Global Anca Vasculitis Treatment Market

Market Size in USD Million

USD

339.50 Million

USD

537.04 Million

2024

2032

USD

339.50 Million

USD

537.04 Million

2024

2032

| 2025 - 2032 | |

| USD 339.50 Million | |

| USD 537.04 Million | |

| % | |

|

ANCA Vasculitis Treatment Market Size

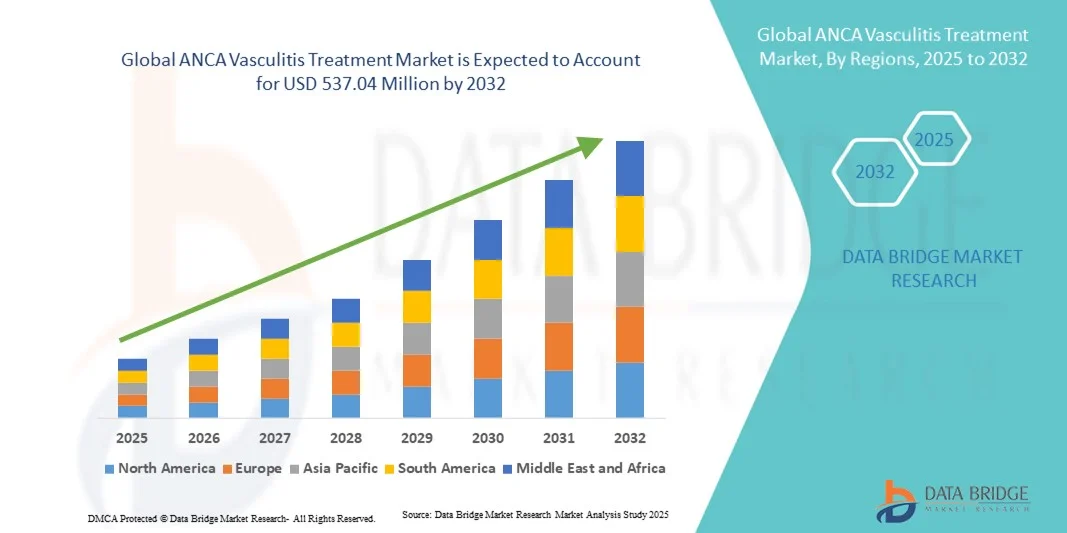

- The global ANCA vasculitis treatment market size was valued at USD 339.50 million in 2024 and is expected to reach USD 537.04 million by 2032, at a CAGR of 5.90% during the forecast period

- The market growth is largely fueled by advancements in targeted therapies, increasing awareness among healthcare professionals and patients, and the rising prevalence of autoimmune diseases, leading to improved disease management and patient outcomes

- Furthermore, the introduction of novel biologic therapies and the growing demand for effective, personalized treatment options for ANCA vasculitis is establishing targeted therapies as the preferred standard of care. These converging factors are accelerating the uptake of ANCA vasculitis treatments, thereby significantly boosting the industry's growth

ANCA Vasculitis Treatment Market Analysis

- ANCA vasculitis treatments, including induction therapy, maintenance therapy, and other supportive treatments, are increasingly vital for managing this rare autoimmune disorder affecting small and medium blood vessels, due to their ability to reduce inflammation, prevent organ damage, and improve patient quality of life in both newly diagnosed and relapsing cases

- The escalating demand for ANCA vasculitis treatments is primarily fueled by the rising prevalence of autoimmune diseases, growing awareness among healthcare professionals and patients, and the increasing availability of advanced diagnostic methods and targeted therapies that offer improved efficacy and safety profiles

- North America dominated the ANCA vasculitis treatment market with the largest revenue share of 42.8% in 2024, driven by early adoption of advanced biologics, high healthcare expenditure, robust R&D pipelines, and the presence of leading pharmaceutical companies actively developing and commercializing novel therapies

- Asia-Pacific is expected to be the fastest growing region in the ANCA vasculitis treatment market during the forecast period due to increasing disease diagnosis rates, rising healthcare spending, growing awareness, and expanding access to innovative treatment options across emerging economies

- Microscopic polyangiitis segment dominated the ANCA vasculitis treatment market with a market share of 45% in 2024, driven by its relatively higher prevalence among the disease types and the increasing demand for effective and targeted therapeutic interventions

Report Scope and ANCA Vasculitis Treatment Market Segmentation

|

Attributes |

ANCA Vasculitis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

ANCA Vasculitis Treatment Market Trends

Advancements in Targeted Biologics and Personalized Therapy

- A significant and accelerating trend in the global ANCA vasculitis treatment market is the development and adoption of targeted biologic therapies and personalized treatment regimens, which improve remission rates and minimize side effects for patients with varied disease severity

- For instance, TAVNEOS and NUCALA therapies have demonstrated efficacy in inducing remission and maintaining disease control in patients with refractory or relapsing ANCA vasculitis, supporting the shift toward personalized medicine

- Biologic and targeted therapies enable physicians to tailor treatment based on disease type, severity, and patient response, reducing long-term organ damage and enhancing quality of life. For instance, Clinical studies have shown improved renal outcomes in microscopic polyangiitis patients receiving biologics versus conventional immunosuppressants

- The integration of novel therapies with ongoing patient monitoring, predictive diagnostics, and digital health platforms allows for optimized treatment schedules and early detection of relapses, creating a more proactive management approach

- This trend toward precision therapy is fundamentally reshaping treatment protocols, driving pharmaceutical companies such as GlaxoSmithKline and Horizon Therapeutics to expand their biologic portfolios with therapies offering targeted immunomodulation

- The demand for more effective, patient-specific treatment strategies is growing rapidly across both hospitals and specialty clinics, as healthcare providers increasingly prioritize improved outcomes and reduced side effects

ANCA Vasculitis Treatment Market Dynamics

Driver

Rising Prevalence of Autoimmune Diseases and Awareness

- The increasing prevalence of ANCA vasculitis and other autoimmune disorders, coupled with rising awareness among healthcare professionals and patients, is a significant driver for the heightened demand for effective treatment options

- For instance, In 2024, Horizon Therapeutics expanded its ANCA vasculitis therapy portfolio with patient support programs to increase disease awareness and access to care, driving treatment adoption

- As more patients are diagnosed early, timely initiation of targeted therapies reduces complications and improves long-term outcomes, creating a strong demand for induction and maintenance treatments

- Furthermore, the growing adoption of specialized diagnostic tools such as blood tests, biopsy, and imaging techniques supports accurate disease identification, encouraging use of targeted treatment protocols

- The convenience of personalized treatment regimens, coupled with improved efficacy and tolerability of biologics, is propelling the uptake of ANCA vasculitis therapies in both hospitals and specialty clinics. The trend toward comprehensive patient management and monitoring further contributes to market growth

Restraint/Challenge

High Treatment Costs and Limited Accessibility in Emerging Markets

- The high cost of biologic therapies and immunosuppressants, along with limited insurance coverage in many regions, poses a significant challenge to broader market penetration

- For instance, Despite the efficacy of TAVNEOS, its premium pricing limits accessibility for patients in emerging Asia-Pacific countries, restricting treatment adoption

- Addressing affordability through patient assistance programs, generic biologics, and government reimbursement initiatives is crucial to expanding access and encouraging adoption

- Additionally, the complex administration requirements of some therapies, such as parenteral delivery and hospital visits, can reduce patient adherence and limit market growth in resource-constrained areas

- While ongoing initiatives aim to improve treatment affordability and accessibility, the perceived high cost and logistical challenges may still hinder widespread adoption, especially in low- and middle-income regions

- Overcoming these challenges through improved healthcare infrastructure, cost-effective therapy models, and awareness campaigns will be vital for sustained growth of the ANCA vasculitis treatment market

ANCA Vasculitis Treatment Market Scope

The market is segmented on the basis of type, diagnosis, treatment type, route of administration, end user, and distribution channel.

- By Type

On the basis of type, the ANCA vasculitis treatment market is segmented into Microscopic Polyangiitis (MPA), Granulomatosis with Polyangiitis (GPA), and Eosinophilic Granulomatosis with Polyangiitis (EGPA). The Microscopic Polyangiitis (MPA) segment dominated the market with the largest revenue share of 45% in 2024, driven by its relatively higher prevalence and the demand for effective therapeutic management to prevent kidney and organ damage. Physicians prioritize early and intensive treatment for MPA due to its rapid progression and severe complications. The segment also benefits from the availability of biologics and immunosuppressants that specifically target MPA, improving patient outcomes. Strong awareness campaigns and established treatment protocols in North America and Europe further support market dominance. Additionally, MPA patients often require ongoing maintenance therapy, creating consistent demand for treatments. The robust pipeline of novel therapies targeting MPA contributes to sustaining its leadership position in the market.

The Eosinophilic Granulomatosis with Polyangiitis (EGPA) segment is anticipated to witness the fastest growth at a CAGR of 6.2% from 2025 to 2032, fueled by increasing diagnosis rates and rising awareness among physicians of the need for early intervention. EGPA management often involves biologics such as mepolizumab, which have shown high efficacy in reducing eosinophilic inflammation. The growing adoption of personalized medicine approaches, tailored to patient symptom severity, is accelerating EGPA treatment uptake. Moreover, the emergence of new therapies in clinical trials targeting rare ANCA vasculitis types supports this growth. Expanding healthcare access in emerging markets, particularly Asia-Pacific, further contributes to the segment’s rapid adoption. Patients increasingly prefer advanced therapies that reduce corticosteroid dependence, enhancing the popularity of EGPA-specific treatments.

- By Diagnosis

On the basis of diagnosis, the ANCA vasculitis treatment market is segmented into blood test, urine test, X-ray, CT scan, bronchoscopy, and biopsy. The Blood Test segment dominated the market in 2024, accounting for the largest share due to its critical role in detecting ANCA antibodies and monitoring disease activity. Blood tests are minimally invasive, cost-effective, and widely accessible, making them a preferred first-line diagnostic tool. High sensitivity and specificity allow early detection, enabling timely initiation of treatment and better patient prognosis. Clinicians often combine blood test results with other diagnostic tools for a comprehensive assessment. The increasing adoption of advanced blood assay kits has further strengthened this segment. Blood tests also support long-term disease monitoring, boosting repeat usage and consistent market demand.

The Biopsy segment is expected to witness the fastest growth from 2025 to 2032 due to its ability to provide definitive diagnosis by assessing tissue involvement, particularly in renal and pulmonary complications. Biopsy procedures guide personalized therapy decisions, helping physicians select appropriate induction and maintenance treatments. The rising prevalence of organ-specific manifestations of ANCA vasculitis increases biopsy adoption. Technological improvements in less invasive biopsy techniques are driving patient acceptance. Growing physician awareness and guideline recommendations for histopathological confirmation also support this segment’s expansion. Emerging markets are increasingly investing in diagnostic infrastructure, further contributing to growth.

- By Treatment Type

On the basis of treatment type, the ANCA vasculitis treatment market is segmented into induction therapy, maintenance therapy, and other treatments. The Induction Therapy segment dominated the market in 2024, capturing the largest revenue share, due to its critical role in achieving rapid remission in newly diagnosed or relapsing patients. Induction regimens often involve potent biologics or high-dose immunosuppressants to control inflammation quickly and prevent organ damage. Clinicians prioritize induction therapy to reduce morbidity and long-term complications. The strong pipeline of new induction therapies contributes to sustained demand. Increased adoption of combination therapy approaches also supports this segment’s market dominance. Healthcare providers emphasize induction therapy adherence, creating consistent market opportunities.

The Maintenance Therapy segment is expected to witness the fastest growth from 2025 to 2032, driven by the need for long-term disease control to prevent relapse. Maintenance treatments often involve lower-dose immunosuppressants or biologics administered over extended periods, supporting sustained remission. Rising patient awareness and adherence programs enhance uptake. The trend toward personalized maintenance regimens tailored to disease type and severity contributes to growth. Expansion of outpatient care facilities and specialty clinics facilitates long-term treatment administration. Advances in oral and parenteral formulations improve patient compliance and convenience, further accelerating the segment.

- By Route of Administration

On the basis of route of administration, the ANCA vasculitis treatment market is segmented into oral and parenteral. The Parenteral segment dominated the market with the largest share in 2024, owing to its critical role in delivering biologics and high-potency therapies directly into systemic circulation for rapid efficacy. Hospital and clinic settings often prefer parenteral administration for controlled dosing and monitoring. The segment benefits from consistent demand due to repeated dosing schedules for induction and maintenance therapy. Parenteral formulations also support combination therapies that enhance treatment outcomes. Clinician preference for parenteral delivery in severe or relapsing cases further drives adoption. The development of prefilled syringes and infusion devices enhances ease of use, supporting market leadership.

The Oral segment is anticipated to witness the fastest growth from 2025 to 2032 due to increasing patient preference for convenient self-administration and reduced hospital visits. Oral therapies are particularly appealing for long-term maintenance therapy, improving adherence. Growing availability of effective oral immunosuppressants supports market expansion. Emerging markets are adopting oral treatment options to reduce healthcare infrastructure burden. Improved patient education and monitoring technologies further enhance adoption. Pharmaceutical companies are investing in oral formulations to meet the rising demand for at-home therapy.

- By End User

On the basis of end user, the ANCA vasculitis treatment market is segmented into government, hospitals, medical clinics, and others. The Hospitals segment dominated the market in 2024, capturing the largest revenue share due to the concentration of advanced diagnostic facilities, infusion centers, and specialist physicians capable of managing complex ANCA vasculitis cases. Hospitals serve as primary points for induction therapy and severe case management. The segment benefits from strong reimbursement support and established treatment protocols. Hospitals often lead patient monitoring and follow-up programs, ensuring adherence to therapy. High patient inflow and access to multiple treatment types reinforce hospital dominance. The presence of specialty wards and multidisciplinary teams further supports this segment.

The Medical Clinics segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing decentralization of care and rising outpatient treatment adoption. Clinics provide convenient long-term maintenance therapy and routine monitoring, reducing patient burden. Expansion of specialty rheumatology and nephrology clinics supports segment growth. Telemedicine integration enhances patient access to clinic-based care. Patient preference for local and accessible care is accelerating adoption. Government initiatives promoting clinic-based disease management further fuel this segment’s growth.

- By Distribution Channel

On the basis of distribution channel, the ANCA vasculitis treatment market is segmented into retail store, pharmacy, and E-commerce. The Pharmacy segment dominated the market in 2024 due to its established presence, regulatory compliance, and role as the primary channel for prescription therapies including biologics and immunosuppressants. Pharmacies ensure consistent supply and adherence support. Strong partnerships with hospitals and clinics further enhance the segment’s reach. Patient education and counseling services provided at pharmacies improve therapy compliance. Centralized pharmacy networks help manage high-demand therapies efficiently. Trusted pharmacy networks maintain market confidence and reliability.

The E-Commerce segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing digital adoption, online prescription fulfillment, and the convenience of home delivery for patients on long-term maintenance therapy. Online platforms offer discreet and timely access to medications. Integration with digital health platforms supports prescription management and adherence tracking. Growing awareness among patients about online options accelerates adoption. Expansion of telemedicine services further complements e-commerce distribution. Companies investing in secure online pharmacy platforms benefit from this growing trend.

ANCA Vasculitis Treatment Market Regional Analysis

- North America dominated the ANCA vasculitis treatment market with the largest revenue share of 42.8% in 2024, driven by early adoption of advanced biologics, high healthcare expenditure, robust R&D pipelines, and the presence of leading pharmaceutical companies actively developing and commercializing novel therapies

- Patients and healthcare providers in the region highly value the availability of targeted therapies, personalized treatment protocols, and comprehensive patient support programs, which improve treatment outcomes and quality of life

- This widespread adoption is further supported by strong R&D pipelines, active clinical trials, regulatory support for innovative therapies, and growing awareness of autoimmune diseases, establishing North America as a leading market for ANCA vasculitis treatments in both hospitals and specialty clinics

U.S. ANCA Vasculitis Treatment Market Insight

The U.S. ANCA vasculitis treatment market captured the largest revenue share of 81% in 2024 within North America, fueled by early adoption of advanced biologics and widespread availability of specialized healthcare facilities. Patients and clinicians increasingly prioritize targeted therapies and personalized treatment plans to improve remission rates and prevent organ damage. The growing preference for induction and maintenance therapy programs, combined with strong patient support initiatives, further propels the market. Moreover, integration of advanced diagnostics such as blood tests, biopsy, and imaging supports early disease detection and optimized therapy management, significantly contributing to market expansion.

Europe ANCA Vasculitis Treatment Market Insight

The Europe ANCA vasculitis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established healthcare infrastructure, increasing diagnosis rates, and stringent regulatory frameworks. Rising awareness of autoimmune diseases and adoption of biologics are fostering the use of targeted therapies. European patients and healthcare providers value improved treatment outcomes and reduced relapse rates, encouraging therapy uptake. The market is experiencing growth across hospitals, specialty clinics, and outpatient facilities, with therapies being incorporated into both newly diagnosed cases and long-term maintenance programs.

U.K. ANCA Vasculitis Treatment Market Insight

The U.K. ANCA vasculitis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising autoimmune disease awareness, early diagnosis, and demand for personalized therapy. Additionally, increasing prevalence of relapsing cases encourages healthcare providers to adopt biologics and induction-maintenance therapy regimens. The U.K.’s robust healthcare system, alongside strong clinical guidelines and patient support programs, is expected to continue stimulating market growth. Growing adoption of outpatient care and specialty clinics also contributes to accessibility and treatment adherence.

Germany ANCA Vasculitis Treatment Market Insight

The Germany ANCA vasculitis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, increasing awareness of autoimmune diseases, and high adoption of biologics. Germany’s emphasis on innovation and precision medicine promotes the uptake of targeted therapies, particularly in hospitals and specialty clinics. Integration of advanced diagnostic tools such as blood tests, imaging, and biopsy supports early intervention and optimized treatment plans. Patients increasingly prefer therapies with proven efficacy and safety, driving consistent demand in both residential and hospital care settings.

Asia-Pacific ANCA Vasculitis Treatment Market Insight

The Asia-Pacific ANCA vasculitis treatment market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by rising healthcare infrastructure, increasing diagnosis rates, and growing awareness of autoimmune diseases in countries such as China, Japan, and India. The region’s expanding access to biologics, coupled with government initiatives promoting healthcare improvements, is driving adoption of both induction and maintenance therapies. Additionally, increased patient awareness and expanding specialty clinics support treatment uptake. Emerging markets are witnessing improved accessibility and affordability of therapies, contributing to rapid market growth.

Japan ANCA Vasculitis Treatment Market Insight

The Japan ANCA vasculitis treatment market is gaining momentum due to the country’s advanced healthcare infrastructure, high awareness of autoimmune disorders, and emphasis on precision medicine. Japan’s aging population further drives demand for effective, safe, and easy-to-administer therapies. The integration of targeted biologics and personalized treatment protocols supports improved patient outcomes and reduced relapse rates. Hospitals and specialty clinics are expanding treatment offerings, while patient support programs and routine monitoring enhance adherence, fueling market growth in both residential and clinical settings.

India ANCA Vasculitis Treatment Market Insight

The India ANCA vasculitis treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to increasing diagnosis rates, rising awareness among physicians and patients, and expanding healthcare infrastructure. India’s growing focus on specialty clinics and outpatient care facilities supports access to biologics and maintenance therapies. The push towards better autoimmune disease management, alongside increasing affordability of therapies and support programs, are key factors propelling market growth. The rapid urbanization and rising disposable income further contribute to wider adoption of ANCA vasculitis treatments.

Anca Vasculitis Treatment Market Share

The ANCA Vasculitis Treatment industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- AstraZeneca (U.K.)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Genentech, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- GSK plc (U.K.)

- Travere Therapeutics, Inc. (U.S.)

- InflaRx (Germany)

- Alentis Therapeutics AG (Switzerland)

- Daiichi Sankyo Company, Limited (Japan)

- Lilly USA, LLC. (U.S.)

- Baxter (U.S.)

- CSL (Switzerland)

- Nkarta, Inc. (U.S.)

- Biogen Inc. (U.S.)

- Sanofi (France)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

What are the Recent Developments in Global ANCA Vasculitis Treatment Market?

- In September 2025, Recent studies have explored the use of iptacopan, a novel complement C3 inhibitor, in treating AAV. Early-phase clinical trials suggest that iptacopan may offer benefits in reducing disease activity and improving renal outcomes, positioning it as a promising candidate in complement inhibition therapy

- In July 2025, A study published in Rheumatology (Oxford) demonstrated that avacopan, a complement C5a receptor inhibitor, is effective and well-tolerated in patients aged 65 and older with AAV. The study reported high remission rates and low relapse rates, suggesting avacopan as a viable treatment option for the elderly population

- In June 2025, The BSR released updated guidelines emphasizing the use of rituximab (RTX) and avacopan as first-line therapies for remission induction in newly diagnosed granulomatosis with polyangiitis (GPA) and microscopic polyangiitis (MPA). These recommendations reflect a shift towards biologic therapies over traditional cyclophosphamide, aiming to reduce glucocorticoid exposure and improve long-term outcomes

- In February 2024, The Kidney Disease: Improving Global Outcomes (KDIGO) organization published updated guidelines focusing on the management of AAV with renal involvement. The guidelines advocate for the use of lower-dose corticosteroids and the incorporation of complement inhibition therapies, aligning with the growing trend towards precision medicine in AAV treatment

- In January 2024, The European League Against Rheumatism (EULAR) released updated recommendations for AAV management, highlighting the importance of individualized treatment plans. The guidelines support the use of RTX and avacopan, particularly in patients with severe renal involvement, and emphasize the need for regular monitoring to tailor therapy effectively

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.