominated the North America Down Syndrome market with a market share of 45.8% in 2024, driven by ongoing clinical research, growing availability of targeted treatments, and rising adoption of early intervention programs to improve quality of life

Report Scope and North America Down Syndrome Market Segmentation

|

Attributes |

North America Down Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Down Syndrome Market Trends

“Advancements in Early Diagnosis and Genetic Screening”

- A significant and accelerating trend in the North America Down Syndrome market is the increasing adoption of advanced prenatal and postnatal diagnostic technologies, including non-invasive prenatal testing (NIPT) and high-resolution chromosomal microarray analysis, enabling earlier and more accurate detection

- For instance, Harmony Prenatal Test has become widely used in the U.S., allowing expecting parents to assess the such aslihood of Down syndrome with high accuracy and minimal risk to the fetus

- Integration of these advanced diagnostic tools with digital health platforms enables better tracking of patient history, facilitates informed decision-making, and provides healthcare professionals with data-driven insights for personalized care

- The availability of AI-assisted diagnostic platforms that analyze genetic and clinical data is further enhancing the precision of early detection, reducing false positives and improving counseling for families

- This trend toward more accessible, accurate, and technologically advanced screening methods is reshaping expectations for early intervention, with companies such as Natera focusing on expanding AI-based solutions for broader prenatal care

- The demand for advanced diagnostic tools and integrated genetic screening solutions is growing rapidly across both clinical and hospital settings, as caregivers and healthcare providers prioritize early identification and comprehensive management strategies

North America Down Syndrome Market Dynamics

Driver

“Rising Awareness and Supportive Healthcare Initiatives”

- The increasing awareness about Down syndrome and government or NGO-led initiatives promoting early diagnosis, intervention, and therapy are significant drivers for market growth in North America

- For instance, in March 2024, the National Down Syndrome Society (NDSS) launched a campaign to expand access to early intervention programs and genetic counseling services across multiple U.S. states, supporting better patient outcomes

- Growing investments in research for novel therapies, behavioral interventions, and assistive technologies are also driving demand, as families and healthcare providers seek comprehensive solutions for improving quality of life

- In addition, expanding access to specialized care centers and support programs ensures patients receive timely therapies, thereby increasing the adoption of clinical and home-based management strategies

- Collaboration between academic institutions, biotech firms, and non-profits is accelerating the development of innovative therapeutic and assistive technologies, enhancing treatment options

- Public awareness campaigns and community programs aimed at destigmatizing Down syndrome are driving social acceptance and encouraging families to seek timely medical and therapeutic support

- Increased coverage of diagnostic tests and therapies by insurance providers, coupled with the rise in patient advocacy and educational initiatives, is further encouraging early intervention and ongoing treatment adoption in the region

Restraint/Challenge

“High Treatment Costs and Limited Access in Certain Areas”

- The relatively high cost of advanced diagnostic tests, therapeutic interventions, and ongoing supportive care remains a key challenge limiting broader adoption, particularly for families without comprehensive insurance coverage

- For instance, the out-of-pocket expenses for genetic testing and early intervention therapies in some U.S. states can be prohibitive, preventing equitable access to care

- Variability in availability of specialized Down syndrome clinics and trained healthcare professionals across urban and rural areas creates accessibility disparities, restricting market growth in underserved regions

- Furthermore, limited awareness among some caregivers about advanced therapies or early intervention programs can delay adoption, affecting overall patient outcomes and market potential

- Addressing these challenges through policy support, subsidized care programs, and broader educational initiatives is crucial to ensure equitable access to diagnostic and therapeutic solutions for all affected individuals

- Regulatory hurdles for approval of novel therapeutics and assistive devices can slow market entry and adoption, impacting the speed of growth for innovative solutions

- Cultural and socioeconomic factors influencing healthcare-seeking behavior in certain communities may limit acceptance of advanced diagnostic and therapeutic interventions, posing additional challenges for market expansion

North America Down Syndrome Market Scope

The market is segmented on the basis of disease type, treatment, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the North America Down Syndrome market is segmented into Trisomy 21, Translocation Down Syndrome, and Mosaic Down Syndrome. The Trisomy 21 segment dominated the market with the largest revenue share in 2024, driven by its high prevalence among diagnosed cases. Early detection programs and routine prenatal screening focus heavily on Trisomy 21, leading to a higher adoption of diagnostic and therapeutic interventions. Healthcare providers and caregivers prioritize early intervention programs for Trisomy 21 due to its significant impact on cognitive and physical development. The availability of specialized treatment protocols, genetic counseling, and supportive therapies further strengthens this segment’s market share. The strong awareness and robust clinical research pipeline targeting Trisomy 21 contribute to sustained market dominance.

The Mosaic Down Syndrome segment is anticipated to witness the fastest growth rate during the forecast period, driven by increasing recognition of its milder phenotypic presentation and expanding demand for targeted diagnostic tools. Improved genetic screening methods, including advanced NIPT and chromosomal microarray analysis, enable early detection of Mosaic cases that were previously underdiagnosed. The growing focus on personalized therapy and intervention programs for Mosaic Down Syndrome supports its rapid uptake. Research initiatives exploring cognitive and behavioral therapies tailored to Mosaic presentations also fuel growth. Increased awareness among clinicians and caregivers regarding Mosaic Down Syndrome enhances early diagnosis and intervention rates, boosting market expansion.

- By Treatment

On the On the basis of treatment, the market is segmented into Diagnosis and Therapy. The Therapy segment dominated the North America Down Syndrome market with a market share of 45.8% in 2024, propelled by rising adoption of behavioral, physical, and cognitive interventions for Down Syndrome patients. Therapy adoption is increasing due to growing caregiver demand for personalized treatment plans to improve quality of life. Companies and clinics are introducing innovative therapies, including speech therapy apps and AI-assisted developmental monitoring tools, boosting segment growth. Expansion of homecare and outpatient therapy services makes these interventions more accessible. The development of targeted pharmacological therapies and assistive technologies also contributes to robust growth. Increasing advocacy for early intervention programs enhances adoption rates across residential and clinical settings.

The Diagnosis segment is expected to witness the fastest growth, supported by widespread adoption of prenatal screening, non-invasive prenatal testing, and postnatal genetic analysis. Healthcare providers prioritize early and accurate diagnosis as it facilitates informed decision-making and timely intervention. Government and insurance support for diagnostic testing in the U.S. further drives adoption. Advanced digital platforms for test reporting and patient tracking enhance the convenience and efficiency of diagnostic services. Collaborations between diagnostic companies and hospitals strengthen access and market penetration. Increasing awareness campaigns emphasizing early detection for better developmental outcomes fuel rapid growth.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, homecare settings, therapy centers, and others. The Hospitals segment dominated in 2024, driven by the central role of hospitals in prenatal screening, postnatal diagnosis, and coordinated care for Down Syndrome patients. Hospitals offer access to specialized genetic testing labs, multidisciplinary therapy programs, and trained professionals, making them the preferred choice for comprehensive care. Adoption of digital health platforms in hospitals improves patient management and follow-up care. High patient footfall and partnerships with diagnostic companies strengthen market penetration. Government support programs often channel resources through hospitals, further enhancing their market share. The integration of research programs and clinical trials within hospitals also reinforces their dominance.

The Homecare Settings segment is expected to witness the fastest growth during the forecast period,, fueled by increasing demand for personalized care and therapy in the patient’s residence. Telemedicine platforms, remote monitoring, and at-home therapy programs enhance convenience and accessibility. Caregivers are increasingly adopting home-based interventions to reduce hospital visits and improve treatment adherence. Expansion of insurance coverage for homecare services encourages adoption. Technology-enabled therapy tools, including mobile apps and AI-assisted monitoring, support rapid segment growth. Rising awareness about the benefits of early intervention at home further accelerates market uptake.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. The Direct Tender segment dominated in 2024, driven by bulk procurement by hospitals, government programs, and specialized therapy centers. Direct Tender contracts ensure consistent supply of diagnostic kits, therapy devices, and genetic testing tools. Bulk procurement provides cost advantages and strengthens supplier relationships with large healthcare institutions. Government and NGO initiatives promoting Down Syndrome care often use direct tender mechanisms for efficiency. The reliability and timely delivery associated with direct tenders reinforce their dominance. Collaboration between suppliers and healthcare providers ensures seamless adoption of advanced diagnostic and therapeutic solutions.

The Retail Sales segment is expected to witness the fastest growth during the forecast period, driven by rising availability of at-home diagnostic kits, therapy devices, and supportive tools through online and offline retail channels. Increased caregiver preference for convenient, self-administered products fuels adoption. E-commerce platforms and specialty medical stores facilitate broader reach and accessibility. Rising awareness campaigns and product demonstrations enhance trust in retail offerings. The affordability of certain home-based diagnostic and therapy products supports rapid market growth. Technology-enabled products with user-friendly interfaces further accelerate adoption in residential settings.

North America Down Syndrome Market Regional Analysis

- The U.S. dominated the North America Down Syndrome market with the largest revenue share of 81.6% in 2024, characterized by advanced healthcare infrastructure, well-established genetic testing facilities, and strong government and non-government support programs

- Families and healthcare providers in the region highly value timely detection, comprehensive therapy options, and integrated care pathways that improve cognitive and physical development outcomes for individuals with Down syndrome

- This widespread adoption is further supported by advanced healthcare infrastructure, strong government and non-government support programs, and the presence of leading diagnostic and therapeutic solution providers, establishing the U.S. as the key contributor to market growth in the region

Canada Down Syndrome Market Insight

The Canada Down Syndrome market is expected to grow at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of early intervention programs and the adoption of advanced diagnostic and therapeutic services. Expanding healthcare infrastructure, coupled with supportive government policies and insurance coverage for prenatal screening and therapy, is fostering market growth. Canadian consumers and caregivers are also increasingly recognizing the benefits of integrated care, early intervention, and ongoing support services. The market is experiencing significant growth across hospitals, clinics, homecare, and therapy centers, with a focus on improving patient quality of life.

Mexico Down Syndrome Market Insight

The Mexico Down Syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness about early diagnosis, genetic testing, and therapy services. In addition, increasing government initiatives and NGO-led programs to improve accessibility and affordability of Down Syndrome care are encouraging adoption. The country’s expanding healthcare infrastructure, coupled with efforts to enhance specialized therapy centers and trained professionals, is expected to continue to stimulate market growth. Growing public education campaigns on Down Syndrome management and intervention programs are further supporting market expansion.

North America Down Syndrome Market Share

The North America Down Syndrome industry is primarily led by well-established companies, including:

- AC Immune SA (Switzerland)

- Alzheon. (U.S.)

- Annovis Bio, Inc. (U.S.)

- Aphios Corporation (U.S.)

- Aelis Farma (France)

- BioMarin (U.S.)

- Demeditec Diagnostics GmbH (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Illumina, Inc. (U.S.)

- Karyopharm. (U.S.)

- ManRos Therapeutics (Switzerland)

- Mayo Clinic Health System (U.S.)

- Myriad Genetics, Inc. (U.S.)

- NeuroNascent, Inc. (U.S.)

- Natera, Inc. (U.S.)

- Next Biosciences (U.S.)

- PerkinElmer (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- The University of Chicago Medical Center. (U.S.)

What are the Recent Developments in North America Down Syndrome Market?

- In October 2025, Penn Station East Coast Subs introduced a fundraising campaign called "Deals for Down Syndrome" across all its locations. The initiative donates 100% of proceeds from sales of fundraising coupon booklets to local Down Syndrome Associations, supporting programs such as summer camps, educational resources, and enrichment services for individuals with Down syndrome and their families

- In September 2025, Goji Labs collaborated with the Down Syndrome Diagnosis Network (DSDN) to introduce a bilingual, accessible digital platform aimed at supporting parents of children with Down syndrome. The platform provides a safe online community offering resources, connections, and support, already serving over 20,000 families

- In June 2025, the Global Down Syndrome Foundation (GLOBAL) and the Down Syndrome Diagnosis Network (DSDN) entered a multi-year collaboration to educate mothers of children with Down syndrome, particularly in the early years, about essential medical care resources and research opportunities

- In October 2024, the National Institutes of Health (NIH) established a USD 20 million program to study Down syndrome, aiming to deepen understanding of the condition and accelerate knowledge of health issues more commonly associated with it

- In April 2023, Mattel launched its first Barbie doll with Down syndrome as part of the Fall Fashionistas collection. This initiative aims to increase representation and inclusivity in the toy aisle, allowing more children to find a Barbie doll that reflects their identity

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.