North America Leber Congenital Amaurosis Market

Market Size in USD Million

USD

400.00 Million

USD

564.50 Million

2025

2033

USD

400.00 Million

USD

564.50 Million

2025

2033

| 2026 - 2033 | |

| USD 400.00 Million | |

| USD 564.50 Million | |

| % | |

|

North America Leber Congenital Amaurosis Market Size

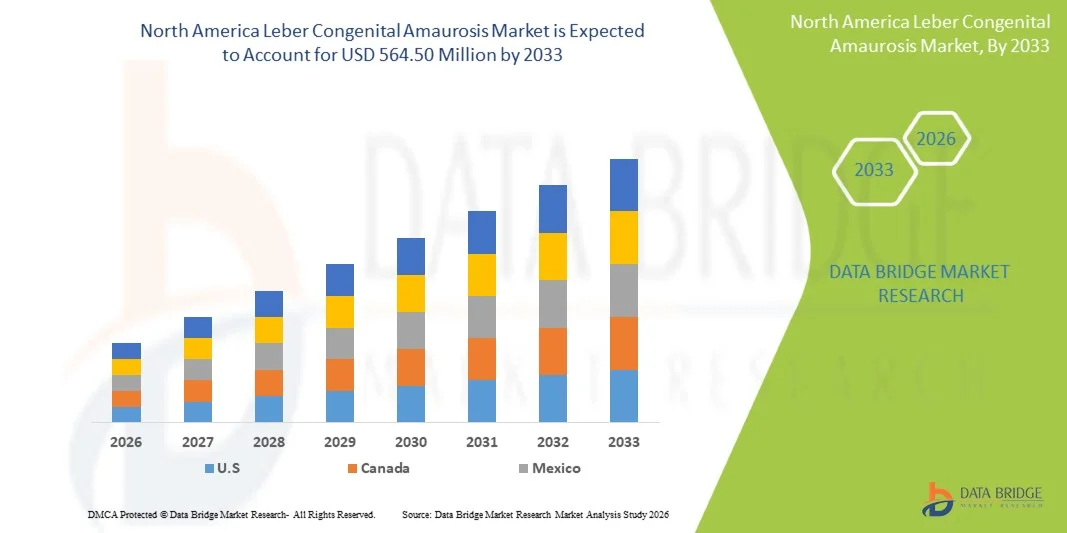

- The North America Leber Congenital Amaurosis market size was valued at USD 400.00 million in 2025 and is expected to reach USD 564.50 million by 2033, at a CAGR of 4.4% during the forecast period

- The market growth is primarily driven by increasing adoption of advanced gene therapies, rising prevalence of inherited retinal disorders, and ongoing clinical advancements in ocular precision medicine across the region

- Furthermore, growing demand for early diagnosis, improved access to rare disease treatment pathways, and expanding investment in ophthalmic research are strengthening the adoption of innovative therapeutic solutions, thereby significantly supporting the market expansion over the forecast period

North America Leber Congenital Amaurosis Market Analysis

- Leber Congenital Amaurosis, a rare inherited retinal disorder market, is increasingly driven by advancements in gene therapy, growing focus on early genetic diagnosis, and expanding clinical research in precision ophthalmology aimed at treating severe childhood-onset vision loss

- The escalating demand for Leber Congenital Amaurosis treatment is primarily fueled by rising prevalence of inherited retinal diseases, increasing adoption of newborn genetic screening programs, and growing availability of targeted gene-based therapies

- The United States dominated the North America Leber Congenital Amaurosis market with the largest revenue share of 88.2% in 2025, characterized by strong healthcare infrastructure, early adoption of approved gene therapies, and robust presence of leading biotechnology and ophthalmology research companies

- Canada is expected to be the fastest growing country in the North America Leber Congenital Amaurosis market during the forecast period due to expanding access to genetic testing, increasing rare disease awareness, and supportive government initiatives for orphan drug development and clinical trials

- Therapy segment dominated the North America Leber Congenital Amaurosis market with a market share of 41.5% in 2025, driven by its ability to address underlying genetic mutations, increasing regulatory approvals, and strong pipeline activity in ocular gene and cell-based therapies

Report Scope and North America Leber Congenital Amaurosis Market Segmentation

|

Attributes |

North America Leber Congenital Amaurosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Leber Congenital Amaurosis Market Trends

“Advancement in Gene Therapy and Precision Ophthalmology”

- A significant and accelerating trend in the North America Leber Congenital Amaurosis market is the growing adoption of gene therapy and precision medicine approaches aimed at correcting underlying genetic mutations responsible for early-onset vision loss in pediatric patients

- For instance, therapies such as voretigene neparvovec have demonstrated functional vision improvement in eligible patients with RPE65-associated LCA, supporting increased clinical adoption and awareness of gene-based interventions

- Advancements in next-generation sequencing and retinal gene editing technologies are enabling earlier and more accurate diagnosis of Leber Congenital Amaurosis, facilitating timely treatment decisions and improving patient outcomes through targeted therapeutic strategies

- The integration of genetic testing platforms with ophthalmic care pathways is allowing clinicians to better stratify patients and personalize treatment approaches, thereby strengthening the role of precision medicine in inherited retinal disease management

- This shift toward mutation-specific therapies and individualized treatment planning is reshaping clinical expectations for rare retinal disorders, with companies increasingly investing in AAV-based gene delivery systems and retinal regenerative research

- The demand for advanced therapeutic solutions is growing across pediatric and specialized ophthalmology centers as healthcare systems increasingly prioritize early intervention and long-term vision preservation strategies

- Furthermore, advancements in artificial intelligence-based retinal imaging are improving disease detection accuracy and supporting earlier intervention, strengthening the overall diagnostic ecosystem for rare inherited eye disorders

North America Leber Congenital Amaurosis Market Dynamics

Driver

“Rising Genetic Disease Burden and Expansion of Rare Disease Treatment Ecosystem”

- The increasing prevalence of inherited retinal disorders combined with growing awareness of genetic eye diseases is a major driver accelerating demand in the North America Leber Congenital Amaurosis market

- For instance, expansion of newborn genetic screening programs and early ophthalmic diagnostic initiatives is enabling faster identification of affected patients, improving eligibility for emerging gene therapy treatments

- Increasing regulatory approvals and orphan drug designations for retinal gene therapies are encouraging biotechnology companies to invest heavily in clinical development for Leber Congenital Amaurosis

- Furthermore, strong research funding from public and private organizations is supporting innovation in ocular gene therapy, retinal imaging technologies, and precision diagnostics for rare eye diseases

- The growing availability of specialized treatment centers and increasing collaboration between research institutions and pharmaceutical companies are further driving market expansion in the region

- Rising patient advocacy initiatives and rare disease awareness campaigns are improving early diagnosis rates and encouraging faster treatment adoption across healthcare systems

- In addition, continuous advancements in vector engineering and delivery mechanisms are enhancing the efficacy and safety profile of gene therapies, supporting stronger clinical acceptance

Restraint/Challenge

“High Treatment Cost and Limited Patient Pool Accessibility Barriers”

- Concerns surrounding the extremely high cost of gene therapy treatments and limited reimbursement coverage pose a significant challenge to broader market penetration in the North America Leber Congenital Amaurosis market

- For instance, one-time gene therapies can cost hundreds of thousands of dollars per patient, creating affordability challenges for healthcare systems and limiting widespread adoption despite proven clinical benefits

- The very small patient population associated with rare genetic disorders makes large-scale clinical trials difficult, slowing down drug development timelines and restricting availability of approved treatment options

- Furthermore, limited awareness among primary healthcare providers and delayed referral to genetic specialists can result in late diagnosis, reducing treatment effectiveness and clinical uptake

- While advancements in research are ongoing, overcoming cost barriers, improving insurance coverage, and expanding diagnostic access will be essential for sustained market growth

- Complex regulatory pathways for gene and cell therapies also extend approval timelines, delaying commercialization and limiting early patient access to innovative treatments

- In addition, long-term safety monitoring requirements for gene therapies add operational and financial burdens for developers, further constraining rapid market expansion

North America Leber Congenital Amaurosis Market Scope

The market is segmented on the basis of disease type, type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the North America Leber Congenital Amaurosis market is segmented into infantile type, juvenile type, and other rare genetic variants. The infantile type segment dominated the market with the largest revenue share of 52.6% in 2025, driven by its early-onset manifestation within the first months of life and higher clinical detection rates through pediatric ophthalmic screening programs. This segment benefits significantly from increasing newborn genetic testing and early diagnosis initiatives, which enable timely intervention using gene therapy approaches. Strong clinical awareness among pediatric ophthalmologists and availability of advanced diagnostic tools further support dominance. In addition, most approved and investigational gene therapies target early-onset genetic mutations, reinforcing the strong share of this segment. The high unmet medical need and severe vision impairment associated with infantile LCA also contribute to priority treatment adoption.

The juvenile type segment is expected to witness the fastest growth rate of 5.8% from 2026 to 2033, driven by improved genetic testing access and increasing diagnosis in later childhood stages. Growing awareness among general ophthalmologists and optometrists is leading to earlier identification of milder or delayed-onset cases. Advances in next-generation sequencing are also improving detection of less severe or atypical mutations associated with juvenile presentations. Rising eligibility for gene-based therapies and expanding clinical trials targeting broader age groups are further supporting growth. In addition, increasing patient registries and rare disease screening initiatives are enhancing diagnosis rates across adolescent populations.

- By Type

On the basis of type, the North America Leber Congenital Amaurosis market is segmented into therapy and diagnosis. The therapy segment dominated the market with the largest revenue share of 41.5% in 2025, driven by the rising adoption of gene therapy treatments and strong clinical pipeline activity focused on addressing the root genetic causes of the disease. The availability of approved gene therapies and increasing physician preference for disease-modifying treatment options are key contributors. High treatment costs and limited but expanding reimbursement frameworks also concentrate value within therapeutic interventions. In addition, increasing clinical trial success rates in retinal gene therapy are boosting adoption across specialized ophthalmology centers. Strong investment from biotechnology companies further reinforces dominance of this segment.

The diagnosis segment is expected to witness the fastest growth rate of 6.2% from 2026 to 2033, driven by rapid advancements in genetic testing technologies and increasing use of next-generation sequencing panels. Expanding newborn screening programs and early ophthalmic evaluation protocols are improving early detection rates. Growing integration of artificial intelligence in retinal imaging is also enhancing diagnostic accuracy and speed. Furthermore, rising awareness of rare diseases among healthcare professionals is increasing referral rates for genetic testing. Expanding accessibility of affordable diagnostic tools is further accelerating market growth in this segment.

- By End User

On the basis of end user, the North America Leber Congenital Amaurosis market is segmented into hospitals, specialty clinics, ambulatory surgical centers, home healthcare, and others. The hospitals segment dominated the market with the largest revenue share of 61.3% in 2025, driven by their advanced diagnostic infrastructure, availability of multidisciplinary ophthalmology departments, and access to gene therapy administration facilities. Hospitals are the primary centers for rare disease diagnosis and treatment initiation, especially for complex genetic disorders. The presence of specialized pediatric ophthalmology units further strengthens hospital dominance. In addition, higher patient inflow for genetic testing and clinical trial enrollment contributes to their leading share. Strong reimbursement systems and institutional funding also support hospital-based care delivery.

The specialty clinics segment is expected to witness the fastest growth rate of 6.5% from 2026 to 2033, driven by increasing preference for focused rare disease care and outpatient-based genetic diagnosis. These clinics are rapidly adopting advanced retinal imaging and genetic testing technologies. Growing patient preference for specialized care environments with shorter waiting times is also supporting demand. Increasing collaboration between specialty ophthalmology clinics and biotech firms conducting gene therapy trials is further accelerating growth. In addition, expansion of private ophthalmic networks is improving accessibility to targeted LCA care.

- By Distribution Channel

On the basis of distribution channel, the North America Leber Congenital Amaurosis market is segmented into direct tender and retail sales. The direct tender segment dominated the market with the largest revenue share of 74.8% in 2025, driven by high-cost gene therapies and institutional procurement through hospitals and government-supported healthcare systems. Most approved treatments for Leber Congenital Amaurosis are administered in controlled clinical settings, making direct procurement the preferred channel. Strong involvement of public healthcare programs and insurance-backed reimbursement models further supports this dominance. In addition, centralized purchasing agreements with biotechnology companies ensure streamlined supply of specialized therapies. High regulatory oversight for rare disease drugs also favors direct distribution channels.

The retail sales segment is expected to witness the fastest growth rate of 5.9% from 2026 to 2033, driven by expanding availability of diagnostic kits and supportive ophthalmic care products. Increasing access to at-home genetic testing kits and tele-ophthalmology services is supporting retail expansion. Growing awareness among caregivers and parents regarding early screening tools is also driving demand. In addition, digital health platforms and pharmacy chains are increasingly offering rare disease-related diagnostic support services. Improvements in distribution networks for specialized ophthalmic products are further accelerating growth in this segment.

North America Leber Congenital Amaurosis Market Regional Analysis

- The United States dominated the North America Leber Congenital Amaurosis market with the largest revenue share of 88.2% in 2025, characterized by strong healthcare infrastructure, early adoption of approved gene therapies, and robust presence of leading biotechnology and ophthalmology research companies

- Patients and healthcare providers in the United States highly value early access to advanced gene-based treatments, strong clinical trial participation, and comprehensive insurance coverage for rare disease therapies

- This widespread adoption is further supported by high healthcare expenditure, strong presence of specialized pediatric ophthalmology centers, and increasing investment in retinal gene therapy research, establishing the United States as the key growth hub within the North America Leber Congenital Amaurosis market

The U.S. Leber Congenital Amaurosis Market Insight

The U.S. Leber Congenital Amaurosis market captured the largest revenue share of 88.2% in 2025 within North America, driven by strong adoption of gene therapy, advanced genetic diagnostic capabilities, and a well-established rare disease treatment ecosystem. Patients are increasingly prioritizing early diagnosis and access to innovative, disease-modifying therapies for inherited retinal disorders. The growing focus on precision medicine, combined with rising clinical trial activity for retinal gene therapies, is further propelling market growth. Moreover, the integration of next-generation sequencing, retinal imaging technologies, and FDA support for orphan drug approvals is significantly contributing to market expansion.

Canada Leber Congenital Amaurosis Market Insight

The Canada Leber Congenital Amaurosis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of rare genetic eye disorders and improving access to advanced diagnostic testing. The rise in newborn screening programs and growing emphasis on early detection of inherited retinal diseases are fostering adoption of gene-based therapies. Canadian healthcare institutions are also increasingly participating in global clinical trials, supporting treatment accessibility. Furthermore, government initiatives for rare disease management and expanding reimbursement support are strengthening market growth across both urban and specialty care centers.

Mexico Leber Congenital Amaurosis Market Insight

The Mexico Leber Congenital Amaurosis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improving healthcare infrastructure and increasing awareness of genetic eye disorders. Rising demand for specialized ophthalmic care and gradual expansion of diagnostic capabilities are encouraging early disease identification. In addition, partnerships with global pharmaceutical companies and participation in rare disease programs are supporting market development. However, limited access to advanced gene therapies continues to restrict faster adoption compared to developed countries.

North America Leber Congenital Amaurosis Market Share

The North America Leber Congenital Amaurosis industry is primarily led by well-established companies, including:

- Spark Therapeutics, Inc. (U.S.)

- Novartis AG (Switzerland)

- MeiraGTx Holdings PLC (U.K.)

- Regenxbio Inc. (U.S.)

- Editas Medicine, Inc. (U.S.)

- Atsena Therapeutics, Inc. (U.S.)

- ProQR Therapeutics N.V. (Netherlands)

- Applied Genetic Technologies Corporation (U.S.)

- Orchard Therapeutics PLC (U.K.)

- Sarepta Therapeutics, Inc. (U.S.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Biogen Inc. (U.S.)

- Oxford Biomedica PLC (U.K.)

- GenSight Biologics S.A. (France)

- Sangamo Therapeutics, Inc. (U.S.)

- Krystal Biotech, Inc. (U.S.)

- AvroBio, Inc. (U.S.)

- Opus Genetics, Inc. (U.S.)

What are the Recent Developments in North America Leber Congenital Amaurosis Market?

- In April 2026, scientists behind Luxturna (voretigene neparvovec) were awarded the Breakthrough Prize for developing the first FDA-approved gene therapy for inherited blindness, including Leber Congenital Amaurosis. The therapy has transformed outcomes for patients with RPE65 mutation-linked LCA by restoring functional vision in clinical trials

- In April 2026, clinical updates confirmed that Luxturna remains the first FDA-approved gene therapy for inherited retinal disease, accelerating over 140 retinal gene therapy trials in the U.S. alone. It continues to serve as a benchmark therapy for Leber Congenital Amaurosis and related inherited retinal disorders. This development reinforces North America’s leadership in ocular gene therapy innovation

- In November 2025, Opus Genetics’ LCA5 gene therapy (OPGx-LCA5) was featured on Good Morning America, highlighting early clinical trial success in restoring partial vision in patients with inherited blindness. The investigational AAV-based therapy showed meaningful visual improvements in patients born blind, bringing national attention to ongoing LCA gene therapy breakthroughs in the U.S.

- In October 2025, Sepul Bio (Théa Open Innovation) initiated the first participant dosing in the Phase 3 HYPERION trial of sepofarsen, targeting CEP290-associated Leber Congenital Amaurosis (LCA10). The therapy aims to restore vision by correcting RNA splicing defects responsible for severe retinal degeneration. This marks a major step toward late-stage commercialization of mutation-specific LCA therapies in North America and Europe

- In May 2024, a CRISPR-based gene editing trial (BRILLIANCE study) conducted by Mass Eye and Ear and Editas Medicine reported that patients with inherited retinal blindness—including LCA-related mutations—showed measurable improvements in vision. The Phase 1/2 study demonstrated safety and functional visual gains in most participants, marking a major milestone for mutation-correcting therapies in North America

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.