North America Ehealth Market

Market Size in USD Billion

CAGR :

%

USD

21.90 Billion

USD

131.37 Billion

2025

2033

USD

21.90 Billion

USD

131.37 Billion

2025

2033

| 2026 –2033 | |

| USD 21.90 Billion | |

| USD 131.37 Billion | |

| % | |

|

North America eHealth Market Size

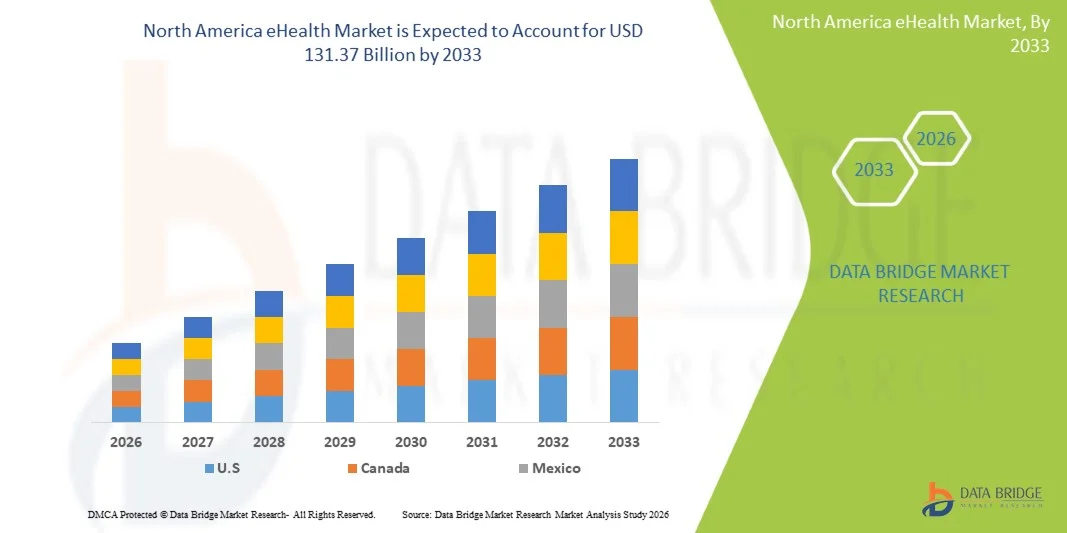

- The North America eHealth market size was valued at USD 21.90 billion in 2025 and is expected to reach USD 131.37 billion by 2033, at a CAGR of 25.1% during the forecast period

- The market growth is largely fueled by the growing adoption and technological advancements in digital health platforms, telemedicine, electronic health records (EHR), and mobile health solutions, leading to increased digitalization across healthcare systems in both clinical and non-clinical settings

- Furthermore, rising demand for efficient, accessible, and patient-centric healthcare services, along with the need to reduce healthcare costs and improve care coordination, is establishing eHealth solutions as a key enabler of modern healthcare delivery. These converging factors are accelerating the uptake of eHealth technologies, thereby significantly boosting the industry's growth

North America eHealth Market Analysis

- eHealth, encompassing digital health solutions such as telemedicine, electronic health records (EHR), mHealth, and healthcare analytics platforms, is increasingly vital to modern healthcare systems in North America due to its ability to enhance patient care delivery, improve clinical decision-making, and enable seamless data exchange across providers and healthcare ecosystems

- The escalating demand for eHealth is primarily fueled by the rising prevalence of chronic diseases, growing adoption of telehealth and remote patient monitoring, increasing integration of AI, cloud computing, and big data in healthcare, and the ongoing shift toward value-based care models aimed at improving outcomes while reducing costs

- The United States dominated the North America eHealth market with the largest revenue share of 85.7% in 2025, characterized by advanced healthcare infrastructure, strong digital maturity, high healthcare expenditure, and widespread implementation of EHR systems, with the country leading in telemedicine adoption, interoperability initiatives, and digital transformation across hospitals, clinics, and outpatient care centers driven by both established healthcare providers and technology innovators

- Canada is expected to be the fastest growing country in the North America eHealth market during the forecast period due to increasing government investments in digital health infrastructure, expanding telehealth services across remote areas, rising adoption of connected healthcare systems, and growing emphasis on improving healthcare accessibility and efficiency

- The cloud segment dominated the eHealth market with a significant market share of 60.9% in 2025, driven by its scalability, flexibility, cost efficiency, and ability to support secure data storage, real-time access to patient records, and interoperability across multiple healthcare stakeholders, making it a preferred deployment model for modern healthcare organizations

Report Scope and North America eHealth Market Segmentation

|

Attributes |

North America eHealth Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America eHealth Market Trends

“Integration of AI, Cloud, and Interoperable Digital Health Platforms”

- A significant and accelerating trend in the North America eHealth market is the deepening integration of artificial intelligence (AI), cloud computing, and interoperable digital health platforms across healthcare systems, enabling improved clinical decision-making, predictive analytics, and real-time access to patient data

- For instance, platforms such as electronic health record (EHR) systems and telehealth solutions increasingly incorporate AI-driven features to support clinical workflows, automate administrative tasks, and enhance diagnostic accuracy, while cloud-based infrastructure enables secure, scalable, and centralized data management across providers

- AI integration in eHealth enables capabilities such as predictive risk stratification, personalized treatment recommendations, and intelligent alerts for patient monitoring systems. In addition, machine learning algorithms are being used to analyze large volumes of healthcare data to identify patterns, improve population health management, and support early intervention strategies

- The seamless integration of eHealth solutions with digital ecosystems facilitates interoperability between hospitals, clinics, pharmacies, and laboratories. Through unified platforms, healthcare providers can share patient records, coordinate care, and improve communication, creating a more connected and efficient healthcare delivery system

- This trend toward more intelligent, data-driven, and interconnected healthcare systems is fundamentally reshaping expectations for digital health services. Consequently, companies and healthcare providers are investing heavily in AI-enabled platforms, cloud-based EHRs, and telehealth solutions to improve efficiency and patient outcomes

- The demand for eHealth solutions that offer seamless AI, cloud, and interoperability integration is growing rapidly across both clinical and non-clinical settings, as stakeholders increasingly prioritize efficiency, accessibility, and integrated care delivery

- In addition, the increasing focus on patient-centric care is encouraging the adoption of mobile health (mHealth) applications that empower individuals to actively manage their health through appointment scheduling, medication reminders, access to medical records, and real-time communication with healthcare providers

North America eHealth Market Dynamics

Driver

“Growing Need Due to Rising Chronic Disease Burden and Digital Healthcare Adoption”

- The increasing prevalence of chronic diseases among the aging population, coupled with the rapid adoption of digital healthcare technologies, is a significant driver for the heightened demand for eHealth solutions in North America

- For instance, healthcare providers and organizations are increasingly implementing telemedicine platforms, remote patient monitoring systems, and EHR solutions to improve care delivery, streamline operations, and reduce hospital visits

- As patients and providers become more aware of the benefits of digital healthcare, eHealth solutions offer advanced capabilities such as real-time health monitoring, virtual consultations, and centralized medical records, providing a compelling alternative to traditional in-person care models

- Furthermore, the growing emphasis on value-based care and healthcare cost optimization is encouraging the adoption of integrated eHealth systems that enhance care coordination, reduce inefficiencies, and improve clinical outcomes across healthcare networks

- The convenience of remote access to healthcare services, improved patient engagement through mobile health applications, and the ability to manage health data digitally are key factors propelling the adoption of eHealth solutions across hospitals, clinics, and homecare settings. The increasing availability of user-friendly platforms and supportive government initiatives further contribute to market growth

- In addition, increasing healthcare workforce shortages are driving healthcare providers to adopt digital solutions that optimize workflows, reduce administrative burden, and enable providers to manage larger patient volumes more efficiently

- Moreover, rising investments by public and private stakeholders in healthcare IT infrastructure and digital transformation initiatives are further accelerating the deployment of advanced eHealth solutions across North America

Restraint/Challenge

“Data Security Concerns and Regulatory Compliance Hurdles”

- Concerns surrounding data privacy, cybersecurity vulnerabilities, and the handling of sensitive patient information pose a significant challenge to broader adoption of eHealth solutions in North America. As digital health systems rely heavily on connected networks and cloud-based infrastructure, they are exposed to risks of data breaches and unauthorized access

- For instance, increasing reports of cyberattacks targeting healthcare organizations have raised concerns among providers and patients regarding the security of electronic health records and telehealth platforms

- Addressing these cybersecurity challenges through robust encryption, multi-factor authentication, secure cloud architectures, and strict compliance with healthcare regulations such as HIPAA is crucial for building trust and ensuring safe data exchange across systems

- In addition, the complexity of regulatory requirements, interoperability standards, and integration with legacy healthcare systems can create implementation barriers for healthcare providers, particularly smaller organizations with limited IT resources

- While investments in cybersecurity and digital infrastructure are increasing, concerns around data protection, regulatory compliance, and system integration continue to hinder seamless adoption of eHealth solutions, making it essential for stakeholders to prioritize secure, compliant, and standardized digital health frameworks for sustained market growth

- Furthermore, resistance to digital transformation among certain healthcare providers due to workflow disruptions, training requirements, and change management challenges can slow down the adoption rate of advanced eHealth technologies

- In addition, disparities in digital literacy among patients and providers may limit the effective utilization of eHealth platforms, particularly in certain segments of the population, highlighting the need for education and user-friendly solution design

North America eHealth Market Scope

The market is segmented on the basis of offering, deployment, enterprise size, functionality, technology, and end user.

- By Offering

On the basis of offering, the eHealth market is segmented into solutions and services. The solutions segment dominated the market with the largest market revenue share in 2025, driven by the widespread adoption of electronic health records (EHR), telemedicine platforms, remote patient monitoring systems, and healthcare analytics solutions across hospitals and clinics. Healthcare providers increasingly rely on integrated digital platforms to streamline clinical workflows, improve patient outcomes, and ensure interoperability across systems. The growing emphasis on digital transformation, along with the need for real-time data access and coordinated care delivery, further strengthens the demand for eHealth solutions across North America.

The services segment is expected to witness the fastest growth rate during the forecast period, fueled by increasing demand for implementation, integration, maintenance, and consulting services associated with eHealth solutions. As healthcare organizations adopt complex digital systems, they require specialized expertise for system deployment, customization, and ongoing support. In addition, managed services, cloud migration support, and cybersecurity services are gaining traction as providers seek to optimize performance, ensure regulatory compliance, and maintain secure and efficient eHealth ecosystems.

- By Deployment

On the basis of deployment, the eHealth market is segmented into cloud and on-premises. The cloud segment dominated the market with the largest revenue share of 60.9% in 2025, driven by its scalability, flexibility, and cost-effectiveness. Cloud-based eHealth solutions enable healthcare providers to store, access, and share patient data in real time, facilitating interoperability and seamless collaboration across healthcare stakeholders. The increasing adoption of cloud platforms is further supported by advancements in cybersecurity, data backup solutions, and the growing need for remote accessibility and centralized data management.

The cloud segment is also expected to witness the fastest growth rate during the forecast period due to the rapid shift toward digital healthcare infrastructure and the increasing preference for Software-as-a-Service (SaaS)-based solutions. Healthcare organizations are moving away from traditional on-premises systems to cloud-based platforms to reduce IT overhead costs, enhance scalability, and improve system integration. The rising adoption of telehealth and remote patient monitoring further accelerates the demand for cloud deployment in eHealth applications.

- By Enterprise Size

On the basis of enterprise size, the market is segmented into large enterprises and small and medium enterprises (SMEs). The large enterprises segment dominated the market with the largest revenue share in 2025, owing to their strong financial capabilities, advanced IT infrastructure, and early adoption of digital health technologies. Large hospitals, integrated healthcare systems, and major healthcare providers are heavily investing in comprehensive eHealth solutions such as EHR systems, AI-driven analytics, and interoperability platforms to manage large patient volumes and improve care coordination.

The SMEs segment is expected to witness the fastest growth rate during the forecast period, driven by increasing affordability of cloud-based eHealth solutions and the availability of subscription-based pricing models. Small clinics, independent practitioners, and mid-sized healthcare providers are increasingly adopting digital health tools to enhance operational efficiency, improve patient engagement, and remain competitive. Government initiatives and incentives promoting healthcare digitization are also encouraging SMEs to adopt eHealth technologies.

- By Functionality

On the basis of functionality, the market is segmented into content management systems, group messaging, dashboard, video sessions, social support, and others. The dashboard segment dominated the market with the largest revenue share in 2025, as dashboards provide healthcare professionals with centralized, real-time visualization of patient data, clinical metrics, and operational performance indicators. These tools support better decision-making, enhance workflow efficiency, and enable monitoring of multiple patients simultaneously, making them a critical component of eHealth platforms.

The video sessions segment is expected to witness the fastest growth rate during the forecast period, driven by the rapid adoption of telemedicine and virtual consultations. Video-based communication enables remote diagnosis, follow-ups, and patient consultations, reducing the need for in-person visits and improving access to healthcare services. The increasing acceptance of virtual care by both patients and providers, along with advancements in high-speed internet connectivity and digital communication tools, is accelerating the growth of video session functionalities in eHealth solutions.

- By Technology

On the basis of technology, the market is segmented into Internet of Things (IoT), chatbots, artificial intelligence, blockchain, big data, and others. The artificial intelligence segment dominated the market with the largest revenue share in 2025, driven by its extensive applications in predictive analytics, clinical decision support, medical imaging analysis, and personalized treatment recommendations. AI-powered tools enhance diagnostic accuracy, automate administrative processes, and improve patient outcomes, making them a core component of modern eHealth systems.

The chatbots segment is expected to witness the fastest growth rate during the forecast period, fueled by increasing demand for automated patient engagement, virtual assistants, and 24/7 support services. Chatbots are widely used for appointment scheduling, answering patient queries, symptom checking, and providing basic healthcare guidance. Their ability to improve patient interaction, reduce workload on healthcare staff, and deliver instant responses is driving their rapid adoption across healthcare providers and digital health platforms.

- By End User

On the basis of end user, the market is segmented into healthcare providers, payers, healthcare consumers, pharmacies, and others. The healthcare providers segment dominated the market with the largest revenue share in 2025, driven by the widespread adoption of eHealth solutions in hospitals, clinics, and diagnostic centers. Providers rely heavily on digital platforms such as EHR systems, telehealth solutions, and clinical management tools to streamline operations, enhance patient care, and ensure efficient data management across departments.

The healthcare consumers segment is expected to witness the fastest growth rate during the forecast period, driven by increasing patient awareness, rising adoption of mobile health applications, and growing demand for personalized and convenient healthcare services. Consumers are increasingly using wearable devices, health apps, and telehealth platforms to monitor their health, access medical consultations, and manage chronic conditions. The shift toward patient-centric care and the growing emphasis on self-management of health are key factors accelerating growth in this segment.

North America eHealth Market Regional Analysis

- The United States dominated the North America eHealth market with the largest revenue share of 85.7% in 2025, characterized by advanced healthcare infrastructure, strong digital maturity, high healthcare expenditure, and widespread implementation of EHR systems, with the country leading in telemedicine adoption, interoperability initiatives

- Healthcare providers and consumers in the region highly value the convenience, accessibility, and efficiency offered by eHealth platforms, including remote consultations, real-time patient monitoring, and seamless access to medical records across integrated digital systems

- This widespread adoption is further supported by high healthcare expenditure, advanced technological infrastructure, favorable government initiatives promoting healthcare digitization, and a highly digitally literate population, establishing eHealth solutions as a preferred approach for both clinical and non-clinical healthcare delivery across hospitals, clinics, and homecare settings

The U.S. eHealth Market Insight

The U.S. eHealth market captured the largest revenue share of 85.7% in 2025 within North America, fueled by the rapid adoption of digital health technologies, widespread implementation of electronic health records (EHR), and the strong presence of advanced healthcare infrastructure. Healthcare providers and patients are increasingly prioritizing telemedicine, remote patient monitoring, and integrated digital platforms to improve care delivery and operational efficiency. The growing preference for AI-driven healthcare solutions, cloud-based platforms, and mobile health applications further propels the eHealth industry. Moreover, the integration of digital ecosystems such as telehealth platforms, interoperable health systems, and connected devices is significantly contributing to the market’s expansion.

Canada eHealth Market Insight

The Canada eHealth market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by government-led digital health initiatives and increasing investments in healthcare IT infrastructure. The growing need for improved healthcare accessibility, especially in remote and rural areas, is fostering the adoption of telehealth and virtual care solutions. Canadian healthcare providers are also embracing cloud-based EHR systems and integrated digital platforms to enhance patient data management and care coordination. In addition, rising awareness of digital health benefits and the increasing focus on efficient healthcare delivery are encouraging the adoption of eHealth solutions across hospitals, clinics, and community care settings.

Mexico eHealth Market Insight

The Mexico eHealth market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the gradual digital transformation of the healthcare sector and increasing efforts to improve healthcare accessibility. The rising burden of chronic diseases, coupled with the need for cost-effective healthcare delivery, is encouraging the adoption of telemedicine and mobile health solutions. Government initiatives aimed at strengthening healthcare infrastructure and expanding digital connectivity are further supporting market growth. In addition, increasing penetration of smartphones and internet services is enabling wider adoption of eHealth platforms among healthcare providers and consumers.

North America eHealth Market Share

The North America eHealth industry is primarily led by well-established companies, including:

- Tencent Holdings Limited (China)

- Alibaba Health Information Technology Limited (China)

- WeDoctor Holdings Limited (China)

- JD Health International Inc (China)

- Practo Technologies Pvt. Ltd (India)

- HealthifyMe (India)

- mFine (India)

- Halodoc (Indonesia)

- MyDoc Pte. Ltd (Singapore)

- Samsung Electronics Co. Ltd (South Korea)

- Koninklijke Philips N.V. (Netherlands)

- Cisco Systems, Inc. (U.S.)

- IBM Corporation (U.S.)

- Epic Systems Corporation (U.S.)

- Allscripts Healthcare, LLC (U.S.)

- McKesson Corporation (U.S.)

- AT&T Inc. (U.S.)

- QSI Management, LLC (U.S.)

- Vodafone Group Plc (U.K.)

What are the Recent Developments in North America eHealth Market?

- In March 2026, Tom Brady-backed telehealth firm eMed raised USD 200 million in a Series A funding round, valuing the company at over USD 2 billion and supporting the development of its AI-powered healthcare platform and new payment model aimed at reducing employer healthcare costs. This reflects growing investment and innovation in telehealth and digital health solutions in the U.S.

- In March 2026, expanded telehealth coverage faced potential disruption as over 67 million Americans were at risk of losing access to telehealth services unless Congress extended Medicare funding, underscoring the reliance on policy support for sustained eHealth adoption

- In January 2026, U.S. digital health funding reached USD 19.2 billion, with capital shifting toward provider-led and workflow-driven solutions that integrate more closely with clinical operations and EHR systems. This shift indicates a maturing market where practical eHealth applications are prioritized

- In October 2025, demand for telehealth services and platforms surged, with hospitals and health systems significantly expanding their telehealth offerings to bring high-quality care directly to patients, highlighting ongoing growth in virtual care adoption across North America

- In August 2025, telehealth’s rapid expansion in GLP-1 obesity care highlighted regulatory and privacy challenges as demand surged for digital weight-loss treatments through virtual care platforms. This trend showed how eHealth services were evolving beyond basic consultations into complex chronic care management

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.