North America Sic Power Semiconductor Market

Market Size in USD Billion

USD

3.25 Billion

USD

20.94 Billion

2024

2032

USD

3.25 Billion

USD

20.94 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.25 Billion | |

| USD 20.94 Billion | |

| % | |

|

SiC Power Semiconductor Market Size

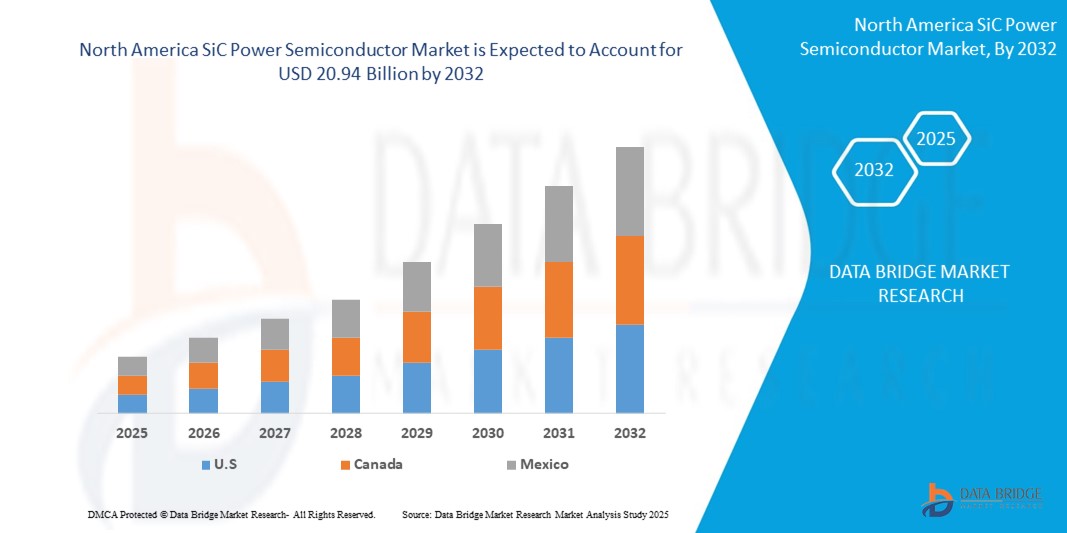

- The North America SiC power semiconductor market size was valued at USD 3.25 billion in 2024 and is expected to reach USD 20.94 billion by 2032, at a CAGR of 26.20% during the forecast period

- The market growth is largely fueled by the increasing demand for energy-efficient, high-performance power electronics across electric vehicles (EVs), renewable energy systems, and industrial applications, as industries prioritize lower energy losses and enhanced operational efficiency

- Furthermore, continuous technological advancements in SiC material quality, wafer production, and device performance are enabling wider deployment of SiC power semiconductors, with manufacturers leveraging these innovations to meet stringent performance, durability, and miniaturization requirements, thereby significantly boosting the market's growth

SiC Power Semiconductor Market Analysis

- SiC power semiconductors, offering superior energy efficiency, high thermal conductivity, and enhanced switching performance, are becoming critical components in electric vehicles, renewable energy systems, industrial motor drives, and next-generation power infrastructure due to their ability to operate at higher voltages, frequencies, and temperatures compared to conventional silicon-based devices

- The escalating demand for SiC power semiconductors is primarily fueled by the rapid adoption of electric mobility, increasing deployment of clean energy solutions, and the industry's growing need for compact, high-performance power electronics that reduce energy losses and enhance overall system efficiency

- U.S. dominated the SiC power semiconductor market with a share of 80.5% 2024, due to the country’s advanced electric vehicle (EV) production ecosystem, extensive renewable energy deployment, and strong presence of leading semiconductor manufacturers

- Mexico is expected to be the fastest growing region in the SiC power semiconductor market during the forecast period due to country’s growing automotive manufacturing base, combined with the rising focus on EV production and export capabilities

- SiC epitaxial wafers segment dominated the market with a market share of 67.8% in 2024, due to their critical role in ensuring high-quality, defect-free substrates essential for fabricating advanced SiC power devices. Epitaxial wafers provide superior electrical properties, including higher breakdown voltages and lower on-resistance, making them indispensable for automotive, energy, and industrial applications demanding high efficiency and reliability

Report Scope and SiC Power Semiconductor Market Segmentation

|

Attributes |

SiC Power Semiconductor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

SiC Power Semiconductor Market Trends

“Increasing Adoption in Electric Vehicles”

- A significant and accelerating trend in the North America SiC power semiconductor market is the widespread integration of SiC-based devices into electric vehicles (EVs), including traction inverters, DC-DC converters, and onboard chargers. This adoption is being driven by the superior efficiency, thermal performance, and power density of SiC technology compared to traditional silicon, enabling faster charging, lighter powertrains, and extended driving ranges

- For instance, companies such as Tesla, Ford, and GM have been incorporating SiC inverters into their EV platforms to enhance drivetrain efficiency and reduce overall system weight. SiC supplier Wolfspeed has established long-term supply agreements with major North American automakers, further reinforcing the trend

- The high-frequency switching capabilities of SiC power devices help reduce passive component sizes, leading to compact and lightweight system designs

- This is particularly beneficial in EV applications, where space, weight, and energy efficiency are key design considerations

- The shift toward mass EV production, spurred by supportive federal and state incentives in the U.S. and Canada, is driving automakers and component suppliers to prioritize SiC technology to meet performance demands and regulatory efficiency targets

- As a result, EV-related demand is becoming a primary growth engine for SiC power semiconductors in the region

SiC Power Semiconductor Market Dynamics

Driver

“Increasing Advancements in Renewable Energy”

- The rapid expansion of renewable energy infrastructure across North America—particularly solar photovoltaics and wind power—is a major driver of demand for SiC power semiconductors. These devices are increasingly deployed in high-efficiency solar inverters, smart grid interfaces, and energy storage systems due to their ability to minimize energy losses and operate reliably under high-voltage, high-temperature conditions

- For instance, in February 2024, Infineon Technologies announced the expansion of its CoolSiC product portfolio in collaboration with North American renewable energy developers. The new SiC-based solutions aim to enhance inverter efficiency and reduce energy losses in large-scale solar and wind installations, supporting the region's transition toward clean energy

- SiC’s faster switching speeds and high breakdown voltages enable more compact and efficient inverter designs for both residential and utility-scale solar applications. In wind energy, SiC devices are being used in converters to increase efficiency and reduce cooling requirements

- The growing need for grid modernization and the integration of distributed renewable sources are also fueling SiC adoption in grid-level applications

- Utilities and energy companies are increasingly seeking power devices that can handle fluctuating loads with higher reliability, and SiC semiconductors are meeting this demand by improving the performance and resilience of critical energy infrastructure

Restraint/Challenge

“High Initial Costs”

- Despite their performance advantages, SiC power semiconductors come with significantly higher manufacturing and material costs compared to traditional silicon-based devices, which presents a major restraint to their broader adoption. SiC substrates are more expensive to produce, have longer processing times, and involve complex fabrication steps, contributing to a higher final product cost

- For instance, Wolfspeed reported in its Q1 2024 earnings call that the cost of producing SiC wafers remains nearly five times higher than that of conventional silicon wafers, with large-scale cost reductions expected only as 8-inch wafer production ramps up and economies of scale improve

- This cost disparity can deter adoption in cost-sensitive applications such as basic power supplies, lower-end EV models, or industrial systems with tight budget constraints. While premium segments are willing to invest in SiC for efficiency gains, many mid-tier and emerging market players continue to rely on silicon alternatives to control capital expenditures

- Although the cost gap is narrowing due to increased production volume, transitions to larger wafer sizes (6-inch and above), and investments in vertical integration by players such as Infineon and Wolfspeed, price sensitivity remains a barrier

- Addressing this challenge will require scale efficiencies and also continuous innovation in fabrication processes and packaging technologies to bring down per-unit costs without compromising performance

SiC Power Semiconductor Market Scope

The market is segmented on the basis of type, voltage range, wafer size, wafer type, application, and vertical.

• By Type

On the basis of type, the North America SiC power semiconductor market is segmented into MOSFETs, hybrid modules, Schottky barrier diodes (SBDs), IGBT, bipolar junction transistors (BJT), PIN diodes, junction FETs (JFET), and others. The MOSFET segment is anticipated to dominate the market with the largest revenue share in 2024, driven by its superior switching performance, high efficiency, and ability to operate at elevated temperatures compared to silicon-based alternatives. Industries such as electric vehicles (EVs) and renewable energy strongly prefer SiC MOSFETs due to their capability to reduce system losses, enable compact system design, and lower cooling requirements. The demand is further reinforced by the growing push for energy-efficient power electronics across automotive and industrial sectors.

The hybrid modules segment is projected to witness the fastest growth rate from 2025 to 2032, propelled by the increasing adoption of integrated, high-performance modules that combine various SiC devices to deliver enhanced efficiency, thermal performance, and reliability. These modules are especially favored in high-voltage applications such as EV traction systems, renewable energy infrastructure, and smart grids, where compactness, durability, and operational efficiency are critical.

• By Voltage Range

Based on voltage range, the market is segmented into 301-900 V, 901-1700 V, and above 1701 V. The 901-1700 V segment captured the largest revenue share in 2024, largely due to its extensive use in electric vehicles, industrial motor drives, and high-power renewable energy systems. This voltage range offers an optimal balance between power handling capability and efficiency, making it the preferred choice for manufacturers seeking to optimize performance while maintaining manageable design complexity.

The above 1701 V segment is expected to register the fastest growth from 2025 to 2032, fueled by rising demand in heavy industrial applications, high-voltage grids, and rail transportation systems. The superior breakdown strength and thermal resilience of SiC components in this voltage category support their deployment in high-stress environments where conventional silicon devices often fall short.

• By Wafer Size

On the basis of wafer size, the market is segmented into 6-inch, 4-inch, 2-inch, and above 6-inch categories. The 6-inch wafer segment accounted for the largest revenue share in 2024, attributed to its maturity in mass production and its role in reducing manufacturing costs through higher device yield per wafer. The shift toward 6-inch wafers is supported by efforts to scale production volumes and lower the cost per SiC component, particularly for automotive and industrial power electronics.

The above 6-inch wafer segment is projected to experience the fastest growth during the forecast period, driven by industry investments in larger wafer technology to further enhance production efficiency and address the escalating demand for high-performance SiC devices. Larger wafers enable greater economies of scale, contributing to the broader affordability and adoption of SiC semiconductors across high-growth markets such as EVs and renewable energy.

• By Wafer Type

The market is segmented into SiC epitaxial wafers and blank SiC wafers. SiC epitaxial wafers dominated the market with the largest revenue share of 67.8% in 2024, owing to their critical role in ensuring high-quality, defect-free substrates essential for fabricating advanced SiC power devices. Epitaxial wafers provide superior electrical properties, including higher breakdown voltages and lower on-resistance, making them indispensable for automotive, energy, and industrial applications demanding high efficiency and reliability.

The blank SiC wafer segment is expected to witness the fastest growth from 2025 to 2032, as ongoing advancements in wafer production technology improve material quality and cost efficiency. These wafers form the foundational substrate for both research and commercial device manufacturing, with growing utilization in prototyping and next-generation device development.

• By Application

On the basis of application, the market is segmented into electric vehicles (EV), photovoltaics, power supplies, industrial motor drives, EV charging infrastructure, RF devices, and others. The electric vehicle (EV) segment dominated the market revenue share in 2024, driven by the accelerating transition toward vehicle electrification and the rising need for efficient, lightweight powertrain solutions. SiC devices are highly sought after for their ability to extend driving range, reduce energy losses, and enable fast charging capabilities, aligning with the North American automotive sector’s focus on sustainable mobility.

The EV charging infrastructure segment is poised to exhibit the fastest growth through 2032, spurred by increasing investments in fast-charging networks and the need for high-efficiency power electronics to support widespread EV adoption. SiC power semiconductors enhance the performance and reliability of charging stations, enabling higher voltage operations and faster energy transfer, essential for meeting consumer expectations around EV charging convenience.

• By Vertical

The North America SiC power semiconductor market is segmented by vertical into automotive, utilities and energy, industrial, transportation, IT and telecommunication, consumer electronics, aerospace and defense, commercial, and others. The automotive segment secured the largest revenue share in 2024, underpinned by growing EV production and manufacturers’ focus on energy-efficient, high-performance powertrains. SiC technology is pivotal in reducing system weight, improving energy conversion efficiency, and supporting advanced vehicle electrification, contributing to its dominance in this vertical.

The utilities and energy segment is expected to grow at the fastest pace from 2025 to 2032, fueled by rising deployment of renewable energy systems, smart grids, and energy storage solutions. SiC devices facilitate more efficient power conversion and transmission, crucial for achieving grid stability, minimizing energy losses, and supporting North America’s transition toward clean energy targets.

SiC Power Semiconductor Market Regional Analysis

- U.S. dominated the SiC power semiconductor market with the largest revenue share of 80.5% in 2024, driven by the country’s advanced electric vehicle (EV) production ecosystem, extensive renewable energy deployment, and strong presence of leading semiconductor manufacturers

- High demand for energy-efficient power electronics in EVs, smart grids, and industrial motor drives continues to fuel market growth across the nation

- Government incentives supporting domestic chip production and carbon reduction targets further amplify investments in SiC technologies, solidifying the U.S. as a key growth hub for next-generation power semiconductors

Canada SiC Power Semiconductor Market Insight

The Canada SiC power semiconductor market is expected to experience steady growth from 2025 to 2032, supported by increasing electrification initiatives across transportation and energy sectors. The country's commitment to clean energy expansion, along with investments in EV charging infrastructure and smart grid modernization, is driving demand for high-performance SiC devices. Canada’s emphasis on reducing carbon emissions, coupled with rising interest in industrial energy efficiency, is creating favorable conditions for the broader adoption of SiC-based power electronics.

Mexico SiC Power Semiconductor Market Insight

Mexico is projected to register the fastest CAGR in the North America SiC power semiconductor market during the forecast period of 2025 to 2032. The country’s growing automotive manufacturing base, combined with the rising focus on EV production and export capabilities, is significantly boosting demand for SiC components. Mexico’s strategic location within North American supply chains and government incentives to attract semiconductor investments are accelerating market development. Increasing efforts to enhance industrial energy efficiency and modernize electrical infrastructure further support the expanding application of SiC power semiconductors across the nation.

SiC Power Semiconductor Market Share

The SiC power semiconductor industry is primarily led by well-established companies, including:

- WOLFSPEED, INC. (U.S.)

- STMicroelectronics (Switzerland)

- ROHM CO., LTD. (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Texas Instruments Incorporated (U.S.)

- Infineon Technologies AG (Germany)

- Semikron Danfoss (Germany)

- Renesas Electronics Corporation (Japan)

- TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION (Japan)

- Microchip Technology Inc. (U.S.)

- Semiconductor Components Industries, LLC (U.S.)

- NXP Semiconductors (Netherlands)

- UnitedSiC (U.S.)

- SemiQ Inc. (U.S.)

- Littelfuse, Inc. (U.S.)

- Allegro MicroSystems, Inc. (U.S.)

- Hitachi Power Semiconductor Device, Ltd. (Japan)

- GeneSiC Semiconductor Inc. (U.S.)

Latest Developments in North America SiC Power Semiconductor Market

- In December 2022, STMicroelectronics and Soitec announced the next stage of their cooperation on Silicon Carbide (SiC) substrates, with ST planning to qualify Soitec's SiC substrate technology over the next 18 months. This collaboration aims for the adoption of Soitec's SmartSiC technology for ST's future 200mm substrate manufacturing, supporting its devices and modules manufacturing. The volume production is expected in the midterm, potentially boosting ST's financials and contributing to the growth of the North America SiC power semiconductor market

- In July 2022, Semikron Danfoss and ROHM Semiconductor, after a decade-long collaboration, advanced their partnership with the qualification of ROHM's latest 4th generation SiC MOSFETs in SEMIKRON's eMPack modules for automotive applications. This collaboration serves global customer needs, enhances both companies' financials, and positively impacts the North America SiC power semiconductor market

- In August 2022, Toshiba Corporation launched its 3rd generation 650V and 1200V silicon carbide MOSFETs, which achieve a 20% reduction in switching losses in industrial equipment. This innovation aims to improve the efficiency and performance of industry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Sic Power Semiconductor Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Sic Power Semiconductor Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Sic Power Semiconductor Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.