North America Premium Chocolate Market Analysis and Size

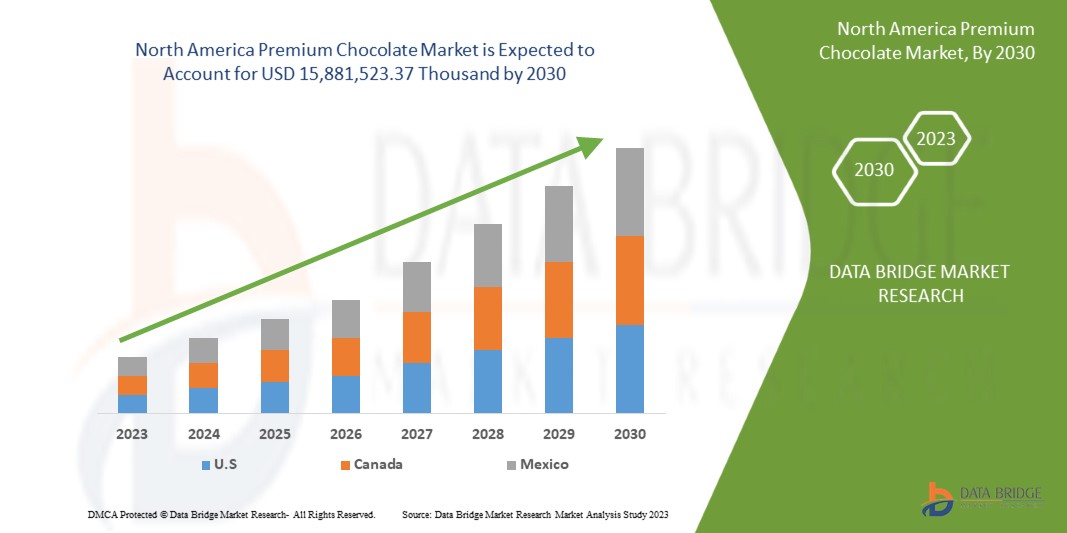

North America premium chocolate market is expected to grow significantly in the forecast period of 2023 to 2030. Data Bridge Market Research analyses that the market is growing with a CAGR of 4.1% in the forecast period of 2023 to 2030 and is expected to reach USD 15,881,523.37 thousand by 2030. The major factor driving the growth of the Premium Chocolate Market is the rise in demand for highly luxurious chocolates.

Premium chocolates are known to have more cocoa content compared to regular ones. It comes in varieties like infused with nuts, fruits, and sometimes alcohol. The presence of all these ingredients gives the premium chocolates a better and more luxurious feel. Customers can get a smoother and richer taste.

The North America premium chocolate market report provides details of market share, new developments, and the impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, products approvals, strategic decisions, product launches, geographic expansions, and technological innovations in the market. To understand the analysis and the market scenario, contact us for an analyst brief. Our team will help you create a revenue-impact solution to achieve your desired goal.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Years |

2021 (Customizable to 2015 - 2020) |

|

Quantitative Units |

Revenue in USD Thousand and Pricing in USD |

|

Segments Covered |

By Type (Milk Chocolate, Dark Chocolate, And White Chocolate), Product Type (Regular/Plain and Filled), Inclusion (With Inclusion Chocolates and Regular and No Inclusions Chocolate), Nature (Conventional and Organic), Category (Standard Premium and Super Premium), Cocoa Content (50-60%, 71-80%, 61-70%, 81-90%, and 91-100%), Flavor (Flavor and Classic/Regular), Packaging (Plastic Wrap, Gift Boxes/Assorted, Pouches, Board Box, Sachets, and Others), Distribution Channel (Store Based Retailers and Non-Store Retailers) |

|

Countries Covered |

U.S., Canada, and Mexico |

|

Market Players Covered |

Mars, Incorporated and its Affiliates (Virginia), Mondelēz International(U.S.), THE HERSHEY COMPANY (U.S.), Ferrero (Italy), Nestlé (Switzerland), General Mills, Inc.(USA), Meiji Holdings Co., Ltd.(Japan), Chocoladefabriken Lindt & Sprüngli AG (Switzerland), Barry Callebaut (Switzerland), The Kraft Heinz Company(USA), Cargill, Incorporated. (U.S.), Cloetta AB(Sweden), ORION CORP.(Korea), Ghirardelli Chocolate Company (A Subsidiary of Lindt & Sprüngli AG) (U.S.), Ezaki Glico Co., Ltd.(Japan), MORINAGA & CO., LTD(Japan), and Arcor(Argentina) among others. |

|

Data Points Covered in the Report |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Market Definition

Premium chocolate is a type of chocolate that has a higher percentage of cocoa solids than regular chocolate milk. It can refer to a number of things, such as the high quantity of cocoa used in the bar; whether it is Fairtrade and sustainably sourced; if it combines other ingredients, such as raspberry chunks or alcohol; and if the packaging has a more sophisticated feel. It is also made with whole milk instead of skim milk and has a higher fat content. Premium chocolate milk has a richer flavor and a thicker consistency than regular chocolate milk.

North America Premium Chocolate Market Dynamics

DRIVERS

- Rise in popularity of vegan, organic, and gluten free chocolates.

The awareness of the consumption of vegan, organic, and gluten free chocolates has slowly evolved among consumers all over the globe. Vegan chocolate helps in improving brain function and is considered much better for health than the standard one. It is made from plant-based ingredients instead of dairy, eggs, and gelatin, which means it contains less fat, fewer calories, and no cholesterol.

The consumption of cocoa products has led to major health benefits, which is expected to drive the growth of the premium chocolate based products market. The health benefits include decreased hypertension, reduced chronic fatigue syndrome, and protection against sunburn, among others. Cocoa is also rich in polyphenols that help in protecting the body's tissues against oxidative stress and associated pathologies such as cancers and inflammation.

Cacao powder is used in making vegan chocolates which come from cacao beans that haven’t been roasted. Since these beans aren’t heated to a high temperature during processing, it helps in keeping all their vitamins and minerals intact. Also, vegan chocolates don’t have any milk in them, so they have a lot of fiber, protein, and antioxidants.

Vegan chocolates have anandamide and raw cacao in them, which bind to the receptors in your brain and make you feel happy and at peace. Vegan chocolate helps in lowering blood pressure. Besides lowering blood pressure, vegan chocolate has other properties that can reduce your risk of heart attack and stroke. Other than cocoa’s positive impact on age-related mental degeneration, its effect on the brain may also improve mood and symptoms of depression.

A gluten-free diet is an alternative for those who have celiac disease. Eating gluten will cause your intestines to become inflamed and damaged, leading to various health problems, including vitamin deficiencies, anemia, and osteoporosis. Pure dark chocolate that is unsweetened and derived from roasted cacao beans doesn't contain gluten naturally. Therefore preference of gluten-free chocolate is a tasty and healthy alternative to regular chocolate due to its health benefits

The consumption of vegan, organic, and gluten-free chocolate based products can help to control heart and blood pressure diseases. So, the increase in the awareness of cocoa products on health is expected to drive the North America premium chocolate market.

- High demand for premium chocolates in the festive seasons.

Seasonal demand plays an important role in the sales of premium chocolates. In the North America market, the gifting of chocolates plays a major role and which leads to the increase in the festive seasons, especially on Easter, Valentine’s Day, Christmas, and others. The growing influence of online retailing is also considered one of the prime reasons to increase the sales of seasonal chocolates. Westernization in the culture has become millennials aware of the gifting culture.

Various seasonal chocolate players launch a wide range of crafted chocolates with new flavors and packaging variations during such special occasions. They are also following integrated marketing communication using various other modes of social media platforms to increase the popularity of their seasonal chocolate offerings. This helps in generating awareness about seasonal chocolates globally

The shifting preference and acceptance of chocolate and its attractive packaging, adopting the gifting culture, Consistency in quality, affluence of urbanization amid youth, and high disposable income is driving the market of premium chocolate culture.

The factors such as the purchasing power of the millennials, the booming e-commerce industry, the soar in the gifting market, and the influence of Westernization and unconventional approaches by retailing brands have spanned which is expected to drive the North America premium chocolate market

OPPORTUNITIES

- Continuous focus on developing new flavored and unique chocolates

The emerging trend of clean-label and organic products to maintain overall health and wellness has led to the rapid escalation in demand for premium or specialty chocolates. The introduction of unique taste and flavors have been seen to be a key factor that has been grabbing the attention of customers.

Moreover, companies are introducing their products with innovative ideas to secure their position in the North America premium chocolate market.

Thus to increase the consumer base, introducing flavored and improved textures of chocolates will create potential opportunities for premium chocolate producers. The companies should introduce local and seasonal flavors to attract consumers all around the globe, focusing both on health and taste. This could open up a whole new area for flavor innovation which is expected to create an opportunity for the market.

- Rising trend of online distribution

E-commerce is redefining commercial activities around the world. Over the years, e-commerce has evolved in profound ways. There are so many health benefits of chocolate, along with the strong desire to add innovative flavors to chocolate drives up the sale of the chocolates. The distribution channel earlier was solely the stores that mainly run without any electronic media usage, but with the increased internet usage, the distribution channels are changed. Since the internet continues influencing everyday lives, e-commerce is necessary for any market's growth and helps extend a business beyond its physical location.

Online distribution channel benefits the manufacturer by exploiting the eagerness of online customers to try new goods. Strong advertising and marketing campaigns for vegan, gluten-free, low sugar chocolates on the online sites will add to the sales of the chocolates. E-commerce is also a hit among consumers due to the multiple offers provided by online platforms on festivals and regular customers, and even on bulk orders.

The increased digitalization and migration of consumers to online distribution channels will continue to spur the growth of e-commerce, the makes the rising trend of online distribution channel, which is expected to create opportunity for the market.

RESTRAINTS/CHALLENGES

- Fluctuating prices of raw materials

The cost of chocolate has changed, but most consumers were unaware of it. The price volatility of chocolate is primarily influenced by the supply of chocolate drivers. The main component in chocolate production is cocoa, which is used in a variety of products. To make chocolate, other ingredients like sugar, dairy products, nuts, corn sweeteners, and energy are also required. The commodities market, which sets the price based on supply and demand levels and can cause varying levels of volatility on commodity prices, is primarily responsible for these commodities' prices.

Cocoa powder and cocoa butter are the two parts of cocoa that are used to make chocolate. Since it produces the richer chocolates and is used in thin chocolate confectionery treats, cocoa butter is by far the more desirable of the two. However, because it is the harder and more expensive to produce, any disruption in the supply of cocoa will eventually filter down and raise consumer prices. The fluctuating price of raw material for production is expected to restraint the premium chocolate growth in the market.

- Rising cost of supply chain

The price volatility of chocolate is primarily influenced by the supply of chocolate. The main component in chocolate production is cocoa, which is used in a variety of products. Other ingredients required for the production of chocolate products include sugar, dairy products, nuts, corn sweeteners, and energy. The price are based on supply and demand levels and can cause varying levels of volatility on prices, is primarily responsible for these commodities' prices. The process by which cocoa becomes the ingredients for goods that are sold on supermarket shelves is a complicated one. At various stages of the production cycle, cocoa grown by a number of farmers, primarily smallholders, is blended together. Since most supply chain risks originate at the individual farm level, it is challenging to trace cocoa back to those locations because of this mixing. Additionally, this supply chain's complexity creates inequities throughout the value chain.

Moreover, the most important problems in cocoa supply chains are the expansion of cocoa production into protected forest reserves and the use of child labor. Due to the anticipated rise in the frequency of pests, diseases, and droughts, climate change also poses a threat to the long-term viability of the cocoa industry.

The disruption in the supply chain leads to the increasing price of the supply chain, which is expected to challenge the market growth in the forecast period

Recent Developments

- Feb 10, 2023, Morinaga Nutritional Foods, Inc. (a subsidiary) announced the acquisition of Turtle Island Foods Holdings, Inc. Turtle Island Foods is a manufacturer of plant-based food products. As a result of this acquisition, Turtle Islands Foods will become a whole subsidiary of Morinaga Nutritional Foods, Inc. This will create an opportunity to develop nutritional chocolates for the premium chocolate market

- In 2021, Lindt and Sprüngli invested around USD 80.95 Million in order to expand its cocoa mass plant in Olten. It is considered the largest and most important cocoa mass plant with the North America production network

North America Premium Chocolate Market Scope

North America Premium Chocolate Market is segmented into nine notable segments based on type, product type, inclusion, nature, category, cocoa content, flavor, packaging, and distribution channel. The growth amongst these segments will help you analyze major growth segments in the industries and provide the users with a valuable market overview and market insights to make strategic decisions to identify core market applications.

TYPE

- Milk Chocolate

- Dark Chocolate

- White Chocolate

On the basis of type, the market is segmented into milk chocolate, dark chocolate, and white chocolate.

PRODUCT TYPE

- Regular/Plain

- Filled

On the basis of product type, the market is segmented into regular/plain and filled.

INCLUSION

- With Inclusion Chocolates And Regular

- No Inclusions Chocolate

On the basis of inclusion, the market is segmented into with inclusion chocolates and regular, no inclusions chocolate.

NATURE

- Conventional

- Organic

On the basis of nature, the market is segmented into conventional and organic.

CATEGORY

- Standard Premium

- Super Premium

On the basis of category, the market is segmented into standard premium and super premium.

COCOA CONTENT

- 50-60%

- 71-80%

- 61-70%

- 81-90%

- 91-100%

On the basis of cocoa-content, the market is segmented into 50-60%, 71-80%, 61-70%, 81-90%, and 91-100%.

FLAVOR

- Flavor

- Classic/Regular

On the basis of flavor, the market is segmented into flavor, classic/regular.

PACKAGING

- Plastic Wrap

- Gift Boxes/Assorted

- Pouches

- Board Box

- Sachets

- Others

On the basis of packaging, the market is segmented into plastic wrap, gift boxes/assorted, pouches, board box, sachets, and others.

DISTRIBUTION CHANNEL

- Store Based Retailer

- Non-Store Retailers

On the basis of distribution channel, the market is segmented into store based retailers and non-store retailers.

North America Premium Chocolate Market Regional Analysis/Insights

The North America premium chocolate market is segmented on the basis of type, product type, inclusion, nature, category, cocoa content, flavor, packaging, and distribution channel.

The countries in the North America premium chocolate market are U.S., Canada, and Mexico.

The U.S. is dominating the North America premium chocolate market in terms of market share and market revenue due to the growing awareness regarding the properties of the Alkylation technologies in this region.

The country section of the report also provides individual market-impacting factors and changes in market regulation that impact the current and future trends of the market. Data point downstream and upstream value chain analysis, technical trends, porter's five forces analysis, and case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, the impact of domestic tariffs, and trade routes are considered while providing forecast analysis of the country data.

Competitive Landscape and North America Premium Chocolate Market Share Analysis

North America premium chocolate market competitive landscape provides details by competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product trials pipelines, product approvals, patents, product width and breadth, application dominance, technology lifeline curve. The above data points provided are only related to the companies’ focus related to the North America premium chocolate market.

Some of the major players operating in the North America premium chocolate market are Mars, Incorporated and its Affiliates, Mondelēz International, THE HERSHEY COMPANY, Ferrero, Nestlé, General Mills, Inc., Meiji Holdings Co., Ltd., Lindt & Sprungli AG, Barry Callebaut, The Kraft Heinz Company, Cargill, Incorporated., Cloetta AB, ORION CORP., Ghirardelli Chocolate Company (A Subsidiary of Lindt & Sprüngli AG), Ezaki Glico Co., Ltd., MORINAGA & CO., LTD, Arcor among others.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA PREMIUM CHOCOLATE MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 GRADE LIFE LINE CURVE

2.7 MULTIVARIATE MODELING

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET APPLICATION COVERAGE GRID

2.11 DBMR MARKET CHALLENGE MATRIX

2.12 DBMR VENDOR SHARE ANALYSIS

2.13 SECONDARY SOURCES

2.14 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ANALYSIS OF HAZELNUT CONTENT FOR TOP NORTH AMERICA PREMIUM CHOCOLATE BRANDS

4.2 BRAND COMPARATIVE ANALYSIS

4.2.1 FERRERO

4.2.2 NESTLE

4.2.3 CHOCOLADEFABRIKEN LINDT & SPRÜNGLI AG

4.3 FACTORS INFLUENCING BUYING DECISION

4.3.1 PACKAGING FACTOR

4.3.2 TASTE

4.3.3 HEALTH

4.3.4 BRAND LOYALTY

4.3.5 GENDER AND AGE

4.3.6 INCOME

4.4 INDUSTRY TRENDS AND FUTURE PERSPECTIVE

4.4.1 RISING CONSUMER PREFERENCE TOWARD DARK AND VEGAN CHOCOLATE

4.4.2 CONSUMERS ARE INTERESTED IN NEW INNOVATIVE FLAVOURS AND TEXTURE

4.4.3 RISING DEMAND FOR PREMIUM CHOCOLATES FOR GIFTING PURPOSES

4.4.4 FUTURE PERSPECTIVE

4.5 MEETING CONSUMER REQUIREMENT

4.6 SUPPLY CHAIN ANALYSIS

4.6.1 RAW MATERIAL PROCUREMENT & MANUFACTURING

4.6.2 DISTRIBUTION

4.6.3 END-USERS

4.7 SHOPPING BEHAVIOR AND DYNAMICS

4.7.1 RECOMMENDATIONS FROM FAMILY AND FRIENDS

4.7.2 RESEARCH

4.7.3 IMPULSIVE

4.7.4 ADVERTISEMENT

4.7.5 TELEVISION ADVERTISEMENT

4.7.6 ONLINE ADVERTISEMENT

4.7.7 IN-STORE ADVERTISEMENT

4.7.8 OUTDOOR ADVERTISEMENT

4.8 NEW PRODUCT LAUNCH STRATEGY

4.8.1 NUMBER OF PRODUCT LAUNCHES

4.8.2 LINE EXTENSION

4.8.3 NEW PACKAGING

4.8.4 RE-LAUNCHED

4.8.5 NEW FORMULATION

4.8.6 DIFFERENTIAL PRODUCT OFFERING

4.8.7 PACKAGE DESIGNING

4.8.8 PRICING ANALYSIS

4.9 REGULATION COVERAGE

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 RISE IN THE POPULARITY OF VEGAN, ORGANIC, AND GLUTEN FREE CHOCOLATES

5.1.2 HIGH DEMAND FOR PREMIUM CHOCOLATES IN FESTIVE SEASONS

5.1.3 DEMAND FOR PREMIUM CHOCOLATES OWING TO THE SHIFT TOWARDS A HEALTHY LIFESTYLE

5.1.4 USE OF PREMIUM CHOCOLATE IN THE BAKING INDUSTRY

5.2 RESTRAINTS

5.2.1 FLUCTUATING PRICES OF RAW MATERIALS

5.2.2 AVAILABILITY OF VARIOUS SUBSTITUTE

5.3 OPPORTUNITIES

5.3.1 CONTINUOUS FOCUS ON DEVELOPING NEW FLAVORED AND UNIQUE CHOCOLATES

5.3.2 RISING TREND OF ONLINE DISTRIBUTION

5.4 CHALLENGES

5.4.1 RISING COST OF SUPPLY CHAIN

5.4.2 RULES AND REGULATIONS ASSOCIATED WITH PREMIUM CHOCOLATES

6 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY REGION

6.1 NORTH AMERICA

6.1.1 U.S.

6.1.2 CANADA

6.1.3 MEXICO

7 NORTH AMERICA PREMIUM CHOCOLATE MARKET: COMPANY LANDSCAPE

7.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

7.2 ACQUISITION

7.3 NEW PRODUCT DEVELOPMENT

7.4 FACILITY EXPANSION

7.5 NEW APPOINTMENT

8 SWOT ANALYSIS

9 COMPANY PROFILES

9.1 MARS, INCORPORATED AND ITS AFFILIATES

9.1.1 COMPANY SNAPSHOT

9.1.2 COMPANY SHARE ANALYSIS

9.1.3 PRODUCT PORTFOLIO

9.1.4 RECENT UPDATES

9.2 MONDELĒZ INTERNATIONAL

9.2.1 COMPANY SNAPSHOT

9.2.2 REVENUE ANALYSIS

9.2.3 COMPANY SHARE ANALYSIS

9.2.4 PRODUCT PORTFOLIO

9.2.5 RECENT DEVELOPMENT

9.3 THE HERSHEY COMPANY

9.3.1 COMPANY SNAPSHOT

9.3.2 REVENUE ANALYSIS

9.3.3 COMPANY SHARE ANALYSIS

9.3.4 PRODUCT PORTFOLIO

9.3.5 RECENT DEVELOPMENT

9.4 FERRERO

9.4.1 COMPANY SNAPSHOT

9.4.2 COMPANY SHARE ANALYSIS

9.4.3 PRODUCT PORTFOLIO

9.4.4 RECENT UPDATES

9.5 NESTLÉ

9.5.1 COMPANY SNAPSHOT

9.5.2 REVENUE ANALYSIS

9.5.3 COMPANY SHARE ANALYSIS

9.5.4 PRODUCT PORTFOLIO

9.5.5 RECENT DEVELOPMENT

9.6 ARCOR

9.6.1 COMPANY SNAPSHOT

9.6.2 REVENUE ANALYSIS

9.6.3 PRODUCT PORTFOLIO

9.6.4 RECENT DEVELOPMENT

9.7 BARRY CALLEBAUT

9.7.1 COMPANY SNAPSHOT

9.7.2 REVENUE ANALYSIS

9.7.3 PRODUCT PORTFOLIO

9.7.4 RECENT UPDATES

9.8 CARGILL, INCORPORATED

9.8.1 COMPANY SNAPSHOT

9.8.2 PRODUCT PORTFOLIO

9.8.3 RECENT UPDATES

9.9 CHOCOLADEFABRIKEN LINDT & SPRÜNGLI AG (2022)

9.9.1 COMPANY SNAPSHOT

9.9.2 REVENUE ANALYSIS

9.9.3 PRODUCT PORTFOLIO

9.9.4 RECENT DEVELOPMENT

9.1 CLOETTA AB

9.10.1 COMPANY SNAPSHOT

9.10.2 REVENUE ANALYSIS

9.10.3 PRODUCT PORTFOLIO

9.10.4 RECENT DEVELOPMENT

9.11 EZAKI GLICO CO., LTD.

9.11.1 COMPANY SNAPSHOT

9.11.2 REVENUE ANALYSIS

9.11.3 PRODUCT PORTFOLIO

9.11.4 RECENT DEVELOPMENT

9.12 GENERAL MILLS, INC.

9.12.1 COMPANY SNAPSHOT

9.12.2 REVENUE ANALYSIS

9.12.3 PRODUCT PORTFOLIO

9.12.4 RECENT DEVELOPMENT

9.13 GHIRARDELLI CHOCOLATE COMPANY

9.13.1 COMPANY SNAPSHOT

9.13.2 PRODUCT PORTFOLIO

9.13.3 RECENT DEVELOPMENT

9.14 MEIJI HOLDINGS CO., LTD.

9.14.1 COMPANY SNAPSHOT

9.14.2 REVENUE ANALYSIS

9.14.3 PRODUCT PORTFOLIO

9.14.4 RECENT DEVELOPMENT

9.15 MORINAGA & CO., LTD.

9.15.1 COMPANY SNAPSHOT

9.15.2 REVENUE ANALYSIS

9.15.3 PRODUCT PORTFOLIO

9.15.4 RECENT DEVELOPMENT

9.16 ORION CORP.

9.16.1 COMPANY SNAPSHOT

9.16.2 REVENUE ANALYSIS

9.16.3 PRODUCT PORTFOLIO

9.16.4 RECENT DEVELOPMENTS

9.17 THE KRAFT HEINZ COMPANY

9.17.1 COMPANY SNAPSHOT

9.17.2 REVENUE ANALYSIS

9.17.3 PRODUCT PORTFOLIO

9.17.4 RECENT DEVELOPMENT

10 QUESTIONNAIRE

11 RELATED REPORTS

List of Table

TABLE 1 ESTIMATED HAZELNUT CONTENT FOR TOP NORTH AMERICA PREMIUM CHOCOLATE COMPANIES

TABLE 2 REGULATORY COVERAGE

TABLE 3 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY COUNTRY, 2021-2030 (USD THOUSAND)

TABLE 4 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 5 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY PRODUCT TYPE, 2021-2030 (USD THOUSAND)

TABLE 6 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY INCLUSION, 2021-2030 (USD THOUSAND)

TABLE 7 NORTH AMERICA WITH INCLUSIONS CHOCOLATES IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 8 NORTH AMERICA INFUSED NUTS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 9 NORTH AMERICA ALMOND IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 10 NORTH AMERICA ALMOND IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 11 NORTH AMERICA HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 12 NORTH AMERICA HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 13 NORTH AMERICA PEANUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 14 NORTH AMERICA PEANUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 15 NORTH AMERICA CASHEW IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 16 NORTH AMERICA CASHEW IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 17 NORTH AMERICA RAISINS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 18 NORTH AMERICA RAISINS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 19 NORTH AMERICA PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 20 NORTH AMERICA PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 21 NORTH AMERICA OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 22 NORTH AMERICA OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 23 NORTH AMERICA INFUSED FRUITS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 24 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY NATURE, 2021-2030 (USD THOUSAND)

TABLE 25 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY CATEGORY, 2021-2030 (USD THOUSAND)

TABLE 26 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY COCOA CONTENT, 2021-2030 (USD THOUSAND)

TABLE 27 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY FLAVOR, 2021-2030 (USD THOUSAND)

TABLE 28 NORTH AMERICA FLAVOR IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 29 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY PACKAGING, 2021-2030 (USD THOUSAND)

TABLE 30 NORTH AMERICA PREMIUM CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2021-2030 (USD THOUSAND)

TABLE 31 NORTH AMERICA STORE BASED RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 32 NORTH AMERICA NON-STORE RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 33 U.S. PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 34 U.S. PREMIUM CHOCOLATE MARKET, BY PRODUCT TYPE, 2021-2030 (USD THOUSAND)

TABLE 35 U.S. PREMIUM CHOCOLATE MARKET, BY INCLUSION, 2021-2030 (USD THOUSAND)

TABLE 36 U.S. WITH INCLUSIONS CHOCOLATES IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 37 U.S. INFUSED NUTS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 38 U.S. ALMOND IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 39 U.S. ALMOND IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 40 U.S. HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 41 U.S. HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 42 U.S. PEANUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 43 U.S. PEANUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 44 U.S. CASHEW IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 45 U.S. CASHEW IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 46 U.S. RAISINS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 47 U.S. RAISINS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 48 U.S. PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 49 U.S. PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 50 U.S. OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 51 U.S. OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 52 U.S. INFUSED FRUITS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 53 U.S. PREMIUM CHOCOLATE MARKET, BY NATURE, 2021-2030 (USD THOUSAND)

TABLE 54 U.S. PREMIUM CHOCOLATE MARKET, BY CATEGORY, 2021-2030 (USD THOUSAND)

TABLE 55 U.S. PREMIUM CHOCOLATE MARKET, BY COCOA CONTENT, 2021-2030 (USD THOUSAND)

TABLE 56 U.S. PREMIUM CHOCOLATE MARKET, BY FLAVOR, 2021-2030 (USD THOUSAND)

TABLE 57 U.S. FLAVOR IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 58 U.S. PREMIUM CHOCOLATE MARKET, BY PACKAGING, 2021-2030 (USD THOUSAND)

TABLE 59 U.S. PREMIUM CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2021-2030 (USD THOUSAND)

TABLE 60 U.S. STORE BASED RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 61 U.S. NON-STORE RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 62 CANADA PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 63 CANADA PREMIUM CHOCOLATE MARKET, BY PRODUCT TYPE, 2021-2030 (USD THOUSAND)

TABLE 64 CANADA PREMIUM CHOCOLATE MARKET, BY INCLUSION, 2021-2030 (USD THOUSAND)

TABLE 65 CANADA WITH INCLUSIONS CHOCOLATES IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 66 CANADA INFUSED NUTS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 67 CANADA ALMOND IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 68 CANADA ALMOND IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 69 CANADA HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 70 CANADA HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 71 CANADA PEANUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 72 CANADA PEANUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 73 CANADA CASHEW IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 74 CANADA CASHEW IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 75 CANADA RAISINS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 76 CANADA RAISINS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 77 CANADA PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 78 CANADA PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 79 CANADA OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 80 CANADA OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 81 CANADA INFUSED FRUITS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 82 CANADA PREMIUM CHOCOLATE MARKET, BY NATURE, 2021-2030 (USD THOUSAND)

TABLE 83 CANADA PREMIUM CHOCOLATE MARKET, BY CATEGORY, 2021-2030 (USD THOUSAND)

TABLE 84 CANADA PREMIUM CHOCOLATE MARKET, BY COCOA CONTENT, 2021-2030 (USD THOUSAND)

TABLE 85 CANADA PREMIUM CHOCOLATE MARKET, BY FLAVOR, 2021-2030 (USD THOUSAND)

TABLE 86 CANADA FLAVOR IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 87 CANADA PREMIUM CHOCOLATE MARKET, BY PACKAGING, 2021-2030 (USD THOUSAND)

TABLE 88 CANADA PREMIUM CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2021-2030 (USD THOUSAND)

TABLE 89 CANADA STORE BASED RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 90 CANADA NON-STORE RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 91 MEXICO PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 92 MEXICO PREMIUM CHOCOLATE MARKET, BY PRODUCT TYPE, 2021-2030 (USD THOUSAND)

TABLE 93 MEXICO PREMIUM CHOCOLATE MARKET, BY INCLUSION, 2021-2030 (USD THOUSAND)

TABLE 94 MEXICO WITH INCLUSIONS CHOCOLATES IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 95 MEXICO INFUSED NUTS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 96 MEXICO ALMOND IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 97 MEXICO ALMOND IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 98 MEXICO HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 99 MEXICO HAZELNUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 100 MEXICO PEANUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 101 MEXICO PEANUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 102 MEXICO CASHEW IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 103 MEXICO CASHEW IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 104 MEXICO RAISINS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 105 MEXICO RAISINS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 106 MEXICO PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 107 MEXICO PISTACHIOS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 108 MEXICO OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY FORM, 2021-2030 (USD THOUSAND)

TABLE 109 MEXICO OTHER NUTS IN PREMIUM CHOCOLATE MARKET, BY CONTENT, 2021-2030 (USD THOUSAND)

TABLE 110 MEXICO INFUSED FRUITS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 111 MEXICO PREMIUM CHOCOLATE MARKET, BY NATURE, 2021-2030 (USD THOUSAND)

TABLE 112 MEXICO PREMIUM CHOCOLATE MARKET, BY CATEGORY, 2021-2030 (USD THOUSAND)

TABLE 113 MEXICO PREMIUM CHOCOLATE MARKET, BY COCOA CONTENT, 2021-2030 (USD THOUSAND)

TABLE 114 MEXICO PREMIUM CHOCOLATE MARKET, BY FLAVOR, 2021-2030 (USD THOUSAND)

TABLE 115 MEXICO FLAVOR IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 116 MEXICO PREMIUM CHOCOLATE MARKET, BY PACKAGING, 2021-2030 (USD THOUSAND)

TABLE 117 MEXICO PREMIUM CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2021-2030 (USD THOUSAND)

TABLE 118 MEXICO STORE BASED RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 119 MEXICO NON-STORE RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 120 MEXICO NON-STORE RETAILERS IN PREMIUM CHOCOLATE MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

List of Figure

FIGURE 1 NORTH AMERICA PREMIUM CHOCOLATE MARKET

FIGURE 2 NORTH AMERICA PREMIUM CHOCOLATE MARKET : DATA TRIANGULATION

FIGURE 3 NORTH AMERICA PREMIUM CHOCOLATE MARKET : DROC ANALYSIS

FIGURE 4 NORTH AMERICA PREMIUM CHOCOLATE MARKET : NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA PREMIUM CHOCOLATE MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA PREMIUM CHOCOLATE MARKET: THE GRADE LIFE LINE CURVE

FIGURE 7 NORTH AMERICA PREMIUM CHOCOLATE MARKET: MULTIVARIATE MODELLING

FIGURE 8 NORTH AMERICA PREMIUM CHOCOLATE MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 9 NORTH AMERICA PREMIUM CHOCOLATE MARKET: DBMR MARKET POSITION GRID

FIGURE 10 NORTH AMERICA PREMIUM CHOCOLATE MARKET: MARKET APPLICATION COVERAGE GRID

FIGURE 11 NORTH AMERICA PREMIUM CHOCOLATE MARKET: THE MARKET CHALLENGE MATRIX

FIGURE 12 NORTH AMERICA PREMIUM CHOCOLATE MARKET: VENDOR SHARE ANALYSIS

FIGURE 13 NORTH AMERICA PREMIUM CHOCOLATE MARKET : SEGMENTATION

FIGURE 14 THE RISE IN POPULARITY OF VEGAN, ORGANIC, AND GLUTEN FREE CHOCOLATE ACROSS THE GLOBE IS EXPECTED TO DRIVE THE NORTH AMERICA PREMIUM CHOCOLATE MARKET IN THE FORECAST PERIOD

FIGURE 15 THE MILK CHOCOLATE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA PREMIUM CHOCOLATE MARKET IN 2023 & 2030

FIGURE 16 SUPPLY CHAIN OF THE NORTH AMERICA PREMIUM CHOCOLATE MARKET

FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE NORTH AMERICA PREMIUM CHOCOLATE MARKET

FIGURE 18 NORTH AMERICA PREMIUM CHOCOLATE MARKET: SNAPSHOT (2022)

FIGURE 19 NORTH AMERICA PREMIUM CHOCOLATE MARKET: BY COUNTRY (2022)

FIGURE 20 NORTH AMERICA PREMIUM CHOCOLATE MARKET: BY COUNTRY (2023 & 2030)

FIGURE 21 NORTH AMERICA PREMIUM CHOCOLATE MARKET: BY COUNTRY (2022 & 2030)

FIGURE 22 NORTH AMERICA PREMIUM CHOCOLATE MARKET: BY TYPE (2023 - 2030)

FIGURE 23 NORTH AMERICA PREMIUM CHOCOLATE MARKET: COMPANY SHARE 2022 (%)

North America Premium Chocolate Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Premium Chocolate Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Premium Chocolate Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.