Asia Pacific Acute Myeloid Leukemia Diagnostics Market

Market Size in USD Million

USD

641.60 Million

USD

1,489.29 Million

2024

2032

USD

641.60 Million

USD

1,489.29 Million

2024

2032

| 2025 - 2032 | |

| USD 641.60 Million | |

| USD 1,489.29 Million | |

| % | |

|

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Size

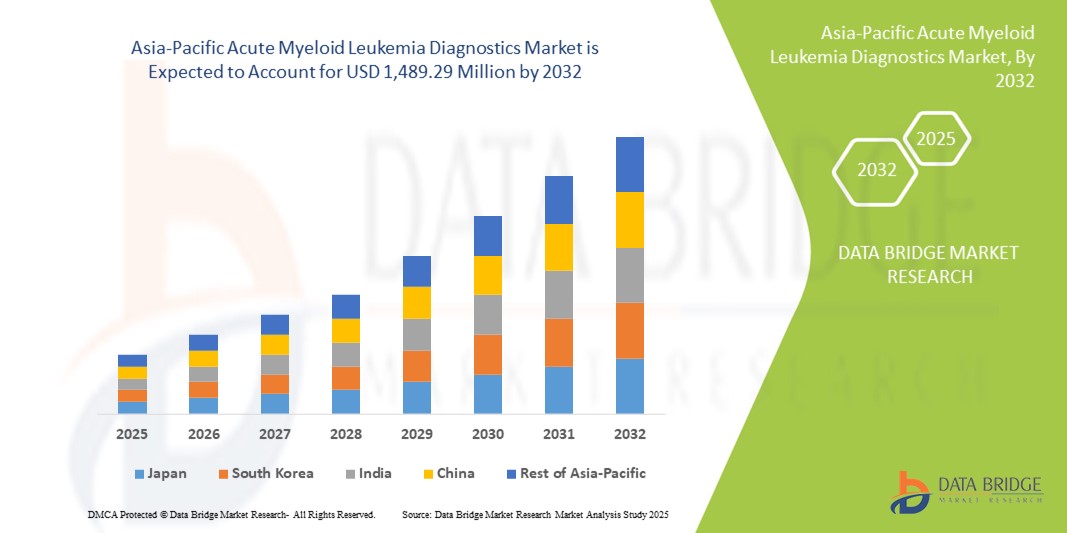

- The Asia-Pacific acute myeloid leukemia diagnostics market size was valued at USD 641.60 million in 2024 and is expected to reach USD 1,489.29 million by 2032, at a CAGR of 11.1% during the forecast period

- The market growth is largely fueled by the rising prevalence of hematological malignancies and increasing adoption of advanced molecular and genetic testing technologies across major healthcare systems in the region

- Furthermore, growing investments in precision medicine, government initiatives to strengthen cancer diagnostics infrastructure, and rising demand for early and accurate detection are positioning AML diagnostics as a critical component in oncology care. These converging factors are accelerating the uptake of diagnostic solutions, thereby significantly boosting the industry’s growth

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Analysis

- AML diagnostics, covering instruments, consumables, and advanced laboratory assays, are increasingly critical in hospitals and diagnostic centers across Asia-Pacific due to their role in early detection, classification, and monitoring of leukemia progression and treatment outcomes

- The escalating demand for AML diagnostics is primarily fueled by the rising prevalence of hematological malignancies, increasing adoption of genetic and biomarker-based testing, and expanding precision medicine initiatives across the region’s oncology practices

- China dominated the Asia-Pacific acute myeloid leukemia diagnostics market with the largest revenue share of 39.1% in 2024, driven by extensive government-backed cancer screening programs, rapid adoption of advanced testing technologies, and the growing availability of diagnostic laboratories with hematology expertise

- India is expected to be the fastest-growing country in the acute myeloid leukemia diagnostics market during the forecast period due to strengthening healthcare infrastructure, government-led cancer awareness initiatives, and the rising availability of affordable diagnostic solutions for leukemia detection

- Consumables & Accessories segment dominated the acute myeloid leukemia diagnostics market with a market share of 62.2% in 2024, owing to their recurring demand in routine blood, bone marrow, biomarker, and genetic testing workflows, ensuring consistent usage compared to one-time instrument installations

Report Scope and Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Segmentation

|

Attributes |

Asia-Pacific Acute Myeloid Leukemia Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Trends

Integration of Advanced Genomics and AI in AML Diagnostics

- A significant and accelerating trend in the Asia-Pacific AML diagnostics market is the increasing integration of advanced genomics technologies and artificial intelligence (AI) into diagnostic workflows, enhancing precision in disease classification and treatment guidance

- For instance, Illumina launched new genomic sequencing panels that help identify genetic mutations in AML patients, allowing oncologists in Asia-Pacific to select targeted therapies with greater confidence

- AI-powered diagnostic solutions are being deployed to analyze large genomic datasets, improving the accuracy of mutation detection and accelerating diagnostic turnaround times in leading hospitals and cancer research institutes. Furthermore, AI tools enable risk stratification and prediction of relapse, offering clinicians deeper insights into patient prognosis

- The seamless integration of genomics and AI-based analytics into routine AML testing enables personalized treatment decisions, such as matching patients with suitable therapies or clinical trials, thereby optimizing outcomes

- This trend towards precision oncology and intelligent diagnostic platforms is fundamentally reshaping expectations for AML care in Asia-Pacific. Consequently, companies such as Thermo Fisher Scientific and BGI Genomics are expanding their AI-enabled diagnostic solutions across China, India, and Southeast Asia

- The demand for diagnostics that combine genomic sequencing with AI-driven analytics is growing rapidly across hospitals, independent laboratories, and cancer institutes, as clinicians prioritize accuracy, speed, and personalized patient management

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Dynamics

Driver

Growing Need Due to Rising Cancer Burden and Precision Medicine Adoption

- The increasing prevalence of acute myeloid leukemia across Asia-Pacific, coupled with the rapid adoption of precision medicine, is a significant driver for the heightened demand for AML diagnostics

- For instance, in February 2024, Roche Diagnostics expanded its molecular testing solutions in China to support hospitals with advanced assays for detecting AML-associated mutations, improving access to cutting-edge diagnostics

- As patients and clinicians become more aware of the importance of early detection and targeted therapy selection, AML diagnostics provide advanced insights through genetic testing, cytogenetics, and biomarker assays, offering a compelling advantage over traditional methods

- Furthermore, the growing investments in healthcare infrastructure and the rising adoption of oncology-focused technologies across Asia-Pacific are making AML diagnostics an integral part of modern cancer care pathways

- The ability to deliver early, accurate diagnosis, guide personalized treatments, and monitor disease progression through specialized tests are key factors propelling the adoption of AML diagnostics in hospitals and laboratories. The growing emphasis on regional cancer control programs and government-backed initiatives further contribute to market growth

Restraint/Challenge

High Cost and Accessibility Gaps in Advanced Diagnostics

- Concerns surrounding the affordability and accessibility of advanced AML diagnostics, particularly in low- and middle-income Asia-Pacific countries, pose a significant challenge to broader market penetration

- For instance, high-profile reports from regional cancer associations have highlighted disparities in access to next-generation sequencing (NGS) technologies, with urban centers adopting advanced solutions while rural areas remain underserved

- Addressing these cost and access barriers through localized manufacturing, government subsidies, and partnerships with regional labs is crucial for improving patient access to AML diagnostics. Companies such as Qiagen and Abbott are focusing on developing cost-effective test kits tailored to emerging markets

- In addition, the relatively high cost of genomic sequencing compared to traditional blood or bone marrow tests can be a barrier for patients without strong insurance coverage, particularly in developing economies. While more affordable molecular panels are being introduced, advanced tests with AI-driven analytics or deep genomic profiling often remain out of reach for a large patient base

- While costs are gradually declining with technological innovation, the perceived financial burden of advanced AML diagnostics can still hinder widespread adoption, especially in markets where reimbursement systems are not fully developed

- Overcoming these challenges through cost innovation, wider insurance coverage, and improved diagnostic infrastructure will be vital for sustained market growth

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Scope

The market is segmented on the basis of product type, test type, cancer type, age group, gender, end user, and distribution channel.

- By Product Type

On the basis of product type, the acute myeloid leukemia diagnostics market is segmented into instruments and consumables & accessories. The consumables & accessories segment dominated the market with the largest revenue share of 62.2% in 2024, driven by their recurrent demand in AML testing workflows. Every diagnostic procedure, from blood smears to genetic assays, requires reagents, kits, and disposable accessories that must be replenished regularly. This ensures a consistent revenue stream compared to one-time instrument purchases. The rising use of biomarker tests and molecular assays across Asia-Pacific has further amplified consumables demand. Hospitals and diagnostic labs also prefer standardized consumables from leading suppliers to ensure reliable test results. This repetitive nature of use makes consumables the backbone of AML diagnostic testing.

The instruments segment is anticipated to witness the fastest growth rate of 10.4% from 2025 to 2032, fueled by increasing adoption of next-generation sequencing (NGS) platforms, flow cytometers, and automated hematology analyzers. As cancer research institutes and advanced hospitals invest heavily in molecular oncology, the demand for high-precision instruments is surging. Instruments also enable labs to expand diagnostic capacity, reduce turnaround time, and enhance accuracy in leukemia detection. The integration of AI and automation in instruments is further accelerating their adoption, particularly in China, Japan, and India.

- By Test Type

On the basis of test type, the acute myeloid leukemia diagnostics market is segmented into imaging test, blood test, bone marrow tests, biomarker test, immunophenotyping, genetic tests, and others. The blood test segment dominated the market with the largest revenue share of 28.7% in 2024, as it remains the first-line diagnostic tool for AML across Asia-Pacific. Blood tests are cost-effective, widely accessible, and essential for detecting abnormal white blood cell counts and blasts. Their simplicity and rapid turnaround make them indispensable in both rural clinics and advanced cancer centers. Physicians prefer blood tests as a routine part of AML screening and monitoring during treatment. Growing government-led health checkup programs in China and India further support blood test demand. Their foundational role in AML diagnostics cements their dominance.

The genetic tests segment is expected to be the fastest growing at a CAGR of 13.9% during 2025–2032, driven by the rise of precision medicine. Genetic testing enables identification of chromosomal translocations and mutations such as FLT3, NPM1, and IDH1/2, which are critical for risk stratification and treatment selection. Increasing availability of NGS-based platforms in hospitals and independent labs across China, Japan, and South Korea is accelerating adoption. Patients and clinicians are showing strong preference for tests that guide targeted therapies. As oncology guidelines increasingly mandate genetic profiling, this segment will expand rapidly across Asia-Pacific.

- By Cancer Type

On the basis of cancer type, the acute myeloid leukemia diagnostics market is segmented into myeloblastic (M0), myeloblastic (M1), myeloblastic (M2), promyelocytic (M3), myelomonocytic (M4), monocytic (M5), erythroleukemia (M6), and megakaryocytic (M7). The myeloblastic (M2) segment dominated the market with a revenue share of 23.1% in 2024, owing to its high prevalence in AML cases across Asia-Pacific. Clinical registries indicate that M2 is among the most frequently diagnosed subtypes, often requiring detailed cytogenetic and molecular testing. Its relatively better prognosis with specific therapies makes early and accurate detection essential. Diagnostic companies focus on offering tailored panels for M2 subtype identification. Hospitals and labs see consistent testing volumes for M2 AML, driving demand for both routine and advanced diagnostics. This strong prevalence ensures sustained dominance of this segment.

The promyelocytic (M3) segment is anticipated to grow the fastest at a CAGR of 12.6% during 2025–2032, fueled by advancements in early detection and targeted therapy availability. Acute promyelocytic leukemia (APL) is considered highly curable if diagnosed quickly, leading to increasing awareness among clinicians for rapid testing. Governments and oncology organizations are promoting faster access to diagnostic resources for M3 AML cases. With growing clinical emphasis on early treatment using ATRA and arsenic trioxide, demand for prompt and accurate diagnostic tests is surging. This therapeutic success story drives stronger investment in diagnostics for this subtype.

- By Age Group

On the basis of age group, the acute myeloid leukemia diagnostics market is segmented into below 21, 21–29, 30–65, and 65 and above. The 30–65 years segment dominated the market with the largest share of 46.8% in 2024, as AML is most commonly diagnosed in middle-aged adults. Patients in this group often have better access to healthcare facilities, diagnostic services, and insurance coverage compared to younger or older age groups. This age group also reflects a high proportion of the working population, making timely diagnosis crucial for quality of life and productivity. Hospitals and research studies often target this demographic, leading to greater testing volumes. The relatively higher incidence rate ensures this group’s sustained dominance.

The 65 and above segment is expected to be the fastest growing with a CAGR of 11.7% during 2025–2032, due to the aging population in Asia-Pacific, especially in Japan and China. AML incidence rises significantly with age, and older patients are increasingly being screened with advanced diagnostics to guide therapy decisions. Despite treatment challenges, there is growing focus on improving survival outcomes in elderly patients through precise diagnostics. Healthcare policies supporting cancer screening in the elderly further support segment growth. Rising life expectancy across Asia-Pacific will continue fueling demand in this segment.

- By Gender

On the basis of gender, the acute myeloid leukemia diagnostics market is segmented into male and female. The male segment dominated the market with the largest revenue share of 58.2% in 2024, consistent with epidemiological data showing higher AML prevalence in men across Asia-Pacific. Genetic predispositions, lifestyle risk factors, and occupational exposures contribute to this imbalance. Hospitals report higher male testing volumes, reinforcing the segment’s dominance. Public health studies also highlight stronger AML incidence rates among men, aligning diagnostic demand accordingly. Pharmaceutical companies and diagnostic firms tailor educational campaigns towards male risk groups. These patterns collectively ensure sustained dominance of this segment.

The female segment is expected to be the fastest growing at a CAGR of 9.8% from 2025 to 2032, as rising cancer awareness campaigns are increasingly targeting women. Improved healthcare access for women in emerging economies such as India and Indonesia is also supporting diagnostic growth. With shifting demographics and better inclusion in screening programs, the female population is experiencing greater testing uptake. As women-centric health initiatives expand, diagnostic adoption among females will accelerate.

- By End User

On the basis of end user, the acute myeloid leukemia diagnostics market is segmented into hospitals, associated labs, independent diagnostic laboratories, diagnostic imaging centres, cancer research institutes, and others. The hospital segment dominated the market with the largest revenue share of 41.5% in 2024, as hospitals remain the primary centers for AML diagnosis and treatment across Asia-Pacific. Hospitals provide access to advanced equipment, trained hematologists, and multidisciplinary cancer care teams. They also handle the majority of AML patient inflows, ensuring consistent diagnostic volumes. Government and private hospital chains are investing in advanced oncology diagnostic facilities, further strengthening their role. Hospitals also benefit from bulk procurement channels for AML diagnostic consumables. Their integrated role ensures their dominance in the end-user landscape.

The independent diagnostic laboratories segment is expected to be the fastest growing at a CAGR of 12.4% during 2025–2032, fueled by the increasing decentralization of diagnostic services. With growing demand for specialized tests such as genetic and biomarker assays, many labs are partnering with hospitals to provide outsourced diagnostic support. Independent labs offer cost-effective services and faster results, making them attractive to patients in urban and semi-urban settings. The rise of private diagnostic chains in India, China, and Southeast Asia is accelerating this trend.

- By Distribution Channel

On the basis of distribution channel, the acute myeloid leukemia diagnostics market is segmented into direct tender and retail sales. The direct tender segment dominated the market with the largest revenue share of 64.9% in 2024, as hospitals and diagnostic labs procure consumables and instruments in bulk. Tender-based procurement ensures standardized quality, reduced costs, and reliable supply for large institutions. Public hospitals in China, Japan, and India largely rely on tender systems to secure AML testing products. Manufacturers benefit from long-term contracts, ensuring consistent revenue streams. This procurement structure cements direct tender as the dominant channel in AML diagnostics.

The retail sales segment is projected to grow the fastest at a CAGR of 11.2% during 2025–2032, as smaller clinics, research labs, and private cancer centers increasingly prefer direct retail purchases. Retail channels also support the distribution of specialized diagnostic kits and reagents for pilot projects and clinical studies. Online retailing and e-procurement platforms are gaining traction, particularly for smaller batches of consumables. The flexibility and accessibility of retail channels make them appealing to independent labs and emerging diagnostic players across Asia-Pacific.

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Regional Analysis

- China dominated the Asia-Pacific acute myeloid leukemia diagnostics market with the largest revenue share of 39.1% in 2024, driven by extensive government-backed cancer screening programs, rapid adoption of advanced testing technologies, and the growing availability of diagnostic laboratories with hematology expertise

- Patients and healthcare providers in the region highly value the accuracy, early detection benefits, and treatment guidance offered by AML diagnostics such as blood tests, bone marrow evaluation, and genetic profiling, which are becoming essential in oncology care pathways

- This widespread adoption is further supported by rapid healthcare infrastructure development, a large and aging population base, and increasing investments in precision medicine, establishing AML diagnostics as a vital component of cancer management in both hospitals and independent laboratories

The China Acute Myeloid Leukemia Diagnostics Market Insight

The China acute myeloid leukemia diagnostics market captured the largest regional revenue share in 2024, driven by high AML prevalence, state-backed healthcare reforms, and substantial investments in oncology diagnostics. The adoption of advanced tools such as next-generation sequencing (NGS), flow cytometry, and genetic testing is increasing rapidly in hospitals and research centers. Strategic partnerships between domestic and global players are further expanding availability of precision diagnostics. China’s emphasis on integrating AI and digital health platforms into cancer care is also strengthening its leadership position within the Asia-Pacific market.

Japan Acute Myeloid Leukemia Diagnostics Market Insight

The Japan acute myeloid leukemia diagnostics market is advancing steadily, supported by the country’s strong healthcare infrastructure, focus on personalized medicine, and growing elderly population vulnerable to blood cancers. The rising demand for biomarker-based diagnostics, immunophenotyping, and genetic profiling is driven by initiatives promoting early detection and tailored therapies. Research collaborations and adoption of digital diagnostic platforms are enhancing efficiency across healthcare facilities. Japan’s leadership in innovation and R&D makes it a vital hub for the development of precision AML diagnostic solutions.

India Acute Myeloid Leukemia Diagnostics Market Insight

The India acute myeloid leukemia diagnostics market is expected to grow at the fastest CAGR within Asia-Pacific, fueled by expanding healthcare awareness, government-backed cancer screening initiatives, and rising healthcare expenditure. A growing middle-class population and the proliferation of private diagnostic chains are improving access to AML testing across urban and semi-urban areas. The adoption of blood tests, bone marrow analysis, and biomarker-based assays is accelerating, while domestic manufacturing of affordable diagnostic consumables is strengthening the local market. India’s push towards digital health and smart healthcare initiatives is set to further enhance accessibility and growth.

South Korea Acute Myeloid Leukemia Diagnostics Market Insight

The South Korea acute myeloid leukemia diagnostics market is witnessing significant growth, driven by rapid advancements in precision medicine, government support for cancer research, and rising healthcare digitization. Increasing adoption of genetic testing, biomarker assays, and imaging-based diagnostic tools is enhancing AML detection capabilities. South Korea’s strong IT and biotechnology ecosystem supports the integration of AI and digital platforms with diagnostic workflows. Collaborative efforts between hospitals, research institutes, and technology providers are accelerating innovation, making the country one of the most progressive AML diagnostics markets in the region.

Asia-Pacific Acute Myeloid Leukemia Diagnostics Market Share

The Asia-Pacific acute myeloid leukemia diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd (Switzerland)

- Abbott (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Netherlands)

- Illumina, Inc. (U.S.)

- BGI Group (China)

- Sysmex Corporation (Japan)

- BIOMÉRIEUX (France)

- Siemens Healthcare AG (Germany)

- PerkinElmer (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- BD (U.S.)

- Novogene Co., Ltd. (China)

- MedGenome (India)

- Molbio Diagnostics Limited (India)

- Takara Bio Inc. (Japan)

- Sonic Healthcare Limited (Australia)

- Metropolis Healthcare Ltd. (India)

- Dr Lal PathLabs Ltd. (India)

What are the Recent Developments in Asia-Pacific Acute Myeloid Leukemia Diagnostics Market?

- In August 2025, the Dr. B Borooah Cancer Institute (BBCI) in Guwahati organized an AML masterclass for young doctors. Discussions included advanced diagnostic tools such as flow cytometry, next-generation sequencing (NGS), and measurable residual disease assessment aiming to elevate clinical practice and diagnostic expertise

- In May 2025, medical experts in New Delhi revealed that the city records approximately 3,000 new cases of acute myeloid leukemia (AML) annually, particularly impacting adults aged 30 to 40. They highlighted significant delays in diagnosis, limited access to genetic testing, and low treatment completion rates only around 30% due to financial and insurance limitations

- In May 2024, HUTCHMED (China) Limited initiated the RAPHAEL Phase III clinical trial of HMPL-306, a novel dual-inhibitor targeting IDH1 and IDH2 mutations in relapsed or refractory AML patients in China. The first patient was dosed on May 11, 2024, marking a significant step toward precision-targeted AML therapy

- In April 2024, Novotech released a report highlighting that Asia reported over 68,000 AML cases with Mainland China, India, and Japan contributing approximately 30% to the Asia-Pacific’s global incidence, and Mainland China alone accounting for over 35% of cases

- In March 2023, QIAGEN entered a strategic collaboration with Servier to develop a companion diagnostic for the AML therapy drug TIBSOVO®, an IDH1 inhibitor. The diagnostic will consist of a real-time PCR test to detect IDH1 gene mutations in AML patients using blood and bone marrow samples, and it will be compatible with QIAGEN’s Rotor-Gene Q MDx platform

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.