تُفضّل اختبارات التشخيص السريع على اختبارات التشخيص القياسية، إذ تُعزّز التحليل السببي للعدوى في حالات مُتعددة (مثل تعفّن الدم، والتهابات الجهاز التنفسي، والتهاب السحايا). لا يُوضّح هذا النوع من الاختبارات التشخيصية السريعة دائمًا، ولذلك لا يُمكنها حتى الآن أن تُحلّ محلّ الاختبارات التقليدية. هناك ثلاثة أنواع من اختبارات التشخيص السريع: شرائط أو أشرطة اختبار المناعة السريعة لقياس تركيز مادة كيميائية. تُستخدم شرائط الاختبار غالبًا لاختبار مستوى الرقم الهيدروجيني (pH) لسائل في عينة، ولكن بعض أنواع شرائط الاختبار تُستخدم لأغراض أخرى، مثل الكشف عن وجود مُلوّث. تُعدّ اختبارات الكروماتوغرافيا المناعية سهلة ومريحة؛ وتُمثّل الاختبارات السريعة بديلاً مناسبًا لطريقة الزراعة الفرعية التقليدية لتحديد مُسبّبات الأمراض بشكل أولي. يُستخدم تفاعل البوليميراز المتسلسل العكسي (PCR) لاختبار المادة الوراثية الموجودة في العينة. تشمل مزايا اختبارات التشخيص السريع سهولة الاستخدام، ومتطلبات التدريب البسيطة، وسرعة النتائج، وقلة الأجهزة. ومع ذلك، فإن نقاط الضعف التي تم ملاحظتها هي التفسير الذاتي للقراءة، ومعدل أقل من البيانات البيولوجية المقدمة، وحساسية أقل مقارنة باختبارات المرجع.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/europe-rapid-diagnostic-tests-rdt-market

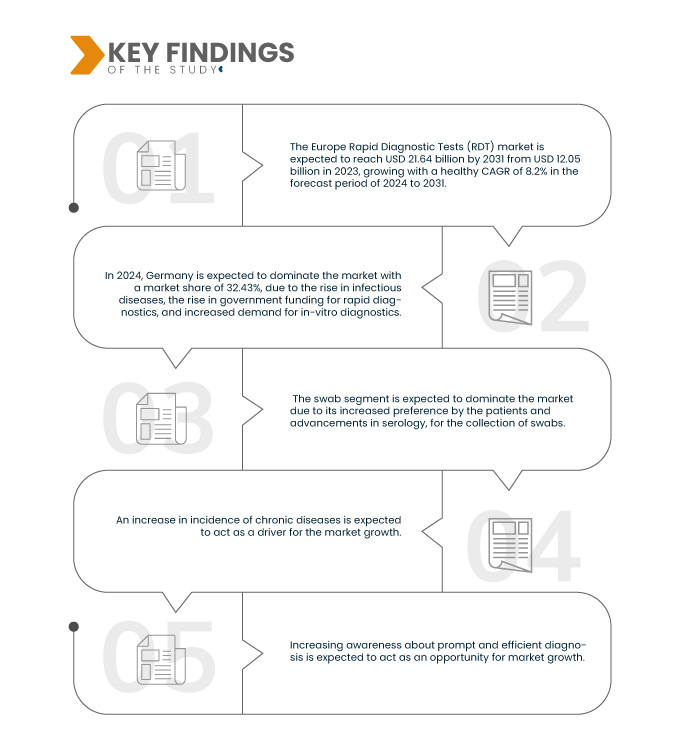

تشير تحليلات Data Bridge Market Research إلى أن سوق اختبارات التشخيص السريع (RDT) في أوروبا من المتوقع أن يصل إلى 21.64 مليار دولار أمريكي بحلول عام 2031 من 12.05 مليار دولار أمريكي في عام 2023، بنمو قدره 8.2٪ في الفترة المتوقعة من 2024 إلى 2031.

النتائج الرئيسية للدراسة

- زيادة في حالات الإصابة بالأمراض المزمنة

العوامل الدافعة لنمو سوق اختبارات التشخيص السريع في أوروبا (RDT) هي زيادة معدل الإصابة بالأمراض المزمنة، وارتفاع عدد كبار السن، والتطورات التكنولوجية في هذه الاختبارات، وزيادة إطلاق المنتجات. ومع ذلك، من المتوقع أن تُعيق هذه العوامل نمو السوق، وهي ارتفاع تكلفة التشخيص السريع، وسحب منتجات هذه الاختبارات من الأسواق، وقلة الوعي باستخدامها. علاوة على ذلك، تُعزز المبادرات الاستراتيجية التي تُقدمها الجهات الفاعلة في السوق، وارتفاع نفقات الرعاية الصحية، نمو السوق. ومع ذلك، تُشكل الحاجة إلى عمالة ماهرة لجمع العينات، والتأخر في الموافقة على إطلاق المنتجات، تحديات تُعيق نمو السوق.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2024 إلى 2031

|

سنة الأساس

|

2023

|

السنوات التاريخية

|

2022 (قابلة للتخصيص حتى 2016-2021)

|

الوحدات الكمية

|

الإيرادات بالمليار دولار أمريكي

|

القطاعات المغطاة

|

نوع المنتج (المواد الاستهلاكية والمجموعات والأجهزة وغيرها)، والوضع (المهني والأدوية المتاحة بدون وصفة طبية)، والتكنولوجيا (القائمة على تفاعل البوليميراز المتسلسل، واختبارات التدفق، واختبارات الكروماتوغرافيا المناعية بالتدفق الجانبي، واختبار التراص، والميكروفلويديك ، وتكنولوجيا الركيزة، وغيرها)، والوسيلة (اختبار قائم على المختبر واختبار غير قائم على المختبر)، والفئة العمرية (البالغين والأطفال)، ونوع الاختبار (تحديد التأكيد، والاختبار المصلي، وتسلسل الفيروس)، والنهج (التشخيص المخبري والتشخيص الجزيئي )، والعينة (المسحة، والدم، والبول، واللعاب، والبلغم، وغيرها)، والتطبيق (اختبار الأمراض المعدية، ومراقبة الجلوكوز، واختبار أمراض القلب، واختبار الأورام، واختبار القلب الأيضي، واختبار تعاطي المخدرات، واختبار الحمل والخصوبة. اختبار السموم، وغيرها)، المستخدم النهائي (المستشفى والعيادة، مختبر التشخيص، بيئة الرعاية المنزلية، المعاهد البحثية والأكاديمية، وغيرها)، قناة التوزيع (العطاء المباشر ومبيعات التجزئة)

|

الدول المغطاة

|

ألمانيا، فرنسا، المملكة المتحدة، إيطاليا، إسبانيا، روسيا، تركيا، بلجيكا، هولندا، سويسرا، وبقية أوروبا

|

الجهات الفاعلة في السوق المغطاة

|

Abbott (الولايات المتحدة)، Danaher (الولايات المتحدة)، Cellex (الولايات المتحدة)، Fujirebio (اليابان)، Access Bio (الولايات المتحدة)، Cardinal Health (الولايات المتحدة)، Bio-Rad Laboratories, Inc. (الولايات المتحدة)، BD (الولايات المتحدة)، F. Hoffmann-La Roche Ltd (سويسرا)، bioMérieux SA (فرنسا)، InBios International, Inc (الولايات المتحدة)، Luminex Corporation (الولايات المتحدة)، Gnomegen LLC (الولايات المتحدة)، QIAGEN (هولندا)، Quidel Corporation (الولايات المتحدة)، Sysmex Europe GMBH (ألمانيا)، Cardinal Health (الولايات المتحدة)، Siemens Healthcare Gmbh (شركة تابعة Siemens Healthineers AG) (ألمانيا)، MEGACOR DIAGNOSTIKGMBH (ألمانيا)، PerkinElmer Inc. (الولايات المتحدة)، Sekisui Diagnostics (الولايات المتحدة)، PTS Diagnostics (الولايات المتحدة)، werfen (إسبانيا)، Nova Biomedical (الولايات المتحدة)، وTrinity Biotech (أيرلندا)، وغيرها

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي أعدتها Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء وعلم الأوبئة للمرضى وتحليل خط الأنابيب وتحليل التسعير والإطار التنظيمي.

|

تحليل القطاعات

يتم تصنيف سوق اختبارات التشخيص السريع في أوروبا (RDT) إلى إحدى عشرة شريحة بارزة بناءً على نوع المنتج والوضع والتكنولوجيا والوسيلة والفئة العمرية ونوع الاختبار والنهج والعينة والتطبيق والمستخدم النهائي وقناة التوزيع.

- على أساس نوع المنتج، يتم تقسيم السوق إلى مواد استهلاكية ومجموعات وأدوات وغيرها

في عام 2024، من المتوقع أن تهيمن شريحة المواد الاستهلاكية والمجموعات على سوق اختبارات التشخيص السريع (RDT) في أوروبا

ومن المتوقع أن تهيمن شريحة المواد الاستهلاكية والمجموعات على السوق في عام 2024 بحصة سوقية تبلغ 55.54% بسبب سهولة الاستخدام وتوافر مجموعات الاختبار وتسليم النتائج بشكل أسرع.

- على أساس الوضع، يتم تقسيم السوق إلى احترافي وخارجي [OTC]

من المتوقع أن يهيمن القطاع المهني على سوق اختبارات التشخيص السريع (RDT) في أوروبا في عام 2024

ومن المتوقع أن تهيمن شريحة منتجات اختبار التشخيص السريع المهني على السوق في عام 2024 بحصة سوقية تبلغ 76.11% بسبب الدقة والاستخدام المتزايد في نقاط الرعاية، مثل المنازل.

- بناءً على التكنولوجيا، يُقسّم السوق إلى فحوصات قائمة على تفاعل البوليميراز المتسلسل (PCR)، وفحوصات التدفق، وفحوصات الكروماتوغرافيا المناعية ذات التدفق الجانبي، وفحوصات التراص، والموائع الدقيقة، وتكنولوجيا الركيزة، وغيرها. في عام 2024، من المتوقع أن يهيمن قطاع تفاعل البوليميراز المتسلسل على السوق بحصة سوقية تبلغ 37.51%.

- بناءً على طريقة الاستخدام، يُقسّم السوق إلى اختبارات معملية واختبارات غير معملية. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع الاختبارات المعملية على السوق بحصة سوقية تبلغ ٧١.٦٨٪.

- بناءً على الفئة العمرية، يُقسّم السوق إلى قسمين: للبالغين والأطفال. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع البالغين على السوق بحصة سوقية تبلغ ٨٤.٩٤٪.

- بناءً على نوع الاختبار، يُقسّم السوق إلى قسمين: قسم التأكيد، وقسم الاختبارات المصلية، وقسم التسلسل الفيروسي. في عام ٢٠٢٤، من المتوقع أن يُهيمن قسم التأكيد على السوق بحصة سوقية تبلغ ٤٣.٢٧٪.

- بناءً على المنهجية المتبعة، يُقسّم السوق إلى تشخيصات داخل المختبر وتشخيصات جزيئية. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع التشخيص داخل المختبر على السوق بحصة سوقية تبلغ ٧٣.٨٨٪.

- بناءً على العينة، يُقسّم السوق إلى مسحات، ودم، وبول، ولعاب، وبلغم، وغيرها. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع المسحات على سوق اختبارات التشخيص السريع (RDT) في أوروبا بحصة سوقية تبلغ ٤٥.٠٤٪.

- بناءً على التطبيق، يُقسّم السوق إلى اختبارات الأمراض المعدية، ومراقبة مستوى الجلوكوز، واختبارات أمراض القلب، واختبارات الأورام، واختبارات القلب الأيضية، واختبارات تعاطي المخدرات، واختبارات الحمل والخصوبة، واختبارات السموم، وغيرها. في عام 2024، من المتوقع أن يهيمن قطاع اختبارات الأمراض المعدية على السوق بحصة سوقية تبلغ 33.74%.

- بناءً على المستخدم النهائي، يُقسّم السوق إلى مستشفيات وعيادات، ومختبرات تشخيصية، ومراكز رعاية منزلية، ومعاهد بحثية وأكاديمية، وغيرها. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع المستشفيات والعيادات على السوق بحصة سوقية تبلغ ٥٥.١٠٪.

- بناءً على قنوات التوزيع، يُقسّم السوق إلى مناقصة مباشرة ومبيعات تجزئة. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع المناقصة المباشرة على السوق بحصة سوقية تبلغ ٦١.٥٣٪.

اللاعبون الرئيسيون

قامت شركة Data Bridge Market Research بتحليل شركة Abbott (الولايات المتحدة)، وشركة F. Hoffmann-La Roche Ltd (سويسرا)، وشركة Siemens Healthcare Gmbh (شركة تابعة لشركة Siemens Healthineers AG) (ألمانيا)، وشركة Danaher (الولايات المتحدة)، وشركة Cardinal Health (الولايات المتحدة) باعتبارها اللاعبين الرئيسيين في سوق اختبارات التشخيص السريع (RDT) في أوروبا.

تطورات السوق

- في مايو 2020، ووفقًا لتقرير صادر عن منظمة الصحة العالمية، قُدِّر أن الأمراض المزمنة ستكون مسؤولة عن ثلاثة أرباع الوفيات في جميع أنحاء العالم. وسيصل عدد الأشخاص الذين يُصابون بأمراض مثل السكري من النوع الثاني وسرطان الرئة إلى 228 مليونًا في عام 2025، مقارنةً بـ 80 مليونًا. ويؤدي الارتفاع السريع في الأمراض المزمنة، مع تغيير نمط الحياة، إلى زيادة معدل السمنة في العالم، وهو أمر يمكن الوقاية منه بسهولة من خلال التشخيص المبكر.

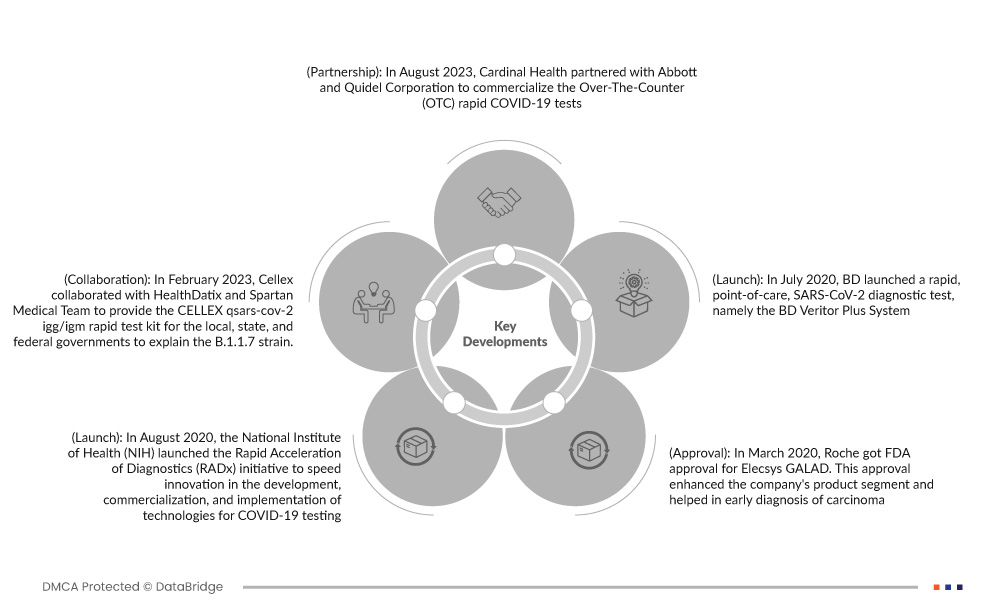

- في أبريل 2020، دخلت كاردينال هيلث في شراكة مع شركتي أبوت وكويدل كوربوريشن لتسويق اختبارات كوفيد-19 السريعة المتاحة بدون وصفة طبية. ستتيح هذه الشراكة لكاردينال هيلث توسيع نطاق خدماتها في فحص ومراقبة كوفيد-19، وستتمكن من الوصول إلى جهازي كويدل كويك فيو المنزلي لفحص كوفيد-19 المتاحين بدون وصفة طبية، وجهاز أبوت بيناكس ناو لاختبار مستضد كوفيد-19 الذاتي، اللذين يتيحان للمرضى إجراء الاختبارات بسهولة دون وصفة طبية.

- في أغسطس 2020، أطلق المعهد الوطني للصحة (NIH) مبادرة تسريع التشخيص السريع (RADx) لتسريع الابتكار في تطوير وتسويق وتطبيق تقنيات فحص كوفيد-19. يوفر هذا الاختبار التشخيصي السريع نتائج دقيقة ومثالية.

- في مارس 2020، حصلت شركة روش على موافقة إدارة الغذاء والدواء الأمريكية (FDA) على دواء Elecsys GALAD. وقد عززت هذه الموافقة قطاع منتجات الشركة وساعدت في التشخيص المبكر للسرطان. كما عززت هذه الموافقة الوضع المالي للشركة.

- في يوليو 2020، أطلقت شركة BD نظام BD Veritor Plus، وهو اختبار تشخيصي سريع لفيروس SARS-CoV-2 في نقطة الرعاية. تتميز هذه الاختبارات الجديدة بسهولة استخدامها وسهولة حملها، مما يجعلها أداة بالغة الأهمية لتحسين الوصول إلى تشخيص كوفيد-19. وقد ساهم هذا المنتج الجديد في تنويع محفظة منتجات الشركة.

التحليل الإقليمي

من الناحية الجغرافية، البلدان التي يغطيها تقرير السوق هي ألمانيا وفرنسا والمملكة المتحدة وإيطاليا وإسبانيا وروسيا وتركيا وبلجيكا وهولندا وسويسرا وبقية أوروبا.

وفقًا لتحليل Data Bridge Market Research:

من المتوقع أن تصبح ألمانيا الدولة المهيمنة والأسرع نموًا في سوق اختبارات التشخيص السريع (RDT) في أوروبا

ومن المتوقع أن تهيمن ألمانيا على السوق بسبب ارتفاع معدلات الأمراض المعدية مع شيخوخة السكان.

لمزيد من المعلومات التفصيلية حول تقرير سوق اختبارات التشخيص السريع (RDT) في أوروبا، انقر هنا - https://www.databridgemarketresearch.com/reports/europe-rapid-diagnostic-tests-rdt-market