North America Health Insurance Market

Market Size in USD Billion

CAGR :

%

USD

878.02 Billion

USD

1,337.30 Billion

2025

2033

USD

878.02 Billion

USD

1,337.30 Billion

2025

2033

| 2026 –2033 | |

| USD 878.02 Billion | |

| USD 1,337.30 Billion | |

| % | |

|

North America Health Insurance Market Size

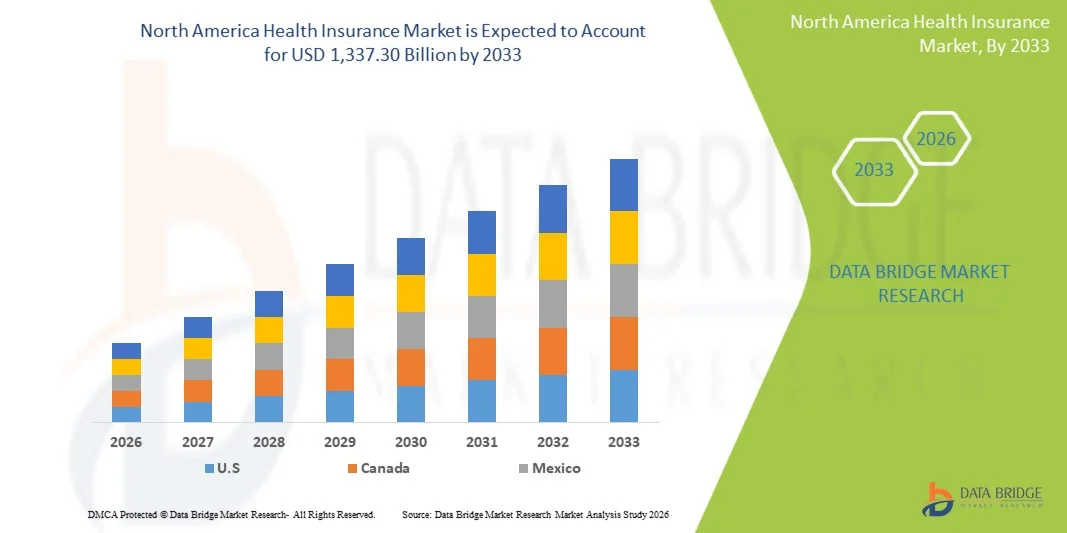

- The North America health insurance market size was valued at USD 878.02 billion in 2025 and is expected to reach USD 1,337.30 billion by 2033, at a CAGR of 5.4% during the forecast period

- The market growth is largely driven by the increasing prevalence of chronic diseases, rising healthcare costs, and expanding government initiatives to improve healthcare coverage across the U.S., Canada, and Mexico

- Furthermore, growing awareness among consumers about health coverage options, coupled with the rising adoption of digital health platforms and telemedicine services, is strengthening health insurance as an essential financial protection tool. These factors are accelerating market penetration, thereby significantly supporting the industry’s growth

North America Health Insurance Market Analysis

- Health insurance, providing financial protection against medical expenses, is a critical component of healthcare in both individual and group settings due to its role in enabling access to quality care, reducing out-of-pocket costs, and supporting preventive health programs

- The rising demand for health insurance is primarily driven by increasing healthcare costs, the prevalence of chronic diseases, and growing consumer awareness regarding financial protection against medical emergencies

- The United States dominated the North America health insurance market with the largest revenue share of 72.8% in 2025, characterized by advanced healthcare infrastructure, high healthcare spending, and the strong presence of key insurance providers

- Canada is expected to be the fastest-growing country in the North America health insurance market during the forecast period due to government initiatives to expand coverage, increasing awareness about health insurance, and rising healthcare expenditure

- Private Health Insurance Providers segment dominated the North America health insurance market with a market share of 55.3% in 2025, driven by the flexibility of plan offerings, extensive provider networks, and growing consumer preference for customized coverage solutions

Report Scope and North America Health Insurance Market Segmentation

|

Attributes |

North America Health Insurance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Health Insurance Market Trends

“Rising Adoption of Digital Health Platforms and Telemedicine”

- A significant and accelerating trend in the North America health insurance market is the increasing integration of digital health platforms and telemedicine services, enhancing accessibility and convenience of healthcare for insured members

- For instance, UnitedHealthcare offers virtual care services integrated with its insurance plans, allowing members to consult physicians remotely, schedule appointments, and access electronic health records seamlessly

- Telemedicine integration enables insurers to monitor patient health more effectively, reduce hospital readmissions, and offer preventive care recommendations, while digital platforms provide tools for claims management and health tracking

- The seamless incorporation of mobile apps and online portals facilitates centralized management of insurance benefits, claims, and provider networks, creating a more connected and efficient healthcare experience

- This trend towards digital-first, patient-centric insurance solutions is reshaping consumer expectations for healthcare access. Consequently, companies such as Anthem are enhancing AI-driven virtual health assistants to guide members through plan benefits and care options

- The demand for integrated digital health and telemedicine-enabled insurance plans is growing rapidly across both individual and group segments, as consumers increasingly prioritize convenience, accessibility, and proactive healthcare management

- Partnerships between insurers and tech companies for AI-driven predictive analytics are becoming common, helping providers identify high-risk patients and optimize care pathways to reduce overall healthcare costs

North America Health Insurance Market Dynamics

Driver

“Increasing Demand Due to Rising Healthcare Costs and Chronic Diseases”

- The growing prevalence of chronic diseases, combined with escalating healthcare costs, is a significant driver of rising demand for comprehensive health insurance coverage across North America

- For instance, Blue Cross Blue Shield highlighted initiatives to expand coverage and wellness programs for members with chronic conditions, reflecting broader industry strategies to address healthcare cost pressures

- As consumers seek protection against high medical expenses, health insurance provides coverage for inpatient and outpatient treatments, preventive care, and specialist consultations, making it an essential financial safety net

- Furthermore, the expansion of employer-sponsored plans, government-backed programs, and individual policy options is increasing accessibility and adoption of health insurance among various demographic segments

- The growing awareness of health insurance benefits, coupled with digital claims management and telemedicine services, is encouraging proactive enrollment, particularly among tech-savvy and cost-conscious consumers

- Increasing government incentives for preventive care and chronic disease management programs are motivating consumers and employers to adopt comprehensive health coverage

- Growing corporate wellness initiatives integrated with insurance plans encourage healthier lifestyles and reduce long-term treatment costs, further driving demand for health insurance products

Restraint/Challenge

“Regulatory Compliance and Affordability Concerns”

- Compliance with complex healthcare regulations, including the Affordable Care Act provisions and state-specific insurance mandates, poses a significant challenge for insurers operating across North America

- For instance, discrepancies in coverage requirements across states can make plan standardization difficult and increase administrative burdens for providers

- Rising premiums and out-of-pocket costs for certain plans create affordability concerns, particularly for small businesses, self-employed individuals, and low-to-middle-income families, limiting adoption rates

- In addition, data privacy and cybersecurity issues related to electronic health records and digital insurance platforms raise consumer apprehension about sharing sensitive personal and medical information online

- Overcoming these challenges requires regulatory alignment, development of cost-effective insurance products, enhanced cybersecurity measures, and increased consumer education about available coverage options and benefits

- Complex claim settlement processes and delayed reimbursements can lead to dissatisfaction among policyholders, affecting retention and adoption rates

- The fragmentation of insurance providers and plans across states can confuse consumers and increase the effort required to compare and select suitable health insurance options

North America Health Insurance Market Scope

The market is segmented on the basis of type, services, level of coverage, service providers, health insurance plans, demographics, coverage type, end users, and distribution channels.

- By Type

On the basis of type, the North America health insurance market is segmented into product and solutions. The product segment dominated the market with the largest revenue share in 2025, driven by the traditional adoption of standard insurance products such as individual and group health plans. Consumers often prioritize product-based offerings for their well-defined benefits, established provider networks, and straightforward claim processes. Product-based plans are widely preferred by employers and government programs due to compliance with regulations and ease of administration. The market sees strong demand for product-based health insurance due to its reliability and alignment with mainstream coverage requirements. In addition, policyholders favor product-based plans for the predictability in premiums and benefits, making them a core component of the market.

The solutions segment is anticipated to witness the fastest growth rate during the forecast period, fueled by increasing adoption of integrated digital health platforms and personalized insurance solutions. Solutions-based offerings, including wellness programs, telemedicine services, and AI-driven risk management tools, provide insurers and policyholders with proactive healthcare management options. Growing awareness of preventive care and chronic disease monitoring further supports demand for solutions-oriented plans. Innovative digital tools allow real-time health tracking, improving member engagement and reducing long-term costs. Corporate and individual clients increasingly prefer solution-based offerings for their flexibility and customization. The expansion of virtual care and personalized insurance packages also drives the accelerated growth of this segment.

- By Services

On the basis of services, the market is segmented into inpatient treatment, outpatient treatment, medical assistance, and others. The inpatient treatment segment dominated the market in 2025, driven by high costs associated with hospitalization and surgical procedures. Policyholders prioritize coverage for expensive inpatient care, making it a critical component of most insurance plans. Inpatient services often include post-operative care, emergency treatments, and specialized hospital services, strengthening their demand among both individual and group buyers. High adoption of employer-sponsored and corporate group plans further enhances this segment’s dominance. The inclusion of advanced treatment options and network hospital access adds additional appeal. Insurers emphasize inpatient coverage as a key selling point to attract and retain customers.

The outpatient treatment segment is expected to witness the fastest growth during the forecast period, supported by increasing utilization of preventive care, minor medical procedures, and telehealth consultations. Outpatient services are cost-effective and convenient, driving consumer preference for plans offering comprehensive outpatient coverage. Digital claims processing and mobile health apps further enhance adoption by providing seamless service access. Integration with virtual care platforms enables remote consultations and follow-up care, boosting popularity. Consumers are increasingly attracted to plans that reduce hospitalization needs while maintaining quality care. The segment benefits from growing awareness of preventive health and early intervention programs.

- By Level of Coverage

On the basis of level of coverage, the market is segmented into Bronze, Silver, Gold, and Platinum plans. The Gold segment dominated the market in 2025 due to its balance of comprehensive coverage and affordable premiums. Gold plans typically include inpatient and outpatient care, specialist consultations, prescription drugs, and preventive services, making them attractive to middle-income families and employers providing group coverage. Policyholders also value Gold plans for cost-sharing structures and network flexibility. Gold plans often come with value-added benefits such as wellness programs, chronic care management, and telehealth integration. Employers frequently select Gold plans to provide employees with robust coverage while managing costs. Consumer trust in Gold-level coverage further reinforces its market dominance.

The Platinum segment is expected to witness the fastest growth during the forecast period, driven by high-income individuals and corporate clients seeking extensive coverage with minimal out-of-pocket expenses. Platinum plans offer top-tier benefits, access to premium healthcare providers, and additional services such as concierge care and international coverage. These plans appeal to affluent policyholders who prioritize comprehensive protection and personalized service. Increasing demand for seamless integration with digital health platforms also fuels growth. Companies are focusing on expanding Platinum offerings to capture premium market share. The rising adoption of high-value plans in corporate and executive segments further accelerates this trend.

- By Service Providers

On the basis of service providers, the market is segmented into public and private health insurance providers. The private health insurance providers segment dominated the market in 2025 with a market share of 55.3% due to their flexibility, wide range of plan options, and rapid adoption of digital tools for claims management and telehealth. Private insurers are preferred by employers and high-income individuals seeking customized coverage solutions. Strong marketing and brand presence also contribute to dominance. Many private providers invest in AI-driven wellness and risk management programs to improve member outcomes. The segment benefits from policy innovation and extensive provider networks. Private providers continue to drive growth with tech-enabled services and personalized plan offerings.

The public health insurance providers segment is expected to witness the fastest growth during the forecast period, driven by government initiatives to expand coverage, increase accessibility, and reduce uninsured populations. Programs offering subsidies, preventive care incentives, and expanded Medicaid or public employee coverage are accelerating adoption. Digital enrollment platforms and mobile-based claim filing enhance accessibility. Public providers increasingly collaborate with tech partners to deliver virtual care. Rising health awareness among lower-income populations supports growth. Expansion of public programs in underserved regions further strengthens this segment’s trajectory.

- By Health Insurance Plans

On the basis of health insurance plans, the market is segmented into POS, EPOS, Indemnity Health Insurance, HSA, QSEHRAs, PPO, HMO, and others. The PPO segment dominated the market in 2025 due to its wide network of healthcare providers and flexibility to access specialists without referrals. Policyholders often prefer PPO plans for freedom of choice, better coverage options, and ease of claim settlement. Employers frequently select PPOs for their scalability and adaptability to diverse workforce needs. PPO plans also attract high adoption among individual consumers seeking premium coverage. Integration with telemedicine and digital platforms further enhances their value proposition. Network breadth and flexibility drive strong retention and continuous demand.

The HSA segment is expected to witness the fastest growth during the forecast period, driven by rising awareness of health savings accounts linked with high-deductible plans, tax benefits, and the ability to cover out-of-pocket medical expenses. HSAs appeal to tech-savvy and cost-conscious consumers seeking more control over healthcare spending. Integration with digital insurance platforms and wellness tracking further increases adoption. Employer incentives and flexible contribution options boost popularity. HSAs provide members with long-term savings potential while encouraging preventive care. Growing preference for customized, cost-efficient coverage underpins the segment’s rapid growth.

- By Demographics

On the basis of demographics, the market is segmented into adults, minors, and senior citizens. The adults segment dominated the market in 2025, due to their high participation in employer-sponsored health insurance and individual plan purchases. Adults often prioritize comprehensive coverage, including preventive, chronic, and emergency care. Rising awareness of personal health management supports adoption. Corporate wellness initiatives and digital health tools increase engagement. Adults represent the largest insured population across the U.S. and Canada. Their income levels and purchasing power further reinforce dominance.

The senior citizens segment is expected to witness the fastest growth during the forecast period, fueled by the increasing aging population, higher healthcare utilization, and demand for coverage addressing age-related chronic conditions. Plans often include additional benefits such as home healthcare, long-term care, and specialized disease management. Government and private incentives target this segment. Digital health and telemedicine adoption is rising among seniors. The need for customized chronic care management supports growth. Expansion of senior-focused insurance programs accelerates market adoption.

- By Coverage Type

On the basis of coverage type, the market is segmented into lifetime coverage and term coverage. The lifetime coverage segment dominated the market in 2025, driven by consumers’ desire for long-term protection against high medical expenses and unpredictable health events. Lifetime plans provide stability, continuity of care, and peace of mind. They are often preferred by families and long-term policyholders. Lifetime coverage ensures consistent benefits regardless of changing health status. Insurers promote lifetime plans to enhance customer loyalty. Strong regulatory support for lifetime policies reinforces market dominance.

The term coverage segment is expected to witness the fastest growth during the forecast period, supported by affordable premiums and flexible policy durations. Term plans appeal to young adults, first-time insurance buyers, and cost-sensitive consumers. Short-term protection offers immediate benefits without long-term commitment. Digital platforms make term plan enrollment easy and fast. Term plans are increasingly bundled with preventive care programs. Growth is accelerated by rising awareness of insurance importance among younger populations.

- By End User

On the basis of end user, the market is segmented into corporates, individuals, and others. The corporates segment dominated the market in 2025 due to widespread employer-sponsored plans and group coverage providing benefits to large employee bases. Corporates negotiate comprehensive plans to reduce absenteeism and improve employee well-being. Employer benefits and tax incentives enhance adoption. Large-scale HR management platforms facilitate seamless enrollment. Corporate plans often include wellness programs and telehealth integration. Strong purchasing power of corporates strengthens market share.

The individuals segment is expected to witness the fastest growth during the forecast period, fueled by rising health awareness, digital enrollment platforms, and availability of personalized plans. Consumers increasingly seek plans offering customized coverage, wellness incentives, and telemedicine integration. Online comparison tools simplify plan selection. Rising middle-class population supports adoption. Young professionals prefer flexible and tech-enabled individual policies. Growth is accelerated by targeted marketing and consumer education initiatives.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct sales, financial institutions, e-commerce, hospitals & clinics, and others. The direct sales segment dominated the market in 2025 due to strong relationships between insurers and policyholders, personalized guidance, and established broker networks. Direct engagement allows insurers to explain complex coverage details efficiently. Policyholders value expert advice and tailored recommendations. Direct sales ensure consistent customer support and claim assistance. Strong brand presence through direct channels reinforces trust. Long-standing broker networks facilitate penetration into corporate and individual segments.

The e-commerce segment is expected to witness the fastest growth during the forecast period, driven by increasing digital adoption, online plan comparison platforms, and convenient policy enrollment. Consumers increasingly prefer digital platforms for easy plan selection, instant quotes, and integrated claim management. Mobile apps and portals enhance customer experience. E-commerce reduces administrative costs for insurers. The segment benefits from younger, tech-savvy consumers. Rising trust in digital transactions and online payments further accelerates adoption.

North America Health Insurance Market Regional Analysis

- The United States dominated the North America health insurance market with the largest revenue share of 72.8% in 2025, characterized by advanced healthcare infrastructure, high healthcare spending, and the strong presence of key insurance providers

- Consumers in the region highly value comprehensive coverage, access to a wide network of healthcare providers, and integration with digital health platforms and telemedicine services, which enhance convenience and quality of care

- This widespread adoption is further supported by well-established healthcare infrastructure, high disposable incomes, regulatory frameworks supporting coverage, and the growing preference for personalized and proactive healthcare management, establishing health insurance as an essential financial protection tool for individuals and corporates alike

U.S. Health Insurance Market Insight

The U.S. health insurance market captured the largest revenue share of 72.8% in 2025 within North America, fueled by rising healthcare costs, increasing prevalence of chronic diseases, and widespread adoption of employer-sponsored and private insurance plans. Consumers are increasingly prioritizing comprehensive coverage that provides access to a wide network of healthcare providers and integrated digital health services. The growing demand for telemedicine, wellness programs, and AI-enabled claims management further propels the health insurance industry. Moreover, regulatory support for individual and corporate insurance coverage, alongside tax incentives and subsidy programs, is significantly contributing to market expansion.

Canada Health Insurance Market Insight

The Canada health insurance market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by government initiatives to enhance healthcare access and coverage. Rising awareness among consumers about supplemental and private insurance options is fostering adoption. Canadians increasingly seek coverage that complements publicly funded healthcare, providing access to prescription drugs, dental, and vision services. The demand for convenience, online plan management, and digital claims processing is also boosting growth. Both urban and rural regions are witnessing increased enrollment in private and employer-sponsored plans.

Mexico Health Insurance Market Insight

The Mexico health insurance market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing healthcare expenditure and rising demand for private coverage. Consumers are seeking better quality care, faster access to medical services, and financial protection against high out-of-pocket costs. Expansion of corporate health plans, government-backed programs, and digital health platforms is supporting market growth. In addition, growing awareness about the benefits of health insurance among middle-class populations is encouraging adoption. Integration with telemedicine services and mobile health apps is further enhancing the appeal of private insurance solutions.

North America Health Insurance Market Share

The North America Health Insurance industry is primarily led by well-established companies, including:

- UnitedHealth Group (U.S.)

- Aetna Inc. (U.S.)

- Centene Corporation (U.S.)

- Humana Inc. (U.S.)

- Elevance Health, Inc. (U.S.)

- Kaiser Foundation Health Plan (U.S.)

- Health Care Services Corporation (U.S.)

- Cigna Healthcare (U.S.)

- Molina Healthcare, Inc. (U.S.)

- GuideWell Mutual Holding Corporation (U.S.)

- Independence Health Group Inc. (U.S.)

- Highmark Inc. (U.S.)

- Blue Cross Blue Shield of Michigan (U.S.)

- Blue Shield of California (U.S.)

- UPMC Health Plan (U.S.)

- Blue Cross Blue Shield of North Carolina (U.S.)

- Health Net of California, Inc. (U.S.)

- CareSource (U.S.)

- CareFirst BlueCross BlueShield (U.S.)

What are the Recent Developments in North America Health Insurance Market?

- In November 2025, the U.S. government announced a new initiative the Generous Model aimed at reducing prescription drug costs for Medicaid beneficiaries by aligning drug prices with those in eight other developed countries, with the program set to begin in 2026. This policy change is expected to impact Medicaid drug coverage and rebates, potentially lowering out‑of‑pocket costs for low‑income Americans

- In November 2025, a new faith‑based health insurance company, Presidio Healthcare, launched its “FortressPlan” in Texas, offering a Catholic‑aligned plan excluding certain services (e.g., abortion, contraceptives) to appeal to consumers who prioritize religious‑based coverage. This reflects diversification in plan offerings within the U.S. market

- In August 2025, Prudential Financial agreed to a USD 100 million settlement with the U.S. Federal Trade Commission over allegations that its Assurance IQ unit misled consumers about the scope of healthcare insurance plans it offered, resulting in unexpected out‑of‑pocket expenses. This settlement highlights regulatory scrutiny on health insurance marketing practices

- In July 2025, analyses reported significant premium hikes for Affordable Care Act (ACA) marketplace plans in 2026, with median premiums expected to rise sharply due to the expiration of enhanced federal subsidy programs and rising healthcare costs the steepest increases in several years

- In November 2024, UnitedHealthcare expanded its Individual & Family ACA Marketplace plans to 30 U.S. states, broadening access to Affordable Care Act coverage with features such as USD 0 deductibles, virtual urgent care, and integrated dental and vision benefits, helping more residents access affordable health insurance options

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.