North America Minimally Invasive Surgery Market

Market Size in USD Billion

USD

25.78 Billion

USD

49.87 Billion

2025

2033

USD

25.78 Billion

USD

49.87 Billion

2025

2033

| 2026 - 2033 | |

| USD 25.78 Billion | |

| USD 49.87 Billion | |

| % | |

|

North America Minimally Invasive Surgery Market Size

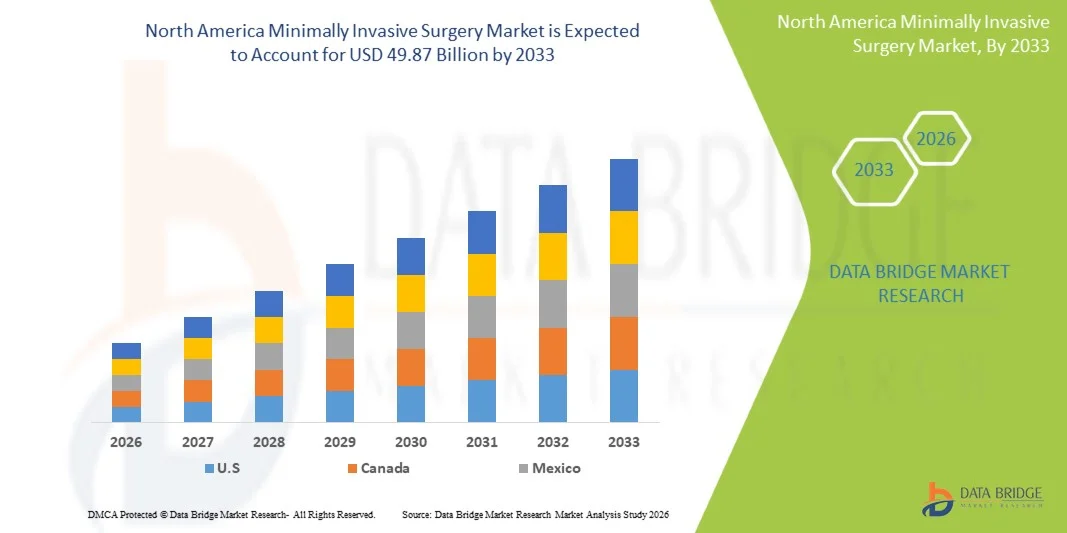

- The North America minimally invasive surgery market size was valued at USD 25.78 billion in 2025 and is expected to reach USD 49.87 billion by 2033, at a CAGR of 8.60% during the forecast period

- The market growth is primarily driven by technological advancements in surgical instruments, rising adoption of robotic-assisted surgeries, and increasing preference for minimally invasive procedures due to reduced recovery time and lower risk of complications

- Moreover, growing awareness among patients, favorable reimbursement policies, and rising demand for outpatient surgical procedures are contributing to the expansion of minimally invasive surgeries across hospitals and specialty clinics in the region. These factors collectively are accelerating the adoption of MIS solutions, thereby significantly boosting the industry's growth

North America Minimally Invasive Surgery Market Analysis

- North America Minimally Invasive Surgery, encompassing procedures performed through small incisions using specialized instruments, endoscopes, and robotic systems, is increasingly becoming a standard in both hospitals and outpatient surgical centers due to faster patient recovery, reduced risk of complications, and enhanced surgical precision

- The escalating demand for minimally invasive surgery is primarily fueled by technological advancements in surgical robotics, endoscopic devices, and energy-based instruments, along with rising patient awareness and a growing preference for outpatient and same-day procedures

- The United States dominated the North America minimally invasive surgery market with the largest revenue share of 78.7% in 2025, characterized by early adoption of advanced surgical technologies, high healthcare expenditure, and a strong presence of key medical device players, with robotic-assisted and laparoscopic procedures experiencing substantial growth, driven by innovations from both established medical companies and startups focusing on AI-enabled surgical tools

- Canada is witnessing steady growth in the North America minimally invasive surgery market supported by increasing healthcare investments, government initiatives promoting minimally invasive procedures, and growing patient preference for less invasive surgeries

- The laparoscopy surgery segment dominated the North America minimally invasive surgery market with a market share of 45.9% in 2025, driven by its proven clinical efficacy, cost-effectiveness, and broad applicability across general, gynecologic, and urologic procedures

Report Scope and North America Minimally Invasive Surgery Market Segmentation

|

Attributes |

North America Minimally Invasive Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Minimally Invasive Surgery Market Trends

“Growing Adoption of Robotic-Assisted and AI-Enabled Surgical Systems”

- A significant and accelerating trend in the North America minimally invasive surgery market is the increasing adoption of robotic-assisted surgical systems and AI-enabled planning tools, enhancing surgical precision and procedural efficiency

- For instance, the da Vinci Surgical System integrates robotic arms with AI-assisted motion scaling, allowing surgeons to perform complex laparoscopic procedures with greater accuracy and control

- AI integration in MIS enables features such as predictive surgical planning, instrument trajectory optimization, and real-time analytics, improving patient outcomes and reducing operative time. For instance, some Medtronic robotic platforms use AI to provide real-time feedback on tissue handling and instrument positioning

- The integration of MIS with digital imaging, navigation systems, and AI platforms facilitates centralized surgical planning and monitoring, enabling coordinated workflows in operating rooms

- This trend towards intelligent, precise, and technology-driven surgical systems is fundamentally reshaping expectations for hospital performance and patient care. Consequently, companies such as Intuitive Surgical and Medtronic are developing AI-enabled robotic platforms with enhanced visualization, haptic feedback, and procedural automation

- The demand for robotic-assisted and AI-integrated MIS solutions is growing rapidly across hospitals and specialty surgical centers, as healthcare providers increasingly prioritize precision, efficiency, and improved patient recovery

- Collaborations between medical device manufacturers and software developers to enhance MIS workflow and integrate real-time analytics into surgical procedures are further accelerating innovation

North America Minimally Invasive Surgery Market Dynamics

Driver

“Increasing Preference for Minimally Invasive Procedures and Advanced Surgical Technologies”

- The growing awareness of patient benefits such as reduced recovery time, lower complication risks, and shorter hospital stays is a major driver for the adoption of MIS procedures

- For instance, in March 2025, Intuitive Surgical reported increased adoption of da Vinci systems across U.S. hospitals, highlighting growing demand for robotic-assisted surgeries

- Rising investments in surgical robotics, advanced endoscopic devices, and energy-based instruments are enabling healthcare providers to offer precise and efficient MIS procedures

- Furthermore, favorable reimbursement policies for minimally invasive procedures and rising patient preference for outpatient surgeries are making MIS solutions a preferred choice for hospitals and surgical centers

- The increasing availability of AI-enabled planning tools, training simulators, and user-friendly robotic systems further propels adoption, enabling surgeons to expand their capabilities while improving surgical outcomes

- Growing geriatric populations and increasing prevalence of chronic diseases are driving demand for MIS procedures that reduce surgical trauma and improve post-operative recovery

- Expansion of MIS training programs and simulation centers for surgeons is supporting faster adoption and broader deployment across hospitals and specialty clinics

Restraint/Challenge

“High Costs and Regulatory Compliance Barriers”

- The high initial investment required for robotic-assisted and AI-integrated MIS systems poses a significant challenge to broader market penetration, particularly for smaller hospitals and clinics

- For instance, high costs of da Vinci and Medtronic platforms can delay adoption in budget-constrained facilities despite clear clinical advantages

- Regulatory requirements for device approval, clinical validation, and safety compliance add complexity and time to market entry for new MIS technologies, limiting rapid deployment

- In addition, the steep learning curve for surgeons and the need for specialized training can slow the adoption of advanced MIS platforms

- Overcoming these challenges through cost optimization, leasing/rental models, surgeon training programs, and streamlined regulatory processes will be crucial for sustained growth in the North America minimally invasive surgery market

- Limited access to advanced MIS systems in rural and low-resource hospitals can restrict market growth despite rising overall demand

- Potential technical failures or complications during robotic-assisted procedures may increase hesitancy among healthcare providers, emphasizing the need for robust support and maintenance services

North America Minimally Invasive Surgery Market Scope

The market is segmented on the basis of product type, application, technology, and end users.

- By Product Type

On the basis of product type, the North America minimally invasive surgery market is segmented into surgical devices, monitoring & visualization systems, laparoscopy devices, endosurgical equipment, and electrosurgical equipment. The Surgical Devices segment dominated the market with the largest revenue share in 2025, driven by their wide usage in multiple minimally invasive procedures such as laparoscopic, thoracic, and urologic surgeries. Surgical devices such as trocars, graspers, and staplers are critical for precise tissue handling and procedural efficiency. Hospitals and specialty surgical centers prioritize surgical devices for their reliability, clinical effectiveness, and compatibility with robotic-assisted systems. The market demand is further supported by continuous innovations that improve ergonomics and functionality. In addition, surgical devices are essential for both routine and complex MIS procedures, making them a core revenue driver for manufacturers. Their integration with AI-enabled platforms and robotic systems enhances surgical accuracy, boosting adoption across healthcare facilities.

The Monitoring & Visualization Systems segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by increasing adoption of high-definition endoscopy, 3D imaging, and real-time patient monitoring tools. These systems provide surgeons with enhanced visibility during complex procedures, improving precision and reducing complications. Advances in imaging technology and augmented reality integration are expanding their applications across gastrointestinal, gynecology, and thoracic surgeries. Hospitals increasingly rely on these systems to support robotic-assisted procedures, providing real-time analytics and intraoperative guidance. The rising need for minimally invasive solutions with reduced operative risk further drives demand. Moreover, integration with AI platforms enables predictive insights and workflow optimization, making monitoring and visualization systems indispensable in modern MIS operating rooms.

- By Application

On the basis of application, the North America minimally invasive surgery market is segmented into gastrointestinal surgery, gynecology surgery, urology surgery, cosmetic surgery, thoracic surgery, vascular surgery, orthopedic & spine surgery, bariatric surgery, breast surgery, cardiac surgery, adrenalectomy surgery, anti-reflux surgery, cancer surgery, cholecystectomy surgery, colectomy surgery, colon & rectal surgery, ear, nose & throat surgery, and obesity surgery. The Gynecology Surgery segment dominated the market with the largest revenue share in 2025, driven by the high prevalence of uterine fibroids, endometriosis, and ovarian disorders requiring minimally invasive intervention. Laparoscopic and robotic-assisted procedures have become standard in gynecology due to faster recovery, minimal scarring, and reduced hospitalization. The segment benefits from strong hospital adoption and favorable reimbursement policies for outpatient procedures. Surgeons prefer MIS approaches in gynecology for their precision and lower complication rates compared to open surgeries. In addition, patient awareness and demand for less invasive options further propel adoption. Continuous innovation in gynecological surgical instruments and visualization systems reinforces its dominance in the market.

The Bariatric Surgery segment is expected to witness the fastest growth from 2026 to 2033, driven by rising obesity rates and increasing demand for weight-loss surgeries such as gastric bypass, sleeve gastrectomy, and adjustable gastric banding. Hospitals and specialized clinics are expanding minimally invasive bariatric programs to meet patient demand. Robotic-assisted and laparoscopic procedures are preferred due to reduced recovery times and better post-operative outcomes. Technological advancements in stapling devices and energy-based instruments enhance procedural safety and efficiency. The growing emphasis on outpatient bariatric procedures is also contributing to segment growth. In addition, patient preference for minimally invasive approaches with reduced surgical trauma continues to drive adoption in this application.

- By Technology

On the basis of technology, the North America minimally invasive surgery market is segmented into transcatheter surgery, laparoscopy surgery, non-visual imaging, and medical robotics. The Laparoscopy Surgery segment dominated the market with the largest revenue share of 45.9% in 2025, driven by its established use across general, urology, gynecology, and gastrointestinal procedures. Laparoscopic surgery offers significant advantages such as smaller incisions, faster recovery, and lower risk of infection. Hospitals widely adopt laparoscopy due to its proven clinical efficacy and cost-effectiveness compared to open surgery. The availability of advanced laparoscopic instruments, high-definition cameras, and AI-enabled guidance systems further enhances its adoption. Surgeons prefer laparoscopic techniques for their precision, reliability, and versatility across multiple procedures. Continuous technological upgrades and compatibility with robotic systems strengthen its dominance in the market.

The Medical Robotics segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing adoption of robotic-assisted platforms in hospitals and specialty surgical centers. Robotics enhances precision, reduces surgeon fatigue, and enables complex procedures to be performed minimally invasively. Integration with AI, imaging, and navigation systems allows for real-time guidance and improved surgical outcomes. The trend is particularly strong in urology, gynecology, and cardiac procedures. Rising investment in robotic platforms and training programs supports rapid adoption. Furthermore, patient demand for reduced recovery time and minimally invasive approaches accelerates growth in this segment.

- By End Users

On the basis of end users, the North America minimally invasive surgery market is segmented into hospital surgical departments, outpatient surgery patients, group practices, and individual surgeons. The Hospital Surgical Departments segment dominated the market with the largest revenue share in 2025, driven by the high volume of minimally invasive procedures performed in hospital settings. Hospitals invest in advanced MIS devices, robotic systems, and visualization platforms to improve surgical outcomes and operational efficiency. The segment benefits from trained surgical teams, established infrastructure, and access to specialized technologies. In addition, hospital adoption is supported by reimbursement policies and patient preference for minimally invasive procedures with faster recovery. Hospitals also serve as key centers for clinical trials and adoption of new surgical innovations, reinforcing dominance. Continuous collaboration between hospitals and medical device manufacturers ensures timely access to advanced MIS solutions.

The Outpatient Surgery Patients segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising demand for same-day procedures and minimally invasive options that reduce hospital stays. Outpatient surgical centers are increasingly equipped with advanced laparoscopic, robotic, and endoscopic technologies. Growing patient awareness, convenience, and cost savings drive the preference for outpatient MIS procedures. Integration of AI-guided planning and telemonitoring solutions enhances patient safety and procedural efficiency. Expansion of outpatient centers in urban and semi-urban regions further supports segment growth. In addition, insurance coverage and favorable reimbursement policies for outpatient procedures accelerate adoption among patients.

North America Minimally Invasive Surgery Market Regional Analysis

- The United States dominated the North America minimally invasive surgery market with the largest revenue share of 78.7% in 2025, characterized by early adoption of advanced surgical technologies, high healthcare expenditure, and a strong presence of key medical device

- Hospitals and surgical centers in the region prioritize robotic-assisted, laparoscopic, and AI-enabled surgical systems due to their proven clinical efficacy, faster recovery times, and reduced risk of complications

- This widespread adoption is further supported by favorable reimbursement policies, extensive healthcare infrastructure, and the presence of leading medical device manufacturers, establishing minimally invasive surgery as a preferred approach across general, gynecology, urology, and specialty surgical procedures

The U.S. Minimally Invasive Surgery Market Insight

The U.S. minimally invasive surgery market captured the largest revenue share of 78.7% in 2025, fueled by early adoption of advanced surgical technologies and increasing patient preference for minimally invasive procedures. Hospitals and specialty surgical centers are investing heavily in robotic-assisted, laparoscopic, and AI-enabled systems to improve surgical precision and reduce recovery times. The growing trend of outpatient and same-day surgeries is further propelling market growth. Moreover, the integration of AI-assisted planning and real-time monitoring in MIS procedures is enhancing procedural efficiency. The rising prevalence of chronic diseases and complex surgical cases is also driving demand. Government support and favorable reimbursement policies strengthen adoption across healthcare facilities.

Canada Minimally Invasive Surgery Market Insight

The Canada minimally invasive surgery market accounted for a market share of 15% in 2025, driven by growing healthcare infrastructure and government initiatives supporting minimally invasive procedures. Hospitals are increasingly implementing robotic-assisted and laparoscopic systems to enhance surgical outcomes and reduce hospital stays. Patient awareness of reduced postoperative complications and faster recovery is further boosting adoption. The market benefits from advanced training programs for surgeons and growing investments in AI-assisted surgical technologies. Private and public hospitals are expanding MIS capabilities across gastrointestinal, urology, and gynecology procedures. The integration of MIS systems with digital imaging and navigation tools is becoming increasingly prevalent in clinical practice.

Mexico Minimally Invasive Surgery Market Insight

The Mexico minimally invasive surgery market held a market share of 7% in 2025, driven by gradual adoption of minimally invasive procedures across private hospitals and specialty clinics. Rising surgical volumes and awareness of patient benefits, such as reduced scarring and shorter recovery, are fueling demand. Hospitals are investing in endoscopic and laparoscopic devices, while robotic-assisted systems are being introduced in urban healthcare centers. Growing partnerships between medical device manufacturers and healthcare providers support the deployment of advanced MIS technologies. Increased access to training programs for surgeons and favorable healthcare policies are further enhancing adoption. The market is expected to grow steadily as urban healthcare infrastructure expands and more patients seek outpatient MIS procedures.

North America Minimally Invasive Surgery Market Share

The North America Minimally Invasive Surgery industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Olympus Corporation (Japan)

- Siemens Healthineers AG (Germany)

- GE Healthcare (U.S.)

- Abbott (U.S.)

- Intuitive Surgical (U.S.)

- Smith & Nephew (U.K.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Boston Scientific Corporation (U.S.)

- Cook (U.S.)

- B. Braun SE (Germany)

- CONMED Corporation (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Renishaw plc (U.K.)

- Distalmotion (Switzerland)

- CMR Surgical (U.K.)

- Think Surgical (U.S.)

What are the Recent Developments in North America Minimally Invasive Surgery Market?

- In October 2025, Zimmer Biomet completed the acquisition of Monogram Technologies, adding semi‑autonomous and fully autonomous robotic surgical technologies (including an FDA‑cleared CT‑based TKA robot) to its robotics portfolio and signaling strategic expansion in AI‑powered MIS solutions

- In July 2025, Moon Surgical’s Maestro Platform, an MIS robotic solution with “Physical AI,” received FDA 510(k) clearance along with enhanced connectivity (Wi‑Fi/5G) and cloud‑based insights, showcasing innovation in collaborative and cost‑effective MIS robotics

- In May 2025, Intuitive Surgical announced FDA clearance for its da Vinci Single Port system for additional minimally invasive indications, expanding the robotic platform’s procedural capabilities and supporting broader adoption of single‑port robotic surgery

- In March 2025, surgeons at Baylor St. Luke’s Medical Center in Houston performed the first fully robotic heart transplant in the United States, using a minimally invasive technique with robotic systems through small incisions, reducing infection risks and recovery time compared to traditional open procedures

- In March 2024, Intuitive Surgical’s da Vinci 5 robotic surgical system received 510(k) clearance from the U.S. FDA, marking a significant product advancement for multiport robotic‑assisted minimally invasive surgeries with enhanced precision and new features

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.