COVID-19パンデミックは医療機器市場全体に大きな影響を与え、複数のセグメントで広範囲にわたる影響が見られました。パンデミック中、重篤なCOVID-19患者にとって不可欠な機器である人工呼吸器の需要が急増しました。メドトロニックは2020年3月までに人工呼吸器の生産量を40%以上増加させました。パンデミック中、これは医療機器の成長に影響を与えました。2020年のCOVID-19パンデミックの第一段階では、ウイルスの存在を検出するために考慮すべき重要な要素があったため、血圧計や体温計などのモニタリング機器の需要が急増しました。

完全なレポートはhttps://www.databridgemarketresearch.com/reports/global-medical-devices-marketでご覧いただけます。

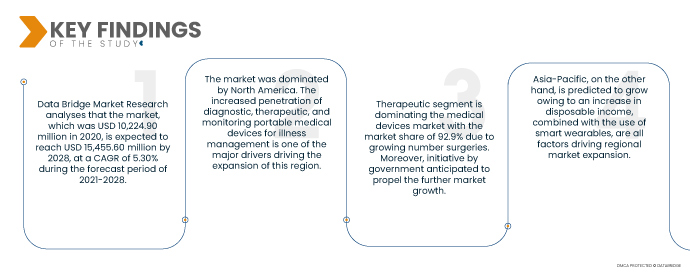

データブリッジ市場調査の分析によると、2020年の市場規模は102億2,490万米ドルでしたが、2021年から2028年の予測期間中に5.30%の年平均成長率(CAGR)で成長し、2028年には154億5,560万米ドルに達すると予想されています。医療費の増加は、新しい診断検査や手術器具の開発に大きな影響を与えています。その結果、医療費の高騰は医療機器市場の成長にとってプラスの要因となっています。一方、医療機器の悪影響の増大は、医療機器市場の需要を抑制し、阻害する要因となっています。新製品の導入は、医療機器市場参加者にとって、医療機器市場における事業成長を加速させる大きな可能性を秘めています。

慢性疾患の罹患率の増加が市場の成長率を押し上げると予想される

世界的な人口の高齢化と慢性疾患の発生率、そして在宅モニタリング機器の需要が、市場の成長を牽引しています。米国癌協会の2022年度年次報告書によると、米国における新規癌症例数は約190万人と予想されており、50万人以上が癌による死亡につながる重篤な疾患を患っています。癌の発生率と死亡率の高さが予想されるため、罹患人口における健康モニタリング技術の導入は増加すると予想されます。

レポートの範囲と市場セグメンテーション

レポートメトリック

|

詳細

|

予測期間

|

2021年から2028年

|

基準年

|

2020

|

歴史的な年

|

2019年(2013~2018年にカスタマイズ可能)

|

定量単位

|

売上高(百万米ドル)、販売数量(個数)、価格(米ドル)

|

対象セグメント

|

製品(人工呼吸器、スパイロメーター、酸素濃縮器、麻酔器、CPAP/BIPAP)、モード(ポータブル、卓上、スタンドアロン)、用途(診断および治療)、施設(大規模、小規模、中規模)、エンドユーザー(病院、外来手術センター、専門クリニック、長期ケアセンター、リハビリテーションセンター、在宅ケア施設)、流通チャネル(直接販売、サードパーティ販売代理店)

|

対象国

|

U.S., Canada and Mexico in North America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe in Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA), Brazil, Argentina and Rest of South America as part of South America

|

Market Players Covered

|

GE Healthcare (U.S.), Koninklijke Philips N.V. (Netherlands), Medtronic (Ireland), Drägerwerk AG & Co. KGaA (Germany), VYAIRE (U.S.), Getinge AB (Sweden), Smiths Medical Inc. (U.S.), NDD Medical Technologies (U.S.), ResMed (U.S.), Invacare Corporation (U.S.), Teijin Limited (Japan), Inogen, Inc. (U.S.), Teleflex Incorporated (U.S.), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), MGC Diagnostics Corporation (U.S.), Midmark Corporation (U.S.), CAIRE Inc. (U.S.), GCE Group (Sweden), Fisher & Paykel Healthcare Limited (New Zealand), Schiller (Switzerland)

|

Data Points Covered in the Report

|

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework

|

Segment Analysis:

Global medical devices market is categorized into six notable segments which are based on product, mode, application, facility, end user and distribution channel.

- On the basis of product, the medical devices market is segmented into ventilator, spirometers, oxygen concentrators, anesthesia machines, CPAP/BIPAP. Ventilator segment is dominating the medical devices market with the market share of 56.0% as large number of patient pool suffering from respiratory diseases and COVID-19.

- On the basis of mode, the medical devices market is segmented into portable, tabletop, standalone. Portable segment is dominating the medical devices market with the market share of 50.9% due to growing demand for highly advanced and efficient medical devices for treatment.

- On the basis of application, the medical devices market is segmented into diagnostic and therapeutic. Therapeutic segment is dominating the medical devices market with the market share of 92.9% due to growing number surgeries. Moreover, initiative by government anticipated to propel the further market growth.

- On the basis of facility, the medical devices market is segmented into large, small and medium. Large segment is dominating the medical devices market with the market share of 55.3% due to increasing number of wealthy hospitals across the world. Furthermore, the growing demand for various medical devices serves as another driving factor.

- On the basis of end user, the medical devices market is segmented into hospital, ambulatory surgical centers, specialty clinics, long term care centers, rehabilitation centers, homecare settings. Hospital segment is dominating the medical devices market with the market share of 30.6% because most patients are suffering from COVID-19 disease so they would be seen in the hospital to get proper diagnosis and treatment.

The hospital segment will dominate the end user segment of the medical devices market

The hospital segment will emerge as the dominating segment end user segment. This is because of the growing number of hospitals in the market especially in the developing economies. Further, growth and expansion of research development services on a global scale will further bolster the growth of this segment.

- On the basis of distribution channel, global medical devices market is segmented into direct sales and third party distributor. Pharmacies segment is dominating the medical devices market with a market share of 41.77% due to full control over the sales and revenue process and direct interaction with your customers. The segment is growing due to the increasing number of hospitals in developed and developing countries.

The pharmacies segment will dominate the distribution channel segment of the medical devices market

The pharmacies segment will emerge as the dominating segment under distribution channel. This is because of the growing number of infrastructural development activities in the market especially in the developing economies. Further, growth and expansion of the healthcare industry all around the globe will further bolster the growth of this segment.

Major Players

Data Bridge Market Research recognizes the following companies as the major market players: GE Healthcare (U.S.), Koninklijke Philips N.V. (Netherlands), Medtronic (Ireland), Drägerwerk AG & Co. KGaA (Germany), VYAIRE (U.S.), Getinge AB (Sweden), Smiths Medical Inc. (U.S.), NDD Medical Technologies (U.S.), ResMed (U.S.), Invacare Corporation (U.S.), Teijin Limited (Japan), Inogen, Inc. (U.S.), Teleflex Incorporated (U.S.), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), MGC Diagnostics Corporation (U.S.), Midmark Corporation (U.S.), CAIRE Inc. (U.S.), GCE Group (Sweden), Fisher & Paykel Healthcare Limited (New Zealand), Schiller (Switzerland).

Market Development

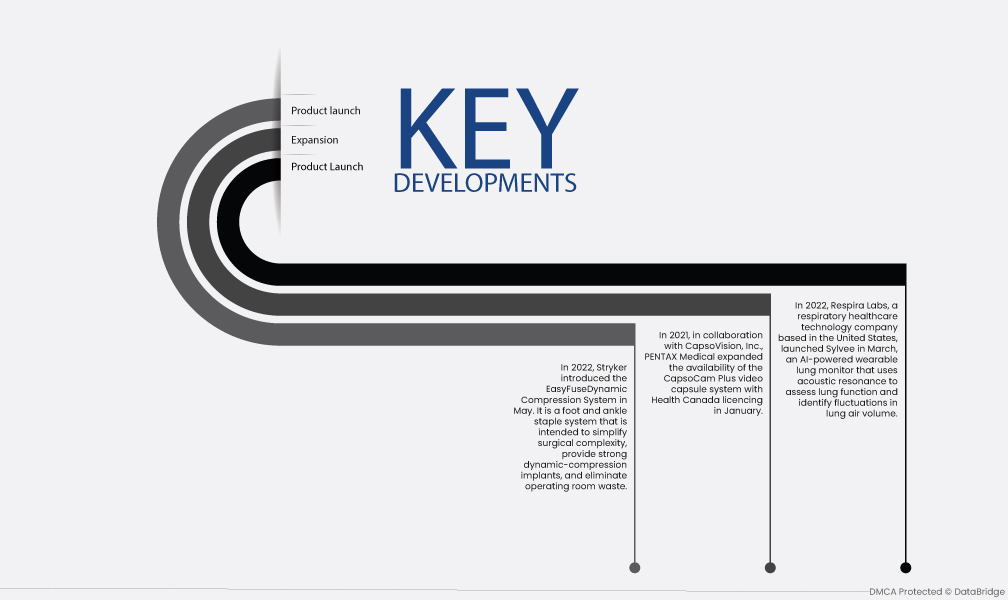

- In 2022, Stryker introduced the EasyFuseDynamic Compression System in May. It is a foot and ankle staple system that is intended to simplify surgical complexity, provide strong dynamic-compression implants, and eliminate operating room waste.

- 2021年、PENTAX MedicalはCapsoVision社と提携し、1月にカナダ保健省の認可を取得し、CapsoCam Plusビデオカプセルシステムの提供範囲を拡大しました。この製品拡充により、COVID-19パンデミック下でも、対象となる患者様はCapsoCam Plus小腸カプセル内視鏡を自宅で使用できるようになります。これにより、完全遠隔でのカプセル内視鏡検査が可能になり、医師と患者様の対面でのやり取りが実質的に不要になります。

- 2022年、米国に拠点を置く呼吸器ヘルスケアテクノロジー企業Respira Labsは、3月にAI搭載のウェアラブル肺モニター「Sylvee」を発売しました。Sylveeは音響共鳴を利用して肺機能を評価し、肺の空気量の変動を検知します。慢性閉塞性肺疾患(COPD)、喘息、COVID-19の早期発見と治療に役立ちます。

地域分析

地理的に、市場レポートでカバーされている国は、北米では米国、カナダ、メキシコ、ヨーロッパではドイツ、フランス、英国、オランダ、スイス、ベルギー、ロシア、イタリア、スペイン、トルコ、ヨーロッパではその他のヨーロッパ、中国、日本、インド、韓国、シンガポール、マレーシア、オーストラリア、タイ、インドネシア、フィリピン、アジア太平洋地域 (APAC) ではその他のアジア太平洋地域、サウジアラビア、UAE、南アフリカ、エジプト、イスラエル、中東およびアフリカ (MEA) の一部としてその他の中東およびアフリカ (MEA)、南米の一部としてブラジル、アルゼンチン、その他の南米です。

Data Bridge Market Researchの分析によると:

2021年から2028年の予測期間中、北米は医療機器市場の主要な地域となる。

市場は北米が圧倒的に優勢です。疾病管理のための診断、治療、モニタリング用携帯型医療機器の普及率向上は、この地域の拡大を牽引する大きな要因の一つです。慢性疾患の増加と人口の高齢化も市場の成長を牽引しています。

アジア太平洋地域は、 2021年から2028年の予測期間において医療機器市場で最も急速に成長する地域になると予測されています。

一方、アジア太平洋地域は、予測期間中に急速な成長が見込まれています。高齢者人口の増加、糖尿病罹患率の上昇、心臓病罹患率の上昇、可処分所得の増加、そしてスマートウェアラブル機器の利用拡大が、いずれもこの地域の市場拡大を牽引する要因となっています。

医療機器市場レポートの詳細については 、こちらをクリックしてください – https://www.databridgemarketresearch.com/reports/global-medical-devices-market