Asia Pacific Blood Screening Market

Market Size in USD Million

USD

793.83 Million

USD

1,468.23 Million

2025

2033

USD

793.83 Million

USD

1,468.23 Million

2025

2033

| 2026 - 2033 | |

| USD 793.83 Million | |

| USD 1,468.23 Million | |

| % | |

|

Asia-Pacific Blood Screening Market Size

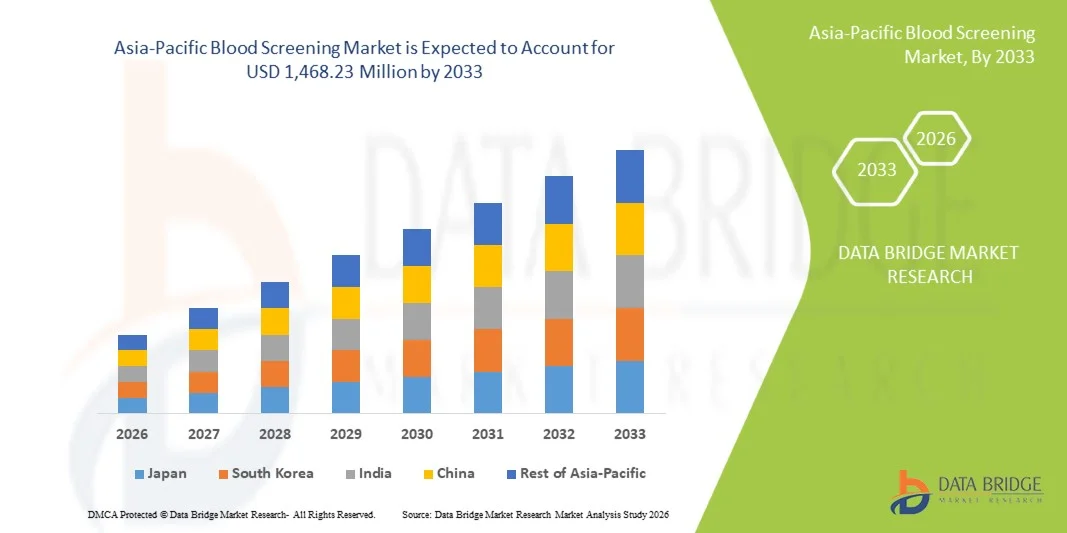

- The Asia-Pacific blood screening market size was valued at USD 793.83 million in 2025 and is expected to reach USD 1,468.23 million by 2033, at a CAGR of 7.99% during the forecast period

- The market growth is primarily driven by increasing prevalence of infectious diseases, growing demand for safe blood transfusions, and rising adoption of advanced diagnostic technologies in hospitals and blood banks across the region

- In addition, government initiatives promoting blood safety, along with the expansion of healthcare infrastructure and rising awareness among the population about transfusion-transmissible infections, are fueling the adoption of blood screening solutions. These factors collectively are accelerating market penetration, thereby significantly boosting the industry's growth

Asia-Pacific Blood Screening Market Analysis

- Blood screening, involving the testing of donated blood for infectious agents and transfusion-transmissible diseases, is becoming an essential component of healthcare safety protocols in hospitals, blood banks, and diagnostic laboratories in key countries

- The rising demand for blood screening is primarily driven by increasing awareness of blood-borne infections, growing prevalence of infectious diseases such as hepatitis and HIV, and the adoption of advanced, automated screening technologies that offer higher accuracy and faster turnaround times

- China dominated the Asia-Pacific blood screening market with the largest revenue share of 42.5% in 2025, supported by a growing population, expanding hospital networks, and strong government initiatives for blood safety

- India is expected to be the fastest growing country during the forecast period due to rising healthcare investments, increasing voluntary blood donations, and modernization of blood banks

- Nucleic Acid Testing segment dominated the Asia-Pacific blood screening market with a market share of 40.9% in 2025, driven by its high sensitivity, ability to detect early-stage infections, and growing adoption by blood banks and hospitals in China, India, and Japan aiming to minimize transfusion-transmitted infections

Report Scope and Asia-Pacific Blood Screening Market Segmentation

|

Attributes |

Asia-Pacific Blood Screening Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Blood Screening Market Trends

“Advancements Through Automated and High-Throughput Technologies”

- A significant and accelerating trend in the Asia-Pacific blood screening market is the adoption of automated and high-throughput screening technologies, enabling faster, more accurate detection of infectious agents in donated blood

- For instance, the Procleix Panther system in China integrates fully automated NAT testing, allowing multiple samples to be processed simultaneously with minimal human intervention, reducing errors and improving throughput

- These automated systems support enhanced pathogen detection, earlier identification of transfusion-transmissible infections, and reduction of human error, thereby increasing overall blood safety and reliability

- The integration of blood screening platforms with laboratory information management systems (LIMS) facilitates centralized monitoring, data analytics, and traceability of blood units across hospitals and blood banks, improving operational efficiency

- This trend towards more precise, efficient, and scalable screening technologies is transforming expectations for blood safety in the region, prompting companies such as Roche Diagnostics to develop fully automated, high-throughput solutions for major hospitals and national blood centers

- The demand for advanced automated blood screening systems is growing rapidly across both public and private healthcare sectors, as stakeholders prioritize efficiency, safety, and compliance with strict regulatory standards

- Rising investment in AI-driven diagnostic algorithms for blood screening is enabling predictive analysis of infection patterns and early intervention strategies

Asia-Pacific Blood Screening Market Dynamics

Driver

“Rising Prevalence of Infectious Diseases and Focus on Blood Safety”

- The increasing prevalence of infectious diseases such as hepatitis B, hepatitis C, and HIV, along with the growing awareness of blood safety, is a major driver for the heightened adoption of blood screening solutions

- For instance, in March 2025, China National Blood Center implemented expanded NAT screening for all donated blood, aiming to improve early detection of transfusion-transmissible infections

- As governments and healthcare providers emphasize safe blood transfusion practices, blood screening solutions offering high sensitivity and rapid turnaround are increasingly preferred over conventional testing methods

- Furthermore, expansion of hospital networks and voluntary blood donation programs across India, Japan, and Australia is boosting the adoption of automated blood screening platforms to handle higher testing volumes efficiently

- The focus on standardized protocols, accurate reporting, and reduced transfusion-related risks is propelling the integration of advanced screening solutions in both large urban hospitals and regional blood banks

- Supportive government policies and regulatory frameworks mandating comprehensive blood testing are accelerating the adoption of modern screening technologies

- Growing public-private partnerships in the healthcare sector are facilitating wider distribution of blood screening solutions to remote and underserved areas

Restraint/Challenge

“High Costs and Limited Infrastructure in Emerging Countries”

- The relatively high initial cost of advanced blood screening systems, coupled with maintenance and reagent expenses, poses a significant challenge to broader market penetration in emerging Asia-Pacific countries

- For instance, smaller hospitals and blood banks in India may face budget constraints that limit adoption of fully automated NAT testing platforms despite the proven safety benefits

- In addition, lack of trained personnel and limited laboratory infrastructure in rural areas hinders the effective deployment of sophisticated blood screening technologies, slowing market growth

- While costs are gradually decreasing, premium systems with high-throughput capabilities and integrated automation still remain expensive, restricting widespread adoption among smaller healthcare providers

- Overcoming these challenges through government subsidies, public-private partnerships, and localized low-cost solutions will be crucial for increasing adoption rates and ensuring safe blood screening across the region

- Variability in regulatory approvals and standards across different countries in Asia-Pacific can delay implementation of new blood screening technologies

- Dependence on imported reagents and equipment exposes smaller blood banks to supply chain disruptions, impacting consistent screening operations

Asia-Pacific Blood Screening Market Scope

The market is segmented on the basis of products and services, technology, disease type, and end user.

- By Products and Services

On the basis of products and services, the market is segmented into reagents and kits, instruments, software and services. The reagents and kits segment dominated the Asia-Pacific blood screening market with the largest revenue share in 2025, driven by the recurring need for high-quality reagents in blood testing, increasing prevalence of infectious diseases, and the expansion of voluntary blood donation programs. Blood banks and hospitals prioritize reagents and kits due to their direct role in ensuring accurate and timely screening of transfusion-transmissible infections. Continuous innovations in reagent formulations, higher sensitivity, and compatibility with automated testing platforms further strengthen the segment’s market position. Moreover, the availability of region-specific reagents tailored to local pathogen profiles enhances the adoption of these solutions across China, India, and Japan. Strong supplier networks and easy procurement also contribute to the sustained dominance of this segment.

The instruments segment is anticipated to witness the fastest growth during 2026–2033, fueled by increasing automation and adoption of high-throughput screening systems in hospitals and blood banks. Advanced instruments such as NAT platforms, ELISA analyzers, and automated sample processors reduce manual errors, increase testing efficiency, and enable simultaneous multi-sample analysis. Rising investments in upgrading laboratory infrastructure in emerging countries such as India and Southeast Asia are also boosting the uptake of instruments. The integration of instruments with laboratory information management systems (LIMS) allows real-time monitoring and data management, further enhancing operational efficiency. In addition, instrument manufacturers are focusing on compact, user-friendly designs suitable for medium-sized diagnostic centers, which accelerates adoption across the region.

- By Technology

On the basis of technology, the market is segmented into nucleic acid test (NAT), enzyme-linked immunosorbent assay (ELISA), rapid tests, Western blot assay, next-generation sequencing (NGS), and others. The Nucleic Acid Test (NAT) segment dominated the Asia-Pacific blood screening market with a revenue share of 40.9% in 2025, driven by its high sensitivity, early detection capabilities, and widespread adoption in major blood banks and hospitals. NAT is critical for identifying viral infections such as HIV, HBV, and HCV in donated blood, minimizing transfusion-transmitted infection risks. The ability to integrate NAT with automated high-throughput platforms makes it an attractive choice for large-scale screening programs. Government regulations and safety mandates across countries such as China and India also mandate NAT testing for blood safety, reinforcing the segment’s market dominance.

The rapid tests segment is expected to witness the fastest growth during 2026–2033, fueled by their quick turnaround time, ease of use, and minimal infrastructure requirements. Rapid tests are particularly valuable in smaller hospitals, rural diagnostic centers, and mobile blood donation units where immediate results are needed. Growing awareness of infectious diseases, increasing outreach programs, and the adoption of point-of-care testing models in countries such as India, Australia, and Southeast Asia are driving this growth. Moreover, manufacturers are innovating rapid test kits with higher sensitivity and broader pathogen coverage, enhancing their adoption in both public and private healthcare settings.

- By Disease Type

On the basis of disease type, the market is segmented into respiratory diseases, diabetes mellitus, oncology, cholesterol, HIV/AIDS, cold and flu, infectious diseases, and others. The infectious diseases segment dominated the Asia-Pacific blood screening market in 2025, driven by the high prevalence of blood-borne infections such as HIV, hepatitis B and C, and emerging pathogens. Blood banks and hospitals prioritize infectious disease testing to ensure safe transfusions and comply with regulatory mandates. Rising awareness among patients and healthcare providers about transfusion-transmissible infections also strengthens the dominance of this segment. Public health initiatives and government-funded blood safety programs in China, India, and Japan further support widespread adoption of screening for infectious diseases.

The HIV/AIDS segment is expected to witness the fastest growth during 2026–2033, fueled by rising incidence rates, government awareness campaigns, and mandatory screening policies for all donated blood. HIV testing is critical in reducing transmission risks, and the adoption of both NAT and rapid test technologies is increasing across diagnostic centers and hospitals. Expansion of voluntary blood donation drives in countries such as India and Thailand is boosting the demand for HIV-focused screening solutions. Furthermore, continuous technological advancements in HIV diagnostics, including point-of-care rapid tests, are facilitating faster adoption and improving accessibility in remote and rural regions.

- By End User

On the basis of end user, the market is segmented into diagnostic centers, blood banks, hospitals, clinics, and ambulatory surgical centers. The blood banks segment dominated the Asia-Pacific market in 2025 with the largest revenue share, as blood banks are the primary hubs for collection, testing, and storage of donated blood. Increasing regulatory emphasis on safe transfusions, implementation of advanced screening protocols, and rising voluntary blood donation programs drive the dominance of blood banks. Adoption of automated and high-throughput testing platforms in major national and regional blood banks across China, India, and Japan also strengthens this segment’s position.

The diagnostic centers segment is expected to witness the fastest growth during 2026–2033, fueled by increasing outsourcing of blood screening services, rising demand for preventive health checks, and the expansion of private healthcare infrastructure in urban and semi-urban areas. Diagnostic centers are increasingly investing in modern screening technologies such as NAT, ELISA, and rapid tests to cater to hospitals, clinics, and individual patients. The convenience of centralized testing, faster turnaround times, and access to advanced technology platforms drive the growing adoption of blood screening services in this segment. In addition, collaborations between diagnostic centers and blood banks enhance testing coverage and operational efficiency across Asia-Pacific countries.

Asia-Pacific Blood Screening Market Regional Analysis

- China dominated the Asia-Pacific blood screening market with the largest revenue share of 42.5% in 2025, supported by a growing population, expanding hospital networks, and strong government initiatives for blood safety

- Healthcare providers and blood banks in China highly prioritize accuracy, rapid testing, and early detection of infectious diseases, leading to widespread adoption of advanced screening technologies such as NAT and automated ELISA platforms

- This extensive adoption is further supported by increasing public awareness of blood-borne infections, rising voluntary blood donations, and continuous investments in modernizing blood screening infrastructure across hospitals and blood banks

The China Blood Screening Market Insight

The China blood screening market captured the largest revenue share in Asia in 2025, supported by the country’s massive population, expanding hospital networks, and stringent regulatory frameworks enforcing mandatory blood safety protocols. The government’s focus on expanding voluntary blood donation programs and implementing high-throughput automated screening systems is driving market adoption. Hospitals and blood banks are increasingly investing in NAT and ELISA platforms to ensure safer transfusions and minimize infection risks. In addition, the integration of these systems with laboratory information management systems (LIMS) allows real-time monitoring, improving efficiency and traceability of blood units across the country.

India Blood Screening Market Insight

The India blood screening market is expected to witness the fastest growth in Asia during the forecast period, fueled by rapid urbanization, modernization of blood banks, and rising awareness of transfusion-transmissible infections. Investments in laboratory automation, point-of-care testing facilities, and regional blood screening centers are enhancing accessibility and efficiency. Government-led initiatives and voluntary blood donation campaigns are expanding the coverage of safe blood transfusions, particularly in urban and semi-urban areas. The rising demand for affordable and reliable screening technologies, coupled with growing private healthcare infrastructure, is further driving market expansion.

Japan Blood Screening Market Insight

The Japan blood screening market is gaining momentum due to advanced healthcare infrastructure, high technology adoption, and stringent quality standards for blood safety. Hospitals and diagnostic centers are increasingly integrating automated, high-sensitivity NAT and ELISA screening technologies to detect infectious diseases at early stages. The country’s emphasis on patient safety, regulatory compliance, and continuous public awareness campaigns is driving widespread adoption. Japan’s aging population and rising demand for preventive healthcare services are also contributing to increased use of blood screening solutions in both hospital and outpatient settings.

Thailand Blood Screening Market Insight

The Thailand blood screening market is gradually expanding, supported by government-led programs and partnerships with private diagnostic providers to improve testing coverage and reduce transfusion-transmitted infection risks. Adoption of automated, rapid, and point-of-care testing technologies is increasing in hospitals, regional blood banks, and mobile blood collection units, particularly in urban centers. Continuous training programs for healthcare personnel, awareness campaigns for safe transfusions, and increasing public participation in voluntary blood donation drives are further promoting market growth.

Asia-Pacific Blood Screening Market Share

The Asia-Pacific Blood Screening industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Thermo Fisher Scientific (U.S.)

- Bio-Rad Laboratories (U.S.)

- Siemens Healthineers AG (Germany)

- BIOMÉRIEUX (France)

- Beckman Coulter (U.S.)

- SD BIOSENSOR (South Korea)

- Fujirebio (Japan)

- Ortho Clinical Diagnostics (U.S.)

- QIAGEN (Netherlands)

- Sysmex Corporation (Japan)

- Mindray (China)

- DiaSorin (Italy)

- Hologic (U.S.)

- Meridian Bioscience (U.S.)

- Illumina (U.S.)

- Agilent Technologies (U.S.)

- PerkinElmer (U.S.)

- Hangzhou Biotest Biotech Co., Ltd. (China)

What are the Recent Developments in Asia-Pacific Blood Screening Market?

- In December 2025, Surat Raktdan Kendra and Research Centre in India upgraded its blood screening with a fully automated Nucleic Acid Testing (NAT) system to detect HIV, Hepatitis B and Hepatitis C at the molecular level, identifying infections that traditional ELISA tests missed and significantly boosting transfusion safety

- In November 2025, the All India Institute of Medical Sciences (AIIMS), Nagpur inaugurated Central India’s first government‑run Individual Donor NAT (ID‑NAT) laboratory for screening donated blood for HIV, Hepatitis B and C during the window period, enhancing regional blood safety and diagnostic precision

- In August 2025, steps began to expand NAT‑PCR testing facilities across Odisha’s government blood centres in India, as the state Health & Family Welfare Department informed the High Court that it is actively working to operationalize Nucleic Acid Testing‑Polymerase Chain Reaction (NAT‑PCR) in 45 additional blood collection centres

- In May 2025, the World Health Organization (WHO) emphasized that all donated blood should be screened for HIV, hepatitis B and C, and syphilis, reinforcing standardized screening protocols critical guidance adopted by many Asia‑Pacific health systems to prevent transfusion‑transmitted infections

- In August 2024, reports from the Asia‑Pacific Plasma Leaders’ Network encouraged member states to improve blood and plasma product quality, safety measures, and wastage reduction a collaborative push that impacts screening practices and transfusion standards

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.