Les réseaux de prestation de soins intégrés (RPI) sont des systèmes de santé qui regroupent divers établissements médicaux, tels que les hôpitaux, les cliniques et les prestataires de soins primaires, afin de proposer des soins coordonnés aux patients. Ils offrent un accès centralisé aux données des patients, garantissant une prise de décision rapide et éclairée. Les RPI simplifient les processus administratifs, optimisent l'allocation des ressources et améliorent les résultats pour les patients. Leurs applications incluent la gestion de la santé de la population, l'amélioration de la qualité des soins et la rentabilité des prestations de soins. Les RPI sont essentiels aux modèles de soins axés sur la valeur, où ils privilégient le bien-être des patients et privilégient les soins préventifs et holistiques.

Accédez au rapport complet sur https://www.databridgemarketresearch.com/reports/us-integrated-delivery-network-market

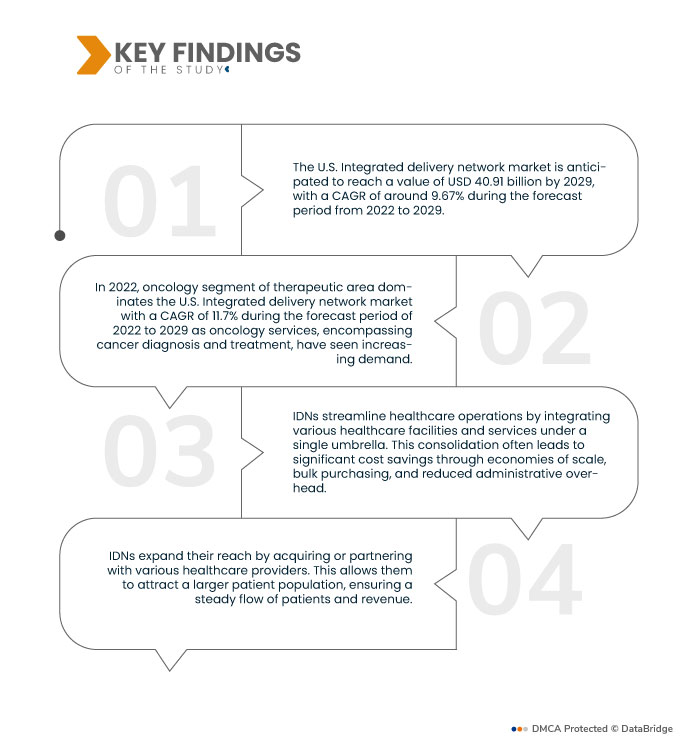

Selon Data Bridge Market Research, le marché américain des réseaux de distribution intégrés ( IDN) est évalué à 19,55 milliards de dollars US en 2021 et devrait atteindre 40,91 milliards de dollars US d'ici 2029, avec un TCAC de 9,67 % sur la période de prévision 2022-2029. Les IDN se concentrent sur la prestation de soins coordonnés et de haute qualité. En partageant les informations sur les patients et en standardisant les protocoles de soins au sein de leur réseau, ils peuvent améliorer les résultats des patients et réduire les erreurs médicales.

Principales conclusions de l'étude

Les soins basés sur la valeur devraient stimuler le taux de croissance du marché

La transition vers des soins basés sur la valeur privilégie le bien-être des patients plutôt que la traditionnelle rémunération à l'acte. Les réseaux de prestation de soins intégrés (RPI) sont parfaitement adaptés à cette évolution, car ils simplifient la coordination des soins entre les différents prestataires de soins. En partageant les informations des patients et en adhérant à des protocoles de soins standardisés, les RPI améliorent la qualité et les résultats des soins. Cette approche centrée sur le patient s'inscrit dans le modèle basé sur la valeur, garantissant aux patients des soins holistiques, efficaces et efficients, contribuant ainsi à une amélioration de leur santé et de leur bien-être.

Portée du rapport et segmentation du marché

Rapport métrique

|

Détails

|

Période de prévision

|

2022 à 2029

|

Année de base

|

2021

|

Années historiques

|

2020 (personnalisable de 2014 à 2019)

|

Unités quantitatives

|

Chiffre d'affaires en milliards USD, volumes en unités, prix en USD

|

Segments couverts

|

Type de service (intégration verticale, intégration horizontale), type (soins aigus, soins primaires, soins de longue durée, cliniques spécialisées, services de soins à domicile, autres), domaine thérapeutique (oncologie, cardiologie interventionnelle, diabète de type 2, hypercholestérolémie, bronchopneumopathie chronique obstructive , maladie de Parkinson, psoriasis , chirurgie orthopédique, chirurgie plastique, autres), utilisateur final (établissements de santé, groupements d'achat, sociétés pharmaceutiques, sociétés de dispositifs médicaux)

|

Pays couverts

|

POU

|

Acteurs du marché couverts

|

CommonSpirit Health (États-Unis), Ascension (États-Unis), Providence (États-Unis), TH Medical (États-Unis), Trinity Health (États-Unis), Regents of the University of California (États-Unis), Universal Health Services, Inc. (États-Unis), CHSPSC, LLC. (États-Unis), Northwell Health (États-Unis), UPMC HEALTH PLAN, INC. (États-Unis), Cleveland Clinic (États-Unis), Baylor Scott & White Health (États-Unis), NewYork-Presbyterian Hospital (États-Unis), Sutter Health (États-Unis), Adventist Health (États-Unis)

|

Points de données couverts dans le rapport

|

En plus des informations sur les scénarios de marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché organisés par Data Bridge Market Research comprennent également une analyse approfondie des experts, une épidémiologie des patients, une analyse du pipeline, une analyse des prix et un cadre réglementaire.

|

Analyse des segments :

Le marché américain des réseaux de distribution intégrés est segmenté en fonction du type de service, du type, du domaine thérapeutique et de l'utilisateur final.

- Selon le type de service, le marché américain des réseaux de prestation de soins intégrés est segmenté en intégration verticale et intégration horizontale. En 2022, le segment de l'intégration verticale domine le marché américain des réseaux de prestation de soins intégrés avec un TCAC de 11,1 % pour la période de prévision 2022-2029. Il implique des établissements de santé possédant divers composants du continuum de soins, notamment des hôpitaux, des cliniques et même des assureurs.

En 2022, le segment de l'intégration verticale domine le marché américain des réseaux de distribution intégrés avec un TCAC de 11,1 % au cours de la période de prévision de 2022 à 2029.

En 2022, le segment de l'intégration verticale domine le marché américain des réseaux de distribution intégrés, avec un TCAC de 11,1 % sur la période de prévision 2022-2029. En contrôlant ces éléments, les IDN peuvent rationaliser leurs opérations, améliorer la coordination des soins et réduire les coûts. Ce modèle intégré s'inscrit dans la transition du secteur vers des soins axés sur la valeur, permettant aux IDN de se concentrer sur la qualité des résultats, la satisfaction des patients et la rentabilité, propulsant ainsi leur croissance et leur influence dans le secteur de la santé.

- Selon le type de prestation, le marché américain des réseaux de soins intégrés est segmenté en soins actifs, soins primaires, soins de longue durée, cliniques spécialisées, services de soins à domicile, etc. En 2022, le segment des soins actifs domine le marché américain des réseaux de soins intégrés avec un TCAC de 9,7 % pour la période de prévision 2022-2029, les établissements de soins actifs, tels que les hôpitaux, jouant un rôle essentiel dans la prestation de services médicaux essentiels.

- Sur la base du domaine thérapeutique, le marché américain des réseaux de distribution intégrés est segmenté en oncologie, cardiologie interventionnelle, diabète de type 2, hypercholestérolémie, bronchopneumopathie chronique obstructive, maladie de Parkinson , psoriasis, chirurgie orthopédique et plastique, entre autres. En 2022, le segment oncologique domine le marché américain des réseaux de distribution intégrés avec un TCAC de 11,7 % pour la période de prévision 2022-2029, la demande en services oncologiques, englobant le diagnostic et le traitement du cancer, étant en hausse.

En 2022, le segment de l'oncologie dominera le marché américain des réseaux de distribution intégrés avec un TCAC de 11,7 % au cours de la période de prévision de 2022 à 2029.

En 2022, le segment de l'oncologie dominera le marché américain des réseaux de distribution intégrés avec un TCAC de 11,7 % sur la période de prévision 2022-2029. Les IDN développent stratégiquement leur offre en oncologie pour répondre à cette demande et proposer des soins complets et spécialisés. Le cancer étant un problème de santé majeur, les IDN qui excellent en oncologie sont plus susceptibles d'attirer des patients, de nouer des partenariats et de conquérir une part significative du marché de la santé, contribuant ainsi à leur croissance et à leur importance.

- En fonction de l'utilisateur final, le marché américain des réseaux de distribution intégrés est segmenté en établissements de santé, centrales d'achat, laboratoires pharmaceutiques et fabricants de dispositifs médicaux. En 2022, le segment des établissements de santé dominera le marché américain des réseaux de distribution intégrés avec un TCAC de 10,8 % sur la période de prévision 2022-2029. En effet, les établissements de santé, notamment les hôpitaux, les cliniques et les centres spécialisés, exercent une influence considérable sur la croissance du marché des réseaux de distribution intégrés (IDN). Ces établissements constituent l'épine dorsale des IDN et constituent les principaux lieux de prise en charge des patients.

Acteurs majeurs

Data Bridge Market Research reconnaît les entreprises suivantes comme les principaux acteurs du marché américain des réseaux de distribution intégrés : CommonSpirit Health (États-Unis), Ascension (États-Unis), Providence (États-Unis), TH Medical (États-Unis), Trinity Health (États-Unis), Regents of the University of California (États-Unis), Universal Health Services, Inc. (États-Unis), CHSPSC, LLC. (États-Unis), Northwell Health (États-Unis).

Évolution du marché

- En février 2020, TH Medical, un réseau intégré de soins comprenant 65 hôpitaux de soins aigus et spécialisés, a annoncé l'acquisition des centres médicaux Good Samaritan et St. Mary's. L'objectif de l'entreprise est d'améliorer les infrastructures et d'accroître la satisfaction des patients et des médecins sur ces sites. Cette décision stratégique devrait se traduire par une augmentation des admissions hospitalières et, à terme, par une amélioration de la rentabilité globale de l'entreprise.

- En février 2020, HCA Healthcare Inc. a dévoilé son intention de construire un centre de formation au Pearland Town Center, couvrant une superficie impressionnante de 48 400 pieds carrés et dont le démarrage des opérations est prévu début 2021. Cette initiative renforce l'engagement de l'entreprise à améliorer ses ressources de formation, permettant à environ 7 000 infirmières d'accéder à une formation clinique continue.

Pour plus d'informations sur le rapport sur le marché des réseaux de livraison intégrés aux États-Unis, cliquez ici : https://www.databridgemarketresearch.com/reports/us-integrated-delivery-network-market