Asia Pacific Interventional Neurology Devices Market

Market Size in USD Million

USD

544.39 Million

USD

1,676.92 Million

2025

2033

USD

544.39 Million

USD

1,676.92 Million

2025

2033

| 2026 - 2033 | |

| USD 544.39 Million | |

| USD 1,676.92 Million | |

| % | |

|

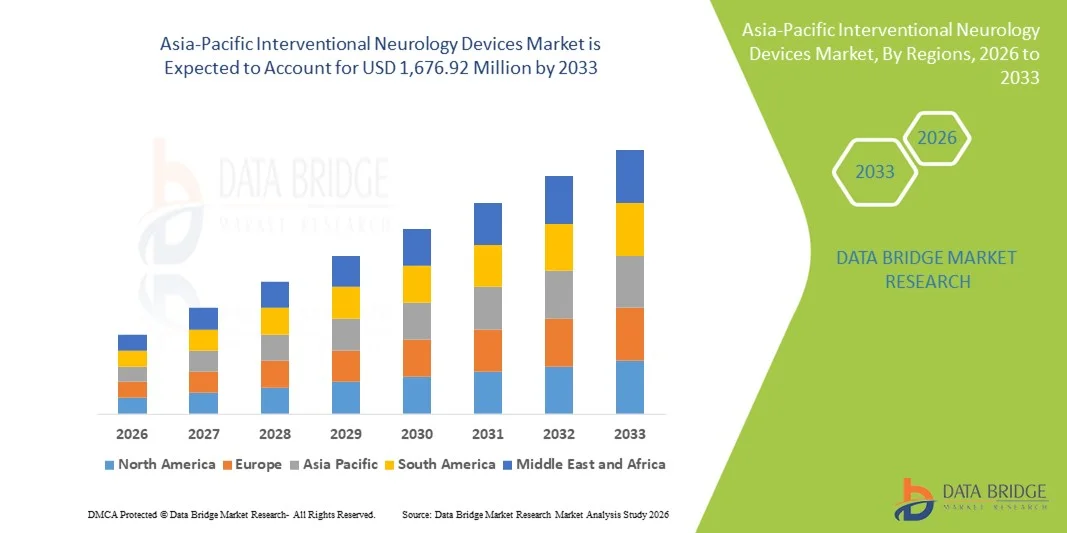

Asia-Pacific Interventional Neurology Devices Market Size

- The Asia-Pacific interventional neurology devices market size was valued at USD 544.39 million in 2025 and is expected to reach USD 1,676.92 million by 2033, at a CAGR of 15.1% during the forecast period

- The market growth is largely driven by rising prevalence of neurovascular disorders expanding healthcare infrastructure, and increasing awareness of minimally invasive neurointerventional procedures across key countries such as China, Japan, and India

- Furthermore, technological advancements in embolization, thrombectomy, and carotid stenting devices, coupled with growing clinical adoption and healthcare expenditure in emerging Asia-Pacific economies, are positioning interventional neurology devices as essential tools in modern cerebrovascular care. These converging factors are accelerating investment and uptake of advanced neurointerventional solutions, thereby significantly boosting the industry’s growth

Asia-Pacific Interventional Neurology Devices Market Analysis

- Interventional neurology devices, including embolization, thrombectomy, and carotid stenting systems, are increasingly vital in modern cerebrovascular care due to their minimally invasive approach, precision, and integration with advanced imaging technologies, improving outcomes for patients with stroke, aneurysms, and other neurovascular disorders

- The escalating demand for interventional neurology devices is primarily fueled by the rising prevalence of neurovascular diseases, expanding healthcare infrastructure, increasing awareness of minimally invasive procedures, and growing healthcare expenditure in key Asia-Pacific countries

- Japan dominated the Asia-Pacific interventional neurology devices market with the largest revenue share of 35.4% in 2025, characterized by a well-established healthcare system, advanced medical technology adoption, and strong presence of leading device manufacturers, with the country witnessing substantial growth in neurointerventional procedures driven by innovations in catheter-based and imaging-assisted therapies

- China is expected to be the fastest-growing markets in the Asia-Pacific region during the forecast period due to increasing urbanization, rising healthcare spending, and expansion of neurointerventional programs in both public and private hospitals

- Embolization devices segment dominated the Asia-Pacific interventional neurology devices market with a market share of 39.4% in 2025, driven by their established efficacy in treating cerebral aneurysms, wide clinical adoption, and compatibility with modern imaging systems

Report Scope and Asia-Pacific Interventional Neurology Devices Market Segmentation

|

Attributes |

Asia-Pacific Interventional Neurology Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Interventional Neurology Devices Market Trends

Minimally Invasive Procedures and Robotics Integration

- A significant and accelerating trend in the Asia-Pacific interventional neurology devices market is the increasing adoption of minimally invasive procedures supported by robotics and advanced catheter-based systems, enhancing procedural precision and reducing patient recovery times

- For instance, robotic-assisted thrombectomy systems allow neurointerventionists to navigate complex cerebral vasculature with higher accuracy, improving procedural outcomes and safety. Similarly, advanced microcatheter technologies provide greater flexibility and access to previously difficult-to-reach neurovascular regions

- Robotics and navigation-assisted interventions enable features such as real-time imaging guidance, automated device positioning, and improved operator ergonomics. For instance, some Magellan robotic platforms improve catheter stability and reduce radiation exposure for clinicians during complex aneurysm or stroke interventions. Furthermore, integration with AI-driven imaging can help identify vascular anomalies and optimize device deployment

- The seamless integration of these devices with advanced imaging modalities and hospital IT systems facilitates centralized procedural planning and post-procedure monitoring. Through a single interface, clinicians can manage imaging, device navigation, and patient monitoring, creating a unified and efficient intervention workflow

- This trend toward more precise, automated, and technology-assisted neurointerventional solutions is fundamentally reshaping expectations for cerebrovascular care. Consequently, companies such as Stryker and Medtronic are developing robotic-enabled interventional neurology devices with advanced navigation and AI-assisted imaging capabilities

- The demand for neurointerventional devices that offer robotic assistance and imaging integration is growing rapidly across both public and private hospitals, as healthcare providers increasingly prioritize procedural safety, efficiency, and patient outcomes

- Increasing collaboration between device manufacturers and AI/software developers is also enabling predictive analytics for patient outcomes, further enhancing the appeal of advanced interventional neurology solutions.

Asia-Pacific Interventional Neurology Devices Market Dynamics

Driver

Rising Prevalence of Neurovascular Disorders and Healthcare Expansion

- The increasing prevalence of stroke, aneurysms, and other neurovascular disorders, coupled with expanding healthcare infrastructure, is a significant driver for the heightened demand for interventional neurology devices

- For instance, in March 2025, Medtronic announced a new AI-assisted thrombectomy program in leading hospitals across India, aiming to improve stroke treatment access and outcomes. Such initiatives by key companies are expected to drive market growth in the forecast period

- As awareness of neurovascular conditions rises and minimally invasive interventions gain acceptance, interventional devices offer advanced features such as real-time imaging guidance, catheter precision, and robotic-assisted navigation, providing a compelling alternative to conventional surgical methods

- Furthermore, government programs and private hospital investments in neurointerventional infrastructure are making these devices an essential component of modern cerebrovascular care, integrating seamlessly with hospital imaging systems

- The combination of increasing patient awareness, rising healthcare expenditure, and technological advancements in device design and procedural efficiency is propelling adoption of interventional neurology devices across Asia-Pacific hospitals and specialized centers

- Rising collaborations between hospitals and device manufacturers for training programs and procedural workshops are also accelerating adoption, ensuring clinicians are confident in using advanced technologies

- Growing investments in research and development to create region-specific devices suitable for diverse anatomical and demographic patient profiles further strengthen market growth

Restraint/Challenge

High Cost and Regulatory Hurdles

- The relatively high cost of advanced interventional neurology devices, including robotic-assisted systems and AI-enabled imaging platforms, poses a significant challenge to broader market adoption, particularly in developing Asia-Pacific countries

- For instance, smaller hospitals and clinics may delay adoption due to budget constraints, limiting the penetration of high-end devices into tier-2 and tier-3 cities

- Addressing these cost barriers through flexible pricing models, leasing options, and local manufacturing is crucial for wider adoption. Companies such as Stryker and Penumbra emphasize cost-effective device options and training programs to support adoption in emerging markets. In addition, navigating regulatory approvals for medical devices in multiple countries can delay product launches and complicate market entry

- While reimbursement policies are gradually improving, the perceived premium of advanced interventional devices can still hinder adoption in price-sensitive regions, especially where traditional surgical approaches are still prevalent

- Overcoming these challenges through regulatory harmonization, clinician training, and cost-optimized device solutions will be vital for sustained market growth

- Limited availability of skilled neurointerventionalists in smaller cities and rural areas further constrains market penetration, requiring additional training initiatives and talent development programs

- The complexity of device maintenance and need for ongoing software updates, particularly for AI-enabled and robotic systems, adds operational challenges for hospitals, which may slow adoption in resource-constrained settings

Asia-Pacific Interventional Neurology Devices Market Scope

The market is segmented on the basis of product type, disease pathology, procedure, and end user.

- By Product Type

On the basis of product type, the Asia-Pacific interventional neurology devices market is segmented into aneurysm coiling and embolization devices, cerebral balloon angioplasty and stenting systems, support devices, and neurothrombectomy devices. The aneurysm coiling and embolization devices segment dominated the market with the largest revenue share of 39.4% in 2025, driven by its critical role in treating cerebral aneurysms and arteriovenous malformations. Hospitals and neurointerventional centers prioritize these devices due to their minimally invasive nature, high clinical efficacy, and ability to reduce patient recovery time. The market sees strong demand as these devices are widely compatible with advanced imaging systems and catheter navigation technologies, enabling safer and more precise interventions. In addition, growing awareness of stroke and aneurysm treatment in Asia-Pacific countries such as Japan, China, and India contributes to the segment’s dominance. Continuous innovations, including coil material improvements and microcatheter design enhancements, further support its market leadership.

The neurothrombectomy devices segment is anticipated to witness the fastest growth rate of 10.5% CAGR from 2026 to 2033, fueled by increasing ischemic stroke incidence and the urgent need for clot removal procedures. These devices are preferred in emergency stroke care due to their ability to rapidly restore blood flow and improve patient outcomes. The segment’s growth is also supported by advancements in catheter design, AI-assisted navigation, and robotic integration, which enhance procedural safety and efficiency. Expansion of stroke care programs in China and India and increasing reimbursement coverage for thrombectomy procedures are additional growth drivers.

- By Disease Pathology

On the basis of disease pathology, the market is segmented into ischemic strokes, cerebral aneurysms, arteriovenous malformation (AVM) and fistulas, and others. The ischemic strokes segment dominated the market with a revenue share of 41% in 2025, driven by the high prevalence of stroke in the Asia-Pacific region and the critical need for rapid intervention to reduce morbidity and mortality. Hospitals and neurology centers widely adopt interventional devices for ischemic stroke management due to improved patient outcomes and reduced long-term care costs. Increasing awareness of stroke symptoms, government initiatives for early intervention, and rising adoption of thrombectomy procedures contribute to this dominance. Advanced neuroimaging and AI-guided intervention systems further reinforce this segment’s importance in clinical practice.

The cerebral aneurysms segment is expected to witness the fastest growth during the forecast period, fueled by rising diagnosis rates due to better imaging technologies and increased public awareness of neurovascular conditions. Embolization and coiling devices are the preferred treatment, offering minimally invasive options that reduce procedural risks. Expansion of specialized neurointerventional centers and training programs across Asia-Pacific countries supports rapid adoption of these devices.

- By Procedure

On the basis of procedure, the market is segmented into embolization, angioplasty, neurothrombectomy, and others. The embolization segment dominated the market with a revenue share of 38% in 2025, due to its essential role in treating cerebral aneurysms, AVMs, and other neurovascular abnormalities. The procedure is widely preferred for its minimally invasive nature, precision, and high success rates, enabling shorter hospital stays and quicker patient recovery. Hospitals and specialized neurology centers often prioritize embolization due to its compatibility with advanced catheter and imaging systems. Continuous technological innovations in embolization coils and delivery systems also strengthen its market position. Furthermore, growing awareness of cerebrovascular diseases and the benefits of minimally invasive procedures drive the segment’s adoption.

The neurothrombectomy procedure segment is anticipated to witness the fastest growth from 2026 to 2033, driven by the rising incidence of ischemic strokes and the urgent need for clot removal interventions. These procedures offer rapid restoration of cerebral blood flow, improving patient survival and functional outcomes. AI-assisted and robotic-guided thrombectomy systems further enhance procedural safety and effectiveness. Increasing investment in stroke treatment programs and healthcare infrastructure across China, India, and Southeast Asia fuels the segment’s growth.

- By End User

On the basis of end user, the market is segmented into hospitals, neurology clinics, ambulatory care centers, and others. The hospitals segment dominated the market with a revenue share of 55% in 2025, due to the availability of advanced neurointerventional facilities, imaging systems, and trained clinicians capable of performing complex procedures. Hospitals provide comprehensive treatment for strokes, aneurysms, and AVMs, making them the primary purchasers of interventional neurology devices. Large hospitals and teaching medical centers also act as key hubs for clinical trials and new device adoption, further strengthening market dominance. In addition, hospitals benefit from better reimbursement policies and government support for high-cost neurointerventional procedures.

The neurology clinics segment is expected to witness the fastest growth from 2026 to 2033, driven by the expansion of specialized outpatient centers and smaller clinics offering minimally invasive interventions. Clinics are increasingly adopting portable and AI-assisted devices to perform selective neurointerventions, enabling faster diagnosis and treatment. Growth in patient awareness, early screening programs, and partnerships with device manufacturers accelerate adoption in this segment.

Asia-Pacific Interventional Neurology Devices Market Regional Analysis

- Japan dominated the Asia-Pacific interventional neurology devices market with the largest revenue share of 35.4% in 2025, characterized by a well-established healthcare system, advanced medical technology adoption, and strong presence of leading device manufacturers

- Healthcare providers in the region prioritize minimally invasive procedures and advanced devices for treating strokes, aneurysms, and AVMs, ensuring high demand for embolization, thrombectomy, and stenting systems

- This widespread adoption is further supported by government initiatives promoting neurovascular care, high healthcare expenditure, and increasing awareness among patients and clinicians about the benefits of early intervention, positioning interventional neurology devices as a preferred choice across hospitals and specialized centers

The Japan Interventional Neurology Devices Market Insight

The Japan interventional neurology devices market captured the largest revenue share of 35.4% in 2025 within Asia-Pacific, driven by advanced healthcare infrastructure, high adoption of minimally invasive neurointerventional procedures, and a strong presence of key device manufacturers. Hospitals and specialized neurocenters prioritize embolization, thrombectomy, and stenting systems due to their precision, improved patient outcomes, and reduced recovery times. The integration of AI-assisted imaging and robotic navigation in procedures is further driving adoption. In addition, Japan’s aging population and rising awareness of stroke and aneurysm treatments are increasing demand for safer and easier-to-use neurointerventional devices in both residential and commercial hospitals.

China Interventional Neurology Devices Market Insight

The China interventional neurology devices market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the rising prevalence of stroke and other neurovascular disorders, coupled with rapid urbanization and expanding healthcare infrastructure. Hospitals and specialty clinics are increasingly investing in advanced embolization, thrombectomy, and stenting systems to improve patient outcomes. Government initiatives promoting stroke care, early diagnosis, and public awareness campaigns further accelerate device adoption. The integration of AI-assisted navigation and minimally invasive techniques enhances procedural efficiency, making China a key growth market in the region.

India Interventional Neurology Devices Market Insight

The India market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising stroke prevalence, expanding healthcare infrastructure, and rapid adoption of minimally invasive neurointerventional procedures. Hospitals and specialty neurocenters are increasingly deploying embolization, thrombectomy, and stenting devices to improve treatment outcomes. Government programs for stroke care, coupled with the growth of smart hospitals and affordable locally manufactured devices, are key factors driving adoption. Increasing clinician training programs and public awareness initiatives further support market penetration across urban and semi-urban regions.

South Korea Interventional Neurology Devices Market Insight

The South Korea interventional neurology devices market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of neurovascular diseases, growing healthcare expenditure, and adoption of AI-assisted and robotic-enabled devices. Hospitals and specialty clinics are actively integrating embolization, thrombectomy, and stenting systems with advanced imaging technologies to enhance procedural precision and patient safety. Government-backed healthcare programs, coupled with high standards of patient care, are driving demand. The country’s strong focus on innovation and technologically advanced interventions positions it as a key market in the Asia-Pacific region.

Asia-Pacific Interventional Neurology Devices Market Share

The Asia-Pacific Interventional Neurology Devices industry is primarily led by well-established companies, including:

- MicroPort Scientific Corporation (China)

- Boston Scientific Corporation (U.S.)

- Penumbra, Inc. (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Terumo Corporation (Japan)

- Acandis GmbH (Germany)

- Phenox GmbH (Germany)

- Kaneka Corporation (Japan)

- Integra LifeSciences Corporation (U.S.)

- Abbott (U.S.)

- Balt Group (France)

- UreSil, LLC (U.S.)

- Medikit Co., Ltd. (Japan)

- B. Braun SE (Germany)

- Cook (U.S.)

- Zylox-Tonbridge Medical Technology Co., Ltd. (China)

- Shunmei Medical (China)

- NeuroFlow Dynamics (India)

What are the Recent Developments in Asia-Pacific Interventional Neurology Devices Market?

- In December 2025, All India Institute of Medical Sciences (AIIMS), New Delhi, successfully concluded the first clinical trial in India of a domestically developed advanced stroke intervention device called Supernova (a stent retriever), demonstrating clinical outcomes comparable with international standards and paving the way for broader, affordable stroke care access across Asia‑Pacific centers

- In December 2025, India’s first homegrown Supernova stent retriever demonstrated strong clinical results, following a successful multicentre trial led by AIIMS New Delhi under the GRASSROOT study, showing 94% blood flow restoration in large vessel occlusion stroke patients. The trial results, matching global performance standards, led to approval by India’s Central Drugs Standard Control Organisation

- In September 2025, Gravity Medical Technology announced that its Supernova stent retriever device, designed for mechanical thrombectomy in ischemic stroke treatment, received regulatory approval in India, marking a key milestone for expanding advanced clot‑retrieval technology in the Asia‑Pacific region’s stroke care landscape. This approval supports wider adoption in hospitals and stroke centers to improve clinical outcomes for acute cerebrovascular events

- In September 2025, India approved the Supernova stent retriever device for ischemic stroke intervention, with regulatory clearance following multicentric clinical trials involving major hospitals including AIIMS Delhi and JIPMER Pondicherry. This revolutionary device, designed to remove blood clots via catheter navigation and mesh expansion, is expected to significantly enhance stroke recovery outcomes in the country

- In August 2023, Rapid Medical’s Tigertriever thrombectomy device secured regulatory approval in China, enhancing localized treatment options for ischemic stroke patients and demonstrating technology transfer partnerships (with MicroPort Scientific) to expand neurointerventional device availability in Asia‑Pacific

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.