Europe Medical Instrument Disinfection Market

Market Size in USD Billion

USD

2.50 Billion

USD

4.02 Billion

2025

2033

USD

2.50 Billion

USD

4.02 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.50 Billion | |

| USD 4.02 Billion | |

| % | |

|

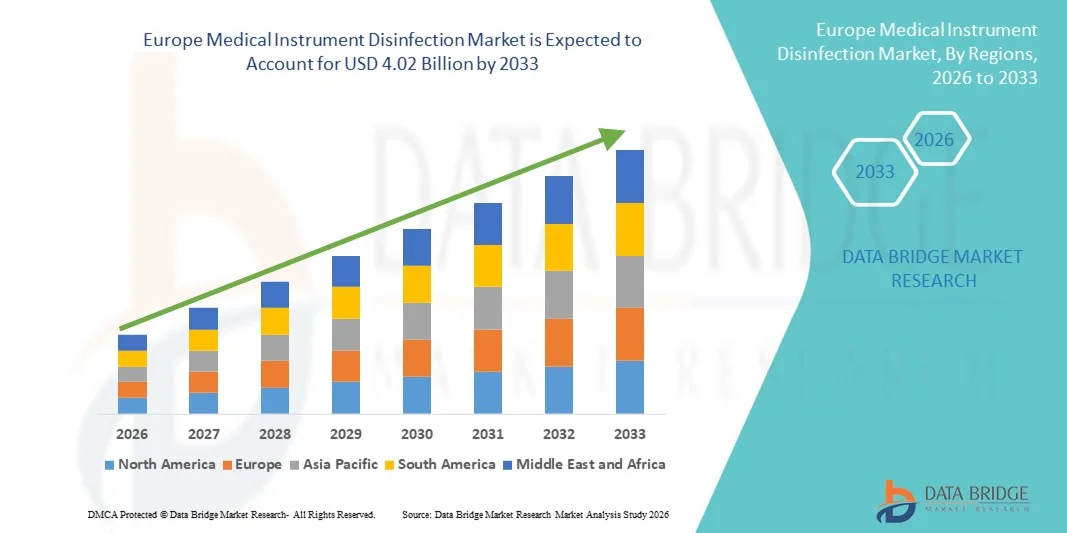

Europe Medical Instrument Disinfection Market Size

- The Europe medical instrument disinfection market size was valued at USD 2.50 billion in 2025 and is expected to reach USD 4.02 billion by 2033, at a CAGR of 6.13% during the forecast period

- The market growth is largely fueled by increasing demand for advanced sterilization and disinfection solutions in hospitals, clinics, and diagnostic centers, alongside stringent hygiene and infection control regulations across Europe

- Furthermore, rising awareness of hospital-acquired infections (HAIs) and cross-contamination risks is driving healthcare providers to adopt automated and efficient disinfection systems. These converging factors are accelerating the adoption of modern medical instrument disinfection solutions, thereby significantly boosting the industry's growth

Europe Medical Instrument Disinfection Market Analysis

- Medical instrument disinfection, covering advanced sterilization and high-level disinfection technologies for surgical instruments, endoscopes, and diagnostic tools, is increasingly critical in European healthcare facilities due to its role in preventing hospital-acquired infections (HAIs) and ensuring patient safety

- The escalating demand for medical instrument disinfection solutions is primarily fueled by stringent hygiene regulations, growing awareness of cross-contamination risks, and the adoption of automated and efficient disinfection systems in hospitals, clinics, and diagnostic centers

- Germany dominated the Europe medical instrument disinfection market with the largest revenue share of 45.2% in 2025, characterized by high healthcare standards, strict infection control protocols, and the presence of key medical device manufacturers, with hospitals and diagnostic centers widely adopting advanced disinfection solutions to meet compliance and patient safety requirements

- Poland is expected to be the fastest-growing country in the Europe medical instrument disinfection market during the forecast period due to increasing healthcare infrastructure investments, rising surgical procedures, and growing awareness of infection prevention measures

- Liquid segment dominated the Europe medical instrument disinfection market with a share of 41.9% in 2025, driven by its proven effectiveness, ease of use for a wide range of instruments, and widespread adoption across hospitals and diagnostic centers in Europe

Report Scope and Europe Medical Instrument Disinfection Market Segmentation

|

Attributes |

Europe Medical Instrument Disinfection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Medical Instrument Disinfection Market Trends

Automation and Integration with Hospital Workflows

- A significant and accelerating trend in the Europe medical instrument disinfection market is the increasing adoption of automated liquid and high-level disinfection systems integrated with hospital workflow management, improving efficiency and compliance with sterilization standards

- For instance, the Getinge Washer-Disinfector integrates seamlessly with hospital central sterilization departments, allowing staff to monitor instrument processing cycles digitally and reduce human errors

- Automation enables features such as real-time monitoring of disinfection cycles, tracking instrument usage, and generating compliance reports for audits, ensuring patient safety and regulatory adherence

- The integration of disinfection systems with hospital management software facilitates centralized control over sterilization processes, inventory management, and maintenance schedules, enhancing operational efficiency

- This trend toward intelligent, automated, and workflow-integrated disinfection systems is fundamentally changing expectations for infection prevention in hospitals, leading companies such as Steris to develop fully automated liquid-based disinfection solutions with data logging and remote monitoring capabilities

- The demand for automated and integrated medical instrument disinfection solutions is growing rapidly across hospitals, diagnostic centers, and outpatient clinics as healthcare providers increasingly prioritize patient safety, compliance, and operational efficiency

- Rising integration of AI-based analytics in disinfection equipment helps predict failure risks, optimize disinfection cycles, and improve resource utilization across large hospital networks

Europe Medical Instrument Disinfection Market Dynamics

Driver

Rising Need Due to Stringent Infection Control Regulations

- The increasing prevalence of hospital-acquired infections (HAIs) and the enforcement of strict infection control regulations across Europe is a significant driver for the heightened adoption of advanced medical instrument disinfection solutions

- For instance, in May 2024, Ecolab launched a hospital-grade liquid disinfection system designed to comply with EU MDR and local sterilization standards, highlighting the regulatory-driven adoption trend

- As healthcare facilities strive to meet stringent hygiene protocols, liquid and automated disinfection systems offer standardized, reliable sterilization and reduced risk of human error, making them a preferred solution over manual methods

- Furthermore, growing awareness among healthcare professionals regarding cross-contamination risks and patient safety is pushing hospitals and clinics to invest in high-efficiency disinfection systems

- The need for traceable compliance, real-time monitoring, and improved patient safety, combined with operational convenience, is significantly propelling the adoption of liquid-based and automated disinfection solutions in European healthcare facilities

- Government subsidies and incentives for hospitals investing in advanced sterilization equipment further encourage market growth, particularly in countries with strict healthcare regulations

- Increasing collaborations between disinfection solution providers and healthcare institutions enable tailored solutions for large hospital networks, accelerating adoption across multiple facilities

Restraint/Challenge

High Initial Investment and Regulatory Compliance Burden

- The relatively high upfront cost of advanced liquid and automated disinfection systems compared to conventional manual methods poses a significant challenge to broader adoption, particularly for smaller clinics and outpatient facilities

- For instance, reports from small hospitals in Italy indicate budget constraints limiting the purchase of fully automated washer-disinfectors despite their operational advantages

- Compliance with evolving EU MDR and national infection control regulations requires additional staff training, validation, and documentation, which can be time-consuming and resource-intensive

- While liquid disinfection systems are highly effective, perceived complexity in operation and maintenance may discourage adoption among healthcare providers accustomed to manual sterilization processes

- Overcoming these challenges through cost-effective solutions, staff training programs, and simplified regulatory compliance workflows will be vital for sustained growth of the medical instrument disinfection market across Europe

- Limited awareness among smaller healthcare facilities regarding the long-term cost benefits of automated disinfection solutions can slow adoption, despite clear efficiency and safety advantages

- Variability in national regulations across European countries creates challenges for solution standardization and multi-country implementation for large hospital networks, adding complexity to market expansion

Europe Medical Instrument Disinfection Market Scope

The market is segmented on the basis of type, environmental protection agency classification, product type, end-user, and distribution channel.

- By Type

On the basis of type, the Europe medical instrument disinfection market is segmented into wipes, liquid, and sprays. The liquid segment dominated the market with the largest revenue share of 41.9% in 2025, driven by its proven effectiveness in disinfecting a wide range of instruments, ease of handling, and widespread adoption across hospitals and diagnostic centers. Liquid disinfectants are preferred for surgical instruments, endoscopes, and reusable medical tools due to their ability to achieve high-level disinfection reliably. Hospitals and clinics benefit from standardized dosing and reduced contamination risk, ensuring compliance with strict hygiene protocols. The segment’s dominance is reinforced by regulatory approvals and the trust of healthcare professionals across Europe. Liquid disinfectants are also compatible with automated disinfection systems, further enhancing operational efficiency and safety.

The wipes segment is anticipated to witness the fastest growth rate of 22.5% from 2026 to 2033, fueled by the need for quick, convenient surface disinfection in hospitals, laboratories, and outpatient clinics. Wipes are increasingly adopted for point-of-care applications, offering portability and rapid action against pathogens, making them ideal for emergency rooms, diagnostic labs, and high-traffic areas in healthcare facilities. Their growing popularity is also attributed to rising awareness of cross-contamination risks, ease of use by non-specialist staff, and minimal training requirements. Wipes also complement other disinfection systems, providing a practical solution for immediate cleaning needs. Their lightweight packaging and single-use design reduce handling errors and maintain hygiene standards.

- By Environmental Protection Agency Classification

On the basis of EPA classification, the market is segmented into low-level, intermediate-level, and high-level disinfection. The high-level disinfection segment dominated the market in 2025, accounting for the largest revenue share due to its ability to completely inactivate bacteria, viruses, and spores on critical and semi-critical medical instruments. Hospitals and diagnostic centers prefer high-level disinfectants for surgical tools, endoscopes, and instruments used in invasive procedures to ensure patient safety. Its dominance is reinforced by regulatory mandates requiring high-level disinfection for critical instruments. High-level disinfection systems are often integrated with automated washers, reducing human error and increasing consistency. Healthcare providers rely on these systems to maintain compliance with EU MDR and national infection control standards. The segment’s widespread use in both public and private healthcare facilities supports its market leadership.

The intermediate-level segment is expected to witness the fastest growth rate of 20.8% from 2026 to 2033, driven by the increasing demand for routine surface and equipment disinfection in hospitals and laboratories. This segment offers cost-effective sterilization for non-critical instruments while maintaining safety standards, making it particularly attractive for outpatient centers, diagnostic labs, and medical device manufacturers. Its growth is fueled by heightened awareness of hospital-acquired infections, infection prevention measures, and the need for flexible disinfection solutions. Intermediate-level disinfectants are easier to handle, require less contact time, and reduce operational costs compared to high-level systems. Increasing adoption in developing European countries further accelerates this segment’s growth.

- By Product Type

On the basis of product type, the market is segmented into disinfectors and others. The disinfector segment dominated the market with the largest revenue share in 2025, driven by the adoption of automated washer-disinfectors and high-level liquid disinfection systems in hospitals and diagnostic centers. Disinfectors ensure standardized sterilization, reduce human error, and provide documentation for compliance audits, making them essential in modern healthcare workflows. The dominance of disinfectors is supported by technological innovations such as remote monitoring and IoT connectivity. Hospitals prefer automated disinfectors for processing critical instruments and reducing staff exposure to hazardous chemicals. Regulatory compliance, repeatable results, and data logging capabilities further reinforce the segment’s leadership.

The others segment, which includes manual sterilization systems and chemical dosing kits, is expected to witness the fastest growth during the forecast period, supported by smaller healthcare facilities and clinics that require flexible, cost-effective disinfection solutions for limited instrument volumes. This growth is primarily supported by smaller healthcare facilities and clinics that require flexible and cost-effective disinfection solutions. These systems are suitable for handling limited instrument volumes without the need for large automated equipment. Manual sterilization and dosing kits offer ease of use, portability, and quick deployment in outpatient settings. They also allow healthcare staff to maintain compliance with infection control standards in resource-constrained environments.

- By End-User

On the basis of end-user, the market is segmented into hospitals, medical device manufacturers, pharmaceutical manufacturers, and laboratories. The hospitals segment dominated the market with the largest revenue share of 50% in 2025, driven by the high volume of surgical procedures, need for compliance with infection control protocols, and increasing adoption of automated and liquid disinfection systems. Hospitals require consistent, reliable disinfection across multiple departments, making them primary consumers of advanced solutions. The dominance is further supported by government regulations, accreditation standards, and patient safety mandates. Hospitals also invest in training staff to optimize the use of liquid and automated systems. Growing hospital infrastructure and expansion of private healthcare networks in Europe further reinforce this segment’s market leadership.

The laboratories segment is expected to witness the fastest growth rate of 23% from 2026 to 2033, due to rising diagnostic testing, research activities, and stricter hygiene requirements. Laboratories benefit from portable wipes, sprays, and small-scale disinfection systems that allow rapid sterilization of instruments and surfaces, ensuring safety during research and diagnostic workflows. Growth is fueled by increasing government and private investments in laboratory infrastructure and clinical research. Laboratories often require flexible and rapid disinfection solutions for multiple applications. The rising number of private diagnostic labs also supports market expansion in this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into tender and over-the-counter (OTC). The tender segment dominated the market with the largest revenue share in 2025, driven by large-scale procurement by hospitals, government healthcare programs, and healthcare networks. Tender-based purchases allow bulk acquisition of disinfectants, automated liquid systems, and documentation-compliant solutions at competitive prices, making it the preferred distribution method for institutional buyers. Tender contracts often include service agreements, maintenance, and staff training, making them attractive for long-term hospital planning. The dominance of tender-based procurement is reinforced by government and EU funding programs.

The over-the-counter (OTC) segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by growing adoption among smaller clinics, laboratories, and outpatient centers that prefer flexible purchase options. OTC availability of wipes, sprays, and liquid disinfectants allows rapid procurement, convenient replenishment, and immediate use, supporting day-to-day infection control activities. The growth of this channel is also reinforced by increasing awareness of hygiene and safety standards in private and semi-private healthcare facilities. OTC purchases provide smaller facilities with flexibility without long procurement cycles.

Europe Medical Instrument Disinfection Market Regional Analysis

- Germany dominated the Europe medical instrument disinfection market with the largest revenue share of 45.2% in 2025, characterized by high healthcare standards, strict infection control protocols, and the presence of key medical device manufacturers, with hospitals and diagnostic centers widely adopting advanced disinfection solutions to meet compliance and patient safety requirements

- Healthcare facilities in Germany prioritize patient safety and compliance, leading to high demand for reliable, standardized, and documented disinfection solutions across surgical, diagnostic, and laboratory departments

- This widespread adoption is further supported by the presence of major medical device manufacturers, strong government mandates for sterilization protocols, and substantial investment in hospital infrastructure, establishing advanced liquid and automated disinfection systems as preferred solutions across both public and private healthcare facilities

The U.K. Medical Instrument Disinfection Market Insight

The U.K. medical instrument disinfection market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of hospital-acquired infections (HAIs) and stricter regulatory mandates for infection prevention. Hospitals and clinics are adopting automated and liquid-based disinfection systems to improve compliance and ensure consistent sterilization outcomes. The U.K.’s well-established healthcare infrastructure, combined with strong government support for infection control, is expected to continue to stimulate market growth. The demand is particularly high in surgical units, diagnostic labs, and outpatient facilities.

Germany Medical Instrument Disinfection Market Insight

The Germany medical instrument disinfection market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s emphasis on patient safety, advanced hospital infrastructure, and strict adherence to EU MDR and national sterilization guidelines. Germany’s healthcare facilities are increasingly integrating automated liquid disinfection systems to improve efficiency, reduce human error, and maintain compliance. The presence of major medical device manufacturers and advanced research hospitals promotes the adoption of state-of-the-art disinfection solutions. Hospitals prioritize solutions that ensure traceable results, high reliability, and workflow integration.

France Medical Instrument Disinfection Market Insight

The France medical instrument disinfection market is growing steadily due to increasing investments in hospital modernization and rising awareness about infection prevention in surgical and diagnostic environments. French hospitals are adopting liquid and automated disinfection systems to ensure compliance with regulatory standards and minimize HAIs. The demand is further driven by the expansion of private healthcare facilities and specialized diagnostic labs. The integration of disinfection systems with hospital management workflows allows real-time monitoring and reporting, which is critical for maintaining high patient safety standards.

Poland Medical Instrument Disinfection Market Insight

The Poland medical instrument disinfection market is poised to be the fastest-growing country in Europe during the forecast period due to increasing healthcare infrastructure investments, rising surgical procedures, and growing awareness of cross-contamination risks. Hospitals, clinics, and laboratories are increasingly adopting liquid and automated disinfection systems to ensure effective sterilization. The government’s push for improved healthcare standards and modernization of medical facilities is accelerating market growth. Rising private healthcare investments and the establishment of multi-specialty diagnostic centers are also contributing to higher adoption rates.

Europe Medical Instrument Disinfection Market Share

The Europe Medical Instrument Disinfection industry is primarily led by well-established companies, including:

- 3M (U.S.)

- STERIS Corporation (U.S.)

- Ecolab Inc. (U.S.)

- Clorox Professional (U.S.)

- Diversey (U.S.)

- Xenex Disinfection Services (U.S.)

- Advanced Sterilization Products (ASP) (U.S.)

- Bioquell (U.S.)

- Medivators Inc. (U.S.)

- Midmark Corporation (U.S.)

- TOMI Environmental Solutions, Inc. (U.S.)

- Stericenter (SciCan Ltd.) (Canada)

- Metrex Research LLC (U.S.)

- Ruhof Corporation (U.S.)

- Nanosonics Inc. (U.S.)

- TBJ, Inc. (U.S.)

- CS Medical LLC (U.S.)

- Pure Processing (U.S.)

- Mettrica (U.S.)

- Helios UVC (U.S.)

What are the Recent Developments in Europe Medical Instrument Disinfection Market?

- In November 2025, AI‑powered UV‑C disinfection robots gained increased interest and adoption among European hospitals, with new models using vision systems to scan rooms and target high‑touch surfaces for more consistent pathogen elimination. These robots assist infection control teams by reducing repetitive tasks, improving hygiene outcomes, and integrating into daily hospital workflows seamlessly

- In July 2025, Nanosonics launched the trophon®3 automated high‑level disinfection (HLD) system and trophon2 Plus software upgrade for ultrasound probe disinfection, offering faster cycles, enhanced digital traceability, and improved workflow efficiency for consistent disinfection in healthcare facilities. This launch reflects ongoing innovation to reduce cross‑contamination risks and optimize device reprocessing

- In July 2024, UV Smart advanced its UV‑C disinfection technology for UK hospitals after successful NHS pilot trials, demonstrating significantly shortened decontamination times for endoscopes and potential advantages in chemical and water savings, marking a notable entry of UV‑based systems into mainstream European healthcare workflows

- In July 2024, Getinge launched the Aquadis Index multi‑chamber washer‑disinfector, a high‑capacity, utility‑efficient system designed for central sterile supply departments (CSSDs) in hospitals. The Aquadis Index combines enhanced throughput with reduced water, energy, and detergent consumption, supporting both operational efficiency and sustainability goals in medical instrument reprocessing

- In September 2021, the European Commission delivered the 200th disinfection robot to a hospital in Barcelona, confirming expanded procurement of these autonomous UV‑based units across EU member states as part of broader hygiene and infection control efforts under emergency pandemic support actions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.