Global Acromicric Dysplasia Treatment Market

Market Size in USD Million

USD

50.50 Million

USD

81.71 Million

2025

2033

USD

50.50 Million

USD

81.71 Million

2025

2033

| 2026 - 2033 | |

| USD 50.50 Million | |

| USD 81.71 Million | |

| % | |

|

Acromicric Dysplasia Treatment Market Size

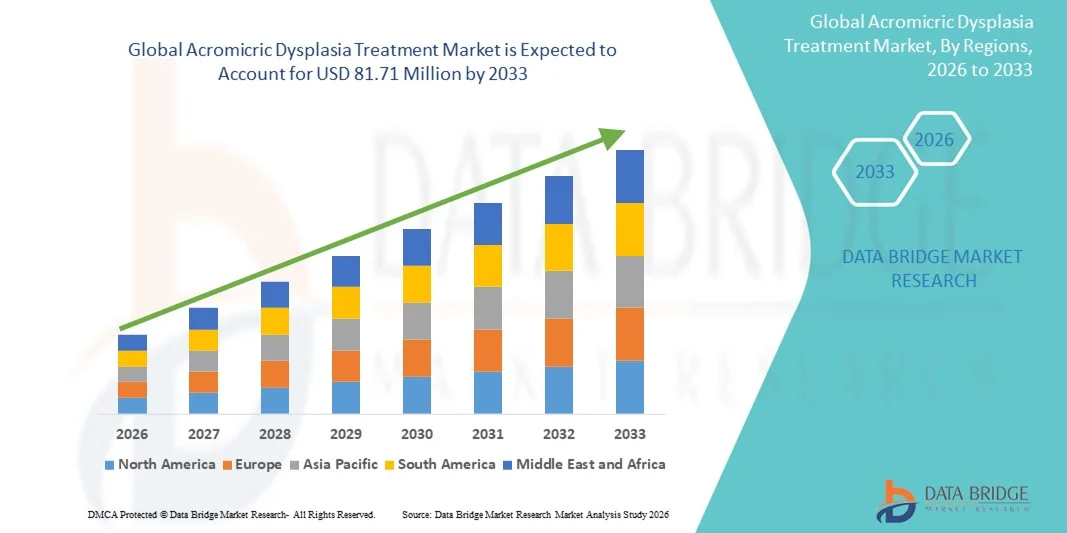

- The global acromicric dysplasia treatment market size was valued at USD 50.50 million in 2025 and is expected to reach USD 81.71 million by 2033, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by advancements in genetic diagnostics, increasing R&D into orphan and ultra-rare bone disorders, and the rising adoption of personalized therapies tailored to rare skeletal conditions

- Furthermore, rising demand from patient advocacy groups and innovation in gene and molecular therapies is positioning acromicric dysplasia treatment as a future beneficiary of the broader rare-disease therapeutics boom, accelerating the uptake of potential treatment solutions and driving long-term industry growth

Acromicric Dysplasia Treatment Market Analysis

- Acromicric dysplasia treatments, including orthopedic management, physical therapy, growth hormone therapy, genetic counseling, and supportive care, are increasingly critical for improving skeletal development and quality of life in patients with this ultra-rare disorder

- The market growth is primarily driven by advancements in genetic diagnostics, rising awareness of rare skeletal disorders, and the increasing adoption of personalized treatment approaches tailored to patients’ specific needs

- North America is expected to dominate the acromicric dysplasia treatment market with the largest revenue share of 43.7% in 2025, owing to advanced healthcare infrastructure, strong research funding for rare diseases, and early adoption of therapies including genetic testing and growth hormone interventions

- Asia-Pacific is projected to be the fastest-growing region during the forecast period due to increasing investment in rare disease research, growing patient advocacy, and improving access to specialized healthcare services such as clinics and hospitals offering comprehensive diagnostic and treatment options

- Orthopedic management is the dominant treatment segment with a market share of 39.5% in 2025, addressing key symptoms such as short hands and feet, growth retardation, and joint limitations, and is primarily delivered through hospital settings

Report Scope and Acromicric Dysplasia Treatment Market Segmentation

|

Attributes |

Acromicric Dysplasia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Acromicric Dysplasia Treatment Market Trends

Advancements in Personalized and Gene-Based Therapies

- A significant and accelerating trend in the global acromicric dysplasia treatment market is the development of personalized therapies, including gene-based interventions and targeted growth hormone programs, which aim to improve skeletal growth and patient quality of life

- For instance, recent research initiatives are exploring individualized growth hormone dosing protocols and gene therapy trials designed to correct mutations associated with acromicric dysplasia, offering patients tailored treatment options

- Personalized therapy approaches enable clinicians to optimize treatment efficacy, minimize side effects, and monitor patient-specific responses over time. For instance, orthopedic management combined with genetic counseling allows for better long-term care planning and growth outcomes

- Integration of advanced diagnostics, such as next-generation genetic testing, with treatment planning facilitates more precise and timely interventions, enabling proactive symptom management for growth retardation, joint limitations, and distinctive facial features

- This trend towards more patient-specific, data-driven, and targeted treatment strategies is reshaping expectations in rare disease care. Consequently, biotech companies are focusing on developing gene-targeted therapies and personalized orthopedic solutions

- The demand for therapies that offer personalized and targeted outcomes is growing steadily, as clinicians and caregivers increasingly prioritize treatments that address both symptomatic relief and the underlying genetic causes of acromicric dysplasia

Acromicric Dysplasia Treatment Market Dynamics

Driver

Growing Need for Rare Disease Therapeutics and Improved Quality of Life

- The increasing recognition of ultra-rare skeletal disorders and the rising focus on improving patient outcomes are significant drivers of demand for acromicric dysplasia treatment

- For instance, clinics and hospitals are expanding access to growth hormone therapy and orthopedic management programs to enhance skeletal development and functional mobility for diagnosed patients

- As awareness of acromicric dysplasia increases among healthcare providers and patient advocacy groups, more individuals are seeking timely diagnosis and intervention, creating a larger addressable market

- Furthermore, advancements in genetic testing and personalized therapy options are encouraging early intervention and better symptom management, reinforcing the adoption of comprehensive treatment approaches

- The convenience of integrated care programs, combining orthopedic management, genetic counseling, and growth hormone therapy, is further driving adoption, as multidisciplinary care ensures holistic patient management

- Increasing government support and orphan drug incentives for rare diseases are promoting research investment and accelerating the development of novel therapies

- The growing role of patient advocacy organizations is facilitating awareness campaigns, early diagnosis programs, and access to treatment, further stimulating market growth

Restraint/Challenge

Limited Patient Population and High Treatment Costs

- The ultra-rare nature of acromicric dysplasia, with only a small number of diagnosed patients worldwide, poses a significant challenge to large-scale market development

- For instance, the extremely low prevalence makes clinical trials and large-scale therapy adoption difficult, limiting the commercial potential of new treatments

- High costs associated with growth hormone therapy, gene-targeted interventions, and specialized orthopedic management can hinder access, especially in regions with limited healthcare coverage

- Limited awareness among general practitioners and delayed diagnosis often result in late intervention, reducing treatment effectiveness and market penetration

- Overcoming these challenges requires increased awareness, patient advocacy programs, cost-effective therapy development, and expanded access to specialized diagnostic and treatment centers for ultra-rare disorders

- Regulatory hurdles and complex approval processes for orphan drugs can slow the introduction of new therapies, delaying patient access to advanced treatments

- Fragmented healthcare infrastructure in emerging regions can limit the availability of specialized care, diagnostics, and therapies, restricting market growth potential

Acromicric Dysplasia Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the acromicric dysplasia market is segmented into orthopedic management, physical therapy, growth hormone therapy, genetic counseling, and others. The orthopedic management segment dominated the market with the largest market revenue share of 39.5% in 2025, driven by its crucial role in addressing skeletal abnormalities, improving joint mobility, and mitigating deformities in patients. Orthopedic interventions are often prioritized by clinicians for long-term care planning, especially in cases involving limb shortening and joint limitations. Hospitals and specialty clinics frequently adopt structured orthopedic programs as the backbone of symptomatic treatment. The segment benefits from established clinical protocols and the availability of trained orthopedic specialists. Its adoption is further supported by patient demand for functional mobility improvements and the ability to complement other therapies such as physical therapy or growth hormone therapy. The combination of efficacy, accessibility, and clinical familiarity makes orthopedic management the preferred choice among treatment options.

The growth hormone therapy segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its targeted action in promoting linear growth and improving overall height outcomes in pediatric patients. Hormone therapy adoption is accelerating due to increasing awareness among clinicians and parents about early intervention benefits. Ongoing research and personalized dosing protocols are enhancing efficacy and safety, boosting confidence in growth hormone therapies. Government and insurance incentives for rare pediatric disorders are supporting broader uptake in specialized centers. The segment also benefits from technological advancements in hormone delivery systems, reducing patient discomfort and improving adherence. Growth hormone therapy’s potential to directly influence disease progression and height outcomes positions it as a high-growth subsegment in the market.

- By Diagnosis

On the basis of diagnosis, the acromicric dysplasia market is segmented into genetic testing, imaging testing, and others. The genetic testing segment dominated the market with the largest revenue share of 41.5% in 2025, as it enables precise identification of mutations in the FBN1 gene responsible for the disorder. Genetic testing allows early diagnosis, facilitating timely intervention with personalized therapies. Clinicians rely on these tests to differentiate acromicric dysplasia from other skeletal dysplasias, ensuring appropriate care pathways. Advancements in next-generation sequencing have increased test accuracy and reduced turnaround time, driving adoption. The segment benefits from growing awareness among healthcare providers and patient advocacy initiatives promoting genetic screening. Genetic testing also supports long-term care planning by guiding orthopedic and growth hormone therapy strategies.

The imaging testing segment is expected to witness the fastest growth from 2026 to 2033, driven by innovations in high-resolution imaging modalities such as MRI and CT scans. Imaging aids in monitoring bone development, skeletal deformities, and treatment outcomes over time. The integration of imaging data with clinical management plans enhances therapy customization. Imaging services are increasingly accessible in specialized centers and pediatric hospitals, facilitating their rapid adoption. Technological improvements in imaging reduce patient exposure to radiation and increase diagnostic precision. The segment’s growth is further supported by its complementary role alongside genetic testing and orthopedic management.

- By Symptoms

On the basis of symptoms, the acromicric dysplasia market is segmented into short hands and feet, growth retardation, distinctive facial features, joint limitations, and others. The growth retardation segment dominated the market with the largest revenue share of 36.8% in 2025, as it represents the most visible and clinically critical symptom affecting patients’ height and development. Growth retardation often prompts early clinical attention, driving demand for therapeutic interventions such as growth hormone therapy. This segment is highly relevant for pediatric monitoring programs and long-term treatment planning. Clinicians frequently combine symptom management strategies with orthopedic care to improve functional outcomes. Patient advocacy and awareness campaigns often highlight growth challenges as key markers for diagnosis. The segment’s clinical significance and impact on quality of life reinforce its market dominance.

The joint limitations segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing adoption of physiotherapy, orthopedic interventions, and supportive care programs aimed at improving mobility. The prevalence of joint stiffness and restricted range of motion in patients creates an urgent demand for therapeutic solutions. Growing awareness of early intervention benefits in preserving joint function supports rapid adoption. Innovative physiotherapy programs, along with wearable monitoring devices, are enhancing treatment efficiency. The segment also benefits from multidisciplinary care approaches, combining orthopedic and physical therapy expertise. The rising focus on functional mobility improvements positions joint limitation management as a high-growth subsegment.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The hospital segment dominated the market with the largest revenue share of 44.3% in 2025, due to the availability of specialized pediatric and orthopedic departments, advanced diagnostic facilities, and multidisciplinary treatment teams. Hospitals provide comprehensive care, combining genetic testing, orthopedic management, and growth hormone therapy in a single care pathway. Patient trust in hospital-based interventions and regulatory standards supports adoption. High patient volumes and access to experienced clinicians make hospitals the preferred care setting. Hospitals are also more such asly to offer innovative therapies and participate in clinical trials, enhancing treatment availability. The integration of electronic health records and coordinated care programs further strengthens hospital dominance.

The clinic segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing specialized rare disease clinics focusing on early diagnosis, growth monitoring, and therapy administration. Clinics offer personalized attention and flexibility in treatment schedules. Telemedicine and outreach programs allow clinics to reach patients in remote regions, enhancing market penetration. The segment benefits from partnerships with hospitals and academic research centers for referrals and specialized testing. Clinics’ focus on patient education and long-term monitoring promotes adherence to therapy. The rise of private rare disease clinics and multidisciplinary outpatient programs supports robust growth in this subsegment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share of 39.6% in 2025, owing to its direct connection with hospital-based treatment programs, immediate availability of prescribed therapies, and integration with patient care pathways. Hospital pharmacies are preferred for administering growth hormone therapy, orthopedic supplements, and supportive medications. They ensure proper handling, storage, and timely dispensing of therapies. Close coordination with clinicians enhances patient adherence and outcomes. The segment benefits from regulatory compliance and trusted sourcing, reassuring patients and caregivers. Hospitals’ centralized procurement and inventory systems further strengthen hospital pharmacy dominance.

The online pharmacy segment is expected to witness the fastest growth from 2026 to 2033, driven by rising e-commerce adoption, convenience of home delivery, and increasing awareness of rare disease therapies. Online platforms enable access to medications for patients in remote or underserved regions. Digital platforms often provide subscription services, reminders, and patient support programs, enhancing adherence. Growth is supported by partnerships with specialty pharmacies and logistics providers. Online pharmacies also offer price transparency and comparative options, appealing to cost-sensitive patients. The increasing comfort with digital health and e-prescription systems positions online pharmacy as a high-growth distribution channel.

Acromicric Dysplasia Treatment Market Regional Analysis

- North America is expected to dominate the acromicric dysplasia treatment market with the largest revenue share of 43.7% in 2025, owing to advanced healthcare infrastructure, strong research funding for rare diseases, and early adoption of therapies including genetic testing and growth hormone interventions

- Patients and clinicians in the region highly value the availability of specialized pediatric and rare disease centers, access to cutting-edge genetic testing, and integrated multidisciplinary care programs that combine diagnosis, treatment, and follow-up

- This widespread adoption is further supported by high healthcare spending, a well-established network of hospitals and clinics, and growing awareness among patient advocacy groups, establishing North America as the preferred region for both early diagnosis and comprehensive treatment of acromicric dysplasia

U.S. Acromicric Dysplasia Treatment Market Insight

The U.S. acromicric dysplasia treatment market captured the largest revenue share of 80% in 2025 within North America, fueled by advanced healthcare infrastructure, early adoption of personalized therapies, and widespread access to pediatric and rare disease centers. Patients and clinicians increasingly prioritize early diagnosis through genetic testing and timely interventions with orthopedic management and growth hormone therapy. The growing awareness among patient advocacy groups, coupled with strong research funding and government incentives for rare diseases, further propels market growth. Moreover, the availability of specialized clinics, integrated multidisciplinary care, and advanced diagnostic technologies significantly contributes to the market’s expansion.

Europe Acromicric Dysplasia Treatment Market Insight

The Europe acromicric dysplasia treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of rare skeletal disorders and supportive healthcare policies for orphan diseases. Increasing urbanization and improving access to specialized hospitals and clinics are fostering adoption of advanced treatment programs. European patients and caregivers are drawn to personalized therapy approaches that combine growth hormone therapy, orthopedic management, and genetic counseling. The region is witnessing significant growth across pediatric hospitals, rare disease centers, and multidisciplinary clinics, with treatments being incorporated into both newly diagnosed patients and ongoing management programs.

U.K. Acromicric Dysplasia Treatment Market Insight

The U.K. acromicric dysplasia treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising trend of personalized care and early intervention programs. Concerns regarding growth retardation, joint limitations, and skeletal deformities are encouraging clinicians and caregivers to adopt integrated treatment strategies. The U.K.’s strong healthcare infrastructure, coupled with robust patient advocacy and awareness campaigns, is expected to continue to stimulate market growth. Access to specialized genetic testing, hospital-based therapy programs, and follow-up care further supports treatment adoption in both public and private healthcare settings.

Germany Acromicric Dysplasia Treatment Market Insight

The Germany acromicric dysplasia treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by high awareness of rare skeletal disorders and the availability of technologically advanced diagnostic and therapeutic solutions. Germany’s well-established healthcare infrastructure and emphasis on innovation promote the adoption of personalized treatment programs. Integration of genetic testing, orthopedic management, and growth hormone therapy in hospital and clinic settings is becoming increasingly prevalent. A strong focus on patient-centered care and multidisciplinary treatment strategies aligns with local expectations and supports steady market expansion.

Asia-Pacific Acromicric Dysplasia Treatment Market Insight

The Asia-Pacific acromicric dysplasia treatment market is poised to grow at the fastest CAGR of 22% during 2026 to 2033, driven by increasing healthcare access, rising awareness of rare diseases, and improving pediatric care infrastructure in countries such as China, Japan, and India. The region’s growing inclination towards early diagnosis and personalized therapy adoption is promoting market uptake. Furthermore, expansion of specialized rare disease clinics, government initiatives supporting rare disease management, and availability of cost-effective treatment options are increasing access for patients across the region.

Japan Acromicric Dysplasia Treatment Market Insight

The Japan acromicric dysplasia treatment market is gaining momentum due to the country’s advanced healthcare system, high focus on rare disease management, and growing number of specialized pediatric centers. Early diagnosis through genetic testing and timely interventions with growth hormone therapy and orthopedic management are driving adoption. Integration of multidisciplinary care programs and follow-up monitoring enhances treatment outcomes. Moreover, increasing awareness among clinicians and caregivers, coupled with government support for rare disease initiatives, is fueling market growth in both residential and clinical settings.

India Acromicric Dysplasia Treatment Market Insight

The India acromicric dysplasia treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising awareness of rare skeletal disorders, expanding pediatric care infrastructure, and increasing availability of specialized clinics. India’s growing middle class, improving healthcare access, and focus on early intervention programs are key factors propelling the market. The presence of cost-effective therapies, combined with supportive government initiatives for rare disease management, further accelerates adoption. In addition, private hospitals and specialty clinics are increasingly providing integrated treatment solutions, contributing to the market’s robust growth.

Acromicric Dysplasia Treatment Market Share

The Acromicric Dysplasia Treatment industry is primarily led by well-established companies, including:

- BioMarin (U.S.)

- RIBOMIC (Japan)

- Ascendis Pharma Denmark)

- BridgeBio Pharma, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- PhaseBio Pharmaceuticals, Inc. (U.S.)

- SISAF LTD (U.S.)

- Novo Nordisk A/S (Denmark)

- F. Hoffmann-La Roche Ltd (Switzerland)

- LG Chem (South Korea)

- Ferring B.V. (Netherlands)

- JCR Pharmaceuticals Co., Ltd (Japan)

- KVK Tech, Inc. (U.S.)

- VIVUS LLC. (U.S.)

- ProLynx Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Eli Lilly and Company (U.S.)

- Ipsen Pharma (France)

- Novartis AG (Switzerland)

- Xiamen Amoytop Biotech Co., Ltd. (China)

What are the Recent Developments in Global Acromicric Dysplasia Treatment Market?

- In April 2025, A publication titled “Acromicric dysplasia: Long-term outcome and evidence of autosomal dominant inheritance” reported a novel FBN1 mutation identified in six family members. The study provided long-term follow-up data on growth, skeletal deformities, and clinical outcomes, emphasizing the hereditary nature of acromicric dysplasia

- In July 2024, The article “Case Report: Two different acromelic dysplasia phenotypes in a Chinese family caused by a missense mutation in FBN1 and a literature review” was published, highlighting the occurrence of two distinct phenotypes (acromicric dysplasia and geleophysic dysplasia 2) within the same family carrying the FBN1 c.5179C>T (p.Arg1727Trp) mutation. The proband received rhGH therapy, showing a body-length gain of 0.72 SDS in six months

- In July 2023, A case report titled “Acromicric dysplasia caused by a mutation of fibrillin 1 in a family” described a four-year-old Chinese patient treated with recombinant human growth hormone (rhGH) for over five years. Height SDS improved from –3.64 to –2.88 in the first year, demonstrating early efficacy of rhGH therapy in promoting linear growth. The study also noted that long-term outcomes remain uncertain and emphasized the need for ongoing monitoring of growth, orthopedic management, and potential side effects

- In August 2021, A natural-history study titled “Geleophysic and acromicric dysplasias: natural history and genotype-phenotype correlation” was published, providing detailed observations on disease progression, skeletal deformities, short stature, and phenotypic variability in acromicric and related dysplasias

- In May 2021, A Chinese study titled “A Review of Three Chinese Cases of Acromicric with FBN1 Mutations” was published, reporting two novel mutations (c.5272G>T (p.D1758Y) and c.5183C>T (p.A1728V)) in the FBN1 gene in three patients. The study expanded the mutational spectrum associated with acromicric dysplasia, providing critical insights for genetic counseling and targeted therapy planning

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.