Asia Pacific Surgical Visualization Products Market

Market Size in USD Billion

USD

1.04 Billion

USD

3.39 Billion

2024

2032

USD

1.04 Billion

USD

3.39 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.04 Billion | |

| USD 3.39 Billion | |

| % | |

|

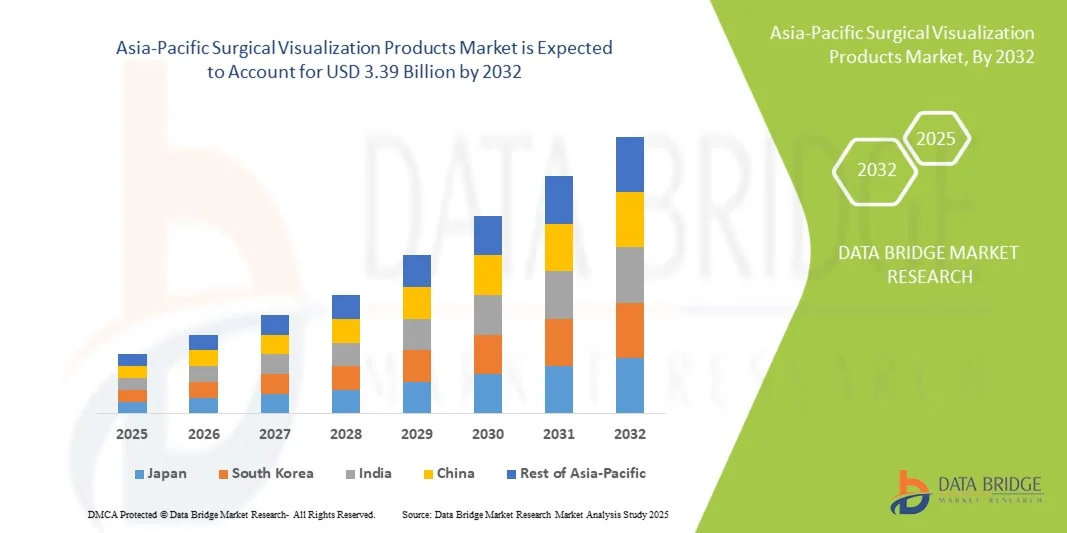

Asia-Pacific Surgical Visualization Products Market Size

- The Asia-Pacific surgical visualization products market size was valued at USD 1.04 billion in 2024 and is expected to reach USD 3.39 billion by 2032, at a CAGR of 15.9% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive surgeries, advancements in imaging technologies, and the rising demand for high-definition visualization systems that enhance surgical precision and patient outcomes

- Furthermore, innovations such as 3D visualization, augmented reality, and fluorescence imaging are transforming surgical practices, making visualization products indispensable in modern operating rooms

Asia-Pacific Surgical Visualization Products Market Analysis

- Surgical visualization products, including endoscopes, cameras, and imaging systems, are increasingly vital components of modern operating rooms in both hospitals and surgical centers due to their ability to enhance precision, improve patient outcomes, and enable minimally invasive procedures

- The escalating demand for surgical visualization products is primarily fueled by the growing adoption of minimally invasive surgeries, rising prevalence of chronic diseases, and increasing investments in advanced healthcare infrastructure across the region

- Japan dominated the Asia-Pacific surgical visualization products market in 2024, with a revenue share of 28.5%, owing to its well-established healthcare infrastructure, early adoption of advanced surgical technologies, and strong presence of key medical device manufacturers in the country

- China is expected to be the fastest-growing country in the Asia-Pacific market during the forecast period, driven by expanding hospital infrastructure, government initiatives to upgrade healthcare facilities, rising medical tourism, and increasing adoption of advanced surgical technologies

- Laparoscopy segment dominated the surgical visualization products market with a market share of 38.9% in 2024, driven by its critical role in minimally invasive surgeries and increasing surgeon preference for high-definition imaging systems

Report Scope and Asia-Pacific Surgical Visualization Products Market Segmentation

|

Attributes |

Asia-Pacific Surgical Visualization Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Surgical Visualization Products Market Trends

“Enhanced Precision and Imaging Through Advanced Technologies”

- A significant and accelerating trend in the Asia-Pacific surgical visualization products market is the increasing incorporation of advanced imaging technologies such as 3D visualization, augmented reality (AR), and fluorescence imaging, which enhance surgical accuracy and improve patient outcomes

- For instance, Olympus’ VISERA ELITE II system integrates high-definition 3D visualization and AR overlays, allowing surgeons to navigate complex anatomical structures with improved precision. Similarly, Stryker’s 1688 AIM 4K camera system provides enhanced clarity and image-guided surgery support

- AR and 3D imaging technologies enable features such as real-time anatomical mapping, improved depth perception, and guidance for minimally invasive procedures, reducing operation times and surgical errors. For instance, Karl Storz systems employ AR-assisted overlays to highlight critical tissue during laparoscopic procedures

- The seamless integration of these visualization systems with robotic-assisted surgery platforms and hospital IT networks facilitates centralized control over surgical procedures, enabling real-time monitoring and collaboration among surgical teams

- This trend towards more intelligent, intuitive, and integrated surgical visualization solutions is fundamentally reshaping expectations for operating room technologies. Consequently, companies such as Medtronic are developing platforms with enhanced imaging guidance and real-time feedback for complex procedures

- The demand for surgical visualization products that offer advanced imaging, real-time guidance, and seamless integration is growing rapidly across hospitals and surgical centers, as medical professionals increasingly prioritize precision and minimally invasive approaches

- Increasing awareness and training programs among surgeons regarding advanced visualization tools are further accelerating adoption, as medical professionals seek to leverage new technologies for improved surgical outcomes

Asia-Pacific Surgical Visualization Products Market Dynamics

Driver

“Rising Adoption of Minimally Invasive Surgeries and Advanced Healthcare Infrastructure”

- The increasing prevalence of minimally invasive surgeries, coupled with expanding healthcare infrastructure across Asia-Pacific, is a significant driver for the heightened demand for surgical visualization products

- For instance, in 2024, China’s Ministry of Health reported substantial investments in upgrading hospitals with advanced laparoscopic and endoscopic imaging systems, supporting growth in the regional market

- As healthcare providers seek to improve surgical precision, patient safety, and post-operative outcomes, surgical visualization products offer high-definition imaging, guidance, and reduced operation times, providing a compelling upgrade over conventional techniques

- Furthermore, the rising medical tourism and government initiatives to modernize hospitals are making surgical visualization systems an integral component of state-of-the-art surgical facilities, offering seamless integration with other medical devices

- The need for enhanced surgical outcomes, combined with increasing investments in advanced technologies and training programs, is propelling the adoption of these products in both public and private healthcare sectors across the region

- Increasing prevalence of chronic diseases and surgical procedures in countries such as India, Japan, and South Korea is driving demand for high-quality visualization tools that improve operative efficiency and patient recovery

- Expansion of telemedicine and remote surgical consultation initiatives is encouraging the use of visualization systems that support real-time video sharing and remote guidance, further boosting market adoption

Restraint/Challenge

“High Costs and Regulatory Compliance Hurdles”

- The relatively high cost of advanced surgical visualization systems, along with stringent regulatory approval requirements, poses a significant challenge to broader market penetration in Asia-Pacific

- For instance, high-end systems such as 4K laparoscopic towers or AR-assisted platforms require substantial capital investment, making adoption challenging for smaller hospitals or clinics in developing countries

- Navigating diverse regulatory standards, including medical device approvals, safety certifications, and import restrictions, is crucial for manufacturers to market their products successfully across multiple countries. For instance, Karl Storz and Stryker must comply with each country’s regulatory framework before launching new imaging systems

- In addition, maintenance costs, specialized training requirements, and limited technical expertise in certain regions can hinder the adoption of these advanced products

- Overcoming these challenges through cost optimization, modular product offerings, regulatory alignment, and surgeon training programs will be vital for sustained market growth in the Asia-Pacific surgical visualization sector

- Limited awareness among smaller healthcare facilities about the benefits of advanced visualization technologies may slow adoption, requiring targeted education and demonstration programs

- Supply chain disruptions and component shortages, particularly for high-tech imaging systems, can delay product availability and adoption, posing a temporary challenge to market expansion

Asia-Pacific Surgical Visualization Products Market Scope

The market is segmented on the basis of product type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the market is segmented into endoscopic cameras, accessories, light sources, display and monitors, video recorders & processors, camera heads, and video converters. The endoscopic camera segment dominated the market in 2024, accounting for the largest revenue share of 32%. This dominance is driven by the critical role of endoscopic cameras in minimally invasive surgeries, providing high-definition imaging and real-time visualization. Hospitals and surgical centers prioritize high-resolution cameras to enhance surgical precision and patient safety. The segment also benefits from technological advancements such as 4K resolution, AR overlays, and integration with robotic-assisted surgical systems. Surgeons prefer endoscopic cameras due to their versatility across multiple procedures including laparoscopy, arthroscopy, and ENT surgeries. Strong manufacturer support for upgrades, service, and maintenance ensures continued adoption and replacement cycles in established hospitals.

The display and monitors segment is anticipated to witness the fastest growth from 2025 to 2032, driven by increasing demand for high-definition visualization and 3D displays that improve surgeon perception during complex procedures. Advanced monitors with AR overlays and customizable display options are being adopted in both public and private hospitals. Integration with imaging platforms allows real-time recording, sharing, and remote consultations, enhancing surgical efficiency. Rising healthcare expenditure and expanding hospital infrastructure in countries such as China and India further support growth. In addition, increasing awareness among surgeons about enhanced visual guidance tools is driving adoption. The trend toward larger, multi-modal operating rooms also supports demand for advanced display systems.

- By Application

On the basis of application, the market is segmented into arthroscopy, laparoscopy, ENT endoscopy, obstetrics/gynecology endoscopy, urology endoscopy, gastroscopy, and others. The laparoscopy segment dominated the market with the largest share of 38.9% in 2024, owing to the widespread adoption of minimally invasive abdominal surgeries and the critical need for precise visualization. Hospitals and specialty clinics rely on laparoscopic visualization systems to reduce patient recovery times, minimize surgical errors, and enhance procedural efficiency. High-definition cameras and AR-assisted visualization are key factors in its adoption. Laparoscopy also benefits from rising patient preference for minimally invasive procedures and increasing training programs for surgeons. The segment is supported by favorable reimbursement policies in several Asia-Pacific countries and rising medical tourism in the region. Strong partnerships between manufacturers and hospitals for surgeon training also drive continued use of laparoscopic visualization systems.

The ENT endoscopy segment is projected to witness the fastest CAGR from 2025 to 2032, driven by increasing ENT disorder prevalence, growing awareness of early diagnosis, and the rising number of specialized ENT clinics. Adoption of high-definition and 3D endoscopes allows precise diagnosis and treatment of nasal, sinus, and ear disorders. Technological advancements and miniaturization of endoscopes enhance surgeon convenience and patient comfort. Growth is further supported by government initiatives promoting ENT care and rising investments in private specialty hospitals. The trend of integrating ENT visualization systems with hospital IT and remote consultation platforms is also accelerating adoption.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, diagnostic imaging centers, ambulatory surgical centers, and others. Hospitals dominated the market in 2024 with a share of 55%, due to their high surgical volumes, established infrastructure, and preference for comprehensive visualization systems. Hospitals adopt advanced surgical visualization tools to support a wide range of procedures, including minimally invasive and complex surgeries. Ongoing capital investments in imaging equipment and surgeon training programs reinforce this dominance. In addition, hospitals leverage these systems for multiple specialties, maximizing return on investment and enhancing patient outcomes. The presence of large healthcare networks in Japan, South Korea, and Australia further consolidates this dominance. Manufacturer-led training programs and service contracts make hospitals the primary buyers of advanced visualization systems.

Ambulatory surgical centers are expected to witness the fastest growth from 2025 to 2032, driven by the rising number of outpatient procedures and cost-effective surgical alternatives to hospitals. These centers are increasingly adopting compact and portable visualization solutions that support day surgeries, reduce operation times, and improve patient throughput. Growth is encouraged by favorable government policies, expanding healthcare infrastructure, and increasing patient preference for outpatient surgical care. Portable visualization platforms allow smaller centers to access high-quality imaging without heavy capital expenditure. Partnerships with distributors to provide turnkey solutions further boost adoption in ambulatory settings.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment dominated the market in 2024 with a share of 60%, owing to strong relationships between manufacturers and hospitals or government institutions. Direct tender ensures reliable supply, customization of products, and long-term service contracts. Hospitals often prefer this channel for large-scale procurement and access to the latest product innovations. Direct procurement also facilitates integration of surgical visualization systems with existing hospital IT and surgical suites. Manufacturer-led training and maintenance programs further reinforce the dominance of direct tender channels. Governments and large hospital chains in Japan, China, and Australia often prefer direct tenders due to centralized procurement efficiency.

The third-party distributors segment is anticipated to witness the fastest growth from 2025 to 2032, driven by expanding reach to specialty clinics, smaller hospitals, and emerging markets across Asia-Pacific. Third-party distributors provide flexibility, localized support, and quicker access to new product launches, particularly in tier-2 and tier-3 cities. Growth is further fueled by partnerships between distributors and manufacturers to provide bundled solutions and training programs for end-users in remote locations. Distributors often offer financing or leasing options, making advanced visualization products accessible to smaller healthcare facilities. Rapid urbanization and expansion of healthcare networks in developing countries also support distributor-led growth.

Asia-Pacific Surgical Visualization Products Market Regional Analysis

- Japan dominated the Asia-Pacific surgical visualization products market in 2024, with a revenue share of 28.5%, owing to its well-established healthcare infrastructure, early adoption of advanced surgical technologies, and strong presence of key medical device manufacturers in the country

- Hospitals and surgical centers in Japan highly value the precision, high-definition imaging, and integration capabilities offered by modern surgical visualization systems, which enhance surgical outcomes and patient safety

- This widespread adoption is further supported by high healthcare expenditure, government initiatives to modernize hospitals, and a skilled medical workforce, establishing surgical visualization systems as the preferred solution for complex and minimally invasive procedures

Japan Surgical Visualization Products Market Insight

The Japan surgical visualization products market is gaining momentum due to the country’s advanced healthcare infrastructure, high adoption of minimally invasive surgeries, and strong presence of key medical device manufacturers. Hospitals and surgical centers in Japan prioritize precision, high-definition imaging, and integration capabilities offered by modern visualization systems. Moreover, the increasing demand for complex and specialty surgeries, coupled with continuous technological upgrades in hospitals, is fueling growth. Japan’s aging population and rising medical tourism further contribute to the adoption of surgical visualization products in both public and private healthcare facilities.

China Surgical Visualization Products Market Insight

The China surgical visualization products market is expected to witness the fastest growth in the Asia-Pacific region, driven by expanding hospital infrastructure, rising medical tourism, increasing government initiatives for healthcare modernization, and growing awareness of advanced surgical technologies. The adoption of high-definition imaging systems and 3D visualization is rapidly increasing across public and private hospitals. In addition, domestic and international manufacturers are investing heavily in R&D and localized production to meet rising demand. Training programs for surgeons in advanced surgical techniques are also accelerating market growth.

India Surgical Visualization Products Market Insight

The India surgical visualization products market accounted for the largest revenue share in the Asia-Pacific region in 2024, attributed to rapid hospital expansion, rising outpatient and minimally invasive surgeries, and increasing healthcare expenditure. Hospitals, specialty clinics, and ambulatory surgical centers are increasingly adopting high-definition endoscopic cameras, displays, and image processing systems. The country’s push toward smart hospitals and digital health solutions, combined with affordable visualization products and local manufacturing, is driving adoption. Furthermore, the growing number of medical colleges and surgeon training programs ensures skilled personnel to operate advanced surgical systems.

Australia Surgical Visualization Products Market Insight

The Australia surgical visualization products market is experiencing steady growth, fueled by well-established healthcare infrastructure, high awareness of advanced surgical procedures, and strong adoption of minimally invasive surgeries. Hospitals and specialty centers prioritize high-quality imaging and real-time visualization systems to enhance patient safety and surgical outcomes. Government support for upgrading hospital technologies, combined with ongoing investments from key market players, is promoting adoption. In addition, collaboration with international manufacturers for technology transfer and training programs is strengthening market growth in Australia.

Asia-Pacific Surgical Visualization Products Market Share

The Asia-Pacific Surgical Visualization Products industry is primarily led by well-established companies, including:

- Olympus Corporation (Japan)

- Stryker (U.S.)

- Medtronic (Ireland)

- Karl Storz GmbH & Co. KG (Germany)

- FUJIFILM Holdings Corporation (Japan)

- Laborie (Netherlands)

- Smith & Nephew (U.K.)

- GE Healthcare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- Alcon Inc. (U.S.)

- Asensus Surgical US, Inc (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- 3D Surgical (U.S.)

- Zowietek Electronics Ltd. (India)

- Richard Wolf GmbH (Germany)

- MediThinQ (India)

What are the Recent Developments in Asia-Pacific Surgical Visualization Products Market?

- In October 2025, Olympus Corporation's feasibility study on endoscopy infection control systems in India was selected for the Ministry of Economy, Trade, and Industry's (METI) Global South Co-Creation Subsidy Program. This initiative aims to enhance the quality and accessibility of endoscopic procedures in developing countries, aligning with Olympus's commitment to global healthcare improvement

- In September 2025, Olympus India inaugurated a state-of-the-art repair facility aimed at strengthening its service capabilities for surgical visualization products. This facility is expected to enhance the company's after-sales support and maintenance services, ensuring the longevity and optimal performance of its medical imaging equipment across the region

- In July 2025, Johnson & Johnson announced the expansion of its VARIPULSE™ platform across the Asia-Pacific region. This platform is designed to advance the treatment of atrial fibrillation through minimally invasive procedures, integrating surgical visualization technologies to improve procedural outcomes and patient safety

- In April 2025, Fujifilm India unveiled its ELUXEO 8000 Therapeutic Endoscopy Solution at the 22nd MUMBAI LIVE Endoscopy event. This advanced system integrates cutting-edge imaging technologies, including a new CMOS sensor and 4K output, to provide enhanced image clarity and superior navigation in complex anatomies. Designed for minimally invasive procedures, the ELUXEO 8000 aims to reduce patient discomfort, expedite recovery times, and lower the risk of complications

- In March 2025, Stryker Corporation showcased the next generation of its Mako SmartRobotics™ system at the American Academy of Orthopaedic Surgeons (AAOS) Annual Meeting. The updated platform features enhanced 3D CT-based planning capabilities, including augment and screw planning, intraoperative screw trajectory guidance, and compatibility with Stryker’s revision hip implant portfolio

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.