Europe Adalimumab Market

Market Size in USD Billion

USD

6.35 Billion

USD

21.10 Billion

2025

2033

USD

6.35 Billion

USD

21.10 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.35 Billion | |

| USD 21.10 Billion | |

| % | |

|

Europe Adalimumab Market Overview

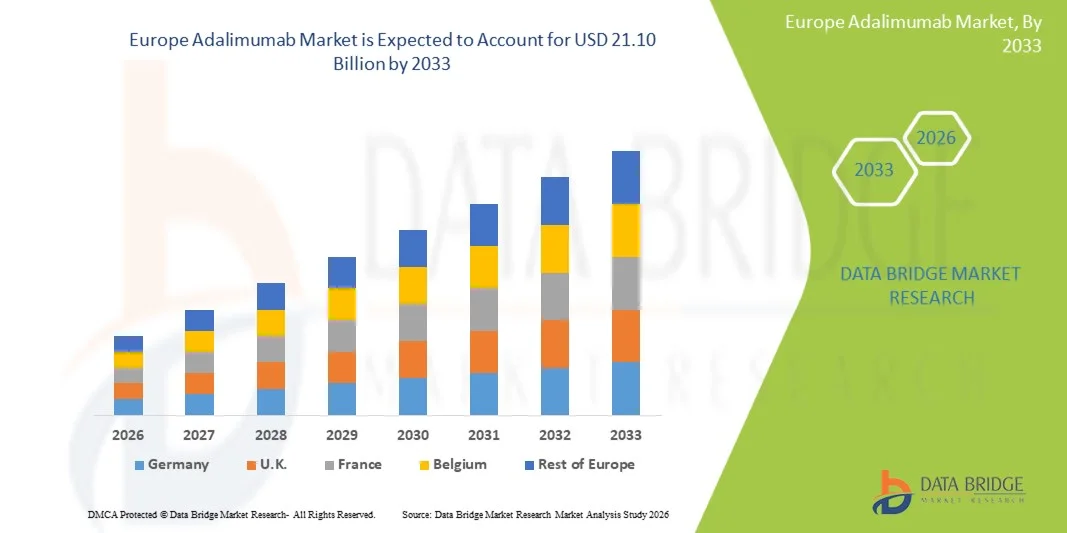

The Europe adalimumab market was valued at USD 6.35 billion in 2025 and is projected to reach USD 21.10 billion by 2033, growing at a CAGR of 16.2% from 2026 to 2033. The market is witnessing steady growth driven by the high prevalence of autoimmune and chronic inflammatory diseases such as rheumatoid arthritis, psoriasis, Crohn’s disease, and ulcerative colitis, along with strong biologics adoption across major European healthcare systems.

The growing shift toward biologic therapies, increasing patient access through national reimbursement programs, and the expanding penetration of biosimilars are key factors supporting market expansion. In addition, rising clinical preference for targeted TNF-alpha inhibitors such as adalimumab, combined with improved healthcare infrastructure and long-term treatment protocols, is further strengthening demand across hospitals, specialty clinics, and retail pharmacy channels.

Key Market Trends & Insights

- Germany dominated the global adalimumab market with the largest revenue share of 26.74% in 2025, supported by a high burden of autoimmune diseases, strong biologics adoption, and well-established reimbursement frameworks across advanced healthcare systems.

- The Rheumatoid Arthritis segment led the market with a 38.6% share in 2025, driven by its high prevalence across aging populations and long-term dependence on TNF-alpha inhibitor therapy.

- Poland is expected to be the fastest-growing country at a CAGR of 8.1% from 2026 to 2033, fueled by improving biologics access, rising diagnosis rates of chronic inflammatory diseases, and expanding healthcare infrastructure.

- Hidradenitis Suppurativa are the fastest-growing indication type, projected to register a CAGR of 9.2%, reflecting the surge in awareness and improved diagnosis across dermatology practices in Europe.

- The Humira segment dominated the drug type category with a 46.8% revenue share in 2025, led by its long-established presence as the reference biologic in Europe.

- Adult accounted for 88.5% of the market, preferred by the higher prevalence of autoimmune diseases in adult populations.

- The Biosimilars segment is the fastest-growing type category, with a CAGR of 10.1%, driven by patent expirations and aggressive cost-containment strategies across European healthcare systems.

Market Size & Forecast

- Global Market Value (2025): USD 6.35 Billion

- Expected Market Value (2033): USD 21.10 Billion

- Forecast CAGR (2026–2033): 16.2%

- Leading Country in 2025: Germany

- Fastest Growing Country: Poland

Report Scope and Europe Adalimumab Market Segmentation

|

Attributes |

Europe Adalimumab Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

· AbbVie Inc. (U.S.) · Amgen Inc. (U.S.) · Pfizer Inc. (U.S.) · Boehringer Ingelheim International GmbH (Germany) · Sandoz Group AG (Switzerland) · Viatris Inc. (U.S.) · Fresenius Kabi AG (Germany) · Teva Pharmaceutical Industries Ltd. (Israel) · Celltrion Inc. (South Korea) · Samsung Bioepis Co., Ltd. (South Korea) · Biogen Inc. (U.S.) · Organon & Co. (U.S.) · Biocon Biologics Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Lupin Limited (India) · STADA Arzneimittel AG (Germany) · Amneal Pharmaceuticals, Inc. (U.S.) · Accord Healthcare Limited (U.K.) · Alvotech (Iceland) · Roche Holding AG (Switzerland) |

|

Market Opportunities |

· Expanding biosimilar penetration in Europe · Rising adoption of home-based self-injection therapies · Increasing use of adalimumab in newer autoimmune indications such as hidradenitis suppurativa and pediatric inflammatory diseases |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Adalimumab Market Trends

Trend: Expansion of Biosimilar Competition Across Europe

Biosimilar adalimumab products are rapidly expanding across Europe, driven by patent expirations of the original molecule and strong pricing pressure from healthcare payers seeking to reduce long-term biologics expenditure. This shift is reshaping prescribing behavior across hospitals and specialty clinics, with physicians increasingly favoring biosimilars due to comparable clinical efficacy and improved affordability. National health systems are also accelerating substitution policies and centralized procurement tenders to improve cost efficiency and widen patient access. For instance, in 2023, countries such as Germany implemented regional tendering systems, while the United Kingdom’s NHS expanded biosimilar switching programs, significantly increasing biosimilar uptake across rheumatology and gastroenterology treatments.

Europe Adalimumab Market Dynamics

Key Market Driver: Rising Prevalence of Autoimmune Disorders in Europe

The steady increase in autoimmune and chronic inflammatory diseases across Europe is a major factor driving demand for adalimumab therapies. Conditions such as rheumatoid arthritis, Crohn’s disease, psoriasis, and ulcerative colitis are becoming more frequently diagnosed due to improved clinical awareness, early screening initiatives, and advanced diagnostic capabilities. In addition, Europe’s aging population is more susceptible to immune-mediated disorders, leading to higher long-term treatment dependency and sustained biologic usage. For instance, in 2024, countries such as France, Italy, and Spain reported rising biologic therapy initiation rates under national insurance programs, particularly in tertiary care hospitals specializing in immunology and gastroenterology.

Key Restraint/Challenge: High Cost Pressure and Biosimilar Price Erosion

While demand for adalimumab remains strong, the market faces significant pressure from escalating cost-containment measures and rapid biosimilar penetration. Originator biologics face shrinking market share as payers enforce strict reimbursement frameworks, tender-based purchasing, and mandatory biosimilar substitution policies to reduce healthcare expenditure. This has led to intense price competition among manufacturers, impacting revenue growth for branded products. For instance, in 2023, countries such as Spain, the Netherlands, and Belgium introduced aggressive national procurement tenders that prioritized low-cost biosimilars, resulting in a notable decline in originator adalimumab prescriptions across public healthcare systems.

Key Market Opportunity: Expansion into New Autoimmune Indications and Home Care Use

The market presents significant growth opportunities through expanding clinical applications and the shift toward decentralized patient care. Ongoing clinical studies are evaluating adalimumab in additional autoimmune and inflammatory indications, broadening its therapeutic scope beyond traditional uses. At the same time, healthcare systems are increasingly promoting home-based self-administration using prefilled pens and auto-injectors, supported by telehealth monitoring and digital adherence tools. For instance, in 2024, countries such as Sweden, Denmark, and the Netherlands expanded reimbursement coverage for home-administered biologic therapies, enabling patients to manage chronic conditions outside hospital settings while improving treatment adherence and reducing healthcare system burden.

Europe Adalimumab Market Scope

The Europe adalimumab market is segmented on the basis of indication, type, dosage strength, drug type, population type, end user, and distribution channel

- By Indication

On the basis of indication, the Europe adalimumab market is segmented into rheumatoid arthritis, juvenile idiopathic arthritis, psoriatic arthritis, ankylosing spondylitis, Crohn’s disease, hidradenitis suppurativa, ulcerative colitis, chronic plaque psoriasis, non-infectious intermediate uveitis, and others. The Rheumatoid Arthritis segment dominated the market with a 38.6% share in 2025, driven by its high prevalence across aging populations and long-term dependence on TNF-alpha inhibitor therapy. It remains one of the most commonly treated autoimmune conditions using adalimumab across Europe. Strong reimbursement coverage ensures continuous patient access in major countries such as Germany, France, and the UK. Hospitals and specialty clinics widely rely on it for chronic disease management. Early diagnosis initiatives are further increasing treatment initiation rates. Long disease duration ensures sustained biologic consumption over time.

The Hidradenitis Suppurativa segment is expected to be the fastest-growing with a 9.2% CAGR from 2026 to 2033, driven by rising awareness and improved diagnosis across dermatology practices in Europe. This condition has historically been underdiagnosed, but improved clinical recognition is increasing patient identification rates. Adalimumab is increasingly recommended as a key biologic therapy for moderate to severe cases. Expanding dermatology treatment guidelines are supporting wider adoption. Increasing biosimilar availability is improving affordability for patients. Growing specialist consultations and better disease screening programs are accelerating market growth.

- By Type

On the basis of type, the market is segmented into biologics and biosimilars. The Biologics segment dominated the market with a 62.4% share in 2025, driven by strong historical adoption of originator adalimumab (Humira) across Europe. It benefits from long-established physician trust and extensive clinical evidence supporting efficacy and safety. Hospitals continue prescribing biologics for stable long-term patients. Reimbursement systems in Western Europe still support originator use in selected clinical cases. Despite biosimilar entry, it maintains strong presence in chronic treatment regimens. However, its share is gradually declining due to increasing biosimilar penetration.

The Biosimilars segment is the fastest-growing with a 10.1% CAGR from 2026 to 2033, driven by patent expirations and aggressive cost-containment strategies across European healthcare systems. Governments and payers are actively promoting biosimilar substitution through tender-based procurement. Hospitals are increasingly shifting to biosimilars due to lower treatment costs and budget optimization. Clinical studies confirming equivalence are improving physician confidence in switching patients. Countries such as Germany, the UK, and the Netherlands are leading adoption. Rising affordability is significantly expanding patient access across Europe.

- By Dosage Strength

On the basis of dosage strength, the market is segmented into 20MG/0.4ML, 40MG/0.8ML, and others. The 40MG/0.8ML segment dominated the market with a 54.3% share in 2025, as it is the most widely used maintenance dose for adult patients with autoimmune diseases. It is commonly prescribed for rheumatoid arthritis, Crohn’s disease, and psoriasis across Europe. Strong clinical guidelines support its standardized use in long-term therapy. Hospitals and specialty clinics prefer this dosage due to predictable treatment outcomes. Availability across both originator and biosimilar products strengthens its adoption. Its consistent dosing schedule improves patient adherence.

The Other dosage strengths segment is the fastest-growing with an 8.4% CAGR from 2026 to 2033, driven by increasing demand for personalized and flexible dosing regimens. Pediatric patients require weight-based dosing, increasing usage of alternative strengths. Rising treatment of juvenile idiopathic arthritis is supporting demand for flexible formulations. Manufacturers are introducing additional dosage options to improve patient convenience. Home-based biologic administration is further increasing need for varied strengths. Shift toward individualized treatment approaches is accelerating growth.

- By Drug Type

On the basis of drug type, the market includes Humira, Amgevita, Imraldi, Hyrimoz, Yuflyma, Hulio, and Idacio. The Humira segment dominated the market with a 46.8% share in 2025, due to its long-established presence as the reference biologic in Europe. It has strong physician familiarity and extensive clinical evidence across multiple indications. Hospitals continue prescribing it for long-term stable patients. Its strong brand recognition supports continued use despite biosimilar competition. However, its market share is gradually declining due to increasing biosimilar penetration. Reimbursement systems still partially support its usage in specific cases.

The Yuflyma segment is the fastest-growing with an 11.2% CAGR from 2026 to 2033, driven by rapid biosimilar adoption across European healthcare systems. It is increasingly included in national procurement tenders focused on cost reduction. Clinical equivalence to Humira supports fast switching in hospitals. Expanding distribution networks are improving availability across regions. Healthcare systems focused on budget optimization are driving uptake. Physician acceptance of newer biosimilars is increasing steadily.

- By Population Type

On the basis of population type, the market is segmented into children and adults. The Adult segment dominated the market with an 88.5% share in 2025, driven by the higher prevalence of autoimmune diseases in adult populations. Conditions such as rheumatoid arthritis and Crohn’s disease primarily affect adults and require long-term biologic therapy. Strong reimbursement coverage ensures continuous access to treatment. Aging populations across Europe further increase disease burden. Hospitals manage most adult cases under structured treatment pathways. Clinical research is also largely focused on adult populations.

The Children segment is the fastest-growing with a 9.0% CAGR from 2026 to 2033, driven by rising cases of juvenile idiopathic arthritis and pediatric inflammatory bowel diseases. Early screening programs are improving diagnosis rates in children. Pediatric approvals for adalimumab are expanding treatment options. Physicians are increasingly adopting early biologic intervention to prevent disease progression. Safety monitoring systems are supporting pediatric use. Rising awareness among parents and clinicians is further accelerating adoption.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, home healthcare, and others. The Hospitals segment dominated the market with a 57.9% share in 2025, due to centralized administration of biologics under specialist supervision. Hospitals manage complex autoimmune cases requiring multidisciplinary care. Strong infrastructure supports injectable biologic delivery. Reimbursement frameworks favor hospital-based initiation of therapy. High patient inflow for chronic diseases sustains dominance. Institutional treatment protocols further reinforce hospital dependency.

The Home Healthcare segment is the fastest-growing with a 10.3% CAGR from 2026 to 2033, driven by increasing adoption of self-injection therapies using auto-injector devices. Patients prefer home-based treatment due to convenience and reduced hospital visits. Telemedicine and remote monitoring systems ensure safe administration. Healthcare systems are encouraging decentralized chronic care models. Biosimilar affordability is supporting wider home adoption. Rising patient preference for self-management is accelerating growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The Hospital Pharmacies segment dominated the market with a 61.2% share in 2025, driven by strong integration with hospital prescribing and biologic administration systems. Most adalimumab therapies are initiated in hospital settings under specialist supervision. Centralized procurement and tender systems strengthen hospital pharmacy dominance. Regulatory oversight ensures safe and controlled distribution of biologics. Specialty care coordination supports consistent usage across hospitals. Large-volume purchasing agreements reinforce market leadership.

The Online Pharmacies segment is the fastest-growing with a 12.5% CAGR from 2026 to 2033, driven by rapid digital transformation of healthcare services across Europe. E-prescription systems are improving accessibility to biologic therapies. Home delivery services enhance patient convenience for chronic disease management. Telehealth integration supports remote prescribing and monitoring. Cost transparency encourages greater patient adoption of online channels. Increasing shift toward at-home care is accelerating growth significantly

Europe Adalimumab Market Regional Analysis

Germany dominated the global adalimumab market with the largest revenue share of 26.74% in 2025, supported by a high burden of autoimmune diseases, strong biologics adoption, and well-established reimbursement frameworks across advanced healthcare systems. The country benefits from advanced hospital infrastructure, early diagnosis of chronic inflammatory disorders, and widespread access to TNF-alpha inhibitor therapies across specialty clinics. Germany also leads in biosimilar adoption due to aggressive tendering systems, cost-containment policies, and strong government support for affordable biologic substitution. Increasing use of adalimumab across rheumatoid arthritis, psoriasis, and Crohn’s disease, along with strong physician familiarity and established treatment guidelines, further reinforces its leadership position in the European market.

The Germany Adalimumab Market Insight

The Germany adalimumab market is witnessing strong growth due to high prevalence of autoimmune diseases, advanced healthcare infrastructure, and widespread biologics adoption. The country benefits from a well-structured statutory health insurance system that ensures broad patient access to adalimumab therapies across hospitals and specialty clinics. Germany also leads Europe in biosimilar penetration, driven by aggressive tendering systems and strong cost-containment policies. Increasing use in rheumatoid arthritis, Crohn’s disease, and psoriasis, along with strong physician familiarity and early diagnosis rates, is further supporting market expansion across the country.

U.K. Adalimumab Market Insight

The U.K. adalimumab market is growing steadily due to strong NHS reimbursement support, rising autoimmune disease burden, and high biosimilar adoption rates. The country is one of the earliest adopters of adalimumab biosimilars, significantly improving patient access and reducing treatment costs. Hospitals and specialty clinics widely prescribe adalimumab for chronic inflammatory diseases such as rheumatoid arthritis and Crohn’s disease. Centralized procurement systems and strong clinical guidelines are further optimizing biologic utilization. Increasing use of self-injectable therapies and homecare treatment models is also strengthening market penetration.

France Adalimumab Market Insight

The France adalimumab market is expanding due to strong government healthcare coverage, increasing prevalence of autoimmune disorders, and growing adoption of biologics in clinical practice. The country’s universal healthcare system ensures high patient access to both originator and biosimilar adalimumab. Hospitals play a key role in biologic administration for rheumatoid arthritis, psoriasis, and inflammatory bowel diseases. Biosimilar adoption is increasing due to national cost-containment policies and procurement initiatives. Rising awareness among physicians and patients is further driving early diagnosis and treatment initiation.

Poland Adalimumab Market Insight

The Poland adalimumab market is witnessing strong growth due to rising prevalence of autoimmune diseases, improving healthcare infrastructure, and increasing access to biologic therapies. The country is benefiting from expanding diagnosis rates for conditions such as rheumatoid arthritis, psoriasis, and Crohn’s disease, supported by growing awareness among physicians and patients. Biosimilar adoption is accelerating rapidly due to cost-sensitive healthcare policies and government-driven reimbursement optimization programs. Hospitals and specialty clinics are the primary centers for biologic administration, with increasing reliance on tender-based procurement systems. In addition, continuous expansion of public healthcare funding and improved availability of adalimumab biosimilars are significantly enhancing treatment accessibility across Poland.

Europe Adalimumab Market Share

The Europe adalimumab industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Sandoz Group AG (Switzerland)

- Viatris Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Celltrion Inc. (South Korea)

- Samsung Bioepis Co., Ltd. (South Korea)

- Biogen Inc. (U.S.)

- Organon & Co. (U.S.)

- Biocon Biologics Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Lupin Limited (India)

- STADA Arzneimittel AG (Germany)

- Amneal Pharmaceuticals, Inc. (U.S.)

- Accord Healthcare Limited (U.K.)

- Alvotech (Iceland)

- Roche Holding AG (Switzerland)

Latest Developments in Europe Adalimumab Market

- In May 2025, European healthcare systems further reinforced biosimilar-first policies for adalimumab through updated procurement frameworks and reimbursement guidelines. Countries such as Germany and the Netherlands intensified tender-based purchasing, prioritizing cost-effective biosimilars over originator biologics. This shift strengthened healthcare budget optimization while maintaining equivalent treatment outcomes for autoimmune diseases

- In March 2024, Sandoz strengthened its European biosimilar portfolio with expanded commercialization of Hyrimoz (adalimumab biosimilar) across multiple EU countries. The company focused on increasing hospital tender participation and improving availability in cost-sensitive healthcare systems. This expansion enhanced competition in the adalimumab market and supported broader patient access to biologic therapies

- In January 2023, AbbVie’s key European patent protection for Humira (adalimumab) expired, enabling widespread entry of biosimilars across major European markets such as Germany, France, and the U.K. This marked a major shift in the anti-TNF biologics landscape, triggering rapid uptake of biosimilars including Amgevita, Hyrimoz, and Imraldi. The event significantly increased price competition and expanded patient access through national tender systems and hospital procurement programs

- In June 2022, NHS England expanded its structured biosimilar switching program for adalimumab, encouraging transition from Humira to lower-cost biosimilars. The initiative targeted major autoimmune indications such as rheumatoid arthritis and Crohn’s disease to reduce pharmaceutical spending while maintaining clinical outcomes. This significantly increased biosimilar penetration across hospitals and specialty care centers in the U.K.

- In July 2021, the European Commission granted marketing authorization for Celltrion’s Yuflyma (adalimumab biosimilar), expanding treatment options across the European Union. This approval strengthened biosimilar competition in autoimmune disease therapy and improved affordability across multiple healthcare systems. Yuflyma’s launch supported wider adoption in countries such as Germany and Nordic regions, enhancing access to TNF-alpha inhibitor therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.