North America Primary Angle Closure Glaucoma Market

Market Size in USD Million

USD

141.35 Million

USD

220.24 Million

2024

2032

USD

141.35 Million

USD

220.24 Million

2024

2032

| 2025 - 2032 | |

| USD 141.35 Million | |

| USD 220.24 Million | |

| % | |

|

North America Primary Angle-Closure Glaucoma Market Size

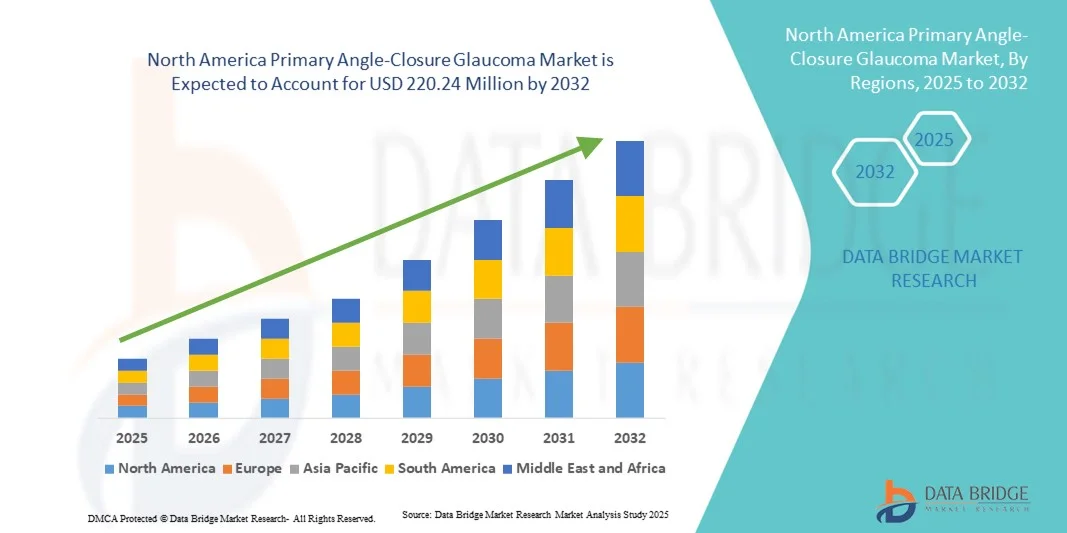

- The North America primary angle-closure glaucoma market size was valued at USD 141.35 million in 2024 and is expected to reach USD 220.24 million by 2032, at a CAGR of 5.70% during the forecast period

- The market growth is largely driven by the increasing prevalence of glaucoma, rising geriatric population, and greater awareness about early diagnosis and effective management of eye disorders. Advancements in ophthalmic diagnostic devices and surgical interventions are further fueling market expansion

- In addition, growing patient preference for minimally invasive procedures, coupled with increasing adoption of advanced treatment modalities in clinical settings, is positioning North America as a key region for PACG management solutions. These combined factors are accelerating the uptake of PACG treatments, thereby substantially propelling market growth

North America Primary Angle-Closure Glaucoma Market Analysis

- Primary angle-closure glaucoma (PACG), a severe ophthalmic condition caused by blocked drainage of aqueous humor leading to elevated intraocular pressure, is driving demand for advanced diagnostic and treatment solutions in both clinical and hospital settings due to its risk of irreversible vision loss if untreated

- The rising prevalence of glaucoma, especially among the aging population, increasing awareness for early diagnosis, and technological advancements in ophthalmic imaging and treatment devices are the main factors fueling PACG market growth

- The United States dominated the PACG market with the largest revenue share of 79.1% in 2024, attributed to its robust healthcare infrastructure, high healthcare expenditure, and presence of key ophthalmic device and pharmaceutical companies

- Canada is expected to experience notable growth during the forecast period, due to rising awareness of eye health, an increasing geriatric population, and the adoption of advanced diagnostic and treatment modalities in hospitals and specialty clinics

- The chronic angle-closure glaucoma segment dominated the North America PACG market with a market share of 55.2% in 2024, reflecting the high prevalence of chronic cases and the need for long-term monitoring and management in hospitals, specialty clinics, and ambulatory surgical centers

Report Scope and North America Primary Angle-Closure Glaucoma Market Segmentation

|

Attributes |

North America Primary Angle-Closure Glaucoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Primary Angle-Closure Glaucoma Market Trends

Advancements in AI-Assisted Diagnosis and Tele-Ophthalmology

- A key and accelerating trend in the North America PACG market is the integration of artificial intelligence (AI) in diagnostic imaging and tele-ophthalmology platforms, significantly improving early detection and monitoring of disease progression

- For instance, AI-powered optical coherence tomography (OCT) systems can automatically detect angle closure and quantify optic nerve damage, supporting ophthalmologists in accurate and timely diagnosis

- AI-driven predictive models are being developed to analyze patient risk factors, enabling ophthalmologists to personalize treatment plans and anticipate disease progression. For instance, tools such as DeepMind-based glaucoma detection algorithms enhance diagnostic precision and efficiency

- Tele-ophthalmology platforms allow remote PACG screening and monitoring, facilitating access for patients in rural or underserved areas. Through secure digital platforms, ophthalmologists can review imaging data, recommend interventions, and follow up with patients virtually

- This trend toward AI-assisted diagnosis and telemedicine is reshaping clinical practices and patient expectations, prompting companies such as Topcon and Zeiss to develop smart imaging systems with integrated AI analysis and remote monitoring capabilities

- The adoption of AI-assisted diagnostics and tele-ophthalmology is rapidly growing in both hospitals and specialty clinics, as providers aim to improve clinical outcomes and streamline PACG management across North America

North America Primary Angle-Closure Glaucoma Market Dynamics

Driver

Rising Prevalence of Glaucoma and Geriatric Population

- The increasing incidence of PACG among the aging population, combined with higher awareness of early eye disease detection, is a major driver of the North America PACG market

- For instance, in 2024, the American Academy of Ophthalmology emphasized early detection programs for high-risk groups, promoting routine screenings and AI-assisted diagnostics to manage PACG effectively

- Rising prevalence of comorbidities such as diabetes and hypertension is further contributing to increased PACG diagnoses, compelling ophthalmologists to adopt advanced diagnostic and treatment modalities

- Furthermore, growing patient demand for minimally invasive procedures and laser-based interventions is driving adoption of innovative surgical treatments in hospitals and specialty clinics

- For instance, MIGS (minimally invasive glaucoma surgery) and laser peripheral iridotomy are being increasingly performed due to efficacy in controlling intraocular pressure and improving patient compliance

- The trend toward patient-centric care, early detection, and advanced treatment adoption is propelling market growth in both urban and semi-urban healthcare centers across North America

Restraint/Challenge

High Treatment Costs and Limited Patient Awareness

- The high cost of advanced diagnostic tools and surgical interventions poses a significant challenge to broader market adoption of PACG management solutions in North America

- For instance, premium imaging devices such as swept-source OCT and MIGS instruments require substantial capital investment by hospitals and specialty clinics, potentially limiting access in smaller healthcare setups

- Insufficient patient awareness regarding PACG symptoms and the importance of early diagnosis contributes to delayed treatment, impacting overall market growth

- For instance, studies indicate that a substantial portion of patients are diagnosed only after significant optic nerve damage has occurred, highlighting gaps in screening and education

- Cybersecurity concerns related to cloud-based tele-ophthalmology platforms and data privacy regulations may hinder adoption of digital PACG solutions among cautious healthcare providers

- Overcoming these challenges through patient education campaigns, insurance coverage expansion, and cost-effective diagnostic and treatment solutions will be critical for sustained growth in the North America PACG market

North America Primary Angle-Closure Glaucoma Market Scope

The market is segmented on the basis of disease type, type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the North America PACG market is segmented into acute angle-closure glaucoma and chronic angle-closure glaucoma. The chronic angle-closure glaucoma segment dominated the market with the largest market revenue share of 55.2% in 2024. This dominance is attributed to the higher prevalence of chronic cases among the aging population and the need for long-term monitoring and management. Patients with chronic PACG often require repeated clinical evaluations, laser therapies, and surgical interventions over extended periods, increasing the market demand for advanced diagnostic and treatment solutions. Hospitals and specialty clinics frequently adopt chronic PACG-focused management programs due to the sustained patient follow-up required. Moreover, insurance coverage and reimbursement policies in the U.S. and Canada favor chronic PACG treatment, supporting broader adoption of related medical devices and procedures. Clinical studies and growing awareness campaigns further reinforce early diagnosis and continuous care, strengthening the segment’s market dominance.

The acute angle-closure glaucoma segment is anticipated to witness the fastest growth rate of 19% from 2025 to 2032, fueled by rising awareness of emergency ophthalmic care and increased adoption of rapid intervention procedures. Acute PACG is a medical emergency requiring immediate diagnosis and treatment, often through laser peripheral iridotomy or surgical intervention. The increasing number of ophthalmology centers equipped with rapid-response facilities and advanced diagnostic imaging is accelerating patient access to care. For instance, AI-assisted screening tools and OCT devices enable faster detection of angle closure in emergency cases. In addition, government-led initiatives and patient education programs on glaucoma symptoms are driving early hospital visits, boosting acute PACG treatment adoption. The segment’s growth is further supported by advancements in minimally invasive surgical techniques, which reduce recovery time and improve patient outcomes, making acute PACG management more attractive to healthcare providers.

- By Type

On the basis of type, the North America PACG market is segmented into diagnosis and treatment. The diagnosis segment dominated the market with a revenue share of 52% in 2024, driven by the increasing emphasis on early detection to prevent irreversible vision loss. Diagnostic solutions such as slit-lamp gonioscopy, optical coherence tomography (OCT), and AI-assisted imaging are widely used in hospitals and specialty clinics to identify patients at risk. Hospitals often integrate these advanced diagnostics with electronic medical record systems for better patient management. Routine screenings and preventive eye check-ups in aging populations contribute to the high demand for diagnostic tools. Furthermore, the growing adoption of tele-ophthalmology platforms in North America facilitates remote PACG screening, enhancing diagnostic reach. Continuous innovations and training programs for ophthalmologists further strengthen the market dominance of the diagnosis segment.

The treatment segment is expected to witness the fastest CAGR of 18% from 2025 to 2032, driven by advancements in laser therapy, minimally invasive glaucoma surgery (MIGS), and pharmacological interventions. Hospitals and ambulatory surgical centers are increasingly adopting MIGS and laser peripheral iridotomy for effective intraocular pressure management. Growing awareness of long-term benefits of early surgical interventions is encouraging more patients to opt for treatment. Insurance coverage for surgical procedures and increasing availability of skilled ophthalmic surgeons support market expansion. For instance, AI-assisted surgical planning systems enhance procedural accuracy and patient outcomes. Rising adoption of combination therapies for chronic PACG cases is also contributing to the rapid growth of the treatment segment.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others. The hospitals segment dominated the market with a share of 50% in 2024, attributed to their advanced ophthalmic infrastructure, access to skilled ophthalmologists, and ability to offer both diagnostic and treatment services under one roof. Hospitals often serve as referral centers for complex PACG cases requiring surgical intervention. The presence of state-of-the-art imaging systems, laser treatment devices, and dedicated glaucoma units strengthens hospital adoption. In addition, hospitals benefit from insurance reimbursements, supporting higher patient volumes and frequent follow-ups. Hospitals also drive research and clinical trials, further expanding PACG-related service offerings. Collaborative programs with specialty clinics and tele-ophthalmology platforms enhance hospital dominance.

The specialty clinics segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing demand for focused glaucoma care and minimally invasive procedures. Specialty clinics offer personalized patient management, quicker appointment access, and adoption of AI-assisted diagnostics. For instance, many clinics now provide same-day OCT scanning and laser treatments, attracting patients seeking timely care. Partnerships with insurance providers and technology firms further boost clinic adoption. Clinics are also increasingly integrating telemedicine for follow-up monitoring, reducing hospital dependence. The rise of outpatient-focused glaucoma centers enhances the growth trajectory of specialty clinics as end users.

- By Distribution Channel

On the basis of distribution channel, the North America PACG market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the market with a share of 60% in 2024, driven by bulk procurement by hospitals and large healthcare networks. Direct tender agreements allow healthcare providers to access high-end ophthalmic devices at competitive prices, facilitating the adoption of advanced diagnostics and treatment solutions. Manufacturers often provide training and maintenance support through direct tender agreements, enhancing reliability and long-term usage. Direct procurement also ensures regulatory compliance and streamlined installation of devices. High-volume hospitals and multispecialty clinics prefer direct tender contracts for device standardization and centralized management.

The retail sales segment is expected to witness the fastest growth rate of 18% from 2025 to 2032, fueled by the increasing availability of home-use diagnostic tools and smaller ophthalmic devices for clinics and individual practitioners. Retail sales provide flexibility for smaller specialty clinics and ambulatory surgical centers to procure cost-effective equipment without long-term contracts. For instance, portable OCT devices and tonometers are increasingly sold through retail channels to meet the rising demand for outpatient PACG monitoring. Online and e-commerce platforms are contributing to the accessibility and convenience of retail purchases. The segment growth is also supported by product innovations focusing on user-friendly, compact, and affordable devices suitable for non-hospital settings.

North America Primary Angle-Closure Glaucoma Market Regional Analysis

- The United States dominated the PACG market with the largest revenue share of 79.1% in 2024, attributed to its robust healthcare infrastructure, high healthcare expenditure, and presence of key ophthalmic device and pharmaceutical companies

- Patients and healthcare providers in the region prioritize early detection, effective management, and access to advanced surgical and diagnostic technologies, contributing to strong market adoption

- This widespread adoption is further supported by well-established ophthalmic centers, high healthcare expenditure, and the presence of leading device manufacturers, establishing PACG management solutions as a preferred choice across hospitals and specialty clinics

The U.S. Primary Angle-Closure Glaucoma Market Insight

The U.S. PACG market captured the largest revenue share of 79.1% in 2024 within North America, fueled by the high prevalence of glaucoma and advanced ophthalmic healthcare infrastructure. Patients and healthcare providers increasingly prioritize early detection, timely intervention, and adoption of minimally invasive surgical procedures. The growing integration of AI-assisted diagnostics, optical coherence tomography (OCT), and tele-ophthalmology platforms further propels the PACG market. Moreover, the presence of leading ophthalmic device manufacturers and established specialty clinics ensures wide accessibility to both diagnostic and treatment solutions, supporting sustained market growth.

Canada Primary Angle-Closure Glaucoma Market Insight

The Canada PACG market is expected to grow at a notable CAGR during the forecast period, driven by increasing awareness of eye health among the aging population and rising adoption of advanced diagnostic and surgical procedures. Hospitals and specialty clinics in Canada are increasingly investing in AI-assisted imaging and minimally invasive interventions for PACG management. Moreover, favorable healthcare policies and reimbursement schemes encourage regular glaucoma screening and treatment adherence. Government initiatives promoting preventive ophthalmic care and collaborations with private clinics further support market expansion across the country.

Mexico Primary Angle-Closure Glaucoma Market Insight

The Mexico PACG market is anticipated to expand steadily during the forecast period, supported by growing investments in ophthalmic infrastructure and rising prevalence of glaucoma among the elderly population. Awareness programs on early detection and treatment, along with increasing accessibility to modern diagnostic tools, are driving market adoption. Hospitals and specialty clinics are focusing on tele-ophthalmology and portable diagnostic devices to enhance coverage in rural regions. In addition, partnerships with device manufacturers and healthcare providers are boosting availability of treatment options, including laser therapies and minimally invasive surgeries.

North America Primary Angle-Closure Glaucoma Market Share

The North America Primary Angle-Closure Glaucoma industry is primarily led by well-established companies, including:

- Johnson & Johnson Services, Inc. (U.S.)

- New World Medical, Inc. (U.S.)

- Sight Sciences, Inc. (U.S.)

- Bausch + Lomb (U.S.)

- MicroSurgical Technology, (U.S.)

- Reichert, Inc. (U.S.)

- Alcon Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceuticals Industries Ltd. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Fera Pharmaceuticals (U.S.)

- EyePoint Pharmaceuticals, Inc. (U.S.)

- Glaukos Corporation (U.S.)

- Nicox S.A. (France)

- Ocular Therapeutix, Inc. (U.S.)

What are the Recent Developments in North America Primary Angle-Closure Glaucoma Market?

- In October 2025, a retrospective longitudinal study found that patients with glaucoma may be at higher risk of developing dementia. This study highlights the importance of early diagnosis and management of glaucoma to potentially mitigate the risk of cognitive decline

- In October 2025, Avisi Technologies received FDA approval to initiate the SAPPHIRE trial, a prospective, multicenter, open-label clinical study evaluating the safety and effectiveness of the VisiPlate® aqueous shunt in glaucoma patients. The VisiPlate® shunt is uniquely designed with a novel metamaterial, thinner than a human hair, aiming for longevity, comfort, and aesthetics. Its multiple, redundant microchannels provide sustained aqueous flow while minimizing the risk of blockage and re-intervention

- In September 2025, a study published in Nature Communications identified functionally deficient UBOX5 variants as being associated with primary angle-closure glaucoma. This research suggests that genetic factors may play a significant role in the development of PACG, opening avenues for potential genetic screening and personalized treatment approaches

- In August 2025, a single-center, prospective, randomized controlled study sought to evaluate whether femtosecond laser-assisted cataract surgery (FLACS) in patients with primary angle-closure disease (PACD) was safe and if the predicted intraocular pressure (IOP) rise could have long-term effects. Patients enrolled in the study had stable PACD and prior laser peripheral iridotomy. They were randomized to receive FLACS, using a specific protocol, or conventional phacoemulsification cataract surgery

- In June 2025, the 12th Consensus Meeting on Angle Closure and Angle Closure Glaucoma was held in Honolulu, Hawaii, USA. This meeting brought together experts to discuss the latest advancements and challenges in the management of angle-closure glaucoma, including diagnostic techniques and treatment strategies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.