North America Infertility Testing Market

Market Size in USD Billion

CAGR :

%

USD

1.60 Billion

USD

2.75 Billion

2025

2033

USD

1.60 Billion

USD

2.75 Billion

2025

2033

| 2026 –2033 | |

| USD 1.60 Billion | |

| USD 2.75 Billion | |

| % | |

|

North America Infertility Testing Market Size

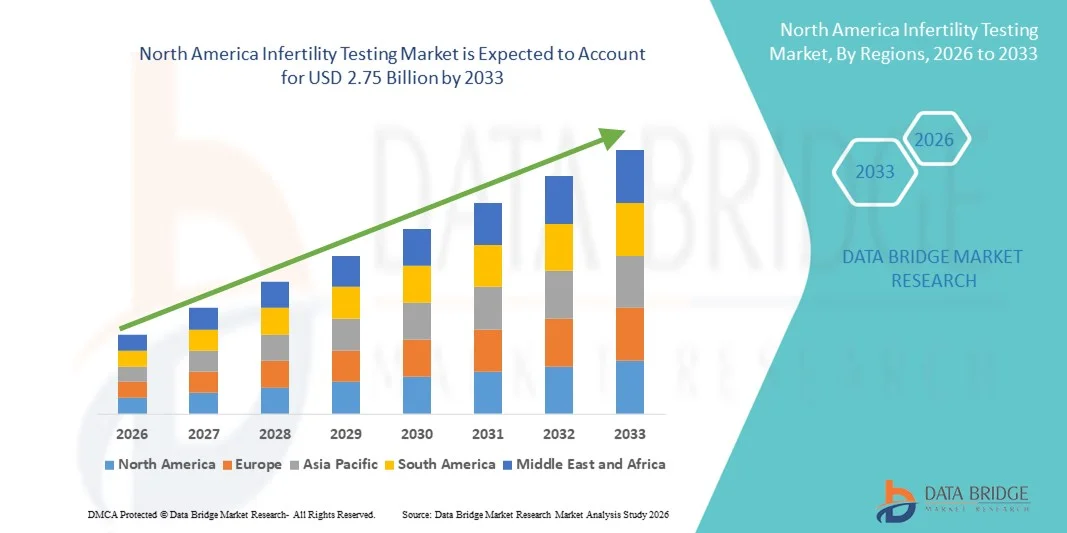

- The North America infertility testing market size was valued at USD 1.60 billion in 2025 and is expected to reach USD 2.75 billion by 2033, at a CAGR of 7.05% during the forecast period

- The market growth in North America is largely fueled by rising infertility prevalence due to lifestyle factors, delayed parenthood, and greater awareness of reproductive health, which are boosting demand for advanced infertility diagnostic and fertility testing solutions

- Furthermore, technological advancements in ovulation prediction tests, home‑based fertility kits, and digital reproductive health monitoring, along with strong healthcare infrastructure and widespread availability through clinical and consumer channels, are driving adoption. These converging factors increasing reproductive health awareness, digitalisation of at‑home testing, and supportive regulatory frameworks in key markets

North America Infertility Testing Market Analysis

- Infertility testing, covering both female and male infertility testing, is becoming an increasingly vital component of reproductive healthcare in the U.S. due to rising awareness of fertility issues, advancements in diagnostic technologies, and the growing availability of accurate, minimally invasive, and home-based test kits

- The escalating demand for infertility testing is primarily fueled by delayed parenthood, lifestyle-related reproductive challenges, increasing prevalence of infertility, and a rising preference for convenient, reliable, and easy-to-use testing solutions that provide actionable insights for both patients and clinicians

- The U.S. dominated the North America infertility testing with the largest revenue share of 68.7% in 2025, characterized by advanced healthcare infrastructure, high consumer awareness, and a strong presence of key market players. The country is experiencing substantial growth in infertility testing adoption, particularly in fertility centers, hospitals, and home-based settings, driven by innovations in Human Follicular Stimulating Hormone (FSH) urine test kits, Luteinizing Hormone (LH) urine test kits, and Human Chorionic Gonadotropin (HCG) blood test kits

- Canada is expected to be the fastest-growing country in the North America infertility testing during the forecast period due to increasing reproductive health awareness, rising disposable incomes, and expanding access to advanced fertility testing solutions across both urban and semi-urban healthcare facilities

- Female infertility testing dominated the North America infertility testing with a market share of 55.9% in 2025, driven by high adoption rates of hormone-based urine and blood test kits, strong clinical validation, and growing consumer trust in reliable, at-home testing solutions

Report Scope and North America Infertility Testing Market Segmentation

|

Attributes |

North America Infertility Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Infertility Testing Market Trends

Enhanced Convenience Through At-Home and Digital Test Kits

- A significant and accelerating trend in the North America infertility testing market is the growing adoption of digital and at-home test kits, including FSH, LH, and HCG hormone kits, enabling consumers to monitor fertility conveniently without visiting clinics

- For instance, the Modern Fertility Hormone Test Kit allows users to collect samples at home and receive results through a secure digital portal, while LetsGetChecked provides similar services for both male and female fertility assessments

- Integration of digital platforms with fertility testing enables features such as tracking ovulation cycles, personalized reproductive health recommendations, and alerts for abnormal hormone levels, allowing users to make timely decisions and seek clinical guidance

- The seamless connectivity of infertility test kits with mobile apps and online platforms facilitates centralized monitoring of fertility parameters, appointment scheduling with clinics, and integration with health management tools, creating a comprehensive fertility tracking experience

- This trend towards more user-friendly, connected, and data-driven infertility testing is fundamentally reshaping consumer expectations in reproductive healthcare. Consequently, companies are developing AI-supported fertility kits and subscription services that provide personalized insights and recommendations

- The demand for convenient, accurate, and at-home infertility testing solutions is growing rapidly across both consumers and healthcare providers, as patients increasingly prioritize privacy, accessibility, and proactive reproductive health management

- Technological advancements in lab-on-a-chip and microfluidic testing are making home-based kits more accurate, faster, and capable of providing results comparable to clinical laboratories, enhancing consumer confidence

North America Infertility Testing Market Dynamics

Driver

Growing Need Due to Rising Infertility Awareness and Delayed Parenthood

- The increasing prevalence of infertility and growing awareness of reproductive health challenges is a significant driver for the heightened demand for infertility testing in the U.S.

- For instance, in March 2025, Modern Fertility expanded its hormone testing services across fertility clinics and direct-to-consumer channels, aiming to improve early fertility detection and patient engagement

- As couples delay parenthood due to career or lifestyle choices, infertility testing offers insights into ovulatory patterns, hormone levels, and sperm quality, providing critical guidance for family planning and treatment options

- Furthermore, rising adoption of digital health platforms and home-based testing solutions is making infertility diagnostics more accessible and convenient for patients, complementing traditional clinic-based testing

- The convenience of at-home test kits, real-time digital reporting, and integration with fertility apps are key factors propelling adoption among patients and healthcare providers. Subscription services and remote monitoring options further contribute to market growth

- Increased investment by biotech and health tech companies into reproductive diagnostics and fertility monitoring solutions is expanding the availability and sophistication of infertility testing options

- Rising collaborations between fertility clinics, telemedicine providers, and at-home testing companies are enhancing patient access and personalized care, driving further market growth

Restraint/Challenge

Privacy Concerns and Regulatory Compliance Hurdles

- Concerns regarding the accuracy, data privacy, and regulatory compliance of at-home infertility testing pose significant challenges to broader market penetration

- For instance, reports of inaccurate results or mishandling of sensitive health data have made some consumers hesitant to adopt direct-to-consumer fertility testing solutions

- Addressing these concerns through strict adherence to FDA regulations, secure data encryption, and clinical validation is crucial for building consumer trust. Companies emphasize privacy policies and certified testing procedures to reassure potential users

- In addition, relatively high costs of comprehensive hormone and fertility test kits compared to standard clinical visits can be a barrier for price-sensitive consumers, despite increasing affordability of basic testing kits

- While prices are gradually decreasing, perceived premium costs and concerns about result reliability can still hinder adoption. Overcoming these challenges through education, regulatory transparency, and affordable yet accurate testing options is vital for sustained market growth

- Limited awareness among certain demographics about at-home fertility testing and hormone monitoring can slow market penetration, requiring targeted educational campaigns by providers

- Differences in regulatory frameworks and approval timelines across U.S. states, along with evolving telehealth policies, create challenges for uniform product distribution and nationwide adoption

North America Infertility Testing Market Scope

The market is segmented on the basis of type, test kits, prescription mode, distribution channel, and end use.

- By Type

On the basis of type, the North America infertility testing market is segmented into female infertility testing and male infertility testing. The Female Infertility Testing segment dominated the market with the largest revenue share of 55.9% in 2025, driven by the higher adoption of hormone-based diagnostic tests such as FSH, LH, and HCG kits. Women often prioritize testing for early detection of ovulatory or hormonal irregularities, which is critical for family planning and assisted reproductive treatments. The segment benefits from strong clinical validation and widespread availability through both hospitals and at-home testing platforms. Digital and AI-enabled testing tools for female infertility further enhance convenience and accuracy, boosting market adoption. In addition, healthcare providers and fertility clinics actively recommend female-focused diagnostic tests, strengthening market dominance.

The Male Infertility Testing segment is anticipated to witness the fastest growth rate, with a CAGR of 10% from 2026 to 2033, fueled by increasing awareness of male reproductive health issues. Growing recognition of factors such as low sperm count, motility issues, and hormonal imbalances is prompting higher demand for semen analysis and hormone test kits for men. Technological innovations, including home-based and digital sperm testing solutions, are making male infertility testing more accessible and convenient. Rising involvement of men in proactive fertility planning and partnerships between telehealth platforms and laboratories also contribute to growth. Awareness campaigns targeting male fertility and lifestyle-related fertility risks are further boosting adoption.

- By Test Kits

On the basis of test kits, the market is segmented into FSH Urine Test Kits, LH Urine Test Kits, HCG Hormone Blood Test Kits, and Others. The FSH Urine Test Kits segment dominated the market with the largest revenue share in 2025, driven by its accuracy in assessing ovarian reserve and reproductive health in women. FSH testing is widely recommended by fertility specialists, enhancing adoption across clinics and home-testing users. The kits’ simplicity, non-invasive sample collection, and integration with digital health apps make them highly convenient. They also provide critical insights for planning assisted reproductive technologies such as IVF. Growing consumer awareness of fertility monitoring and preventive testing further supports the segment’s dominance.

The LH Urine Test Kits segment is expected to witness the fastest growth during the forecast period, due to its ability to precisely predict ovulation and support family planning efforts. Rising adoption of at-home LH testing among women trying to conceive is driving demand. Integration with fertility tracking apps and digital health platforms enhances user convenience and engagement. The kits’ affordability and ease of use compared to clinical testing also contribute to rapid adoption. Telehealth services promoting remote monitoring of ovulation cycles are fueling growth. Continuous technological innovations, including AI-assisted LH detection, further strengthen the segment’s expansion.

- By Prescription Mode

On the basis of prescription mode, the market is segmented into prescription-based and over-the-counter (OTC) based solutions. The Prescription-Based segment dominated in 2025, accounting for the largest revenue share, as many infertility tests require physician oversight to ensure accurate interpretation and subsequent treatment planning. Clinics and fertility centers often prescribe hormone and ovulation test kits to guarantee clinical reliability. Prescription-based testing also assures regulatory compliance and integration with assisted reproductive treatment workflows. Patients with complex fertility issues rely heavily on these controlled testing channels for precision and safety. The clinical guidance provided with prescription kits enhances trust and encourages higher adoption.

The OTC-Based segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer preference for privacy, convenience, and at-home fertility monitoring. Digital health platforms, subscription-based kits, and telehealth services enable direct access to OTC test kits without clinic visits. Growing awareness of reproductive health and proactive family planning among younger adults is boosting demand. Ease of sample collection, app integration, and faster reporting make OTC solutions highly attractive. Increasing marketing by fertility startups and online pharmacies further accelerates growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospitals & clinics, online pharmacies, and pharmacies & drug stores. The Hospitals & Clinics segment dominated in 2025, driven by the high adoption of infertility testing in fertility centers and specialized reproductive healthcare facilities. Patients often prefer clinic-based testing due to professional supervision, validated results, and integration with treatment plans. The availability of specialized laboratory infrastructure and expert interpretation of results supports market dominance. Clinics also offer bundled diagnostic services that include multiple hormone and fertility tests. Strategic partnerships between fertility centers and test kit manufacturers further enhance this channel’s dominance.

The Online Pharmacies segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing consumer preference for home delivery, telehealth integration, and subscription-based fertility testing kits. The convenience of ordering kits online, receiving guidance digitally, and tracking results remotely is appealing to tech-savvy users. Rising e-commerce adoption and awareness campaigns about fertility health boost this channel. Online pharmacies also allow discreet and private access to OTC and at-home test kits. Expanding digital platforms offering AI-assisted interpretation are driving rapid market growth.

- By End Use

On the basis of end use, the market is segmented into fertility centers, hospitals and clinics, research institutes, and cryobanks. The Fertility Centers segment dominated in 2025 with the largest revenue share, as these centers perform a majority of infertility testing for both diagnosis and treatment planning. They offer comprehensive testing services, including FSH, LH, and HCG analysis, often integrated with IVF and assisted reproductive technology programs. Fertility centers benefit from high patient throughput, specialized lab infrastructure, and professional guidance, supporting dominant adoption. Partnerships with at-home kit providers also expand their service portfolio. Strong patient trust in specialized centers reinforces market leadership.

The Hospitals and Clinics segment is expected to witness the fastest growth during the forecast period due to expanding access to reproductive healthcare, telehealth integration, and government support for fertility awareness programs. Hospitals are increasingly offering infertility testing as part of women’s health and wellness packages. Growing investments in diagnostic laboratories, AI-assisted testing, and digital reporting further boost adoption. The trend of combining clinical testing with at-home sample collection is accelerating growth. Increased patient awareness of fertility monitoring drives rapid expansion in this channel.

North America Infertility Testing Market Regional Analysis

- The U.S. dominated the North America infertility testing with the largest revenue share of 68.7% in 2025, characterized by advanced healthcare infrastructure, high consumer awareness, and a strong presence of key market players

- Consumers and patients in the region highly value the convenience, accuracy, and early detection capabilities offered by infertility tests, including hormone-based FSH, LH, and HCG kits, as well as digital and AI-enabled reporting tools

- This widespread adoption is further supported by advanced healthcare infrastructure, high disposable incomes, a digitally connected population, and the growing preference for at-home and telehealth-enabled fertility monitoring, establishing infertility testing as a key component of reproductive healthcare services for both clinics and home users

U.S. Infertility Testing Market Insight

The U.S. infertility testing market captured the largest revenue share of 68.7% in 2025 within North America, fueled by increasing awareness of reproductive health, rising infertility prevalence, and the growing adoption of advanced diagnostic and at-home fertility testing solutions. Consumers and patients are increasingly prioritizing early detection through hormone-based FSH, LH, and HCG test kits, as well as digital platforms offering AI-assisted reporting. The growing preference for telehealth services and home-based fertility monitoring further propels the market. Moreover, integration with mobile apps and fertility tracking platforms is significantly enhancing accessibility, convenience, and personalized care.

Canada Infertility Testing Market Insight

The Canada infertility testing market is expected to grow at the fastest CAGR during the forecast period, driven by increasing reproductive health awareness, rising disposable incomes, and expanding access to fertility clinics and digital health services. The adoption of home-based and OTC fertility test kits is rising rapidly, supported by government initiatives promoting reproductive healthcare and telemedicine solutions. Canadians are increasingly seeking convenience, privacy, and accurate results, making at-home hormone and ovulation testing highly popular. The growing number of collaborations between telehealth providers and fertility centers further supports market expansion.

Mexico Infertility Testing Market Insight

The Mexico infertility testing market is witnessing steady growth due to increasing awareness of reproductive health issues and rising demand for affordable diagnostic solutions. Fertility clinics are expanding services, and home-based test kits are gaining traction among urban populations. Government programs promoting maternal and reproductive health are contributing to the market’s development. In addition, the integration of digital reporting tools and mobile platforms is enhancing accessibility and convenience. The trend of combining clinical and at-home testing solutions is encouraging adoption in both urban and semi-urban regions.

North America Infertility Testing Market Share

The North America Infertility Testing industry is primarily led by well-established companies, including:

- Modern Fertility (U.S.)

- Proov (U.S.)

- YO Home Sperm Test (U.S.)

- Quest Diagnostics (U.S.)

- Labcorp (U.S.)

- Sema4 (U.S.)

- First Response (U.S.)

- Mira (U.S.)

- LetsGetChecked (Ireland)

- Fairhaven Health (U.S.)

- Fertility Focus (U.K.)

- Abcam (U.K.)

- Thermo Fisher Scientific (U.S.)

- Cook (U.S.)

- Vitrolife (Sweden)

- Hamilton Thorne (U.S.)

- FUJIFILM Irvine Scientific (U.S.)

- CooperSurgical (U.S.)

- Bio Rad Laboratories (U.S.)

- Abbott (U.S.)

What are the Recent Developments in North America Infertility Testing Market?

- In December 2025, Femasys received U.S. FDA 510(k) clearance for its next‑generation FemVue Controlled diagnostic device. Femasys Inc. announced that its FemVue Controlled device a new diagnostic tool for evaluating fallopian tube status received FDA 510(k) clearance in late 2025. This innovation integrates previous FemVue and FemChec technologies into a single platform, enabling broader clinical use and more efficient fertility diagnostics

- In November 2025, Anova Fertility & Reproductive Health, a leading fertility clinic network, celebrated a landmark USD 50 million government investment to support the Ontario Fertility Program (OFP), aimed at reducing wait times, tripling access to publicly funded IVF cycles and associated infertility testing, and enhancing reproductive care across the province

- In June 2025, doctors reported the first pregnancy using a new AI‑based sperm detection system (STAR). At Columbia University Fertility Center, clinicians reported a landmark case where a couple achieved pregnancy using STAR (Sperm Track and Recovery) an AI‑powered platform that detects and isolates rare sperm in azoospermic samples previously undetectable with standard methods

- In April 2025, U.S. IVF usage data showed continued growth with nearly 96,000 babies born via ART. The Society for Assisted Reproductive Technology (SART) released national data for 2023 in April 2025, showing that over 95,860 babies were born from IVF cycles in the U.S. up from about 91,771 in 2022. The total number of IVF cycles also rose significantly, reflecting increased demand for assisted reproductive technologies and associated diagnostic testing

- In March 2025, Femasys announced that the U.S. FDA granted Investigational Device Exemption (IDE) approval to advance the final pivotal clinical trial (Part B) for its FemBloc® system a non‑surgical, in‑office permanent birth control option. The announcement also highlighted a USD 12M financing round to support the trial, underlining investor confidence in fertility‑related innovations

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.