North America Vaccine Administration Devices Market

Market Size in USD Billion

USD

2.24 Billion

USD

4.31 Billion

2024

2032

USD

2.24 Billion

USD

4.31 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.24 Billion | |

| USD 4.31 Billion | |

| % | |

|

North America Vaccine Administration Devices Market Size

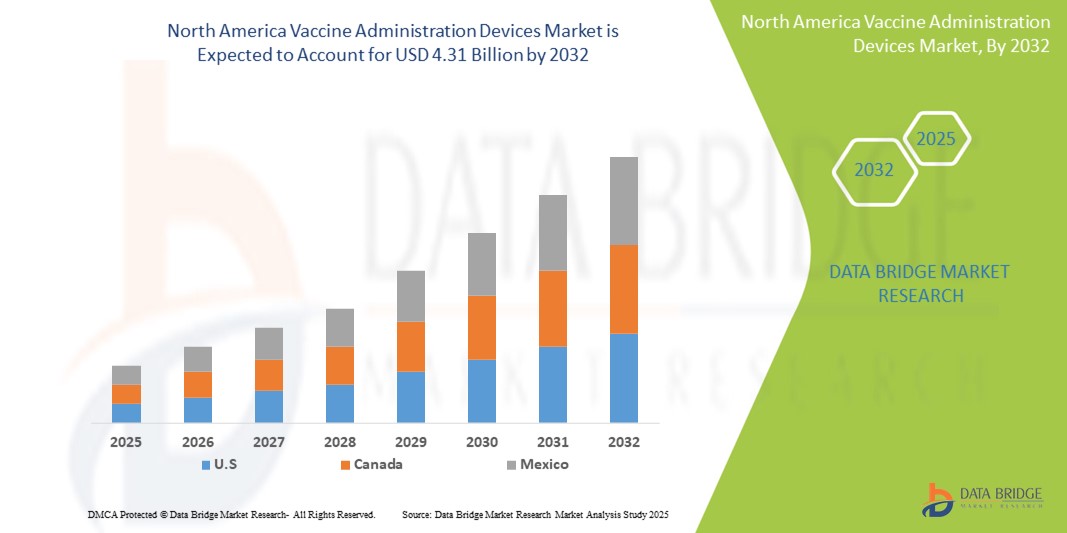

- The North America vaccine administration devices market size was valued at USD 2.24 billion in 2024 and is expected to reach USD 4.31 billion by 2032, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by the increasing focus on immunization programs globally, rising prevalence of infectious diseases, and growing awareness about preventive healthcare

- Furthermore, technological advancements in vaccine delivery systems, such as auto-disable syringes, needle-free injectors, and prefilled devices, are enhancing safety, efficacy, and patient compliance. These factors are accelerating the adoption of vaccine administration devices, thereby significantly boosting the industry’s growth

North America Vaccine Administration Devices Market Analysis

- Vaccine administration devices, including auto-injectors, prefilled syringes, and safety needles, are increasingly vital components of modern healthcare delivery in both hospital and outpatient settings due to their enhanced precision, ease of use, patient safety features, and efficiency in vaccine administration

- The escalating demand for Vaccine Administration Devices is primarily fueled by the growing need for efficient immunization programs, rising prevalence of infectious diseases, and increasing government and private sector focus on vaccination coverage in both adults and children

- U.S. dominated the vaccine administration devices market with the largest revenue share of 40.5% in 2024, supported by advanced healthcare infrastructure, high adoption of modern vaccination practices, strong R&D activities, and the presence of leading device manufacturers. The country experienced substantial growth due to widespread immunization campaigns, continuous innovations in prefilled syringes, auto-disable syringes, and safety-engineered injection devices, which enhance patient safety and reduce administration errors

- Canada is expected to be the fastest-growing country in the vaccine administration devices market during the forecast period, projected to expand at a CAGR of 11.2% from 2025 to 2032. This growth is supported by rising government initiatives to improve vaccination coverage, increasing awareness of preventive healthcare, and the growing adoption of advanced vaccine delivery systems in public and private healthcare settings

- The Disposable segment dominated the vaccine administration devices market with the largest market revenue share of 62.4% in 2024, driven by safety benefits, ease of use, and alignment with public health protocols. Disposable devices, such as prefilled syringes and auto-disable injections, minimize contamination risks, reduce cross-infection, and simplify workflow in hospitals, clinics, and mass immunization campaigns

Report Scope and Vaccine Administration Devices Market Segmentation

|

Attributes |

Vaccine Administration Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Vaccine Administration Devices Market Trends

Enhanced Convenience and Efficiency in Vaccine Delivery

- A significant and accelerating trend in the North America vaccine administration devices market is the adoption of devices that enhance convenience, accuracy, and safety during vaccine administration. These devices improve patient compliance, reduce dosing errors, and streamline workflow in both hospital and outpatient settings

- For instance, auto-disable syringes and prefilled devices allow healthcare providers to deliver precise doses with minimal preparation, reducing the risk of contamination and ensuring safe handling. Prefilled syringes from companies such as BD and Gerresheimer have been widely adopted for large-scale immunization programs

- Innovations in needle-free injectors and jet injectors provide pain-free, rapid vaccine delivery, making them particularly suitable for pediatric and mass vaccination campaigns. These technologies are increasingly preferred for their ease of use and reduction in needle-stick injuries

- Safety-engineered devices, including retractable needles and auto-shielding mechanisms, are enhancing the protection of healthcare workers and patients alike, reducing the risk of accidental injuries and improving overall workplace safety

- Companies such as Becton Dickinson, Terumo, and West Pharmaceutical Services are actively developing advanced delivery devices that combine reliability, usability, and patient comfort, driving adoption across North America

- The growing demand for efficient vaccine administration is further supported by public health initiatives, increasing vaccination rates, and the need for rapid immunization in response to outbreaks and seasonal diseases

- Integration of ergonomic and user-friendly designs in auto-injectors and prefilled devices is improving the patient experience and simplifying administration for healthcare providers, particularly in high-volume settings

- The trend toward standardized, ready-to-use vaccine delivery systems is reshaping expectations for healthcare efficiency and safety, with both government and private healthcare providers prioritizing adoption of these advanced devices

North America Vaccine Administration Devices Market Dynamics

Driver

Growing Need Due to Rising Healthcare Safety and Efficient Vaccine Delivery

- The increasing prevalence of vaccine-preventable diseases, coupled with the growing focus on public health initiatives, is a significant driver for the heightened demand for advanced Vaccine Administration Devices

- For instance, in April 2024, BD (Becton Dickinson) announced the launch of its new prefilled safety syringe platform, designed to reduce dosing errors and enhance safety during mass immunization campaigns. Such strategies by key companies are expected to drive the vaccine administration devices industry growth in the forecast period

- As healthcare providers aim to improve patient compliance and minimize administration errors, modern devices such as auto-disable syringes, safety-engineered needles, and jet injectors provide precision dosing and safer handling

- Furthermore, the rising adoption of vaccination programs in hospitals, clinics, and community health centers is accelerating demand for devices that ensure consistent and reliable vaccine delivery, enhancing overall healthcare efficiency

- The convenience of ready-to-use prefilled devices, coupled with ergonomic designs for healthcare workers, is increasing adoption in both large-scale immunization drives and routine clinical practice

- Safety-engineered devices with retractable needles and auto-shielding mechanisms are particularly important for protecting healthcare professionals from accidental needle-stick injuries and improving workplace safety

- The ongoing development of needle-free injectors and innovative delivery technologies is enabling faster, pain-free administration, making vaccines more acceptable to patients, including children and the elderly

- Increasing government initiatives, rising awareness of immunization benefits, and growing demand for standardized, user-friendly vaccine delivery systems further contribute to market growth

Restraint/Challenge

Concerns Regarding Device Costs and Regulatory Compliance

- High initial costs of advanced vaccine administration devices can be a barrier for adoption, particularly in developing regions or smaller healthcare facilities with budget constraints

- The complex regulatory requirements for device approval in North America and other regions can slow product launches and delay market penetration for new technologies

- Ensuring sterility, accurate dosing, and consistent device performance requires strict compliance with FDA and health authority guidelines, which adds to manufacturing and operational costs

- Training healthcare staff to use advanced delivery devices effectively can be time-consuming, posing challenges to rapid adoption in high-volume clinical settings

- While innovations improve safety and convenience, perceived higher costs compared to conventional syringes or needles may make some institutions hesitant to upgrade immediately

- Limited availability of certain advanced vaccine administration devices in rural or remote areas can hinder widespread adoption, creating disparities in access to safer and more efficient delivery system

- Supply chain disruptions, including shortages of raw materials and logistical challenges, may delay the production and distribution of advanced devices, affecting timely vaccine administration

- Overcoming these challenges through cost-effective manufacturing, streamlined regulatory approvals, targeted healthcare provider education, and enhanced supply chain management will be vital for sustained growth of the Vaccine Administration Devices market

North America Vaccine Administration Devices Market Scope

The market is segmented on the basis of product, route of administration, type, brand, dosage, vaccine type, modality, usability, end user, and distribution channel.

- By Product

On the basis of product, the North America vaccine administration devices market is segmented into syringes, auto injectors, jet injectors, micro needles, inhalation/pulmonary delivery, microinjection system, pen injector devices, biodegradable implants, electroporation-based needle free injection systems, buccal/sublingual vaccine delivery systems, auto-injector trainer devices, and others devices. The syringes segment dominated the largest market revenue share of 41.2% in 2024. Syringes are widely used in hospitals, clinics, and community vaccination programs due to their ease of use, cost-effectiveness, and compatibility with multiple vaccine types. Prefilled syringes reduce preparation time and contamination risks while ensuring accurate dosing. Safety-engineered designs prevent needle reuse, enhancing patient safety. Routine immunization programs, government campaigns, and public health initiatives further reinforce the dominance of syringes. Their adaptability to intramuscular, subcutaneous, and intradermal delivery adds versatility. Syringes continue to be the preferred choice for large-scale immunization programs. Ongoing innovations such as auto-disable and prefilled designs improve operational efficiency.

The Auto Injectors segment is expected to witness the fastest CAGR of 19.5% from 2025 to 2032. Auto injectors provide user-friendly, self-administrable solutions suitable for homecare and emergency vaccination. They reduce administration errors and enhance dosing accuracy. The portability and compact design support outpatient care and home-based immunization programs. Technological improvements, including spring-assisted mechanisms and integrated safety features, increase usability. Growing awareness of needle-phobia alternatives encourages adoption. Auto injectors also support chronic disease management and vaccination in remote areas. Rising public health initiatives and telehealth integration further accelerate growth. Their convenience and ease of use position them as the fastest-growing product sub-segment.

- By Route of Administration

On the basis of route of administration, the vaccine administration devices market is segmented into intramuscular, subcutaneous, and intradermal. The Intramuscular segment dominated the largest market revenue share of 47.1% in 2024. Intramuscular devices are used for a broad range of vaccines, including influenza, tetanus, and COVID-19 vaccines. They ensure rapid absorption and robust immune responses. Hospitals and community health centers rely on these devices due to standardized training and familiarity. Prefilled syringes and auto-injectors reduce errors and contamination risks. Government vaccination programs reinforce segment dominance. Ease of standardization and compatibility with various vaccine delivery devices further support growth. Intramuscular administration is widely preferred for routine immunizations and mass campaigns. Efficiency and proven efficacy make it the most trusted route.

The subcutaneous segment is expected to witness the fastest CAGR of 18.4% from 2025 to 2032. Subcutaneous devices are preferred for vaccines requiring slower absorption, such as MMR and biologics. They minimize discomfort and support home-based administration. Auto-injectors and safety-engineered devices enhance usability. School-based immunization and community vaccination programs increase adoption. Technological advancements improve accuracy and reduce errors. The segment’s versatility makes it suitable for outpatient and remote care. Growing awareness of self-administration encourages adoption. Its convenience and minimal invasiveness drive the fastest growth in this category.

- By Type

On the basis of type, the vaccine administration devices market is segmented into marketed vaccines and clinical-stage vaccines (electroporation). The Marketed Vaccines segment dominated the largest market revenue share of 62.3% in 2024. Marketed vaccines include widely approved vaccines for influenza, measles, polio, and pneumococcal diseases. They benefit from established safety profiles and regulatory approval. Hospitals, clinics, and public health programs rely heavily on marketed vaccines for routine immunization. Prefilled syringes and auto-injectors improve dosing accuracy and minimize errors. Integration with electronic health records facilitates tracking and compliance. Government vaccination campaigns reinforce segment dominance. Ongoing public awareness campaigns support adoption. Continuous technological innovations improve usability and patient safety.

The Clinical-Stage Vaccines (Electroporation) segment is expected to witness the fastest CAGR of 20.5% from 2025 to 2032. Electroporation devices deliver DNA and gene-based vaccines directly into cells for enhanced immune response. Growing R&D in therapeutic and personalized vaccines accelerates adoption. Clinical trials and biotech collaborations expand applications. Safety-engineered and automated devices improve comfort and usability. Technological advancements reduce errors and facilitate controlled dosing. Interest in novel immunotherapies fuels growth. Precision delivery supports emerging infectious disease management. This segment represents the fastest-growing category due to innovation and emerging applications.

- By Brand

On the basis of brand, the vaccine administration devices market is segmented into BD Accuspray Nasal Spray System, BD Hypak for Vaccines Glass Pre-Fillable Syringe System, BD Uniject Auto-Disable Pre-Fillable Injection System, Gx InnoSafe, Gx RTF ClearJect, Plajex, and Others. The BD Uniject Auto-Disable Pre-Fillable Injection System dominated the largest market revenue share of 38.7% in 2024. Its safety-engineered design prevents needle reuse, making it suitable for mass immunization. The system is portable, easy to use, and ensures accurate dosing. Widely adopted in public and private healthcare, it aligns with WHO safety guidelines. Prefilled syringes reduce preparation errors and streamline workflows. Hospitals, clinics, and community programs extensively use BD Uniject. Continuous ergonomic improvements support consistent usage. Integration with safety protocols reinforces dominance. Its reliability and ease of administration strengthen its market position.

The Gx InnoSafe segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032. Gx InnoSafe’s modular, user-friendly auto-injectors support homecare and community vaccination. Its safety features reduce risks and improve patient compliance. Rising adoption in outpatient and remote programs drives growth. Technological improvements enhance convenience and accuracy. Awareness of needle safety and training initiatives encourage adoption. Expansion in chronic disease management and self-administration boosts growth. Compatibility with multiple vaccine types accelerates uptake. This segment’s rapid adoption makes it the fastest-growing brand.

- By Dosage

On the basis of dosage, the vaccine administration devices market is segmented into fixed and variable. The Fixed Dosage segment dominated the largest market revenue share of 52.4% in 2024. Fixed dosing ensures standardized vaccine administration, consistent immune responses, and regulatory compliance. Prefilled syringes and auto-injectors reduce errors and wastage. Hospitals, clinics, and immunization campaigns prefer fixed dosage for mass vaccination. Integration with safety-engineered systems enhances patient protection. Reliable performance, ease of use, and prefilled convenience reinforce dominance. Government-led initiatives support adoption. Continuous use in public health programs further strengthens its leadership. Operational efficiency is maximized in high-volume immunization programs.

The Variable Dosage segment is expected to witness the fastest CAGR of 18.3% from 2025 to 2032. Variable dosing enables personalized immunization strategies in clinical trials, specialty vaccines, and research settings. Adjustable auto-injectors and digital dose monitoring enhance precision. Growing interest in patient-centric care supports adoption. Home-based and flexible dosing programs increase demand. Technological innovations improve usability and safety. Emerging therapies and experimental vaccines further accelerate growth. Adaptability to patient requirements positions this segment for rapid expansion. Its flexibility and precision make it the fastest-growing dosage sub-segment.

- By Vaccine Type

On the basis of vaccine type, the vaccine administration devices market is segmented into Bivalent Oral Polio Vaccine, B.C.G. Vaccine, Tetanus-Diphtheria Vaccine, DTP-HEPB-HIB Vaccine, Influenza Vaccine, Pneumococcal Conjugate Vaccine, Measles Vaccine, and Others. The Influenza Vaccine segment dominated the largest market revenue share of 28.9% in 2024. Annual vaccination campaigns, strong government initiatives, and widespread public awareness drive adoption. Prefilled syringes and auto-injectors ensure safe, accurate, and rapid administration. Hospitals, clinics, and community centers extensively rely on influenza vaccines. The consistency and efficiency of device-based delivery reduce errors. Routine seasonal programs reinforce segment leadership. Standardized devices ensure patient safety and operational efficiency. Technological innovations such as safety-engineered syringes enhance reliability. Influenza vaccination programs remain a cornerstone of public health immunization efforts.

The Pneumococcal Conjugate Vaccine segment is expected to witness the fastest CAGR of 17.9% from 2025 to 2032. Pediatric and elderly populations drive demand. School-based immunization programs, preventive healthcare awareness, and advanced delivery devices accelerate adoption. Prefilled syringes and auto-injectors improve dosing accuracy and safety. Increased focus on community health and preventive care supports growth. Technological improvements enhance usability and accessibility in homecare and clinical settings. Rising awareness of respiratory disease prevention boosts uptake. Public health initiatives reinforce rapid expansion. This segment is positioned as the fastest-growing vaccine type.

- By Modality

On the basis of modality, the vaccine administration devices market is segmented into automatic vaccine administration device and manual vaccine administration device. The automatic vaccine administration device segment dominated the largest market revenue share of 55.7% in 2024. Automated systems reduce errors, improve dosing consistency, and enhance workflow efficiency. Prefilled syringes and auto-injectors support large-scale immunization in hospitals and community clinics. Government vaccination programs reinforce dominance. Integration into standardized healthcare protocols ensures patient safety. Technological improvements such as spring-assisted and digital monitoring systems enhance usability. High-volume immunization campaigns benefit from automated delivery. Operational efficiency and reliability strengthen leadership.

The Manual Vaccine Administration Device segment is expected to witness the fastest CAGR of 16.8% from 2025 to 2032. Manual devices are cost-efficient, portable, and flexible, ideal for low-resource and remote healthcare settings. Emergency and outpatient immunization programs rely on manual administration. Technological improvements in ergonomics and safety increase usability. Community-based vaccination initiatives expand adoption. Remote healthcare delivery benefits from manual devices. Growing awareness of self-administration encourages usage. Flexibility and accessibility drive rapid growth. This sub-segment is positioned as the fastest-growing modality category.

- By Usability

On the basis of usability, the vaccine administration devices market is segmented into disposable and reusable. The Disposable segment dominated the largest market revenue share of 62.4% in 2024. Single-use devices reduce contamination risks, prevent cross-infection, and align with public health protocols. Prefilled syringes and auto-disable systems ensure accurate dosing and compliance. Hospitals, clinics, and mass immunization campaigns benefit from ease of use and operational efficiency. Government initiatives reinforce adoption. Safety-engineered designs minimize errors and wastage. Continuous technological improvements support workflow efficiency. The disposable segment remains the preferred choice across healthcare settings. Standardized and single-use features strengthen dominance.

The Reusable segment is expected to witness the fastest CAGR of 15.6% from 2025 to 2032. Reusable devices are adopted in research, clinical trials, and specialized healthcare programs where sustainability and cost efficiency are prioritized. Multiple administration capability reduces medical waste. Advanced cleaning, sterilization, and ergonomic designs improve usability. Controlled experimental programs benefit from flexible dosing. Technological innovations enhance safety and reliability. Cost-effective and environmentally conscious healthcare solutions drive growth. Reusable devices are positioned as the fastest-growing usability sub-segment.

- By End User

On the basis of end user, the vaccine administration devices market is segmented into hospitals, community centers, homecare setting, research and academic institutes, ambulatory surgical center, and others. The hospitals segment dominated the largest market revenue share of 54.3% in 2024. Hospitals utilize vaccine administration devices for large-scale immunization programs and routine vaccination schedules. Controlled environments, trained personnel, and standardized protocols ensure accuracy. Prefilled syringes, auto-injectors, and safety-engineered systems enhance efficiency. Government-led campaigns reinforce segment dominance. Seasonal vaccination drives strengthen adoption. Integration with modern technologies supports workflow optimization. Hospitals are the primary hub for vaccine administration. Continuous adoption of advanced devices maintains leadership.

The Homecare Setting segment is expected to witness the fastest CAGR of 14.9% from 2025 to 2032. Homecare vaccination programs offer patient-centric solutions for individuals with mobility limitations or chronic illnesses. Portable auto-injectors, prefilled syringes, and safety-engineered devices support safe, accurate, and convenient administration. Telehealth, remote monitoring, and awareness campaigns encourage adoption. Flexibility and convenience drive growth. Patient preference for at-home care increases market potential. Homecare infrastructure expansion supports uptake. Rising demand for accessible healthcare solutions accelerates growth. The homecare segment is positioned as the fastest-growing end-user category.

- By Distribution Channel

On the basis of distribution channel, the vaccine administration devices market is segmented into direct tender and retail sales. The Direct Tender segment dominated the largest market revenue share of 57.6% in 2024. Government procurement programs, hospital tenders, and bulk supply agreements ensure large-volume, reliable distribution. Standardized supply chains, competitive pricing, and streamlined logistics support uninterrupted vaccine administration. Strategic partnerships between manufacturers and government agencies reinforce dominance. Integration with national immunization programs strengthens adoption. Large-scale healthcare initiatives sustain market leadership. Direct tender ensures consistent delivery to public healthcare facilities. Bulk procurement facilitates cost-efficiency. Government-backed campaigns maintain segment prominence.

The Retail Sales segment is expected to witness the fastest CAGR of 13.8% from 2025 to 2032. Retail distribution improves access to vaccination devices through pharmacies, online platforms, and private healthcare providers. Convenience, rapid availability, and flexibility drive adoption. Self-administration trends and homecare vaccination programs boost retail demand. Technological improvements in prefilled syringes and auto-injectors enhance usability. Awareness campaigns and marketing initiatives increase uptake. Small healthcare facilities and outpatient clinics benefit from retail channels. Growing preventive healthcare adoption supports growth. Retail Sales is the fastest-growing distribution channel segment.

North America Vaccine Administration Devices Market Regional Analysis

- North America dominated the vaccine administration devices market with the largest revenue share in 2024, driven by advanced healthcare infrastructure, widespread immunization programs, and the presence of leading device manufacturers

- Consumers and healthcare providers in the region highly value innovations such as prefilled syringes, auto-disable syringes, and safety-engineered injection devices, which enhance patient safety, reduce administration errors, and improve efficiency in both public and private healthcare settings

- This widespread adoption is further supported by strong R&D activities, government vaccination initiatives, and rising awareness of preventive healthcare, establishing advanced vaccine delivery systems as the preferred choice for immunization programs across North America

U.S. Vaccine Administration Devices Market Insight

The U.S. vaccine administration devices market captured the largest revenue share of 40.5% in 2024 within North America, fueled by substantial growth in prefilled syringes, auto-disable syringes, and safety-engineered injection devices. The country experienced significant expansion due to continuous immunization campaigns, technological innovations by leading manufacturers such as BD, Gerresheimer, and West Pharmaceutical Services, and robust healthcare infrastructure. Ongoing research and development initiatives, along with increasing patient and provider awareness, are further propelling the growth of the U.S. Vaccine Administration Devices industry.

Canada Vaccine Administration Devices Market Insight

The Canada vaccine administration devices market is expected to be the fastest-growing country in the Vaccine Administration Devices market during the forecast period, projected to expand at a CAGR of 11.2% from 2025 to 2032. The growth is supported by rising government initiatives to improve vaccination coverage, increasing adoption of advanced delivery systems in public and private healthcare settings, and growing awareness of preventive healthcare practices. Expanding healthcare infrastructure, technological innovations, and targeted funding for immunization programs in remote regions are expected to further drive market expansion in Canada.

North America Vaccine Administration Devices Market Share

The vaccine administration devices industry is primarily led by well-established companies, including:

- B.D. (U.S.)

- INOVIO Pharmaceuticals (U.S.)

- Vaxxas (U.S.)

- Gerresheimer AG (Germany)

- Corium Inc. (U.S.)

- Enesi (U.S.)

- Micropoint Technologies (Singapore)

- SCHOTT AG (Germany)

- 3M (U.S.)

- Mystic Pharmaceuticals (U.S.)

- NanoPass Rev (U.S.)

- Terumo North America NV (Belgium)

- West Pharmaceutical Services, Inc. (U.S.)

- Viatris Inc. (U.S.)

- Medical International Technologies Inc. (Canada)

- Antares Pharma (U.S.)

Latest Developments in North America Vaccine Administration Devices Market

- In September 2024, the U.S. Food and Drug Administration (FDA) approved AstraZeneca's nasal spray flu vaccine, FluMist, for self-administration. This marked the first vaccine of its kind that does not require administration by healthcare providers. AstraZeneca distributed the vaccine through a third-party online pharmacy, allowing customers to complete a screening and eligibility assessment online. This approval aimed to enhance convenience, flexibility, and accessibility for receiving the seasonal flu vaccine

- In June 2024, the U.S. Food and Drug Administration (FDA) approved Merck's new pneumococcal vaccine, Capvaxive, for adults. This vaccine targets 21 serotypes of the bacteria that cause pneumococcal disease, which can lead to serious infections such as pneumonia. Capvaxive has demonstrated effectiveness across various adult demographics in clinical studies. The vaccine is priced at USD 287 per dose, but many individuals may receive it at no cost if recommended by the Centers for Disease Control and Prevention (CDC). The CDC discussed this recommendation later that month, and the vaccine was expected to be available by late summer

- In August 2025, AstraZeneca launched FluMist Home, a nasal spray flu vaccine with at-home delivery service. This service allows eligible individuals to receive the vaccine without visiting a clinic—ideal for those with needle phobia. FluMist Home is accessible in 34 U.S. states and can be self-administered by adults aged 18-49 or by caregivers to children aged 2-17. Eligible users complete an online medical screening questionnaire to determine eligibility and obtain a prescription. Once approved, the vaccine is shipped to their home with full instructions and storage guidance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.