Mayo Foundation for Medical Education and Research

Quest Diagnostics Incorporated

Eurofins Scientific

UNILABS

SYNLAB International GmbH

Europe Clinical Laboratory Services Market, By Specialty (Clinical Chemistry Testing, Hematology Testing, Microbiology Testing, Immunology Testing, Drugs Of Abuse Testing, Anatomic Pathology Services, Cytology Testing, Genetic Testing, and Other Esoteric Testing), Technology (Chemiluminescence Immunoassay, Enzyme-Linked Immunosorbent Assay, Mass Spectrometry, Real-Time PCR, DNA Sequencing, Flow Cytometry, and Other Technologies), Provider (Independent & Reference Laboratories, Hospital-Based Laboratories, Clinical Based Laboratories, and Nursing and Physician Office-Based Laboratories), Application (Drug Discovery Related Services and Development Related Services, Bioanalytical & Lab Chemistry Services, Toxicology Testing Services, Cell & Gene Therapy Related Services, Preclinical & Clinical Trial Related Services, and Other Clinical Laboratory Services) - Industry Trends And Forecast to 2030.

Europe Clinical Laboratory Services Market Analysis and Size

The market is expected to gain market. Growing application of high-throughput assays and advancement in clinical diagnostic methods act as a driver for the market growth.

Clinical labs provide testing products to public and private health service agencies, including health centers, clinics, medical centers, and nursing homes. Laboratory research areas protected by accreditation include medicinal chemistry, clinical microbiology, hematology, anatomy, clinical physics, psychology, nuclear medicine, and clinical neurophysiology.

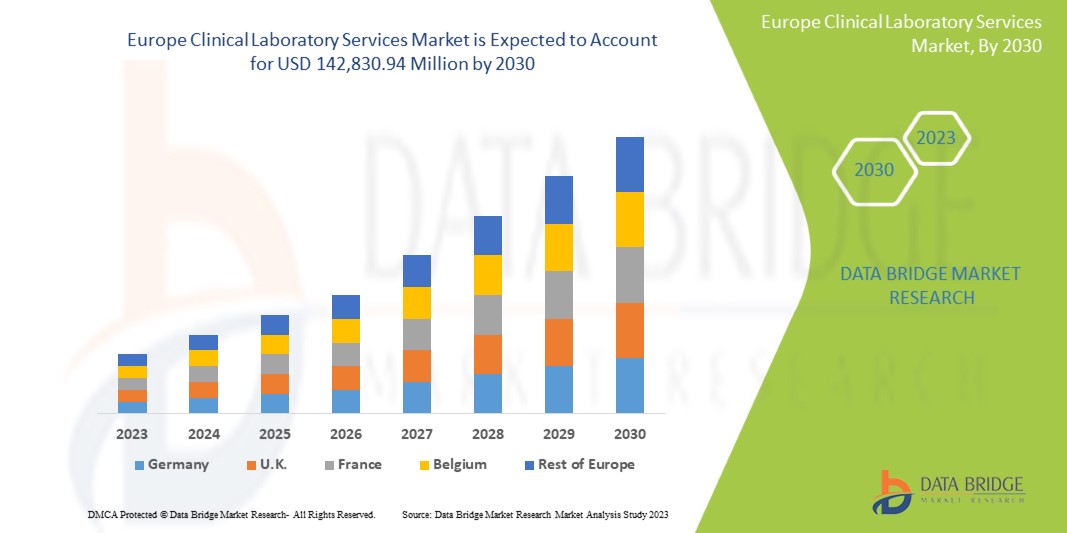

Data Bridge Market Research analyses that the Europe clinical laboratory services market is expected to reach the value of USD 142,830.94 million by 2030, at a CAGR of 6.6% during the forecast period.

Report Metric

Details

Forecast Period

2023 to 2030

Base Year

2022

Historic Year

2021 (Customizable to 2015-2020)

Quantitative Units

Revenue in USD Million

Segments Covered

Specialty (Clinical Chemistry Testing, Hematology Testing, Microbiology Testing, Immunology Testing, Drugs Of Abuse Testing, Anatomic Pathology Services, Cytology Testing, Genetic Testing, and Other Esoteric Testing), Technology (Chemiluminescence Immunoassay, Enzyme-Linked Immunosorbent Assay, Mass Spectrometry, Real-Time PCR, DNA Sequencing, Flow Cytometry, and Other Technologies), Provider (Independent & Reference Laboratories, Hospital-Based Laboratories, Clinical Based Laboratories, and Nursing and Physician Office-Based Laboratories), Application (Drug Discovery Related Services and Development Related Services, Bioanalytical & Lab Chemistry Services, Toxicology Testing Services, Cell & Gene Therapy Related Services, Preclinical & Clinical Trial Related Services, and Other Clinical Laboratory Services)

Countries Covered

Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland and Rest Of Europe

Market Players Covered

Mayo Foundation for Medical Education and Research, Quest Diagnostics Incorporated, Eurofins Scientific, UNILABS, SYNLAB International GmbH, H.U. Groups Holdings, Inc., Sonic Healthcare Limited, ACM Global Laboratories, Amedes Medical Services GmbH, Abbott, Charles River Laboratories, Cerba Healthcare, Q2 Solutions (A subsidiary of IQVIA Inc) and among others

Market Definition

Clinical laboratories are an important part of the healthcare field. Most diagnostic tests, starting from the blood test to the genetic analysis, are conducted in these clinical laboratories to detect different diseases. Clinical laboratories offer data and resources that optimize the required distribution in the healthcare system, such as diagnostics and test results. This maintains and provides reliable and correct test results that enable doctors to make appropriate clinical and diagnostic decisions across various levels of health care services. This allows clinicians to adapt, begin, and stop treatment, which would be hindered in the absence of medical laboratory facilities. Clinical laboratory services include drug discovery, drug development, bioanalytical & lab chemistry, toxicology testing, cell & gene therapy, and preclinical & clinical trial-related services. Independent and reference laboratories, hospital-based laboratories, nursing, and physician office-based laboratories are some of the major providers of clinical laboratory services.

Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints, and challenges. All of this is discussed in detail below:

Driver

Rise in the Cases of Infectious Diseases

In recent times, there has been an increasing incidence of infectious diseases, such as viral outbreaks and antibiotic-resistant pathogens that has raised the demand for diagnostic testing and clinical laboratory services. Infectious diseases affected by organisms such as viruses, parasites, fungi, and bacteria are directly or indirectly passed from one person to another. The clinical laboratories are investing substantially in advanced diagnostic technologies, including molecular diagnostics and serology testing, to effectively identify and manage these diseases. Increasing infectious diseases impact increasing the demand for clinical laboratories as laboratory diagnosis of infectious diseases of the patients. The clinical laboratory provides different types of services for the diagnosis and treatment of patients due to infectious diseases, including blood count, immunology and allergy testing, and urinalysis among others.

Opportunities

Rising Popularity of Digital Pathology Platforms

Digital pathology platforms are computer workstations used to view digital whole slide images acquired from glass microscope high-resolution slide scanning. Digital pathology platforms use algorithms for analysis and diagnostic reporting to ensure reproducibility, greater accuracy, and standardization of studies. Applications of digital pathology platforms are increasing in various clinical laboratories to implement full-scale operations in the laboratories successfully. In addition, the adoption of digital pathology platforms has increased as whole slide imaging has shown various improvements in scanner capacities, scan times, image resolution, image management software, laboratory information systems integration, and simple image viewing and evaluation.

Digital pathology platforms have displayed their utility in team communication, case management, workflow acceleration and facilitation in image analytics, slide imaging, tumor boards, and remote consultations, which is creating a more collaborative, efficient, and rewarding environment for researchers and clinicians, which in increasing adoption of digital pathology platforms around the world.

The adoption of digital pathology platforms is increasing in developed and developing countries due to increasing functional ability in various departments in the clinical laboratory, including training, teaching, team communication, research activities, and primary diagnostic reporting. Digital pathology platforms have shown their efficacy in clinical laboratories with many benefits in clinical laboratory operations.

Growth in Awareness Among Population for Preventive Health Check-Ups

Preventive health check-ups are preventive actions performed for the initial detection of disease and to safeguard against likely exposure to any disease in the future. The check-up is comprised of the identification of disease and examinations of risk factors to limit loss at an early stage. Preventive health check-ups are performed with the help of various lab tests, including blood chemistry, hemoglobin, urinalysis, screening for prostate cancer, screening for ovarian cancer, ECG, lipid panel, and others.

Preventive health check-ups are increasing worldwide as various studies and research have proven their effectiveness in disease prevention and economics. Furthermore, the demand for preventive health check-ups has increased as preventive health check-ups are insured by health insurance companies in various counties, and the current COVID-19 situation has added up as a necessity for the safety of individuals. When a communicable disease outbreak begins, the ideal response is for public health officials to begin testing for it early. That leads to quick identification of cases, quick treatment for those people, and immediate isolation to prevent spread. Early testing also helps to identify anyone who came into contact with infected people so they too can be quickly treated.

Restraints/Challenges

Lack of Skilled and Certified Professionals

The requirement for skilled and certified professionals is a big restraint for clinical laboratories. Clinical laboratory services have increased due to the high growth in the number of people aged 65 or older who need a routine diagnostic test for their health, but the number of skilled professionals present in the laboratory center is expected to restrain the market growth. The method and laboratory procedure have advantages, but there are certain gaps in standardization, equalization, and knowledge. Technicians are facing technical training gaps related to problems in adopting advanced methods safely to perform procedures efficiently. There is a need for highly skilled professionals in the clinical laboratory for method development, validation, operation, and troubleshooting activities.

Inaccurate Test Outcomes Undermining Precision and Reliability

Inaccuracies in diagnostic test outcomes have negative consequences for patient safety, potentially leading to misdiagnoses or delayed diagnoses that harm patients' health. Many Inaccurate results and diagnostic test errors are linked to laboratory practices. Laboratory practice could be divided into three segments which are pre-analytical, analytical, and post-analytical.

Analytical Errors: During the establishment and verification of test methods as per the performance specifications to test precision, accuracy, specificity, sensitivity, and linearity are the areas where errors are high in clinical laboratory testing.

Pre-Analytical Errors: The pre-analytical error phase is the process where the maximum laboratory errors occur. Pre-analytical errors can arise during patient assessment, patient identification, request completion, test order entry, specimen transport, specimen collection, and specimen receipt in the laboratory.

Post-Analytical Errors: The post-analytical phase is the phase of diagnostic and therapeutic decisions. Post-analytical errors can arise due to inappropriate use of laboratory test outcomes, the transmission of correct outcomes, and critical outcomes reporting are areas of potential error in the post-analytical phase of the total laboratory testing process.

Recent Developments

In August 2023, Abbott received FDA clearance for its Alinity h-series hematology system, expanding its diagnostic Service lineup for complete blood counts (CBC) testing. This system is crucial in routine checkups, aiding in the screening of various disorders such as infections, anemia, immune system diseases, and blood cancers. The Alinity h-series comprises Alinity hq, an automated hematology analyzer, and Alinity hs, an integrated slide maker and stainer. Notably, Alinity HQ employs MAPSSTM technology for advanced cell identification using light scattering.

In November 2022, Microba Life Sciences announced a strategic partnership with Sonic Healthcare Limited, a global leader in medical diagnostics. Sonic is set to acquire a 19.99% stake in Microba, with an option for an additional 5% pending shareholder approval.

Market Scope

Europe clinical laboratory services market is categorized into four notable segments on the basis of specialty, technology, provider, and application. The growth amongst these segments will help you analyze major growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Specialty

Clinical Chemistry Testing

Hematology Testing

Microbiology Testing

Immunology Testing

Drugs of Abuse Testing

Cytology Testing

Genetic Testing

Anatomic Pathology Services

Other Estoric Testing

On the basis of specialty, the market is segmented into clinical chemistry testing, hematology testing, microbiology testing, immunology testing, drugs of abuse testing, cytology testing, genetic testing, anatomic pathology services and other esoteric testing.

On the basis of technology, the market is segmented into enzyme-linked immunosorbent assay, real-time PCR, chemiluminescence immunoassay, mass spectrometry, flow cytometry, DNA sequencing and other technologies.

Provider

Hospital-Based Laboratories

Independent & Reference Laboratories

Nursing and Physician Office-Based Laboratories

Clinic Based Laboratories

On the basis of provider, the market is segmented into hospital-based laboratories, independent & reference laboratories, nursing and physician office-based laboratories, and clinic-based laboratories.

Application

Bioanalytical & Lab Chemistry Services

Drug Discovery and Development Related Services

Toxicology Testing Services

Cell & Gene Therapy Related Services

Preclinical & Clinical Trial Related Services

Other Clinical Laboratory Services

On the basis of application, the market is segmented into drug discovery and development related services, bioanalytical & lab chemistry services, toxicology testing services, cell & gene therapy related services, preclinical & clinical trial related services, and other clinical laboratory services.

Regional Analysis/Insights

The Europe clinical laboratory services market is categorized into four notable segments on the basis of specialty, technology, provider, and application.

The countries covered in the Europe clinical laboratory services market report are Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland and Rest Of Europe.

Germany is expected to dominate the market due to its advanced healthcare infrastructure and extensive network of high-quality clinical laboratories.

The country section of the report also provides individual market impacting factors and changes in market regulation that impact the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of regional brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Competitive Landscape and Share Analysis

The Europe clinical laboratory services market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, regional presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus on the Europe clinical laboratory services market.

Some of the major players operating in the Europe clinical laboratory services market are Mayo Foundation for Medical Education and Research, Quest Diagnostics Incorporated, Eurofins Scientific, UNILABS, SYNLAB International GmbH, H.U. Groups Holdings, Inc., Sonic Healthcare Limited, ACM Global Laboratories, Amedes Medical Services GmbH, Abbott, Charles River Laboratories, Cerba Healthcare, Q2 Solutions (A subsidiary of IQVIA Inc) and among others.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

Interactive Data Analysis Dashboard

Company Analysis Dashboard for high growth potential opportunities

Research Analyst Access for customization & queries

Competitor Analysis with Interactive dashboard

Latest News, Updates & Trend analysis

Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE CLINICAL LABORATORY SERVICES MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 MARKET APPLICATION COVERAGE GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTLE ANALYSIS

4.1.1 POLITICAL FACTORS

4.1.2 ECONOMIC FACTORS

4.1.3 SOCIAL FACTORS

4.1.4 TECHNOLOGICAL FACTORS

4.1.5 LEGAL FACTORS

4.1.6 ENVIRONMENTAL FACTORS

4.2 PORTER’S FIVE FORCES

4.2.1 THREAT OF NEW ENTRANTS

4.2.2 THREAT OF SUBSTITUTES

4.2.3 CUSTOMER BARGAINING POWER

4.2.4 SUPPLIER BARGAINING POWER

4.2.5 INTERNAL COMPETITION (RIVALRY)

5 REGULATORY FRAMEWORK

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 RISE IN THE CASES OF INFECTIOUS DISEASES

6.1.2 TECHNOLOGICAL ADVANCEMENTS IN THE CLINICAL DIAGNOSTIC METHODS

6.1.3 DEVELOPMENT IN DATABASE MANAGEMENT TOOLS AND WIDE ACCEPTANCE OF POINT-OF-CARE (POC) TESTING SOLUTIONS

6.1.4 RISE IN DEMAND FOR EARLY AND ACCURATE DISEASE DIAGNOSIS

6.2 RESTRAINTS

6.2.1 LACK OF SKILLED AND CERTIFIED PROFESSIONALS

6.2.2 STRICT REGULATORY POLICIES

6.3 OPPORTUNITIES

6.3.1 RISING POPULARITY OF DIGITAL PATHOLOGY PLATFORMS

6.3.2 GROWTH IN AWARENESS AMONG POPULATION FOR PREVENTIVE HEALTH CHECK-UPS

6.4 CHALLENGE

6.4.1 INACCURATE TEST OUTCOMES UNDERMINING PRECISION AND RELIABILITY

7 EUROPE

8 EUROPE CLINICAL LABORATORY SERVICES MARKET: COMPANY LANDSCAPE

8.1 COMPANY SHARE ANALYSIS: EUROPE

9 SWOT ANALYSIS

10 COMPANY PROFILES

10.1 ABBOTT

10.1.1 COMPANY SNAPSHOT

10.1.2 REVENUE ANALYSIS

10.1.3 SERVICE PORTFOLIO

10.1.4 RECENT DEVELOPMENTS

10.2 SONIC HEALTHCARE LIMITED

10.2.1 COMPANY SNAPSHOT

10.2.2 REVENUE ANALYSIS

10.2.3 SERVICE PORTFOLIO

10.2.4 RECENT DEVELOPMENT

10.3 SYNLAB INTERNATIONAL GMBH

10.3.1 COMPANY SNAPSHOT

10.3.2 REVENUE ANALYSIS

10.3.3 SERVICE PORTFOLIO

10.3.4 RECENT DEVELOPMENTS

10.4 QUEST DIAGNOSTICS INCORPORATED

10.4.1 COMPANY SNAPSHOT

10.4.2 REVENUE ANALYSIS

10.4.3 SERVICE PORTFOLIO

10.4.4 RECENT DEVELOPMENT

10.5 SIEMENS HEALTHINEERS AG

10.5.1 COMPANY SNAPSHOT

10.5.2 REVENUE ANALYSIS

10.5.3 SERVICE PORTFOLIO

10.5.4 RECENT DEVELOPMENTS

10.6 ACM GLOBAL LABORATORIES

10.6.1 COMPANY SNAPSHOT

10.6.2 SERVICE PORTFOLIO

10.6.3 RECENT DEVELOPMENT

10.7 AMEDES MEDICAL SERVICES GMBH

10.7.1 COMPANY SNAPSHOT

10.7.2 SERVICE PORTFOLIO

10.7.3 RECENT DEVELOPMENT

10.8 CERBA HEALTHCARE

10.8.1 COMPANY SNAPSHOT

10.8.2 SERVICE PORTFOLIO

10.8.3 RECENT DEVELOPMENT

10.9 CHARLES RIVER LABORATORIES

10.9.1 COMPANY SNAPSHOT

10.9.2 REVENUE ANALYSIS

10.9.3 SERVICE PORTFOLIO

10.9.4 RECENT DEVELOPMENT

10.1 EUROFINS SCIENTIFIC

10.10.1 COMPANY SNAPSHOT

10.10.2 REVENUE ANALYSIS

10.10.3 SERVICE PORTFOLIO

10.10.4 RECENT DEVELOPMENT

10.11 EXACT SCIENCES CORPORATION

10.11.1 COMPANY SNAPSHOT

10.11.2 REVENUE ANALYSIS

10.11.3 SERVICE PORTFOLIO

10.11.4 RECENT DEVELOPMENT

10.12 H.U. GROUP HOLDINGS, INC.

10.12.1 COMPANY SNAPSHOT

10.12.2 REVENUE ANALYSIS

10.12.3 SERVICE PORTFOLIO

10.12.4 RECENT DEVELOPMENT

10.13 MAYO FOUNDATION FOR MEDICAL EDUCATION AND RESEARCH

10.13.1 COMPANY SNAPSHOT

10.13.2 SERVICE PORTFOLIO

10.13.3 RECENT DEVELOPMENT

10.15 Q2 SOLUTIONS (A SUBSIDIARY OF IQVIA INC)

10.15.1 COMPANY SNAPSHOT

10.15.2 SERVICE PORTFOLIO

10.15.3 RECENT DEVELOPMENTS

10.16 UNILABS

10.16.1 COMPANY SNAPSHOT

10.16.2 SERVICE PORTFOLIO

10.16.3 RECENT DEVELOPMENTS

11 QUESTIONNAIRE

12 RELATED REPORTS

List of Figure

FIGURE 1 EUROPE CLINICAL LABORATORY SERVICES MARKET: SEGMENTATION

FIGURE 2 EUROPE CLINICAL LABORATORY SERVICES MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE CLINICAL LABORATORY SERVICES MARKET: DROC ANALYSIS

FIGURE 4 EUROPE CLINICAL LABORATORY SERVICES MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE CLINICAL LABORATORY SERVICES MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE CLINICAL LABORATORY SERVICES MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE CLINICAL LABORATORY SERVICES MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE CLINICAL LABORATORY SERVICES MARKET APPLICATION COVERAGE GRID

FIGURE 9 EUROPE CLINICAL LABORATORY SERVICES MARKET: SEGMENTATION

FIGURE 10 RISING INFECTIOUS DISEASES WORLDWIDE AND RISING DEMAND FOR EARLY AND ACCURATE DISEASE DIAGNOSIS ARE EXPECTED TO DRIVE THE EUROPE CLINICAL LABORATORY SERVICES MARKET IN THE FORECAST PERIOD OF 2023 TO 2030

FIGURE 11 THE ROUTINE TESTING SERVICES SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE CLINICAL LABORATORY SERVICES MARKET IN 2023 & 2030

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE EUROPE CLINICAL LABORATORY SERVICES MARKET

FIGURE 13 EUROPE CLINICAL LABORATORY SERVICES MARKET: SNAPSHOT (2022)

FIGURE 14 EUROPE CLINICAL LABORATORY SERVICES MARKET: COMPANY SHARE 2022 (%)

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.

Claudio Rondena

Group Business Development & Strategic Marketing Director, C.O.C Farmaceutici SRL

"This morning we were involved in the first part, the data presentation of MKT analysis, selected abstract from your work. The board team was really impressed and very appreciated, as well."

David Manning - Thermo Fisher Scientific

Director, Global Strategic Accounts,

Dear Ricky, I want to thank you for the excellent market analysis (LIMS INSTALLED BASE DATA) that you and your team delivered, especially end of year on short notice.

Sachin and Shraddha captured the requirements, determined their path forward and executed quickly.

You, Sachin and Shraddha have been a pleasure to work with – very responsive, professional and thorough.

Your work is much appreciated.

Manager - Market Analytics,

Uriah D. Avila - Zeus Polymer Solutions

Thank you for all the assistance and the level of detail in the market report. We are very pleased with the results and the customization. We would like to continue to do business.

Business Development Manager,

(Pharmaceuticals Partner for Nasal Sprays) | Renaissance Lakewood LLC

DBMR was attentive and engaged while discussing the Global Nasal Spray Market. They understood what we were looking for and was able to provide some examples from the report as requested. DBMR Service team has been responsive as needed. Depending on what my colleagues were looking for, I will recommend your services and would be happy to stay connected in case we can utilize your research in the future.

Business Intelligence and Analytics,

Ipsen Biopharm Limited

We are impressed by the CENTRAL PRECOCIOUS PUBERTY (CPP) TREATMENT report - so a BIG thanks to you colleagues.

Competition Analyst,

Basler Web

I just wanted to share a quick note and let you know that you guys did a really good job. I’m glad I decided to work with you. I shall continue being associated with your company as long as we have market intelligence needs.

Marketing Director,

Buhler Group

It was indeed a good experience, would definitely recommend and come back for future prospects.

COO,

A global leader providing Drug Delivery Services

DBMR did an outstanding job on the Global Drug Delivery project, We were extremely impressed by the simple but comprehensive presentation of the study and the quality of work done. This report really helped us to access untapped opportunities across the globe.

Marketing Director,

Philips Healthcare

The study was customized to our targets and needs with well-defined milestones. We were impressed by the in-depth customization and inclusion of not only major but also minor players across the globe. The DBMR Market position grid helped us to analyze the market in different dimension which was very helpful for the team to get into the minute details.

Product manager,

Fujifilms

Thankful to the team for the amazing coordination, and helping me at the last moment with my presentation. It was indeed a comprehensive report that gave us revenue impacting solution enabling us to plan the right move.

Investor relations,

GE Healthcare

Thank you for the report, and addressing our needs in such short time. DBMR has outdone themselves in this project with such short timeframe.

Market Analyst,

Medincell

We found the results of this study compelling and will help our organization validate a market we are considering to enter. Thank you for a job well done.

Andrew - Senior Global Marketing Manager,

Medtronic (US)

I want to thank you for your help with this report – It’s been very helpful in our business planning and it well organized.

Amarildo - Manager, Global Strategic Alignment

MasterCard

We believe the work done by Data Bridge Team for our requirements in the North America Loyalty Management Market was fantastic and would love to continue working with your team moving forward.

Tor Hammer

Green Nexus LLc

Thank you for your quick response to this unfortunate circumstance. Please extend my thanks to your reach team. I will be contacting you in the future with further projects

I acknowledge the difficulty given by the very short warning for this report, and I think that its quality and your delivering time have been very satisfying.

Obviously, as a provider Data Bridge Market Research will be considered as a plus for future needs of Nippon Gases.

Yuki Kopyl (Asian Business Development Department)

UENO FOOD TECHNO INDUSTRY, LTD. (JAPAN)

Xylose report was very useful for our team. Thank you very much & hope to work with you again in the future