Global Anaplastic Astrocytoma Market

Market Size in USD Billion

USD

1.23 Billion

USD

1.67 Billion

2025

2033

USD

1.23 Billion

USD

1.67 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.23 Billion | |

| USD 1.67 Billion | |

| % | |

|

Anaplastic Astrocytoma Market Size

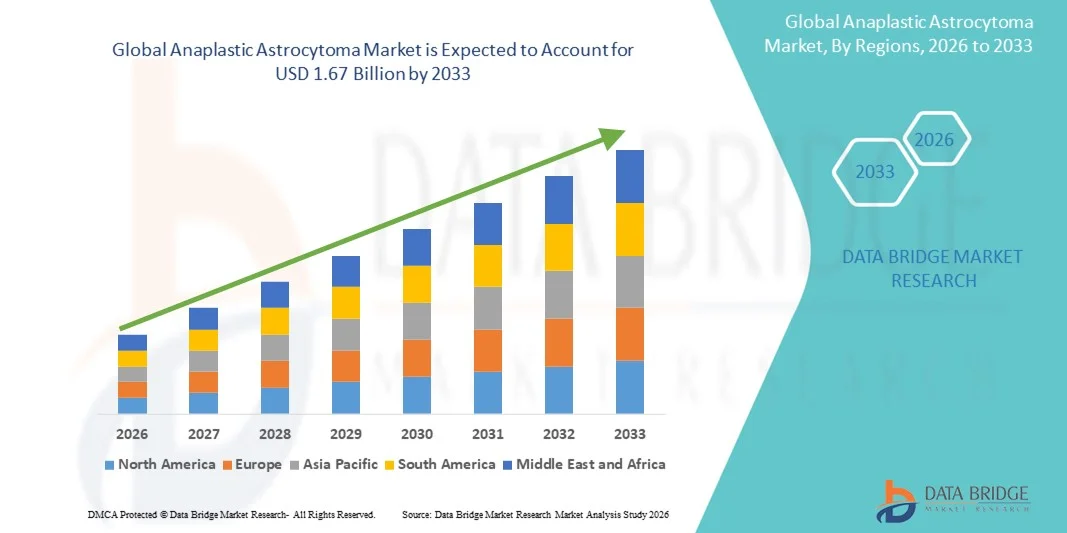

- The global Anaplastic Astrocytoma market size was valued at USD 1.23 billion in 2025 and is expected to reach USD 1.67 billion by 2033, at a CAGR of 3.9% during the forecast period

- The market growth is largely fueled by rising incidence of brain tumors, advancements in diagnostic techniques, and increasing adoption of targeted therapies and precision medicine in oncology, leading to improved patient outcomes and better disease management

- Furthermore, growing public awareness, supportive healthcare policies, expansion of oncology infrastructure, and ongoing clinical trials for novel therapies are establishing effective treatment options as the modern standard of care for Anaplastic Astrocytoma. These converging factors are accelerating the uptake of advanced therapies, thereby significantly boosting the industry’s growth

Anaplastic Astrocytoma Market Analysis

- Anaplastic Astrocytoma, an aggressive brain tumor, represents a significant challenge in neuro-oncology due to its rapid progression and complexity in treatment. Advanced diagnostic methods, including MRI, CT scan, and biopsy, are increasingly essential for accurate detection and personalized therapy planning

- The escalating demand for Anaplastic Astrocytoma treatments is primarily fueled by rising prevalence of brain tumors, growing investments in drug development, and increasing adoption of targeted therapeutic approaches such as Temodar, Procarbazine, and Temozolomide to improve patient outcomes

- North America dominated the Anaplastic Astrocytoma market with the largest revenue share of 40.2% in 2025, driven by advanced healthcare infrastructure, high R&D expenditure, early adoption of innovative therapies, and a strong presence of key industry players, with the U.S. leading in clinical trials and approvals for novel therapies

- Asia-Pacific is expected to be the fastest-growing region in the Anaplastic Astrocytoma market during the forecast period due to improving healthcare infrastructure, increasing awareness of brain cancer, and rising access to advanced diagnostics and treatment options

- Surgery segment dominated the Anaplastic Astrocytoma market with a market share of 42.9% in 2025, driven by its critical role in tumor removal, improved survival rates, and widespread adoption as the first-line treatment, often followed by radiation therapy and chemotherapy for enhanced efficacy

Report Scope and Anaplastic Astrocytoma Market Segmentation

|

Attributes |

Anaplastic Astrocytoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Anaplastic Astrocytoma Market Trends

Advancements in Targeted Therapies and Precision Medicine

- A significant and accelerating trend in the global Anaplastic Astrocytoma market is the increasing adoption of targeted therapies, including Temozolomide and Procarbazine, and precision medicine approaches based on molecular profiling, improving personalized treatment outcomes

- For instance, the use of IDH-mutant specific therapies allows clinicians to tailor treatment protocols based on tumor genetic profiles, enhancing effectiveness while minimizing side effects. Similarly, combination therapies integrating surgery, radiation, and chemotherapy are increasingly being optimized using patient-specific molecular data

- Targeted therapy integration with precision diagnostics enables features such as predicting patient response, monitoring tumor progression, and adjusting treatment regimens dynamically. For instance, molecular-guided treatment plans have improved survival rates in several clinical trials and can alert clinicians to early signs of treatment resistance

- The seamless integration of molecular diagnostics with therapeutic interventions facilitates centralized treatment planning, allowing clinicians to manage surgery, radiation, and drug administration in a coordinated and data-driven manner, improving patient care

- This trend toward more precise, personalized, and integrated treatment approaches is fundamentally reshaping patient expectations and standards of care. Consequently, companies such as Novocure and Celgene are developing precision medicine-based therapies with molecular profiling guidance and optimized treatment sequencing

- The demand for advanced targeted and personalized therapies is growing rapidly across hospitals and clinics, as patients increasingly seek optimized treatment efficacy and reduced systemic toxicity

Anaplastic Astrocytoma Market Dynamics

Driver

Increasing Incidence of Brain Tumors and Rising Awareness

- The growing prevalence of Anaplastic Astrocytoma globally, coupled with rising awareness of brain cancer symptoms and treatment options, is a significant driver of market growth

- For instance, in March 2025, Novocure announced expansion of its TTFields therapy clinical trials in glioma patients, aiming to improve adoption and accessibility of non-invasive treatment modalities. Such initiatives by key companies are expected to drive market growth in the forecast period

- As patients and healthcare providers become more aware of tumor risks and advanced treatment options, therapies such as Temozolomide and combination regimens are increasingly preferred over conventional chemotherapy alone

- Furthermore, expansion of oncology infrastructure, early diagnosis programs, and increasing availability of advanced imaging and molecular testing are making targeted treatment approaches more feasible and widely adopted

- The convenience of integrating surgery, radiation, and personalized chemotherapy regimens, along with clinical guidance through molecular diagnostics, is propelling adoption in both hospital and clinic settings. The trend toward multidisciplinary care and increased treatment accessibility further contributes to market growth

- For instance, growing investments in research and development of IDH-wildtype targeted drugs are enabling more precise therapeutic options, attracting increased adoption among leading cancer centers

- Increasing public and physician awareness campaigns about early detection, symptom monitoring, and treatment options are driving higher patient enrollment in clinical trials and expanding overall market uptake

Restraint/Challenge

High Treatment Costs and Limited Access in Developing Regions

- The relatively high cost of advanced therapies, including targeted drugs and molecular diagnostics, poses a significant challenge to broader market adoption, particularly in price-sensitive regions

- For instance, the pricing of Temozolomide-based regimens and combination therapy protocols can limit patient access in developing countries, restricting market penetration and uptake

- Addressing affordability challenges through insurance coverage, patient assistance programs, and cost-effective treatment alternatives is crucial for expanding access and adoption. Companies such as Celgene and Novocure emphasize financial support programs and generic options to mitigate these barriers

- In addition, limited access to advanced neuro-oncology facilities and trained specialists in certain regions can hinder timely diagnosis and treatment initiation, affecting overall market growth

- Overcoming these challenges through improved healthcare infrastructure, expanded clinical training, and financial assistance programs will be vital for sustained growth and broader patient access globally

- For instance, the lack of widespread availability of molecular diagnostics in rural regions delays early intervention, which can negatively impact treatment efficacy and outcomes

- Regulatory hurdles and prolonged clinical trial approvals for novel therapies may also slow the introduction of innovative treatment options, affecting market expansion and limiting patient access to next-generation therapies

Anaplastic Astrocytoma Market Scope

The market is segmented on the basis of disease type, drug type, treatment, diagnosis, molecule development phase, symptoms, end-users, and distribution channel.

- By Disease Type

On the basis of disease type, the Anaplastic Astrocytoma market is segmented into IDH-mutant, IDH-wildtype, and others. The IDH-wildtype segment dominated the market in 2025 due to its higher prevalence among adult patients and association with aggressive tumor progression. Patients with IDH-wildtype tumors often require combination therapy approaches, including surgery, radiation, and targeted chemotherapy, contributing to increased treatment volume and market revenue. In addition, the availability of targeted drugs and ongoing clinical trials focusing on this subtype is further reinforcing its dominance. Healthcare providers prioritize IDH-wildtype diagnosis to optimize treatment planning and improve patient survival outcomes. The segment also benefits from growing research investments aimed at developing novel targeted therapies specific to this tumor type.

The IDH-mutant segment is anticipated to witness the fastest growth from 2026 to 2033, driven by increasing adoption of personalized treatment protocols based on molecular profiling. Early detection and targeted therapy approaches, such as IDH-inhibitor drugs, are enabling more effective management of this subtype. Rising awareness among clinicians about prognostic advantages of IDH-mutant tumors is further accelerating adoption. Advances in biomarker-based diagnostics and companion therapeutics are increasing patient enrollment in clinical trials. This segment also benefits from improved patient outcomes and reduced side effects due to precision therapies. Overall, the IDH-mutant segment is rapidly gaining traction in developed and emerging oncology markets.

- By Drug Type

On the basis of drug type, the market is segmented into matulane, temodar, procarbazine, temozolomide, and others. The Temozolomide segment dominated the market in 2025 due to its widespread adoption as a first-line chemotherapy agent for Anaplastic Astrocytoma. It is often used in combination with radiotherapy, enhancing overall treatment efficacy and improving survival rates. Temozolomide’s oral formulation offers ease of administration and better patient compliance compared with intravenous therapies. Its established clinical profile and inclusion in global treatment guidelines further contribute to its dominance. Key pharmaceutical companies continue to invest in extended-release formulations and combination regimens, maintaining high demand. Moreover, its compatibility with both adult and pediatric oncology protocols reinforces consistent revenue generation.

The Procarbazine segment is expected to witness the fastest growth from 2026 to 2033, driven by its increasing inclusion in multi-drug regimens and combination therapy protocols. Clinical studies have highlighted its efficacy when combined with other alkylating agents, enhancing tumor response rates. Emerging generic formulations and expanded accessibility are also contributing to adoption in developing markets. Rising physician preference for combination chemotherapy regimens that include Procarbazine is accelerating its uptake. In addition, ongoing research to optimize dosage schedules and reduce adverse effects is supporting market growth.

- By Treatment

On the basis of treatment, the market is segmented into surgery, radiation therapy, and chemotherapy. The Surgery segment dominated the market in 2025 with a market share of 42.9%, due to its essential role in tumor removal and as a first-line intervention. Surgical resection is often combined with radiotherapy and chemotherapy for improved survival outcomes. Availability of advanced neurosurgical techniques, such as intraoperative MRI and fluorescence-guided surgery, has improved precision and reduced complications. Hospitals and specialized oncology centers prioritize surgical intervention to achieve maximal safe resection. The segment also benefits from increasing investments in advanced neuro-oncology facilities and skilled neurosurgeons. Furthermore, post-surgical adjuvant therapies increase overall treatment adoption and drive market revenue.

The Radiation Therapy segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by the adoption of advanced techniques such as stereotactic radiosurgery (SRS) and intensity-modulated radiotherapy (IMRT). These technologies enable precise targeting of tumor tissue while minimizing damage to surrounding healthy tissue. Rising use in combination with chemotherapy and targeted therapies is driving adoption in both developed and emerging markets. Increased awareness of radiation therapy’s efficacy in improving survival outcomes supports its rapid uptake. Expanding availability of specialized radiotherapy centers further accelerates segment growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into MRI, CT scan, X-ray, and Biopsy. The MRI segment dominated the market in 2025 due to its superior imaging resolution and ability to detect tumor size, location, and progression. MRI is critical for surgical planning and monitoring treatment response over time. The non-invasive nature and repeated usability of MRI make it preferred for both initial diagnosis and follow-up. High adoption of advanced MRI protocols, including functional MRI and diffusion-weighted imaging, enhances diagnostic accuracy. Hospitals and clinics continue to invest in high-field MRI scanners to meet growing demand. MRI’s integration with molecular imaging and AI-assisted tools is further reinforcing its dominant position.

The Biopsy segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing use of molecular and genetic profiling for personalized treatment planning. Biopsy provides tissue samples critical for IDH mutation testing, MGMT promoter methylation analysis, and other biomarkers. Growing emphasis on precision medicine and targeted therapy selection is accelerating biopsy adoption. Minimally invasive biopsy techniques and robotic-assisted procedures are increasing patient acceptance. Rising awareness among oncologists regarding the prognostic value of biopsy results further boosts its usage.

- By Molecule Development Phase

On the basis of molecule development phase, the market is segmented into pre-registration phase and clinical trial phase. The Clinical Trial Phase segment dominated the market in 2025 as most innovative therapies for Anaplastic Astrocytoma are currently undergoing trials to establish efficacy and safety profiles. Leading pharmaceutical companies and research institutions are conducting multiple Phase II and III trials globally. Growth in trial activities reflects high investment in next-generation targeted therapies and combination regimens. Clinical trials also provide early access to therapies for eligible patients, further increasing market engagement. Collaboration between hospitals and biotech firms drives the scale and success of trials. Strong pipeline development continues to sustain dominance of this segment.

The Pre-Registration Phase segment is expected to witness the fastest growth from 2026 to 2033, driven by an increasing number of novel compounds entering the development pipeline. Rising focus on rare tumor subtypes and unmet medical needs is prompting accelerated development strategies. Regulatory incentives and orphan drug designations in multiple regions are encouraging innovation. Early-stage development of IDH-targeted inhibitors and immune-oncology agents is expanding. Growing partnerships between biotech firms and academic centers support rapid molecule advancement.

- By Symptoms

On the basis of symptoms, the market is segmented into headache, lethargy, seizures, vision problems, memory loss, behavioral problems, and others. The Headache segment dominated the market in 2025 as it is the most common presenting symptom, prompting patients to seek medical consultation and early diagnostic testing. Early detection due to headache awareness drives higher diagnostic and treatment adoption. Healthcare providers prioritize symptom-based screening, increasing use of imaging and biopsy. Patient education campaigns and routine neurological check-ups contribute to consistent demand. Symptom-focused market initiatives support high revenue generation. Headache severity often correlates with tumor progression, reinforcing the need for rapid intervention.

The Seizures segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by rising awareness of seizure management and monitoring. Seizures are often an early indicator of tumor activity, driving rapid diagnostic evaluation. Advances in anti-epileptic therapies integrated with oncology care further enhance treatment adoption. Growing patient awareness regarding seizure management protocols accelerates hospital visits. Continuous EEG monitoring and AI-assisted seizure prediction technologies support clinical decision-making. Early seizure intervention improves survival outcomes, promoting adoption of integrated care approaches.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The Hospital segment dominated the market in 2025 due to the availability of multidisciplinary neuro-oncology teams, advanced imaging and surgical facilities, and comprehensive treatment options. Hospitals provide integrated care, combining surgery, chemotherapy, and radiotherapy under one roof. Large patient volumes and higher treatment complexity favor hospital adoption. Specialized cancer centers within hospitals support clinical trials and novel therapy administration. Revenue generation is higher in hospitals due to advanced procedures and multi-modality treatments. Hospitals continue to drive market penetration in developed and emerging regions.

The Clinic segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing establishment of outpatient oncology clinics and localized treatment centers. Clinics provide convenient access to follow-up care, minor procedures, and targeted therapy administration. Rising awareness of outpatient management benefits supports adoption. Integration of telemedicine for monitoring and treatment guidance further accelerates growth. Clinics expand patient access in semi-urban and rural areas. Flexible treatment schedules and personalized care contribute to the rising adoption of clinic-based services.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market in 2025 due to direct access to in-patient treatment protocols, chemotherapy administration, and specialty drugs. Hospitals control drug dispensing for complex therapies, ensuring compliance and safety. Availability of high-cost targeted drugs and chemotherapy agents at hospital pharmacies supports dominance. Hospitals also manage patient follow-up and combination therapy coordination. Market leaders prioritize hospital pharmacy partnerships for early therapy adoption. Comprehensive distribution in hospitals ensures continuous supply of essential medications.

The Online Pharmacy segment is anticipated to witness the fastest growth from 2026 to 2033, driven by rising e-commerce adoption, convenience, and home delivery of specialty drugs. Patients increasingly prefer online platforms for prescription refills and remote access to targeted therapies. Integration with telemedicine and electronic prescription systems facilitates growth. Online pharmacies expand market reach to remote and underserved areas. Promotions, discounts, and subscription models boost adoption. Regulatory frameworks supporting safe online drug distribution enhance credibility and trust.

Anaplastic Astrocytoma Market Regional Analysis

- North America dominated the Anaplastic Astrocytoma market with the largest revenue share of 40.2% in 2025, driven by advanced healthcare infrastructure, high R&D expenditure, early adoption of innovative therapies, and a strong presence of key industry players, with the U.S. leading in clinical trials and approvals for novel therapies

- Patients and healthcare providers in the region prioritize early detection, molecular profiling, and comprehensive treatment protocols, including surgery, radiation, and chemotherapy, which significantly contribute to market revenue

- This dominance is further supported by a strong presence of key pharmaceutical and biotechnology companies, extensive clinical trial activity, and growing public awareness of brain cancer, establishing North America as a leading market for innovative Anaplastic Astrocytoma therapies in both hospital and clinic settings

U.S. Anaplastic Astrocytoma Market Insight

The U.S. Anaplastic Astrocytoma market captured the largest revenue share of 82% in 2025 within North America, fueled by advanced healthcare infrastructure, high adoption of targeted therapies, and widespread use of precision medicine. Patients and clinicians increasingly prioritize early detection, molecular profiling, and integrated treatment protocols including surgery, radiation, and chemotherapy. The growing number of clinical trials and R&D investment in novel therapies further propels the market. Moreover, rising public awareness of brain tumors, improved insurance coverage, and access to specialized neuro-oncology centers significantly contribute to market expansion.

Europe Anaplastic Astrocytoma Market Insight

The Europe Anaplastic Astrocytoma market is projected to expand at a substantial CAGR during the forecast period, primarily driven by government initiatives for cancer research, increasing investment in oncology infrastructure, and growing demand for advanced diagnostics and targeted therapies. Rising urbanization, coupled with a higher prevalence of brain tumors, fosters the adoption of precision medicine and combination treatment protocols. Patients are also increasingly seeking minimally invasive surgical techniques and improved post-operative care, boosting treatment uptake across hospitals and clinics.

U.K. Anaplastic Astrocytoma Market Insight

The U.K. Anaplastic Astrocytoma market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of early diagnosis, preference for targeted therapy, and integration of molecular diagnostics in treatment planning. In addition, rising incidence of aggressive brain tumors and a strong healthcare system encourage both hospitals and clinics to adopt advanced treatment regimens. The U.K.’s emphasis on clinical trial participation and patient access programs is expected to continue stimulating market growth.

Germany Anaplastic Astrocytoma Market Insight

The Germany Anaplastic Astrocytoma market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of neuro-oncology therapies, widespread availability of advanced diagnostics such as MRI and biopsy, and rising adoption of personalized treatment protocols. Germany’s well-developed healthcare infrastructure and focus on innovative oncology solutions support the market. Integration of targeted therapies and combination treatment approaches in hospitals is becoming increasingly prevalent, aligning with local clinical guidelines and patient care standards.

Asia-Pacific Anaplastic Astrocytoma Market Insight

The Asia-Pacific Anaplastic Astrocytoma market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by increasing healthcare expenditure, rising incidence of brain tumors, and improving access to advanced diagnostics and treatments in countries such as China, Japan, and India. Government initiatives supporting cancer awareness, digital health, and specialized neuro-oncology centers are driving adoption. Furthermore, growing patient awareness, expansion of private hospitals, and availability of affordable targeted therapies are expanding treatment accessibility across the region.

Japan Anaplastic Astrocytoma Market Insight

The Japan market is gaining momentum due to advanced healthcare infrastructure, high public awareness of neurological disorders, and rapid adoption of precision medicine. The prevalence of targeted therapies and combination treatment protocols is increasing, supported by well-established hospital networks. Japan’s aging population is such asly to drive demand for easier-to-administer and less invasive treatment options. Moreover, integration of molecular diagnostics with clinical care enhances early detection and personalized therapy planning.

India Anaplastic Astrocytoma Market Insight

The India Anaplastic Astrocytoma market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising healthcare access, increasing incidence of brain tumors, and growing awareness of advanced oncology treatments. Expanding urban centers, rising disposable incomes, and the development of specialized cancer hospitals are key growth factors. The push towards affordable targeted therapies and participation in clinical trials, alongside growing public awareness campaigns, is further propelling market adoption across residential, urban, and semi-urban areas.

Anaplastic Astrocytoma Market Share

The Anaplastic Astrocytoma industry is primarily led by well-established companies, including:

- Merck & Co., Inc., (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Amgen Inc. (U.S.)

- Novocure (Switzerland)

- Sanofi (France)

- GSK plc (U.K.)

- AbbVie Inc. (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Ipsen (France)

- Jazz Pharmaceuticals, Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- BeiGene (China)

What are the Recent Developments in Global Anaplastic Astrocytoma Market?

- In August 2025, researchers presented a new deep-learning model called FoundBioNet — a foundation-based model that analyzes multi-parametric MRI scans to noninvasively predict mutation status in gliomas. On a large, multi-center cohort (1,705 patients), FoundBioNet achieved ~ 90.6% AUC in IDH-mutation prediction a big step toward “MRI-only, non-invasive molecular diagnosis,” which could reduce dependence on biopsy for astrocytoma and other gliomas

- In August 2024, the U.S. FDA approved Vorasidenib (Voranigo) for adult and pediatric patients (≥12 years) with grade-2 astrocytoma or oligodendroglioma harboring susceptible IDH1/IDH2 mutations. This approval is historic because it represents the first-ever targeted systemic therapy approved for low-grade gliomas. Although approved for grade-2 tumors, it also impacts the broader astrocytoma treatment landscape by validating IDH inhibition as a clinically meaningful approach

- In June 2023, the Phase III INDIGO trial data were presented at the ASCO Annual Meeting, providing significant clinical progress for IDH-mutant gliomas, including early-stage astrocytomas. The study demonstrated that Vorasidenib, an oral dual IDH1/IDH2 inhibitor, dramatically improved progression-free survival and delayed the need for intensive treatments such as radiation and chemotherapy

- In March 2023, research teams published findings on DeepGlioma, an ultra-fast artificial-intelligence–based molecular diagnostic tool designed for diffuse gliomas, including anaplastic astrocytoma. The system uses rapid optical imaging of tumor tissue combined with deep-learning algorithms to classify key molecular markers such as IDH mutation status in under 90 seconds. This eliminates long waits associated with conventional genetic testing, which often takes several days

- In August 2022, the American Society for Radiation Oncology (ASTRO) published its first-ever guideline for treatment of lower-grade gliomas (including IDH-mutant astrocytomas) under the redefined classification by World Health Organization (WHO) 2021 criteria. The guideline lays out evidence-based recommendations for when to use radiation therapy (dose, timing, technique such as intensity-modulated RT), and when close surveillance may be appropriate

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.