North America Non Hodgkin Lymphoma Diagnostics Market

Market Size in USD Billion

USD

2.34 Billion

USD

4.69 Billion

2024

2032

USD

2.34 Billion

USD

4.69 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.34 Billion | |

| USD 4.69 Billion | |

| % | |

|

North America Non-Hodgkin Lymphoma Diagnostics Market Size

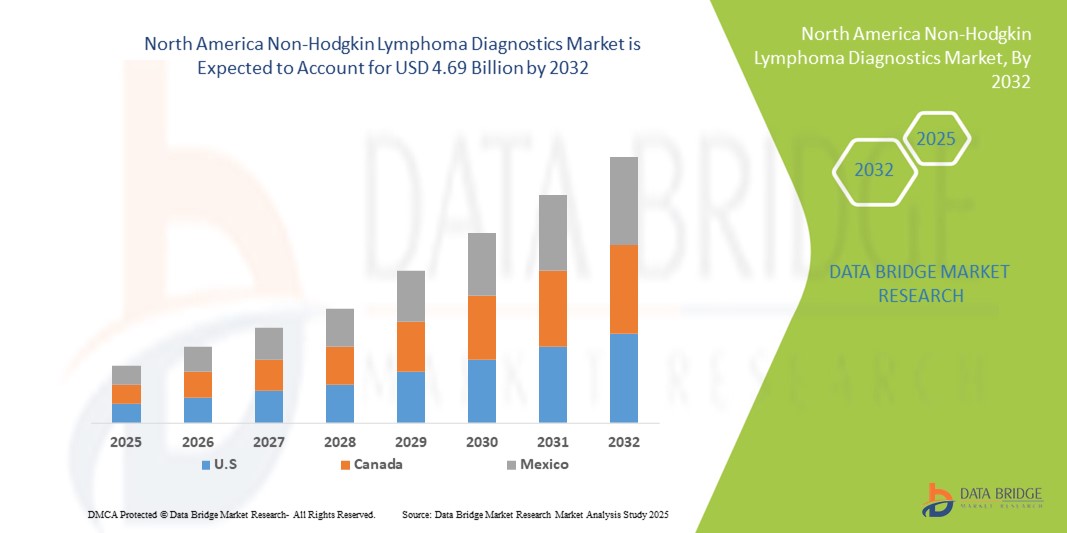

- The North America non-Hodgkin lymphoma diagnostics market size was valued at USD 2.34 billion in 2024 and is expected to reach USD 4.69 billion by 2032, at a CAGR of 9.10% during the forecast period

- The market growth is primarily driven by increasing prevalence of Non-Hodgkin Lymphoma (NHL) worldwide and the rising demand for early and accurate diagnostic solutions. Advanced diagnostic technologies, such as flow cytometry, immunohistochemistry, and molecular profiling, are playing a critical role in improving disease detection and patient outcomes

- Furthermore, growing awareness among healthcare professionals and patients regarding personalized treatment plans and precision medicine is boosting adoption of innovative diagnostic solutions. Continuous advancements in laboratory automation, high-throughput testing, and integration with clinical decision support systems are enhancing efficiency and accuracy in NHL diagnostics

North America Non-Hodgkin Lymphoma Diagnostics Market Analysis

- The non-hodgkin lymphoma diagnostics market is witnessing rapid growth due to increasing awareness of early cancer detection, technological advancements in diagnostic tools, and rising adoption of precision medicine approaches

- The escalating demand for non-Hodgkin lymphoma diagnostics is primarily fueled by growing healthcare spending, rising incidence of hematologic cancers, and increasing adoption of AI-enabled and next-generation diagnostic technologies

- U.S. dominated the non-Hodgkin lymphoma diagnostics market with the largest revenue share of 78.6% in 2025, characterized by high healthcare expenditure, advanced medical infrastructure, and a strong presence of key industry players, with substantial growth in diagnostic installations driven by innovations from both established companies and startups focusing on AI-enabled screening and precision diagnostics

- Canada is also expected to be the fastest-growing country in the non-Hodgkin lymphoma diagnostics market during the forecast period due to rising awareness of early diagnosis, increasing availability of advanced diagnostic tests, and expanding healthcare access

- The aggressive lymphoma segment dominated the non-Hodgkin lymphoma diagnostics market with a share of 57.2% in 2025, due to the urgent need for rapid and accurate diagnostics in fast-progressing cases. Aggressive lymphomas require intensive monitoring and precise molecular characterization to guide immediate treatment decisions

Report Scope and Non-Hodgkin Lymphoma Diagnostics Market Segmentation

|

Attributes |

Non-Hodgkin Lymphoma Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Non-Hodgkin Lymphoma Diagnostics Market Trends

Advancements in Non-Hodgkin Lymphoma Diagnostics

- A significant trend in the U.S. non-Hodgkin lymphoma diagnostics market is the increasing adoption of advanced diagnostic technologies, including flow cytometry, immunohistochemistry, and next-generation sequencing (NGS), which are improving accuracy and enabling earlier detection of the disease

- For instance, modern flow cytometry platforms can rapidly identify and classify lymphoma subtypes, allowing clinicians to design more precise treatment plans. Similarly, NGS-based diagnostics provide comprehensive genetic profiling, supporting personalized therapy approaches

- Integration of automated laboratory systems and advanced diagnostic workflows enables faster turnaround times, reduces human error, and enhances overall laboratory efficiency

- These technological advancements facilitate centralized patient data management, allowing healthcare providers to track disease progression, monitor treatment response, and make informed decisions through streamlined diagnostic processes

- The trend towards more precise, rapid, and reliable diagnostics is fundamentally transforming clinical practices and patient management in Non-Hodgkin Lymphoma care. Consequently, companies are investing in innovative diagnostic solutions, expanding test availability, and improving accessibility for healthcare providers

- The demand for advanced non-Hodgkin lymphoma diagnostics is growing rapidly in the U.S., as healthcare systems focus on early detection, accurate classification, and personalized treatment approaches to improve patient outcomes

North America Non-Hodgkin Lymphoma Diagnostics Market Dynamics

Driver

Growing Need Due to Rising Awareness and Early Detection Initiatives

- The increasing prevalence of hematologic cancers, coupled with growing awareness of early detection benefits, is a significant driver for the heightened demand for Non-Hodgkin Lymphoma Diagnostics

- For instance, in April 2024, leading diagnostic companies introduced advanced flow cytometry and next-generation sequencing platforms aimed at improving early detection and precise classification of Non-Hodgkin Lymphoma. Such innovations by key players are expected to drive market growth in the forecast period

- As patients and healthcare providers become more aware of the importance of early diagnosis and tailored treatment plans, advanced diagnostic solutions offer higher accuracy, rapid results, and comprehensive disease profiling, providing a compelling upgrade over traditional diagnostic methods

- Furthermore, the growing emphasis on personalized medicine and precision oncology is increasing the adoption of integrated diagnostic platforms that enable seamless testing, monitoring, and reporting within clinical workflows

- The convenience of faster turnaround times, minimally invasive testing options, and improved accessibility to specialized diagnostics are key factors propelling the adoption of Non-Hodgkin Lymphoma Diagnostics across hospitals, diagnostic labs, and specialized clinics. The trend towards centralized and automated laboratory solutions further contributes to market growth

Restraint/Challenge

Concerns Regarding High Costs and Limited Accessibility

- The high initial cost of advanced non-Hodgkin lymphoma diagnostics systems, including flow cytometry and NGS platforms, poses a significant challenge to broader market penetration, particularly for smaller clinics or budget-conscious healthcare providers

- For instance, while some diagnostic tests have become more affordable through innovations in automation and reagent efficiency, premium features such as multi-parameter analysis or rapid genetic profiling often come with higher costs, which can limit adoption in resource-constrained settings

- Addressing these challenges through cost-effective solutions, partnerships with healthcare institutions, and wider insurance coverage is crucial for expanding market access. Companies are increasingly offering scalable and modular diagnostic platforms to accommodate diverse healthcare facility sizes

- While prices are gradually decreasing due to technological advancements and competition, the perceived high cost of advanced diagnostics can still hinder widespread adoption, particularly in smaller hospitals or emerging healthcare markets

- Overcoming these challenges through improved affordability, patient education on the benefits of early detection, and enhanced availability of diagnostic services will be vital for sustained market growth

North America Non-Hodgkin Lymphoma Diagnostics Market Scope

The market is segmented on the basis of test type, cancer stage, tumor type, product, technology, application, end user, and distribution channel.

- By Test Type

On the basis of test type, the North America non-Hodgkin lymphoma diagnostics market is segmented into imaging, biopsy, immunohistochemistry, biomarker, genetic test, cytogenetics, lumbar puncture, blood test, cytochemistry, and others. The biopsy segment dominated the market with the largest revenue share of 38.5% in 2025, driven by its high diagnostic accuracy and ability to provide definitive histopathological confirmation of lymphoma subtypes. Hospitals and diagnostic centers widely adopt biopsy procedures due to their reliability and established clinical trust. Technological advancements such as automated tissue processing and high-resolution imaging have further enhanced result accuracy and workflow efficiency. Biopsy testing plays a key role in guiding personalized treatment plans and monitoring therapeutic response. Integration with molecular profiling and immunohistochemistry strengthens its utility for precision oncology. The segment’s dominance is supported by consistent adoption across major hospitals and specialized cancer centers, making it the preferred standard for diagnosing Non-Hodgkin Lymphoma.

The biomarker segment is anticipated to witness the fastest growth rate with a CAGR of 22.0% from 2025 to 2032, fueled by increasing demand for early detection and therapy monitoring. Biomarker tests enable precise patient stratification and guide personalized treatment approaches. Expansion of molecular assay capabilities and high-throughput testing platforms accelerates adoption in both hospitals and specialized diagnostic labs. Clinician awareness of biomarker importance and regulatory approvals further support market growth. These tests also facilitate integration with next-generation sequencing and other molecular diagnostics. Research initiatives and clinical trials increasingly incorporate biomarker testing, driving further adoption. Continuous innovation in assay sensitivity and specificity ensures rapid market expansion.

- By Cancer Stage

On the basis of cancer stage, the North America non-Hodgkin lymphoma diagnostics market is segmented into Stage IV, Stage III, Stage II, Stage I, and Stage 0. The Stage II segment dominated the market with a share of 35.8% in 2025, supported by standardized diagnostic protocols for patients diagnosed at intermediate stages. Stage II testing helps clinicians optimize treatment intensity while minimizing adverse effects. Diagnostic procedures for this stage are widely adopted across hospitals and outpatient centers for monitoring disease progression and planning combination therapies. Stage II diagnostics integrate well with molecular and imaging studies, improving diagnostic confidence. Early intervention at this stage significantly improves patient prognosis. The segment benefits from high patient volumes and established workflows, reinforcing its leadership. Clinicians rely on Stage II diagnostics to guide both immediate treatment and long-term disease management.

The Stage IV segment is expected to witness the fastest growth rate with a CAGR of 19.5% from 2025 to 2032, driven by the need for comprehensive monitoring of advanced-stage patients. Stage IV diagnostics require complex, multi-modal testing, including imaging, molecular profiling, and genetic analysis. Hospitals and specialized cancer centers increasingly adopt these high-precision techniques to track disease progression and therapeutic response. Rising incidence of late-stage diagnoses and the demand for personalized treatment strategies further fuel growth. Technological advancements and improved accessibility to advanced diagnostics support rapid adoption. Stage IV testing remains a critical focus area for oncology care.

- By Tumor Type

On the basis of tumor type, the North America non-Hodgkin lymphoma diagnostics market is segmented into aggressive lymphomas and indolent lymphomas. The aggressive lymphoma segment dominated the market with a share of 57.2% in 2025, due to the urgent need for rapid and accurate diagnostics in fast-progressing cases. Aggressive lymphomas require intensive monitoring and precise molecular characterization to guide immediate treatment decisions. Hospitals and cancer centers prioritize these high-risk patients, ensuring adoption of advanced testing methods. Rapid identification of aggressive subtypes allows oncologists to tailor intensive therapies and monitor therapeutic outcomes. The prevalence of aggressive lymphomas in North America, coupled with clinical urgency, drives consistent demand. Established diagnostic workflows and integration with molecular profiling strengthen the segment’s dominance. Research initiatives focusing on aggressive lymphoma detection further reinforce its market leadership.

The indolent lymphoma segment is expected to witness the fastest CAGR of 17.8% from 2025 to 2032, driven by growing demand for long-term monitoring and minimally invasive testing. Indolent lymphoma diagnostics emphasize biomarker-based and genetic tests to track disease progression over time. Hospitals, outpatient clinics, and specialized labs increasingly adopt these diagnostics for early detection and personalized care. The segment benefits from increasing awareness among clinicians of the importance of ongoing patient monitoring. Technological innovations in molecular and immunohistochemical assays support improved diagnostic accuracy. Research studies and clinical trials targeting indolent lymphomas further stimulate growth. Rising adoption in precision oncology programs accelerates market expansion for this segment.

- By Product

On the basis of product, the North America non-Hodgkin lymphoma diagnostics market is segmented into instrument-based products, platform-based products, kits and reagents, and other consumables. The kits and reagents segment dominated the market with a share of 42.0% in 2025, driven by recurring demand in hospitals and diagnostic laboratories for standardized, ready-to-use solutions. Kits enable faster processing times, minimize operator variability, and ensure consistent results across multiple testing sites. They support a wide range of diagnostic applications, including biopsy, molecular, and biomarker testing. Hospitals and research institutes rely on high-quality kits for both routine diagnostics and clinical studies. Increasing adoption of molecular diagnostics and immunohistochemistry further boosts demand. Kits and reagents offer ease of storage, reliability, and compatibility with multiple instruments, reinforcing market dominance. Availability from established suppliers enhances procurement efficiency for large healthcare facilities.

The platform-based products segment is expected to witness the fastest CAGR of 20.2% from 2025 to 2032, as integrated systems combine multiple diagnostic capabilities into single automated workflows. Platform solutions streamline laboratory processes, reduce manual intervention, and support high-throughput testing. Hospitals and diagnostic centers increasingly prefer platforms for scalability, efficiency, and ease of use. Integration with molecular and imaging modules enables comprehensive analysis from a single system. The segment benefits from innovations in automation, software analytics, and modular design. Growing adoption in academic and research institutes further accelerates growth. Platform-based diagnostics also support multi-test connectivity, improving overall lab productivity.

- By Technology

On the basis of technology, the North America non-Hodgkin lymphoma diagnostics market is segmented into fluorescent in situ hybridization (FISH), next-generation sequencing (NGS), fluorimmunoassay, comparative genomic hybridization, immunohistochemical, and others. The next-generation sequencing (NGS) segment dominated the market with a share of 40.5% in 2025, due to its comprehensive genetic profiling capabilities and critical role in precision oncology. NGS allows detection of multiple mutations simultaneously, facilitating patient stratification and therapy selection. Hospitals and cancer centers widely adopt NGS for its high sensitivity, scalability, and compatibility with biomarker studies. Integration with biopsy and molecular diagnostics enhances clinical utility. Ongoing research and clinical trials increase demand for high-throughput NGS platforms. The segment is further supported by regulatory approvals and growing adoption in routine oncology workflows.

The fluorescent in situ hybridization (FISH) segment is expected to witness the fastest CAGR of 18.7% from 2025 to 2032, driven by its ability to rapidly detect genetic abnormalities and chromosomal translocations. FISH is essential for early diagnosis, prognosis evaluation, and treatment planning. Adoption is increasing in hospitals, diagnostic labs, and specialized research centers. Technological enhancements in probe design and imaging systems improve accuracy and turnaround times. FISH testing complements other molecular diagnostics for comprehensive patient evaluation. Rising awareness of its diagnostic value in hematologic malignancies drives market growth. Expanding clinical applications further support rapid adoption.

- By Application

On the basis of application, the North America non-Hodgkin lymphoma diagnostics market is segmented into screening, diagnostic and predictive, prognostic, and research. The diagnostic and predictive segment dominated the North America Non-Hodgkin Lymphoma Diagnostics market with a share of 45.3% in 2025, driven by the growing need for accurate disease classification and therapy guidance. Diagnostic and predictive tests combine molecular, genetic, and imaging data to provide clinicians with comprehensive insights into disease progression and patient prognosis. Hospitals and specialized diagnostic centers rely heavily on these tests to support treatment planning and clinical decision-making. The segment benefits from integration with personalized medicine programs, enabling tailored therapeutic strategies. Ongoing research and clinical validation of predictive biomarkers further reinforce its market dominance. Its established clinical utility and widespread adoption in oncology centers maintain its leadership. The increasing complexity of treatment protocols and the need for early identification of high-risk patients further cement this segment’s strong position in North America.

The screening segment is expected to witness the fastest CAGR of 19.0% from 2025 to 2032, fueled by rising awareness of early detection and preventive healthcare initiatives. Screening tests facilitate timely diagnosis, helping clinicians initiate treatment before disease progression. Outpatient diagnostic centers and hospitals increasingly adopt screening programs for high-risk populations. Advances in biomarker assays, imaging technologies, and minimally invasive techniques enhance test accuracy and patient comfort. Government initiatives and insurance coverage programs supporting early detection further drive adoption. Technological innovations reduce turnaround times and operational costs, enabling broader deployment. The segment also benefits from growing educational campaigns targeting physicians and patients. Expansion of screening programs in both clinical and research settings is expected to accelerate market growth significantly over the forecast period.

- By End User

On the basis of end user, the North America non-Hodgkin lymphoma diagnostics market is segmented into hospitals, diagnostic centers, cancer research centers, academic institutes, ambulatory surgical centers, and others. The hospitals segment dominated the market with a share of 50.0% in 2025, due to their capability to manage complex diagnostic workflows, access to advanced instrumentation, and availability of specialized staff. Hospitals offer integrated services from initial testing to treatment monitoring, ensuring continuity of care for Non-Hodgkin Lymphoma patients. Multidisciplinary oncology teams rely on hospital-based diagnostics to guide therapeutic decisions and monitor patient response. Hospitals also invest in high-throughput platforms and molecular testing capabilities to handle large patient volumes efficiently. The segment benefits from well-established procurement channels and long-term supplier relationships. Additionally, hospitals participate in clinical trials and research initiatives, further strengthening the segment’s leadership. Their centralized infrastructure, regulatory compliance, and advanced laboratory networks reinforce dominance in the North America market.

The diagnostic centers segment is expected to witness the fastest CAGR of 21.5% from 2025 to 2032, driven by the expansion of specialized outpatient testing facilities offering rapid and cost-effective diagnostics. Diagnostic centers provide flexibility for patients seeking convenient and timely testing without hospitalization. The increasing adoption of biomarker-based and molecular diagnostic tests in these centers supports growth. Investments in automation and advanced laboratory equipment enhance efficiency and result accuracy. Partnerships with hospitals and academic institutes help expand service offerings. Patient awareness campaigns and referral programs from healthcare providers further boost adoption. Regulatory support and insurance coverage improvements accelerate utilization. The growth of diagnostic centers is also fueled by increasing focus on preventive healthcare and early detection initiatives across North America.

- By Distribution Channel

On the basis of distribution channel, the North America non-Hodgkin lymphoma diagnostics market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the North America Non-Hodgkin Lymphoma Diagnostics market with a share of 46.8% in 2025, supported by bulk procurement by hospitals, government institutions, and large diagnostic networks. Direct tender agreements enable long-term contracts, predictable supply, and cost efficiency, ensuring continuity of diagnostic services. Hospitals and cancer centers rely on direct tender to secure high-quality instruments, reagents, and consumables. These agreements also include technical support, training, and maintenance, enhancing reliability for end users. Suppliers benefit from stable revenue streams and stronger relationships with key clients. The segment’s dominance is reinforced by the growing adoption of integrated diagnostic platforms and advanced laboratory systems. Efficient supply chain management and streamlined procurement processes further strengthen the leadership of direct tender distribution in North America.

The retail sales segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, driven by the increasing availability of ready-to-use diagnostic kits, reagents, and consumables through commercial distributors. Retail channels provide access to smaller laboratories, academic institutes, and outpatient clinics that may not participate in bulk tender agreements. Easy availability, competitive pricing, and product variety make retail distribution an attractive option for end users. Technological innovations in packaging, shelf-life extension, and pre-validated kits enhance adoption. Awareness campaigns targeting smaller healthcare facilities further drive growth. Retail channels also support rapid deployment of new diagnostic technologies and reagents, expanding market reach. Growing online and offline distribution networks accelerate accessibility across North America, contributing to rapid expansion of this segment.

North America Non-Hodgkin Lymphoma Diagnostics Market Regional Analysis

- North America dominated the non-Hodgkin lymphoma diagnostics market with the largest revenue share in 2025, driven by high healthcare expenditure, advanced medical infrastructure, and a strong presence of leading diagnostic service providers

- The region benefits from widespread adoption of AI-enabled screening, precision diagnostics, and innovative testing platforms, enabling early detection and personalized patient management

- Continuous R&D, increasing collaborations between established companies and startups, and growing awareness about lymphoma screening further support market growth

U.S. Non-Hodgkin Lymphoma Diagnostics Market Insight

The U.S. non-Hodgkin lymphoma diagnostics market captured the largest share of 78.6% within North America in 2025, fueled by rapid adoption of advanced molecular, genetic, and immunohistochemistry-based diagnostic solutions. The country’s high healthcare expenditure, robust medical infrastructure, and strong focus on early cancer detection support widespread implementation of precision diagnostics. Innovations from both established companies and startups, including AI-driven tools and high-throughput testing platforms, are driving substantial growth. The integration of advanced diagnostic workflows in hospitals, research centers, and clinical laboratories further strengthens the U.S. position as the dominant market in the region.

Canada Non-Hodgkin Lymphoma Diagnostics Market Insight

The Canada non-Hodgkin lymphoma diagnostics market is expected to be the fastest-growing country in the Non-Hodgkin Lymphoma Diagnostics market during the forecast period, projected to expand at a robust CAGR due to increasing awareness of early cancer detection, expanding access to advanced diagnostic tests, and government support for healthcare modernization. The adoption of next-generation sequencing, biomarker testing, and molecular diagnostics is rising in hospitals, diagnostic centers, and research institutes. Investments in healthcare infrastructure, coupled with initiatives to improve early screening and personalized patient care, are fueling rapid market expansion in Canada.

North America Non-Hodgkin Lymphoma Diagnostics Market Share

The Non-Hodgkin Lymphoma Diagnostics industry is primarily led by well-established companies, including:

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthcare AG (Germany)

- Danaher Corporation (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- General Electric Company (U.S.)

- Sysmex Corporation (Japan)

- Grail (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Neusoft Corporation (China)

- Agilent Technologies, Inc. (U.S.)

- NeoGenomics Laboratories (U.S.)

- Hologic, Inc. (U.S.)

- Integrated DNA Technologies, Inc. (U.S.)

- CENTOGENE N.V. (Germany)

- Merit Medical Systems (U.S.)

- Labcorp Genetics Inc. (U.S.)

- PerkinElmer (U.S.)

- QIAGEN (U.S.)

- GeneDx, LLC (U.S.)

Latest Developments in North America Non-Hodgkin Lymphoma Diagnostics Market

- In May 2025, Roche announced the expansion of its Columvi (glofitamab) therapy for relapsed or refractory diffuse large B-cell lymphoma (DLBCL). Data from a two-year follow-up study demonstrated a 40% improvement in overall survival for patients treated with Columvi® in combination with gemcitabine and oxaliplatin (GemOx), compared to the standard rituximab plus GemOx regimen. This advancement underscores Roche's commitment to enhancing treatment options for NHL patients through innovative therapies

- In August 2025, Foresight Diagnostics entered into a licensing agreement with Roche Molecular Systems and Roche Sequencing Systems for its PhasED-Seq technology. This collaboration aims to advance diagnostic capabilities in Non-Hodgkin's Lymphoma by leveraging Foresight's patented sequencing technology. The agreement also resolves previous litigation between the parties, reflecting a strategic partnership to enhance diagnostic precision in oncology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.