Europe Sarcopenia Treatment Market

Market Size in USD Million

USD

789.43 Million

USD

1,131.28 Million

2024

2032

USD

789.43 Million

USD

1,131.28 Million

2024

2032

| 2025 - 2032 | |

| USD 789.43 Million | |

| USD 1,131.28 Million | |

| % | |

|

Europe Sarcopenia Treatment Market Size

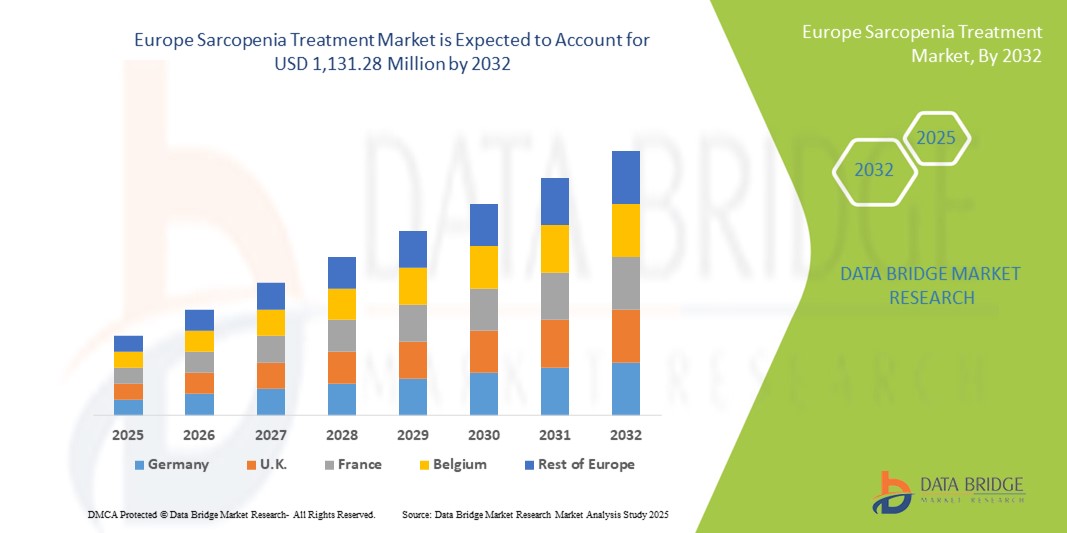

- The Europe sarcopenia treatment market size was valued at USD 789.43 million in 2024 and is expected to reach USD 1,131.28 million by 2032, at a CAGR of 4.6% during the forecast period

- The market growth is largely fueled by the increasing prevalence of malnutrition, vitamin deficiencies, and age-related muscle loss, coupled with growing awareness about sarcopenia’s impact on health and quality of life

- Furthermore, rising demand for effective treatment options such as nutritional supplementation, physical therapy, and medications is establishing sarcopenia treatments as essential for aging populations. These converging factors are accelerating the uptake of therapeutic solutions, thereby significantly boosting the industry's growth

Europe Sarcopenia Treatment Market Analysis

- Sarcopenia treatments, encompassing nutritional supplements, physical therapy, and pharmacological interventions, are becoming increasingly vital for managing age-related muscle loss and maintaining functional independence among the elderly population in Europe due to their effectiveness in improving muscle mass, strength, and overall quality of life

- The rising demand for sarcopenia treatments is primarily driven by the aging European population, increasing awareness about the health impacts of sarcopenia, and growing emphasis on preventive care and healthy aging programs

- Germany dominated the sarcopenia treatment market with the largest revenue share of 23.9% in 2024, characterized by advanced healthcare infrastructure, high healthcare spending, and proactive government initiatives promoting elderly care, with extensive adoption of nutritional supplementation and physical therapy programs

- Italy is expected to be the fastest growing country in the sarcopenia treatment market during the forecast period due to increasing healthcare investments, growing geriatric population, and rising awareness of age-related muscle loss

- Dietary Supplements segment dominated the sarcopenia treatment market with a market share of 39.2% in 2024, driven by the well-established role of protein, vitamin D, and calcium in muscle maintenance and recovery among older adults

Report Scope and Europe Sarcopenia Treatment Market Segmentation

|

Attributes |

Europe Sarcopenia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Sarcopenia Treatment Market Trends

Integration of Digital Health and Telemedicine

- A significant and accelerating trend in the Europe sarcopenia treatment market is the integration of digital health solutions and telemedicine platforms, allowing elderly patients to monitor muscle health, track nutrition, and receive remote guidance from healthcare professionals

- For Instance, the NutriTrack Telehealth Program enables patients to log dietary intake and muscle-strengthening exercises, while physiotherapists provide real-time recommendations for therapy adjustments

- Digital health integration allows continuous monitoring of patient progress, offering personalized treatment plans and reminders for supplementation and exercises, improving adherence and outcomes

- The seamless combination of wearable sensors, mobile apps, and teleconsultations facilitates centralized management of sarcopenia treatment, enabling clinicians to coordinate nutritional, therapeutic, and pharmacological interventions efficiently

- This trend towards technology-enabled care is reshaping expectations for sarcopenia management, with companies such as PhysioPlus developing platforms that integrate patient data, remote exercise supervision, and digital coaching

- The demand for digital health-supported sarcopenia treatments is growing rapidly across hospitals, outpatient clinics, and home-based care, as patients increasingly prioritize convenience, monitoring, and personalized interventions

Europe Sarcopenia Treatment Market Dynamics

Driver

Rising Geriatric Population and Awareness of Age-Related Muscle Loss

- The increasing aging population in Europe, combined with greater awareness of sarcopenia’s impact on mobility and quality of life, is a major driver for the heightened demand for effective treatments

- For Instance, in 2024, Germany launched the “Healthy Aging Program,” promoting nutritional supplementation and exercise interventions in elderly care facilities to mitigate sarcopenia prevalence

- As older adults experience greater risk of falls, frailty, and functional decline, healthcare providers and caregivers are increasingly seeking interventions that improve muscle mass and strength

- The growing emphasis on preventive healthcare, including early diagnosis and timely treatment of sarcopenia, is accelerating the adoption of nutritional supplements, physical therapy, and pharmacological options

- Public health campaigns and geriatric programs are promoting awareness of sarcopenia, driving both patient demand and healthcare provider engagement in delivering targeted treatment solutions

Restraint/Challenge

Limited Accessibility and High Treatment Costs

- Concerns surrounding the affordability and accessibility of sarcopenia treatments pose a significant challenge to broader market adoption across Europe

- For Instance, despite evidence supporting protein supplementation and physiotherapy, some elderly patients in Eastern Europe have limited access to these interventions due to high costs or insufficient healthcare infrastructure

- Variability in healthcare reimbursement policies across countries may restrict patient access to nutritional supplements, medications, or specialized physiotherapy sessions

- While treatment efficacy is well-documented, lack of standardized guidelines and limited awareness among caregivers can reduce adherence and uptake of therapies

- Clinical trials for sarcopenia treatments may use different diagnostic criteria, making it challenging to compare the results of various studies. This lack of standardization can hinder the development and approval of new treatments by regulatory agencies

- Overcoming these challenges through government-supported programs, affordable therapy options, and educational initiatives for patients and caregivers will be vital for sustained market growth

Europe Sarcopenia Treatment Market Scope

The market is segmented on the basis of treatment type, type of sarcopenia, stages, route of administration, gender, end user, and distribution channel.

- By Treatment Type

On the basis of treatment type, the sarcopenia treatment market is segmented into medications, vitamin/dietary supplements, and others. The vitamin/dietary supplements segment dominated the market with the largest revenue share of 39.2% in 2024, driven by the widespread use of protein, vitamin D, and calcium supplementation among the elderly population to prevent muscle loss. Supplements are preferred due to their safety, ease of administration, and ability to maintain muscle mass and function. Increasing awareness about nutritional interventions and supportive government programs further boosts adoption. Patients often receive supplements as the first-line approach in both primary and secondary sarcopenia. The market sees steady demand due to the availability of fortified foods and specialized high-protein formulas. Healthcare providers recommend supplements as part of preventive and therapeutic care for aging populations.

The medications segment is anticipated to witness the fastest growth rate of 11.8% from 2025 to 2032, fueled by novel pharmacological treatments targeting muscle atrophy, hormonal therapies, and myostatin inhibitors. Medications are increasingly prescribed for patients with severe sarcopenia or secondary sarcopenia linked to chronic diseases. Rising R&D investments and regulatory approvals in European countries are accelerating market adoption. Medications provide targeted, clinically validated benefits for improving muscle mass and strength. Awareness campaigns are promoting their use alongside supplements and physiotherapy. Advanced therapies offer potential for combination treatment strategies, further driving growth in the segment.

- By Type

On the basis of type, the sarcopenia treatment market is segmented into primary sarcopenia and secondary sarcopenia. The primary sarcopenia segment dominated the market with the largest revenue share of 55.3% in 2024, driven by age-related muscle loss affecting the elderly population across Europe. Preventive and early intervention programs targeting age-related decline are common in countries such as Germany and France. Primary sarcopenia is often managed through lifestyle interventions, nutritional supplementation, and physiotherapy. Awareness campaigns and geriatric healthcare programs support wide adoption. The prevalence of primary sarcopenia in aging populations ensures consistent demand. Hospitals and clinics integrate preventive measures, maintaining steady market dominance.

The secondary sarcopenia segment is expected to witness the fastest growth rate of 12.3% from 2025 to 2032, fueled by the increasing incidence of sarcopenia due to chronic conditions such as diabetes, COPD, and cancer. Treatment often requires a combination of medications, supplementation, and supervised physiotherapy. Growing research on disease-linked sarcopenia supports development of targeted therapies. Rising prevalence of lifestyle-related and chronic diseases in Europe drives adoption. Clinical programs increasingly include secondary sarcopenia interventions. Awareness among healthcare providers and patients contributes to the accelerating uptake of therapies.

- By Stages

On the basis of stages, the sarcopenia treatment market is segmented into pre-sarcopenia, sarcopenia, and severe sarcopenia. The sarcopenia stage dominated the market with the largest revenue share of 47.8% in 2024, as patients are typically diagnosed during early to moderate stages. Interventions including nutrition, exercise, and medication are most effective at this stage. Regular screening and geriatric programs support early treatment adoption. Hospitals and specialty clinics emphasize timely interventions to prevent progression. Awareness campaigns and proactive management strategies contribute to market dominance. Adoption is driven by improved patient outcomes and reduced risk of mobility decline.

The severe sarcopenia segment is expected to witness the fastest growth rate of 13.1% from 2025 to 2032, fueled by an increasing number of elderly patients with advanced muscle loss. Intensive combination therapies including medications, supplementation, and physiotherapy are required at this stage. Healthcare providers focus on improving mobility, reducing fall risks, and enhancing quality of life. Increasing prevalence of severe sarcopenia among aging populations drives demand for effective interventions. Advanced stage management programs are being implemented in hospitals and clinics. The rising geriatric population ensures sustained market growth in this segment.

- By Route of Administration

On the basis of route of administration, the sarcopenia treatment market is segmented into oral, injectable, and others. The oral segment dominated the market with the largest revenue share of 53.7% in 2024, due to the ease of administering dietary supplements and medications orally. Patients prefer oral treatments for convenience, compliance, and safety. Supplements and medications are widely available over-the-counter and recommended for both primary and secondary sarcopenia. Oral products include fortified foods, capsules, and powders tailored for elderly populations. Adoption is supported by home healthcare programs and clinical recommendations. Market growth is further driven by public awareness campaigns promoting oral supplementation.

The injectable segment is expected to witness the fastest growth rate of 14.2% from 2025 to 2032, fueled by the development of injectable therapies targeting severe sarcopenia and anabolic treatments. Injectable medications provide precise dosing and faster efficacy for advanced cases. Hospitals and specialty clinics are increasingly adopting injectable options to enhance patient outcomes. Advanced therapies enable targeted muscle recovery in chronic or severe sarcopenia patients. Clinical trials and approvals in European markets are supporting adoption. Rising awareness of treatment efficacy among healthcare providers and patients drives segment growth.

- By Gender

On the basis of gender, the sarcopenia treatment market is segmented into male and female. The female segment dominated the market with the largest revenue share of 51.5% in 2024, driven by higher prevalence of sarcopenia among aging women, especially post-menopause due to hormonal changes affecting muscle mass. Nutritional interventions, physiotherapy, and medications are commonly recommended for women. Public health initiatives focusing on women’s health further support adoption. Awareness campaigns target early detection and management in females. Healthcare providers prioritize tailored interventions for older women. The combination of preventive care and therapeutic treatments ensures sustained demand.

The male segment is expected to witness the fastest growth rate of 10.9% from 2025 to 2032, fueled by rising awareness of sarcopenia in elderly men and increasing participation in preventive care programs. Lifestyle interventions, supplementation, and clinical therapies are gaining traction among men. Government and private programs promote early detection in men. Increasing focus on mobility, strength, and functional independence drives adoption. Clinical research highlighting sarcopenia in men supports growth. Rising geriatric male population ensures market expansion in this segment.

- By End User

On the basis of end user, the sarcopenia treatment market is segmented into hospitals, specialty clinics, home healthcare, and others. Hospitals dominated the market with the largest revenue share of 46.2% in 2024, providing comprehensive sarcopenia management including diagnostics, supplementation, medications, and physiotherapy programs. Hospitals have established geriatric care programs, facilitating treatment adoption. Early detection and continuous monitoring in hospitals ensure optimal patient outcomes. Hospitals often collaborate with home healthcare and clinics to extend care. Public and private hospitals actively promote preventive care initiatives. The centralized treatment approach in hospitals ensures consistent market demand.

The home healthcare segment is expected to witness the fastest growth rate of 15.3% from 2025 to 2032, fueled by rising demand for elderly care at home and home-based nutritional and physiotherapy interventions. Remote monitoring and telemedicine programs allow effective management outside hospital settings. Personalized home care programs improve compliance and treatment outcomes. Growth is supported by increasing awareness of convenience and independence among elderly patients. Home healthcare providers integrate digital tools for real-time monitoring. The segment benefits from healthcare policies promoting aging-in-place strategies.

- By Distribution Channel

On the basis of distribution channel, the sarcopenia treatment market is segmented into direct tender, retail sales, and others. The retail sales segment dominated the market with the largest revenue share of 49.6% in 2024, driven by wide availability of supplements and medications through pharmacies, supermarkets, and e-commerce platforms. Easy accessibility, OTC availability, and convenience support market dominance. Consumers prefer retail for frequent purchase and immediate access. Retail expansion in urban and semi-urban areas contributes to revenue growth. Marketing campaigns by brands targeting caregivers and elderly populations increase awareness. The segment benefits from established distribution networks and brand visibility.

The direct tender segment is expected to witness the fastest growth rate of 12.7% from 2025 to 2032, fueled by increasing procurement of sarcopenia treatment products by hospitals, specialty clinics, and government programs for elderly care. Bulk tender orders ensure consistent supply for institutional use. Growing awareness of preventive care and aging programs supports tender-based distribution. Government healthcare initiatives are increasingly relying on direct supply of supplements and medications. Institutional adoption ensures higher-volume sales and sustained revenue. Partnerships with manufacturers and distributors accelerate market growth in this channel.

Europe Sarcopenia Treatment Market Regional Analysis

- Germany dominated the sarcopenia treatment market with the largest revenue share of 23.9% in 2024, characterized by advanced healthcare infrastructure, high healthcare spending, and proactive government initiatives promoting elderly care, with extensive adoption of nutritional supplementation and physical therapy programs

- Patients and healthcare providers in the country increasingly adopt nutritional supplements, physiotherapy, and medications for early intervention and management of sarcopenia

- The widespread adoption is further supported by proactive government programs, public health campaigns, and well-established geriatric care systems, making sarcopenia treatments a critical component of elderly healthcare

Germany Sarcopenia Treatment Market Insight

The Germany sarcopenia treatment market held the largest revenue share in Europe in 2024, driven by advanced healthcare facilities and well-established geriatric care programs. Healthcare providers emphasize early detection and management of sarcopenia through dietary supplementation, physical therapy, and medications. Public health campaigns and government-supported elderly care initiatives promote awareness and adoption of treatments. Germany’s strong focus on preventive healthcare, combined with high healthcare expenditure, encourages the integration of multi-modal sarcopenia management approaches. The market is witnessing growth across hospitals, clinics, and home-based care, reflecting broad acceptance of treatment solutions. Patients benefit from accessible therapeutic options and technological integration in monitoring and care.

France Sarcopenia Treatment Market Insight

The France sarcopenia treatment market is projected to expand at a significant CAGR during the forecast period, primarily driven by the country’s aging population and rising awareness of healthy aging practices. French healthcare providers are increasingly recommending nutritional supplements and physiotherapy to prevent and manage sarcopenia. Government initiatives and preventive healthcare programs targeting elderly populations further support market growth. The integration of telemedicine and digital health platforms enhances patient adherence and treatment monitoring. Residential, outpatient, and home healthcare segments are witnessing increased adoption. The emphasis on quality of life and functional independence among older adults is a key driver for the market in France.

Italy Sarcopenia Treatment Market Insight

The Italy sarcopenia treatment market is expected to grow at a noteworthy CAGR, fueled by an increasing geriatric population and rising awareness of muscle loss-related health risks. Italian healthcare providers promote early intervention through supplementation, exercise programs, and medications. Government-supported initiatives and preventive health campaigns enhance adoption, especially in community and home healthcare settings. Patients are increasingly engaged in self-care programs, supported by digital health and telemonitoring. Hospitals and specialty clinics continue to expand service offerings to address sarcopenia comprehensively. The market growth is driven by the combined effect of preventive care emphasis, healthcare accessibility, and patient awareness.

U.K. Sarcopenia Treatment Market Insight

The U.K. sarcopenia treatment market is anticipated to grow at a considerable CAGR during the forecast period, driven by rising awareness of age-related muscle deterioration and preventive healthcare programs. Healthcare providers are recommending nutritional supplementation, physical therapy, and medications for early intervention. Government initiatives promoting elderly health and healthy aging practices support increased adoption. Digital health integration, including remote monitoring and telemedicine, enhances patient engagement and treatment adherence. Residential and clinical adoption of sarcopenia management programs is expanding steadily. Overall, the U.K.’s emphasis on preventive care, functional independence, and patient-centered interventions is propelling market growth.

Europe Sarcopenia Treatment Market Share

The Europe sarcopenia treatment industry is primarily led by well-established companies, including:

- Biophytis (France)

- Novartis AG (Switzerland)

- Sanofi (France)

- Bayer AG (Germany)

- UCB S.A. (Belgium)

- Teva Pharmaceutical Industries Ltd. (Israel)

- H. Lundbeck A/S (Denmark)

- Galapagos NV (Belgium)

- Ipsen S.A. (France)

- Almirall S.A. (Spain)

- Orion Corporation (Finland)

- Biocryst Pharmaceuticals, Inc. (U.S.)

- Haplogen Pharmaceuticals AG (Switzerland)

- Medtronic (Ireland)

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Lilly USA, LLC (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

What are the Recent Developments in Europe Sarcopenia Treatment Market?

- In September 2025, Biophytis unveiled its Phase 2 trial strategy for Sarconeos (BIO101) targeting obesity-related sarcopenia. The trial will be conducted in Europe and Brazil, aiming to assess the efficacy of BIO101 in improving muscle strength and function in obese patients. This expansion into obesity-related sarcopenia underscores the versatility of BIO101 as a potential treatment for multiple sarcopenia-related conditions

- In August 2025, Biophytis announced that it had received approval from the European Medicines Agency (EMA) and Belgian regulatory authorities to initiate Part I of its Phase 3 clinical trial for Sarconeos (BIO101), a drug candidate for sarcopenia. This approval marks a significant step in the development of pharmacological treatments for sarcopenia in Europe

- In June 2025, Biophytis announced the initiation of the Phase 3 SARA clinical trial for Sarconeos (BIO101), a drug candidate aimed at treating sarcopenia in older adults. This pivotal trial is being conducted across multiple European countries and is designed to evaluate the efficacy and safety of Sarconeos in improving physical performance and muscle strength in sarcopenic patients. The outcome of this trial could pave the way for the first pharmacological treatment for sarcopenia in Europe

- In April 2025, a European initiative led by the COMET (Core Outcome Measures in Effectiveness Trials) group developed a Core Outcome Set (COS) for sarcopenia. This COS aims to standardize the outcomes measured in clinical trials and routine clinical practice, ensuring consistency and comparability across studies. The establishment of this COS is a significant step towards improving the quality of evidence and treatment strategies for sarcopenia in Europe

- In August 2024, TNF Pharmaceuticals announced plans to launch a Phase 2b clinical trial of isomyosamine's efficacy in sarcopenia and frailty early in the first quarter of 2025. This trial aims to further explore the drug's efficacy in sarcopenia/frailty, building on statistically significant positive results from an earlier Phase 2 clinical study

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.