Global Abdominal Adhesions Treatment Market

Market Size in USD Billion

USD

1.70 Billion

USD

2.49 Billion

2024

2032

USD

1.70 Billion

USD

2.49 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.70 Billion | |

| USD 2.49 Billion | |

| % | |

|

Abdominal Adhesions Treatment Market Size

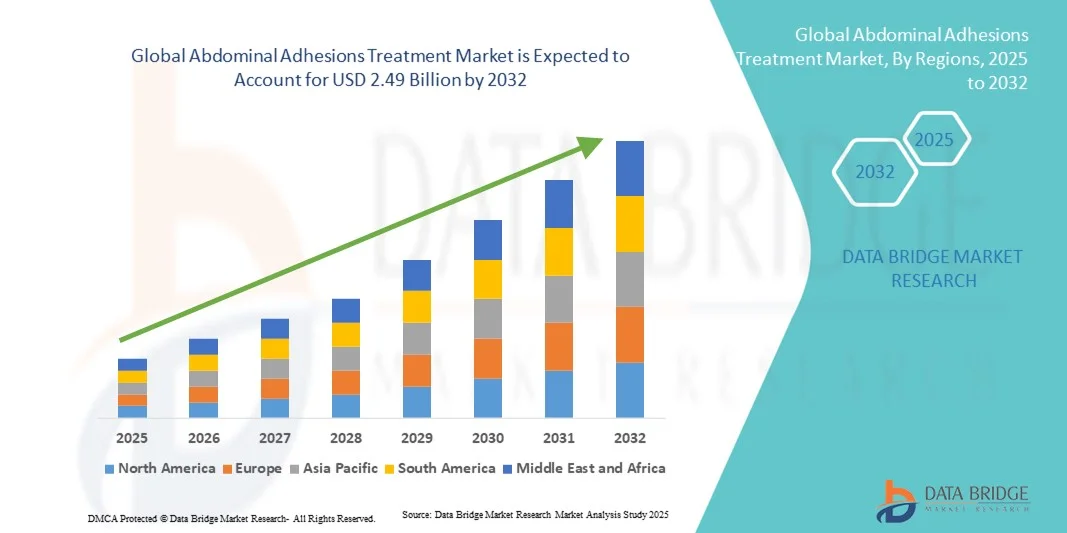

- The global abdominal adhesions treatment market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 2.49 billion by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of abdominal adhesions, rising post-surgical complications, and advancements in minimally invasive surgical techniques, driving demand for effective treatment solutions

- Furthermore, growing awareness among patients and healthcare providers about adhesion-related complications, along with rising healthcare expenditure and development of novel therapeutic interventions, is positioning abdominal adhesion treatments as critical interventions in post-operative care. These converging factors are accelerating the adoption of both surgical and non-surgical treatment options, thereby significantly boosting the industry's growth

Abdominal Adhesions Treatment Market Analysis

- Abdominal adhesions, characterized by fibrous bands forming between abdominal tissues and organs, are increasingly recognized as significant post-surgical complications affecting gastrointestinal, gynecological, and urological procedures, with effective treatments being critical for improving patient outcomes and reducing hospital readmissions

- The escalating demand for abdominal adhesions treatment is primarily fueled by the rising prevalence of post-operative adhesions, advancements in minimally invasive surgical techniques, and growing awareness among healthcare providers and patients regarding adhesion-related complications

- North America dominated the abdominal adhesions treatment market with the largest revenue share of 38.1% in 2024, driven by well-established healthcare infrastructure, high awareness levels, and strong adoption of advanced surgical and therapeutic interventions, with the U.S. witnessing substantial growth in adhesion prevention and treatment procedures, supported by both leading medical device manufacturers and innovative biotechnology firms

- Asia-Pacific is expected to be the fastest-growing region in the abdominal adhesions treatment market, due to expanding healthcare infrastructure, increasing surgical procedures, and rising investments in post-operative care solutions

- Surgery segment dominated the abdominal adhesions treatment market with a 45.9% share in 2024, driven by its effectiveness in severe adhesion cases, rising adoption of laparoscopic and minimally invasive techniques, and continued research and development in adhesion prevention technologies

Report Scope and Abdominal Adhesions Treatment Market Segmentation

|

Attributes |

Abdominal Adhesions Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Abdominal Adhesions Treatment Market Trends

Minimally Invasive Surgical Techniques and Bioengineered Barriers

- A significant and accelerating trend in the global abdominal adhesions treatment market is the growing adoption of minimally invasive surgical techniques, including laparoscopic and robotic-assisted surgeries, reducing post-operative complications and enhancing patient recovery

- For instance, the use of laparoscopic adhesion lysis combined with bioresorbable adhesion barriers improves surgical outcomes and reduces the recurrence of adhesion-related complications

- Bioengineered anti-adhesion barriers, including films and gels, are being increasingly integrated with surgical procedures to prevent fibrous tissue formation, thereby improving patient outcomes and reducing hospital readmissions

- These advanced therapeutic options facilitate safer surgeries and shorter recovery times, while offering physicians more controlled approaches to adhesion prevention

- This trend towards innovative, patient-friendly, and evidence-based interventions is reshaping clinical expectations and standards of care in post-operative management

- The demand for adhesion prevention technologies and minimally invasive interventions is growing rapidly across hospitals and outpatient surgical centers, as healthcare providers increasingly prioritize safety, efficiency, and long-term patient outcomes

Abdominal Adhesions Treatment Market Dynamics

Driver

Rising Post-Surgical Complications and Awareness

- The increasing prevalence of post-surgical adhesions and complications, coupled with rising awareness among healthcare providers and patients, is a significant driver for the heightened demand for abdominal adhesions treatments

- For instance, in 2024, hospitals increasingly adopted laparoscopic surgery combined with anti-adhesion barriers to reduce complications and readmission rates, boosting market demand

- As clinicians become more aware of adhesion-related morbidity, treatment options including surgical intervention and pharmacological therapies are being prioritized to improve patient outcomes

- Furthermore, the expanding number of gastrointestinal, gynecological, and urological procedures globally is increasing the need for effective adhesion management solutions

- The combination of growing surgical volumes, advanced therapeutic options, and preventive strategies is propelling adoption across hospitals, specialty clinics, and outpatient surgical centers

Restraint/Challenge

High Treatment Costs and Regulatory Compliance Hurdles

- The relatively high cost of surgical and barrier-based adhesion prevention treatments poses a challenge to broader market penetration, particularly in developing regions or for smaller healthcare facilities

- For instance, advanced bioresorbable adhesion barriers and robotic-assisted surgical interventions often require significant capital investment, limiting adoption among price-sensitive institutions

- Regulatory compliance and approval requirements for new anti-adhesion products can delay market entry and limit immediate availability, affecting overall adoption rates

- While costs are gradually decreasing with innovation and competition, the perceived premium for advanced therapies can still hinder uptake among healthcare providers with limited budgets

- Overcoming these challenges through cost-effective solutions, streamlined regulatory approvals, and increased clinician education on treatment benefits will be vital for sustained market growth

Abdominal Adhesions Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the abdominal adhesions treatment market is segmented into surgery and others (non-surgical/pharmacological/therapeutic interventions). The surgery segment dominated the market in 2024, accounting for the largest revenue share of 45.9%, driven by its effectiveness in severe adhesion cases and the widespread adoption of laparoscopic and minimally invasive procedures. Surgical intervention remains the preferred option for clinicians to restore intestinal function and relieve chronic pain or bowel obstruction caused by adhesions. Hospitals and specialized surgical centers prioritize surgical solutions due to their reliability and proven outcomes. The segment also benefits from continuous innovation in surgical instruments, adhesion lysis techniques, and post-operative adhesion prevention barriers, which enhance success rates and reduce recurrence. Furthermore, patient preference for definitive treatment options reinforces the dominance of surgical interventions.

The others segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the rising development of anti-adhesion pharmacological therapies, bioresorbable films, and gels that reduce fibrous tissue formation. Non-surgical interventions offer minimally invasive alternatives suitable for mild-to-moderate cases, outpatient management, and combination therapy with surgery. Growing awareness among healthcare providers and patients about post-surgical adhesion prevention is driving adoption. In addition, increasing investment in R&D for novel therapeutic approaches and the push for safer, cost-effective alternatives contribute to the rapid growth of this segment.

- By Diagnosis

On the basis of diagnosis, the abdominal adhesions treatment market is segmented into blood tests, ultrasound, CT scan, X-ray, and others. The CT scan segment dominated the market in 2024, driven by its high accuracy in detecting adhesions, intestinal obstructions, and complications associated with post-operative adhesion formation. CT scans are widely available in hospitals and specialized imaging centers, making them a preferred diagnostic tool for clinicians. The detailed cross-sectional images provided allow surgeons to plan minimally invasive procedures effectively. Clinicians also rely on CT imaging to monitor post-operative recovery and assess the efficacy of adhesion prevention methods. Patient preference for precise diagnosis and faster treatment decisions further supports this segment. Continuous technological advancements in CT imaging, such as higher resolution and lower radiation doses, maintain the segment’s market leadership.

The ultrasound segment is expected to witness the fastest CAGR from 2025 to 2032, due to its non-invasive nature, real-time imaging capabilities, and cost-effectiveness. Portable ultrasound devices are increasingly used in outpatient and emergency settings for preliminary assessment of adhesions or intestinal obstruction. Clinicians value ultrasound for its ease of use, repeatability, and avoidance of radiation exposure. Growing awareness and training in point-of-care ultrasound are also supporting its adoption. The segment benefits from rising demand in developing regions where access to CT and MRI facilities is limited.

- By Symptoms

On the basis of symptoms, the abdominal adhesions treatment market is segmented into vomiting, nausea, loud bowel sounds, bloating, inability to have a bowel movement or pass gas, abdominal swelling, abdominal pain, constipation, and others. The abdominal pain segment dominated the market in 2024, as it is the most common and clinically significant symptom that prompts patients to seek medical attention. Chronic or severe abdominal pain caused by adhesions often necessitates surgical intervention or combination therapy. Hospitals and clinics prioritize management protocols addressing pain relief alongside definitive adhesion treatment. Awareness campaigns about adhesion-related pain among post-surgical patients reinforce early diagnosis and treatment, supporting the segment’s dominance. Treatment innovations targeting pain mitigation, including minimally invasive surgery and barrier therapies, also contribute to segment leadership.

The bloating segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the growing recognition of bloating as an early indicator of adhesion-related complications. Patients increasingly seek treatment for gastrointestinal discomfort, fueling demand for both surgical and non-surgical therapies. The segment growth is supported by advancements in diagnostic imaging and early intervention strategies. Lifestyle management, pharmacological therapies, and bioengineered barriers for mild cases are contributing to rising adoption. Increasing awareness among healthcare providers to address quality-of-life symptoms such as bloating is accelerating market uptake.

- By End-Users

On the basis of end-users, the abdominal adhesions treatment market is segmented into clinics, hospitals, and others. The hospital segment dominated the market in 2024, owing to the higher volume of complex surgical procedures, availability of advanced surgical instruments, and comprehensive post-operative care units. Hospitals are preferred for both surgical interventions and non-surgical therapies due to access to multidisciplinary care, diagnostic imaging, and trained specialists. The segment benefits from high procedural throughput, insurance coverage, and government healthcare initiatives supporting surgical treatment of adhesions. Major hospital chains and teaching hospitals contribute significantly to revenue, maintaining dominance. Integration of minimally invasive surgical techniques and adherence to clinical guidelines further reinforce the hospital segment’s leadership.

The clinic segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the expansion of outpatient surgical centers and specialized gastrointestinal or gynecological clinics. Clinics increasingly adopt laparoscopic procedures, anti-adhesion therapies, and diagnostic imaging for post-operative care. Convenience, cost-effectiveness, and accessibility drive patient preference for clinics for follow-up treatments and minor interventions. Telehealth consultations and outpatient management strategies also support rapid growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the abdominal adhesions treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market in 2024, as hospitals directly procure anti-adhesion pharmacological agents, bioresorbable barriers, and surgical supplies for in-patient procedures. Hospitals maintain centralized supply chains, ensuring availability of both surgical and non-surgical adhesion treatment products. Procurement policies, bulk purchasing, and integration with hospital inventory systems contribute to segment dominance. Clinicians rely on hospital pharmacies to access the latest approved therapeutic options and barriers. Training programs for hospital pharmacists and clinicians further strengthen this segment.

The online pharmacy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing patient awareness, convenience, and digital adoption. Patients and caregivers prefer online platforms for easy access to prescribed adhesion prevention therapies, over-the-counter products, and post-operative care medications. E-commerce platforms offer home delivery, cost comparisons, and subscription services, enhancing accessibility. Growth in telemedicine and virtual consultations further drives online pharmacy adoption. Rising smartphone penetration and e-health initiatives also support rapid uptake in developing regions.

Abdominal Adhesions Treatment Market Regional Analysis

- North America dominated the abdominal adhesions treatment market with the largest revenue share of 38.1% in 2024, driven by well-established healthcare infrastructure, high awareness levels, and strong adoption of advanced surgical and therapeutic interventions, with the U.S. witnessing substantial growth in adhesion prevention and treatment procedures, supported by both leading medical device manufacturers and innovative biotechnology firms

- Patients and healthcare providers in the region highly value advanced surgical interventions, minimally invasive techniques, and anti-adhesion barriers, which improve clinical outcomes and reduce hospital readmissions

- This widespread adoption is further supported by strong research and development capabilities, high healthcare expenditure, and early adoption of innovative therapies, establishing North America as a key market for both surgical and non-surgical adhesion treatment solutions

U.S. Abdominal Adhesions Treatment Market Insight

The U.S. abdominal adhesions treatment market captured the largest revenue share of 82% in 2024 within North America, driven by a high volume of post-surgical procedures and widespread awareness of adhesion-related complications. Patients increasingly seek minimally invasive surgeries and anti-adhesion therapies to reduce post-operative pain, bowel obstruction, and readmission rates. The adoption of advanced laparoscopic techniques, bioresorbable adhesion barriers, and pharmacological interventions is further propelling the market. In addition, growing focus on patient outcomes, insurance coverage for post-operative treatments, and the presence of leading healthcare providers are contributing to market expansion.

Europe Abdominal Adhesions Treatment Market Insight

The Europe market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing surgical volumes and stringent post-operative care standards. Rising awareness of adhesion-related complications among healthcare professionals, coupled with strong hospital infrastructure, is fostering the adoption of both surgical and non-surgical treatments. Countries across Europe are incorporating adhesion prevention protocols in gastrointestinal, gynecological, and urological surgeries. The region is also witnessing growth across private and public hospitals, clinics, and specialized surgical centers, with a strong emphasis on evidence-based clinical outcomes.

U.K. Abdominal Adhesions Treatment Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the rising prevalence of post-operative adhesions and a strong focus on patient care quality. Hospitals and outpatient surgical centers are increasingly adopting minimally invasive surgical procedures and bioresorbable adhesion barriers. Growing concerns regarding post-surgical complications and readmissions are encouraging healthcare providers to implement adhesion prevention strategies. The U.K.’s robust healthcare system and adoption of advanced diagnostic imaging and therapeutic interventions are expected to continue supporting market growth.

Germany Abdominal Adhesions Treatment Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, driven by high awareness of post-operative complications and demand for technologically advanced treatment solutions. Germany’s well-established healthcare infrastructure, emphasis on innovation in surgical procedures, and stringent clinical guidelines promote the adoption of adhesion prevention therapies. Hospitals and specialized clinics increasingly integrate minimally invasive surgery and barrier technologies to improve patient outcomes. Rising focus on patient safety and post-surgical quality of care also reinforces the market’s growth trajectory.

Asia-Pacific Abdominal Adhesions Treatment Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR of 6.2% during the forecast period of 2025 to 2032, fueled by increasing surgical procedures, rapid urbanization, and expanding healthcare infrastructure in countries such as China, Japan, and India. Rising awareness among healthcare providers and patients about post-operative adhesions is driving the adoption of both surgical and non-surgical treatments. Government initiatives supporting healthcare modernization, investment in hospital networks, and increasing disposable incomes are accelerating market growth.

Japan Abdominal Adhesions Treatment Market Insight

The Japan market is gaining momentum due to the country’s advanced healthcare infrastructure, high surgical volumes, and growing patient focus on post-operative recovery. Minimally invasive surgeries, combined with adhesion prevention strategies, are becoming widely adopted in hospitals and specialized surgical centers. The integration of advanced diagnostic tools with post-operative care management is further fueling market growth. In addition, the aging population is such asly to drive demand for safer, less invasive treatments and therapies that reduce adhesion-related complications.

India Abdominal Adhesions Treatment Market Insight

The India market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, rising surgical procedures, and increasing patient awareness of post-operative adhesion complications. Hospitals and clinics are adopting minimally invasive techniques and bioresorbable adhesion barriers to improve patient outcomes. Government initiatives promoting healthcare access and expansion of surgical infrastructure, combined with the availability of cost-effective treatment options, are key factors propelling the market. Increasing healthcare spending and the presence of domestic manufacturers supporting affordable therapies further contribute to market growth.

Abdominal Adhesions Treatment Market Share

The Abdominal Adhesions Treatment industry is primarily led by well-established companies, including:

- Baxter. (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Medtronic Ireland)

- BD (U.S.)

- Anika Therapeutics, Inc. (U.S.)

- Fziomed, Inc. (U.S.)

- Mast Biosurgery, Inc. (Switzerland)

- Innocoll Holdings PLC (Ireland)

- Atrium Health (U.S.)

- CorMatrix Cardiovascular, Inc. (U.S.)

- Terumo Corporation (Japan)

- BiosCompass (U.S.)

- W.L. Gore & Associates (U.S.)

- GUNZE LIMITED (Japan)

- Leader Biomedical (Netherlands)

- Luna (U.S.)

- PlantTec Medical GmbH (Germany)

- Actamax Surgical Materials, LLC (U.S.)

- KCI Medical (U.S.)

What are the Recent Developments in Global Abdominal Adhesions Treatment Market?

- In August 2025, The American College of Surgeons awarded a two-year, USD 100,000 grant to researchers at Stanford University to further develop the T-5224-hydrogel therapy for preventing abdominal adhesions. The grant supports sustained-release intraperitoneal therapy, aiming to reduce adhesion formation post-surgery

- In March 2025, Researchers at Stanford Medicine have developed a gel that prevents abdominal adhesions in animal models following surgery. The gel, containing the small molecule T-5224, is applied as a spray or wash inside the abdominal cavity immediately after surgery. Over two weeks, it releases T-5224, blocking the activation of fibroblasts without affecting normal wound healing. This approach offers a potential non-surgical method to prevent adhesions

- In September 2024, The American College of Surgeons hosted a summit bringing together experts from nearly a dozen countries to discuss surgical adhesions. The summit focused on understanding, preventing, and treating surgical adhesions, which affect a significant percentage of patients undergoing abdominal or pelvic surgery

- In May 2024, Radboud University Medical Center secured millions in funding to investigate the prevention of abdominal adhesions. The research focuses on using barrier agents to prevent adhesions from regrowing after surgery, monitoring disease recurrence, abdominal pain, and nutritional issues in patients across multiple hospitals

- In December 2023, Researchers at Radboud University Medical Center in the Netherlands have developed a method to prevent abdominal adhesions by applying a layer of sugar during surgery. This approach, detected via MRI video, aims to reduce chronic pain and adhesion formation post-abdominal surgery

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.