Global Api Contract Manufacturing Market

市场规模(十亿美元)

CAGR :

%

USD

8.10 Billion

USD

12.57 Billion

2024

2032

USD

8.10 Billion

USD

12.57 Billion

2024

2032

| 2025 –2032 | |

| USD 8.10 Billion | |

| USD 12.57 Billion | |

| % | |

|

全球 API 合約製造市場細分,按類型(有機、無機、其他)、產量(低、大、中、其他)、形態(固體、液體、半固體、其他)、最終用戶(製藥業、研究機構、其他)、分銷管道(直接投標、零售商、其他)——行業趨勢及預測(至 2032 年)

API合約製造市場規模

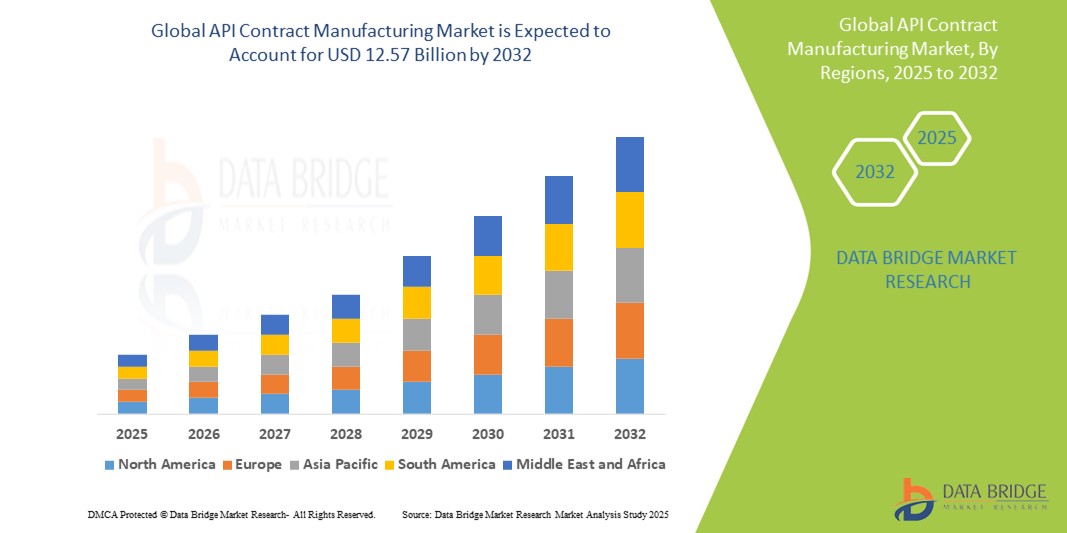

- 2024 年全球 API 合約製造市場規模為81 億美元 ,預計 到 2032 年將達到 125.7 億美元,預測期內 複合年增長率為 5.87%。

- 製藥公司越來越多地將 API 生產外包,以提高成本效率、簡化營運並確保遵守法規,從而推動了市場擴張

- 此外,各治療領域對高品質、價格合理的API的需求不斷增長,加之藥物配方日益複雜,促使創新藥和仿製藥製造商都依賴專業的合約生產組織(CMO)。這一趨勢正在推動全球市場的發展,尤其是在擁有強大製造能力和監管適應能力的新興市場。

API合約製造市場分析

- API合約製造是指將活性藥物成分的生產外包給第三方製造商,使製藥公司能夠降低成本、提高可擴展性,並專注於研發和商業化等核心競爭力。這些服務對於滿足嚴格的監管標準和確保持續供應高品質的API至關重要。

- API合約製造需求的不斷增長,源自於藥物分子日益複雜的特性、藥物開發成本壓力,以及製藥公司將非核心業務外包給專業合約製造組織(CMO)的趨勢日益增長。而對產能彈性和全球供應鏈優化的需求,則進一步推動了這項需求的成長。

- 北美目前在API合約製造市場中處於領先地位,2025年其營收份額將達到37.5%,位居全球首位。這得歸功於北美大型製藥公司的強大影響力、先進的製造基礎設施以及嚴格的監管。尤其在美國,由於開發成本上升和專利懸崖,品牌藥和仿製藥開發商的外包需求持續成長。

- 預計亞太地區將成為預測期內市場成長最快的地區,這得益於低成本製造能力、政府對醫藥出口的支持以及 FDA 和 EMA 批准的生產設施的增加,尤其是在印度和中國等國家。

- 在所有類型中,有機 API 部分預計將在 2025 年佔據市場主導地位,市場份額為 45.6%,這得益於有機化合物在藥物製劑中的廣泛使用以及大量依賴傳統化學合成路線的仿製藥。

報告範圍和 API 合約製造市場細分

|

屬性 |

API合約製造關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

API合約製造市場趨勢

“戰略合作夥伴關係和複雜API產能擴張”

- 全球API合約製造市場的一個重要且日益增長的趨勢是,對產能擴張和合作夥伴關係的策略投資,主要集中在複雜高效API(HPAPI)的生產。這些措施旨在滿足腫瘤、神經病學和自體免疫疾病領域對特種藥物和標靶治療日益增長的需求。

- For instance, in 2024, Piramal Pharma Solutions announced an expansion of its API manufacturing capabilities in Aurora, Canada, specifically targeting HPAPIs and complex molecules. Similarly, Lonza Group has continuously invested in scalable containment facilities to attract large-scale HPAPI contracts from global pharma companies.

- With the increase in biologics, antibody-drug conjugates (ADCs), and highly targeted drug therapies, CMOs are enhancing their offerings to include integrated development services, multi-product lines, and modular containment suites to manufacture niche APIs safely and efficiently.

- Moreover, partnerships between CMOs and pharmaceutical giants are growing in importance. These collaborations often include technology transfers, long-term supply agreements, and joint investments, enabling innovators to reduce time-to-market and avoid capital expenditure while ensuring compliance with regulatory standards.

- This trend toward specialization and collaboration is reshaping the competitive landscape of API manufacturing, especially in North America, Europe, and Asia-Pacific. Companies such as Cambrex, Siegfried, and Wuxi STA are increasingly gaining contracts due to their flexible manufacturing models and strong regulatory track records.

- As drug formulations become more personalized and sophisticated, API contract manufacturers that can provide end-to-end support from early-phase development to commercial-scale production are positioned to gain a competitive edge and attract long-term clients.

API Contract Manufacturing Market Dynamics

Driver

“Rising Outsourcing Due to Cost Pressures and Capacity Constraints”

- Increasing cost pressures, patent expirations, and R&D complexity are prompting pharmaceutical and biotech companies to outsource API manufacturing to reliable CMOs. This strategic shift enables them to focus on core competencies like drug discovery, while leveraging external expertise for production scalability and compliance.

- For instance, Teva Pharmaceuticals and Sun Pharma have continued to outsource a portion of their API needs to reduce capital burden and optimize global supply chains. This has become particularly important in the face of evolving regulatory environments and demand surges.

- Moreover, small and mid-sized pharma firms, which may lack the resources to build and maintain in-house API facilities, are increasingly dependent on contract manufacturers. The flexibility to choose between batch size, dosage forms, and geographical distribution through outsourcing makes API CMOs vital stakeholders in the drug production ecosystem.

- The growth of generic drugs, biosimilars, and the increased focus on rapid commercialization are also contributing to the demand for agile and scalable API production partnerships.

Restraint/Challenge

“Regulatory Compliance and Supply Chain Vulnerabilities”

- The API contract manufacturing market faces challenges in navigating diverse and evolving regulatory frameworks, particularly when operating across multiple regions. Contract manufacturers must comply with the stringent quality standards set by regulatory authorities such as the FDA (U.S.), EMA (Europe), PMDA (Japan), and CDSCO (India), which often involve time-consuming audits and certifications.

- For instance, a delay in regulatory approvals or a failed inspection can lead to supply disruptions and revenue loss for both CMOs and their client companies. Maintaining consistent documentation, adopting electronic batch records (EBRs), and achieving data integrity compliance are ongoing concerns.

- Additionally, the global nature of API supply chains has exposed manufacturers to geopolitical risks, raw material shortages, and logistical bottlenecks, as observed during the COVID-19 pandemic. Overdependence on a few countries for key raw materials (e.g., China and India for intermediates) can disrupt the production pipeline.

- To mitigate these challenges, many companies are now investing in diversified supply chains, dual sourcing strategies, and in-region manufacturing capabilities to ensure business continuity. However, these measures may require significant upfront investment, making them a constraint for smaller CMOs.

- Addressing these barriers through regulatory harmonization, investments in quality management systems, and strategic supply chain resilience planning will be essential to ensure long-term sustainability and client trust in the global API contract manufacturing ecosystem

API Contract Manufacturing Market Scope

The market is segmented on the basis of type, volume, form, end-users, and distribution channel.

- By Type

On the basis of type, the API contract manufacturing market is segmented into organic, inorganic, and others. The organic segment dominates the market with the largest revenue share of 61.3% in 2025, attributed to the widespread use of chemically synthesized APIs in generics and branded medications. Organic APIs are commonly utilized in treatments for chronic diseases such as cardiovascular conditions, diabetes, and infectious diseases. Their proven effectiveness, scalable production, and cost-efficiency make them a preferred choice for contract manufacturers and pharma clients alike.

The inorganic segment is expected to witness the fastest CAGR of 6.7% from 2025 to 2032, driven by rising demand for inorganic compounds in specialized formulations, especially in oncology and diagnostic imaging. These compounds often require precision engineering and compliance with stringent purity standards, which positions experienced contract manufacturers at a strategic advantage in this space.

• By Volume

On the basis of volume, the market is segmented into low, medium, large, and others. The large-volume production segment holds the largest revenue share in 2025 due to the high demand for bulk production of generic APIs across key therapeutic categories. Large-volume production offers economies of scale, consistent quality, and cost-effectiveness, especially when targeting mass-market drugs for global distribution.

The low-volume segment is anticipated to register the highest CAGR from 2025 to 2032, driven by the growth in orphan drugs, personalized medicine, and early-phase clinical trials. These low-volume APIs require specialized containment and tailored manufacturing, creating opportunities for niche CMOs equipped to handle complex, small-batch projects with agility and regulatory compliance.

• By Form

On the basis of form, the API contract manufacturing market is segmented into solid, liquid, semi-solids, and others. The solid form segment leads the market revenue share in 2025, as most oral solid dosage forms (tablets and capsules) are derived from powdered APIs. Solid APIs are relatively stable, easy to transport, and widely applicable, making them a dominant format in global manufacturing.

The liquid API segment is expected to grow at the fastest rate during the forecast period, fueled by the rising preference for injectable and suspension formulations in high-precision therapies such as oncology and biologics. Liquid APIs require advanced storage, transport, and sterilization standards, giving an edge to CMOs with specialized liquid handling capabilities.

• By End-Users

On the basis of end-users, the market is segmented into pharmaceutical industries, research organizations, and others. The pharmaceutical industries segment accounted for the largest market revenue share in 2025, driven by the increasing need to outsource API manufacturing to reduce operational costs, optimize R&D investments, and enhance production efficiency. Leading pharma companies are forming long-term strategic partnerships with CMOs to ensure consistent API quality and global regulatory compliance.

The research organizations segment is projected to grow at the fastest CAGR from 2025 to 2032, as academic institutes, biotech startups, and CROs increasingly require small-batch APIs for preclinical and early-phase trials. These users often lack in-house manufacturing facilities and rely on contract partners for speed, scalability, and technical support.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retailers, and others. The direct tender segment dominates the market in 2025, largely due to bulk procurement of APIs by government health bodies, large pharmaceutical firms, and international aid organizations. This channel ensures competitive pricing, regulatory transparency, and volume-driven supply commitments.

The retailers segment is expected to expand at the fastest pace during the forecast period, supported by the emergence of third-party API marketplaces and specialized intermediaries. Retail distribution is particularly relevant for specialty and rare APIs, where direct relationships between smaller pharma firms and API distributors enable rapid sourcing and delivery across global markets.

API Contract Manufacturing Market Regional Analysis

- North America dominates the API contract manufacturing market with the largest revenue share of 37.5% in 2024, driven by a high concentration of pharmaceutical and biotech companies, stringent regulatory standards, and strong demand for outsourcing services to reduce operational costs and improve scalability

- The region's robust manufacturing infrastructure, advanced technological capabilities, and presence of leading CMOs position it as a hub for high-value API production, including high-potency and specialty APIs

- Additionally, the region benefits from a mature healthcare ecosystem, growing demand for generics, and increasing R&D investments. These factors contribute to sustained outsourcing activity across both large pharmaceutical firms and smaller biotech players, making North America a key driver of global market growth

U.S. API Contract Manufacturing Market Insight

The U.S. API contract manufacturing market captured the largest revenue share of 79% within North America in 2025, driven by the country's dominant position in the pharmaceutical and biotechnology sectors. The increasing need for outsourcing complex and high-value APIs, coupled with rising R&D costs and patent expirations, is prompting companies to rely on contract manufacturers. U.S.-based CMOs benefit from advanced infrastructure, robust regulatory compliance, and strategic partnerships with global pharma firms. Furthermore, the demand for high-potency APIs (HPAPIs) and biologics is strengthening the role of U.S. manufacturers in the global supply chain.

Europe API Contract Manufacturing Market Insight

The European API contract manufacturing market is projected to grow steadily during the forecast period, fueled by stringent regulatory frameworks, increasing demand for GMP-certified production, and the expansion of specialty pharmaceutical manufacturing. Countries such as Germany, Switzerland, and Italy are home to several leading CMOs that serve both local and global clients. The market is supported by strong government backing for pharmaceutical innovation, a rise in generics production, and cross-border collaborations with major drug developers. Europe’s emphasis on quality, traceability, and sustainability is also enhancing the region's CMO capabilities.

U.K. API Contract Manufacturing Market Insight

預計英國 API 合約製造市場在預測期內將實現顯著的複合年增長率,這得益於英國蓬勃發展的醫藥研發生態系統以及中小企業日益增長的外包業務。脫歐後,英國致力於提升國內 API 能力,以減少對進口的依賴。對利基 API、生物製藥和早期開發服務的需求,使英國的 CMO 成為尋求高品質、合規製造服務的全球客戶的策略合作夥伴。

德國API合約製造市場洞察

預計德國API合約製造市場將以顯著的複合年增長率成長,這得益於該國強大的製藥基礎、成熟的化學工業以及嚴格的品質和合規標準。德國是歐洲主要的API出口國,擁有生產小分子和生物API的先進技術專長。全球知名的CMO、對創新的執著以及對歐盟GMP指南的嚴格遵守,使德國成為極具吸引力的合約製造目的地。

亞太地區API合約製造市場洞察

受低成本製造優勢、優惠的政府政策以及不斷增長的FDA和EMA批准設施的推動,亞太地區API合約製造市場預計將在2025年實現超過7.5%的最快複合年增長率。印度和中國等國家憑藉其龐大的生產能力、熟練的勞動力以及日益增長的仿製藥需求,在該地區處於領先地位。由於具有競爭力的價格和更快的周轉時間,區域CMO正在獲得越來越多的國際合同,這使得亞太地區成為API生產的重要全球樞紐。

印度API合約製造市場洞察

2025年,印度的API合約製造市場將佔據亞太地區最大的收入份額,這得益於其成熟的仿製藥行業、強勁的國內需求以及“生產掛鉤激勵計劃”(PLI)等政府舉措。印度擁有數千家API製造商,其中許多製造商已獲得全球監管機構的批准。印度能夠以極具競爭力的價格生產傳統和複雜的API,使其成為全球製藥公司的首選外包目的地。

中國API合約製造市場洞察

中國原料藥合約生產市場正在快速擴張,這得益於中國在化學合成、成本效益和已開發產業集群方面的主導地位。隨著中國越來越重視提高監管標準和向受監管市場出口,中國合約生產企業正在投資品質升級和技術整合。中國政府大力推動原料藥自力更生和創新,加上其在全球關鍵中間體供應中所扮演的作用,使其繼續成為全球原料藥供應鏈的基石。

API合約製造市場份額

API 合約製造業主要由知名公司主導,包括:

- 梯瓦製藥工業股份有限公司(以色列)

- 太陽製藥工業有限公司(印度)

- 勃林格殷格翰有限公司(德國)

- Piramal Pharma Solutions(印度)

- 山德士股份公司(瑞士)

- 葛蘭素史克公司(英國)

- 魯冰花(印度)

- 瞻博製藥(美國)

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。