Global Allogeneic Stem Cells Market

Market Size in USD Billion

USD

1.09 Billion

USD

2.70 Billion

2025

2033

USD

1.09 Billion

USD

2.70 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.09 Billion |

Market Size (Forecast Year) |

USD 2.70 Billion |

CAGR |

% |

Major Markets Players |

|

Allogeneic Stem Cells Market Size

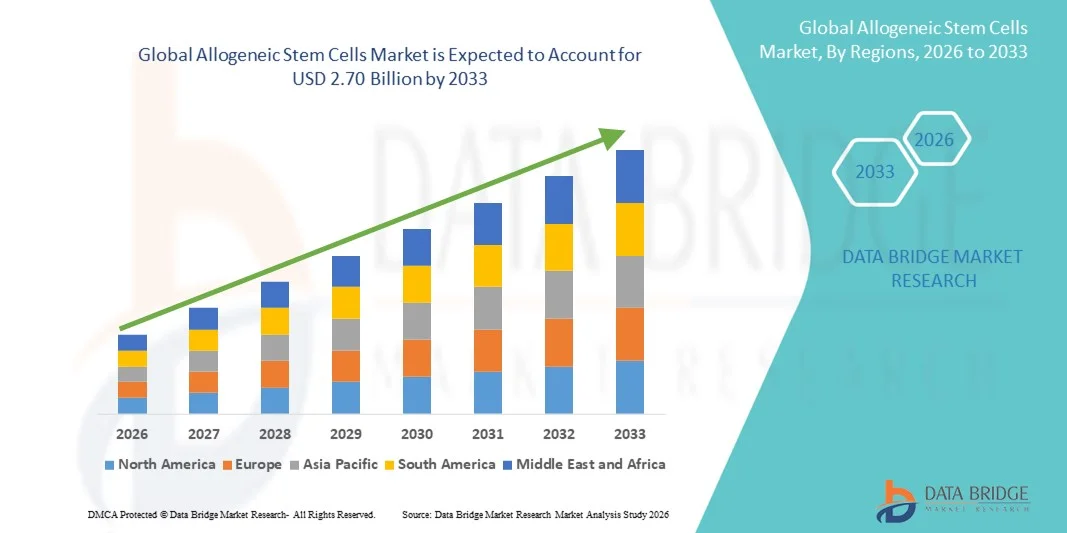

- The global allogeneic stem cells market size was valued at USD 1.09 billion in 2025 and is expected to reach USD 2.70 billion by 2033, at a CAGR of 12.04% during the forecast period

- The market growth is largely driven by increasing prevalence of chronic diseases, rising demand for regenerative therapies, and advancements in stem cell processing and storage technologies, which are enhancing clinical applications in hematology, oncology, and immunology

- In addition, growing investments in stem cell research, government initiatives supporting cell therapy, and the rising adoption of allogeneic stem cell transplants as a treatment for life-threatening conditions are fueling market expansion. These combined factors are significantly accelerating the uptake of allogeneic stem cell therapies, thereby boosting the industry's overall growth

Allogeneic Stem Cells Market Analysis

- Allogeneic stem cells, derived from healthy donors, are increasingly critical in regenerative medicine, drug development, and therapeutic applications due to their ability to replace or repair damaged cells in various diseases

- The growing demand for allogeneic stem cell therapies is primarily driven by rising prevalence of chronic and genetic disorders, advancements in cell processing and storage technologies, and increasing adoption in clinical research and drug development

- North America dominated the allogeneic stem cells market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, significant R&D investments, favorable regulatory frameworks, and the presence of key industry players in cell therapy and regenerative medicine

- Asia-Pacific is expected to be the fastest-growing region in the allogeneic stem cells market during the forecast period, fueled by rising healthcare expenditure, increasing patient awareness, expanding medical facilities, and supportive government initiatives promoting stem cell research and clinical adoption

- MUD (Matched Unrelated Donor) transplant segment dominated the market with a share of 52.9% in 2025, driven by the growing demand for stem cell transplants in patients lacking compatible family donors

Report Scope and Allogeneic Stem Cells Market Segmentation

|

Attributes |

Allogeneic Stem Cells Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Allogeneic Stem Cells Market Trends

Advancements in Off-the-Shelf Allogeneic Therapies

- A significant trend in the allogeneic stem cells market is the development of off-the-shelf, ready-to-use stem cell therapies, which are reducing treatment preparation times and enabling scalable regenerative solutions

- For instance, companies such as Fate Therapeutics are developing induced pluripotent stem cell-derived allogeneic therapies that can be administered without patient-specific customization, improving accessibility and speed of treatment

- Technological innovations allow for cryopreservation and long-term storage of allogeneic stem cells while maintaining viability, which enhances clinical adoption across multiple therapeutic areas

- Integration with advanced delivery systems and automated manufacturing platforms is enabling consistent quality and faster deployment of stem cell therapies, improving clinical outcomes and operational efficiency

- This trend toward off-the-shelf, highly standardized allogeneic cell therapies is transforming patient treatment expectations, with companies focusing on scalable solutions for oncology, hematology, and degenerative disease applications

- The demand for such ready-to-use therapies is increasing rapidly, as healthcare providers and research institutions seek faster, more reliable, and widely applicable stem cell treatment options

- The growing integration of digital health platforms and AI for monitoring patient outcomes and optimizing allogeneic stem cell therapy protocols is further shaping the market trend toward personalized, data-driven treatments

Allogeneic Stem Cells Market Dynamics

Driver

Rising Prevalence of Chronic and Genetic Disorders

- The increasing prevalence of chronic diseases, blood disorders, and genetic conditions is a major driver for the growing adoption of allogeneic stem cell therapies

- For instance, the rising incidence of leukemia, lymphoma, and aplastic anemia has heightened the need for matched donor transplants, boosting clinical demand for allogeneic stem cells

- Advancements in stem cell processing, storage, and transplantation techniques have improved patient outcomes, encouraging wider adoption in clinical and research settings

- Growing investments by biotech companies in regenerative medicine and stem cell therapy pipelines are further supporting market expansion and innovation

- The ability of allogeneic stem cells to treat conditions where autologous sources are not viable reinforces their increasing importance across therapeutic areas, driving market growth

- Increasing government initiatives and funding for regenerative medicine research are promoting clinical trials and facilitating faster commercialization of allogeneic stem cell therapies

- Rising collaborations between global pharmaceutical companies and academic institutions to accelerate R&D and expand therapeutic applications are further strengthening market growth

Restraint/Challenge

Immune Rejection Risk and Regulatory Complexities

- Challenges in the allogeneic stem cells market include potential immune rejection and graft-versus-host disease, which can limit clinical success and patient safety

- For instance, transplant recipients sometimes experience immune complications that require additional immunosuppressive therapy, complicating treatment protocols

- Rigorous regulatory requirements for cell therapy manufacturing, safety, and clinical trials increase time-to-market and operational costs for companies

- The high cost of allogeneic stem cell therapies compared to conventional treatments can restrict adoption, particularly in developing regions or among price-sensitive healthcare providers

- Addressing these challenges requires improved immunomodulation techniques, robust clinical protocols, and adherence to evolving regulatory standards to ensure safety, efficacy, and broader market penetration

- Limited availability of matched donors, especially for ethnically diverse populations, poses a challenge for wide-scale adoption of allogeneic stem cell therapies

- Concerns around long-term safety and efficacy, including potential tumorigenicity or unintended differentiation, remain a critical restraint for both clinicians and patients

Allogeneic Stem Cells Market Scope

The market is segmented on the basis of product type, application, and end users.

- By Product Type

On the basis of product type, the global allogeneic stem cells market is segmented into Close Family Member Transplant and MUD (Matched Unrelated Donor) Transplant. The MUD transplant segment dominated the market with the largest revenue share of 52.9% in 2025, driven by the growing need for stem cell transplants among patients who do not have compatible family donors. MUD transplants are increasingly preferred in clinical settings due to their ability to treat a wider range of hematologic and genetic disorders, including leukemia and aplastic anemia. The segment also benefits from advancements in donor matching technologies, improved graft-versus-host disease management, and enhanced cryopreservation methods that ensure higher transplant success rates. Healthcare providers and research institutions are adopting MUD transplants more frequently due to their broader applicability across diverse patient populations. In addition, growing awareness among patients and clinicians regarding donor registries and international collaborations is supporting market expansion in this segment.

The Close Family Member Transplant segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing emphasis on personalized medicine and lower risk of immune rejection. These transplants offer improved compatibility and reduced post-transplant complications, making them attractive for families with identified genetic matches. Technological advancements in HLA matching and stem cell processing further facilitate the efficiency and success of these transplants. In addition, government programs and awareness campaigns promoting family donor registries are expected to accelerate the adoption of this segment globally.

- By Application

On the basis of application, the market is segmented into regenerative therapy and drug discovery and development. The Regenerative Therapy segment dominated the market in 2025, attributed to its extensive use in treating degenerative, hematologic, and immunologic disorders. Allogeneic stem cells provide solutions for patients who cannot use their own cells, offering life-saving treatments in oncology and bone marrow transplantation. The segment’s growth is supported by ongoing clinical trials, technological improvements in cell delivery systems, and increasing investments in regenerative medicine. In addition, rising patient awareness and healthcare infrastructure improvements in developed regions contribute to the segment’s dominance.

The Drug Discovery and Development segment is expected to witness the fastest growth from 2026 to 2033, driven by the expanding use of allogeneic stem cells in preclinical and clinical research. Pharmaceutical and biotech companies are leveraging these cells to model diseases, test novel drugs, and optimize therapeutic pipelines, reducing time and cost in drug development. Advancements in high-throughput screening and stem cell engineering are also accelerating this adoption. Furthermore, collaborations between stem cell providers and drug developers are fostering innovation in this rapidly evolving segment.

- By End Users

On the basis of end users, the market is segmented into therapeutics companies, cell and tissue banks, tools and reagents companies, and service companies. The Therapeutics Companies segment dominated the market with the largest share in 2025, driven by the development and commercialization of advanced stem cell therapies. Leading biotech and pharmaceutical firms are investing heavily in clinical trials, manufacturing, and distribution of allogeneic stem cell products, fueling revenue growth in this segment. The segment also benefits from strategic collaborations with hospitals, research institutes, and contract development organizations to expand global reach.

The Cell and Tissue Banks segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising demand for reliable donor stem cell storage, cryopreservation, and matching services. These banks play a crucial role in enabling timely access to MUD and family donor transplants, supporting both clinical and research applications. Increasing establishment of regional and international stem cell registries, coupled with government and private sector initiatives, is further driving the expansion of this segment globally.

Allogeneic Stem Cells Market Regional Analysis

- North America dominated the allogeneic stem cells market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, significant R&D investments, favorable regulatory frameworks, and the presence of key industry players in cell therapy and regenerative medicine

- Patients and healthcare providers in the region increasingly prefer allogeneic stem cell therapies due to their efficacy in treating hematologic disorders, cancers, and genetic diseases, along with improved transplant success rates

- This widespread adoption is further supported by favorable regulatory frameworks, high R&D expenditure, and the presence of leading biotech and pharmaceutical companies actively developing and commercializing allogeneic stem cell products

U.S. Allogeneic Stem Cells Market Insight

The U.S. allogeneic stem cells market captured the largest revenue share of 42% in 2025 within North America, driven by the widespread adoption of stem cell therapies for hematologic, immunologic, and degenerative disorders. Patients and clinicians increasingly rely on MUD (Matched Unrelated Donor) transplants and family donor programs to treat leukemia, lymphoma, and other blood disorders. The growing preference for off-the-shelf allogeneic therapies and the expansion of stem cell registries further propels market growth. Moreover, strong investments in regenerative medicine, advanced cryopreservation techniques, and the integration of AI for patient outcome monitoring are significantly contributing to the market's expansion.

Europe Allogeneic Stem Cells Market Insight

The Europe allogeneic stem cells market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of chronic diseases and favorable healthcare policies supporting regenerative medicine. Rising patient awareness of stem cell therapies and government funding for clinical research foster adoption across hospitals, research centers, and specialized clinics. European healthcare providers are also adopting MUD transplants and off-the-shelf therapies for patients lacking family donors. The region is experiencing significant growth across therapeutic, clinical trial, and drug development applications, with stem cell therapies being incorporated into both established hospitals and research-focused medical centers.

U.K. Allogeneic Stem Cells Market Insight

The U.K. allogeneic stem cells market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the increasing demand for advanced therapies to treat hematologic disorders and chronic diseases. The rising prevalence of leukemia, aplastic anemia, and other blood-related conditions is encouraging hospitals and research institutions to adopt MUD and family donor transplant programs. In addition, the U.K.’s strong healthcare infrastructure, well-established stem cell registries, and supportive government initiatives are expected to continue stimulating market growth.

Germany Allogeneic Stem Cells Market Insight

The Germany allogeneic stem cells market is expected to expand at a considerable CAGR during the forecast period, driven by a strong focus on clinical research, technological advancements in stem cell processing, and rising awareness of regenerative medicine. German healthcare providers are increasingly adopting MUD transplants and off-the-shelf stem cell therapies to treat complex blood and immune disorders. Integration of stem cells in research, drug development, and therapeutic programs, coupled with robust regulatory support, promotes adoption in both hospitals and biotech research facilities.

Asia-Pacific Allogeneic Stem Cells Market Insight

The Asia-Pacific allogeneic stem cells market is poised to grow at the fastest CAGR of 26% during the forecast period of 2026 to 2033, driven by rising prevalence of chronic and genetic disorders in countries such as China, Japan, and India. Increasing healthcare expenditure, government initiatives supporting regenerative medicine, and the expansion of donor registries are accelerating adoption. The region’s growing inclination towards advanced therapies and increasing presence of global stem cell companies for clinical trials and manufacturing are also fueling market growth.

Japan Allogeneic Stem Cells Market Insight

The Japan allogeneic stem cells market is gaining momentum due to the country’s advanced healthcare system, high investment in regenerative medicine research, and increasing incidence of blood disorders. The adoption of off-the-shelf allogeneic therapies and integration with precision medicine programs are driving demand. Moreover, the government’s focus on promoting clinical trials, donor registries, and advanced cell therapy infrastructure is supporting growth in both therapeutic and research applications.

India Allogeneic Stem Cells Market Insight

The India allogeneic stem cells market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s rising patient population, increasing prevalence of hematologic disorders, and growing healthcare infrastructure. India is witnessing expanding adoption of both family donor and MUD transplant programs in hospitals and research centers. The government’s push toward regenerative medicine initiatives, increasing awareness among clinicians and patients, and affordable therapy options are key factors propelling the market. In addition, collaborations between domestic and global stem cell companies are strengthening clinical and commercial adoption across the country.

Allogeneic Stem Cells Market Share

The Allogeneic Stem Cells industry is primarily led by well-established companies, including:

- Fate Therapeutics (U.S.)

- Allogene Therapeutics (U.S.)

- Mesoblast Ltd. (Australia)

- Gamida Cell Ltd. (Israel)

- Pluri Inc. (Israel)

- Athersys, Inc. (U.S.)

- Cynata Therapeutics Ltd. (Australia)

- Artiva Biotherapeutics (U.S.)

- Cellular Biomedicine Group, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Lonza Group Ltd. (Switzerland)

- AllCells LLC (U.S.)

- Takara Bio Inc. (Japan)

- Escape Therapeutics, Inc. (U.S.)

- Lineage Cell Therapeutics, Inc. (U.S.)

- Stempeutics Research Pvt. Ltd. (India)

- MEDIPOST Co., Ltd. (South Korea)

- Biosolution Co., Ltd. (Japan)

- JCR Pharmaceuticals Co., Ltd. (Japan)

What are the Recent Developments in Global Allogeneic Stem Cells Market?

- In August 2025, the European Medicines Agency’s Committee for Medicinal Products for Human Use adopted a positive opinion recommending conditional marketing authorization for an allogeneic umbilical cord‑derived CD34⁺ cell therapy (dorocubicel/Zemcelpro) for adults with hematological malignancies lacking suitable donor cells, expanding regulatory recognition of allogeneic transplant innovations in the EU

- In June 2025, global clinical momentum grew as Taiwan‑based Steminent Biotherapeutics unveiled full Phase 2 clinical results for Stemchymal®, an allogeneic MSC therapy for spinocerebellar ataxia, and prepared regulatory submissions in Japan and U.S. Phase 2 IND filings, marking expansion of allogeneic applications into rare neurodegenerative disease areas

- In April 2025, Cellenkos Inc. announced that the U.S. FDA granted Orphan Drug Designation to CK0801, an allogeneic cord blood‑derived T regulatory (Treg) cell therapy for aplastic anemia, offering regulatory incentives and highlighting the emergence of novel allogeneic immune cell therapies targeting rare hematologic disorders

- In December 2024, the FDA approved Ryoncil (remestemcel‑L‑rknd), the first allogeneic bone marrow‑derived mesenchymal stromal cell (MSC) therapy for pediatric steroid‑refractory acute graft‑versus‑host disease (SR‑aGVHD), representing the first U.S. MSC therapy approval and a major advancement in donor‑derived allogeneic treatments

- In April 2023, the U.S. Food and Drug Administration (FDA) approved Omisirge (omidubicel‑onlv), a modified allogeneic cord blood‑based cell therapy, to speed neutrophil recovery and reduce infection risk after stem cell transplantation in adults and pediatric patients with blood cancers, marking a significant regulatory milestone for allogeneic stem cell therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.