Global Aneurysmal Subarachnoid Hemorrhage Market

Market Size in USD Billion

USD

3.70 Billion

USD

7.05 Billion

2024

2032

USD

3.70 Billion

USD

7.05 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.70 Billion | |

| USD 7.05 Billion | |

| % | |

|

Aneurysmal Subarachnoid Hemorrhage Market Size

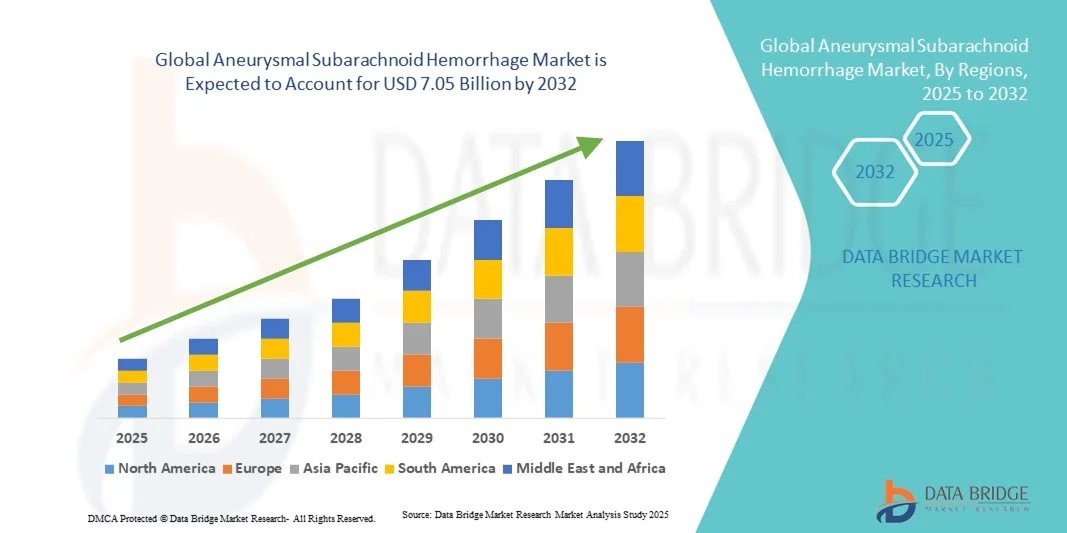

- The global aneurysmal subarachnoid hemorrhage market size was valued at USD 3.70 billion in 2024 and is expected to reach USD 7.05 billion by 2032, at a CAGR of 8.40% during the forecast period

- The market growth is largely fueled by advancements in diagnostic imaging, such as CT and MRI scans, and the adoption of minimally invasive surgical techniques such as endovascular coiling, leading to improved patient outcomes and reduced recovery times

- Furthermore, rising awareness, increasing healthcare investments, and the introduction of novel drug therapies targeting secondary complications such as vasospasm and delayed cerebral ischemia are establishing advanced treatment approaches as the preferred management strategy for aSAH patients. These converging factors are accelerating the uptake of innovative treatment solutions, thereby significantly boosting the industry's growth

Aneurysmal Subarachnoid Hemorrhage Market Analysis

- Aneurysmal subarachnoid hemorrhage (aSAH), a life-threatening type of stroke caused by bleeding in the space surrounding the brain, requires timely diagnosis and intervention. The aneurysmal subarachnoid hemorrhage market is increasingly driven by advancements in diagnostic imaging and treatment options, which improve early detection and patient outcomes in both acute and preventive care settings

- The rising prevalence of cerebrovascular disorders, growing awareness about stroke management, and increasing demand for advanced therapies are the primary factors fueling the aneurysmal subarachnoid hemorrhage market growth

- North America dominated the aneurysmal subarachnoid hemorrhage market with the largest revenue share of 42.5% in 2024, attributed to advanced healthcare infrastructure, high adoption of modern diagnostic technologies, and significant investments in neurovascular research. The U.S. in particular is witnessing substantial growth in the use of prescription drugs such as nimodipine, antiemetics, and anticonvulsants for managing aSAH complications

- Asia-Pacific is expected to be the fastest-growing region in the aneurysmal subarachnoid hemorrhage market during the forecast period, driven by increasing healthcare investments, rising incidence of cerebrovascular disorders, and growing awareness regarding early diagnosis and treatment options using advanced imaging modalities such as CT scan, MRI scan, and cerebral angiography

- Nimodipine dominated the aneurysmal subarachnoid hemorrhage market by drug class in 2024 with a market share of 46.5%, owing to its effectiveness in preventing vasospasm and improving neurological outcomes

Report Scope and Aneurysmal Subarachnoid Hemorrhage Market Segmentation

|

Attributes |

Aneurysmal Subarachnoid Hemorrhage Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Aneurysmal Subarachnoid Hemorrhage Market Trends

Advancements in Minimally Invasive Procedures and Imaging

- A significant and accelerating trend in the global aneurysmal subarachnoid hemorrhage market is the growing adoption of minimally invasive procedures such as endovascular coiling and flow diversion, alongside advanced imaging technologies such as CT and MRI, improving diagnosis accuracy and patient recovery outcomes

- For instance, hospitals increasingly employ high-resolution CT angiography combined with 3D reconstruction to precisely locate aneurysms and plan patient-specific interventions, enhancing procedural success rates

- Integration of computational imaging and predictive analytics enables clinicians to assess rupture risk and personalize treatment plans, contributing to safer and more efficient patient management

- For instance, some neurovascular centers use AI-based image analysis to detect micro-aneurysms earlier than traditional methods, facilitating timely intervention

- The trend toward combining treatment and monitoring tools with hospital information systems allows centralized management of patient records, imaging data, and post-procedural monitoring, creating a more streamlined and effective care pathway

Aneurysmal Subarachnoid Hemorrhage Market Dynamics

Driver

Increasing Prevalence and Rising Awareness About Stroke Management

- The growing prevalence of cerebrovascular disorders and increased awareness of stroke management among healthcare professionals and patients is a key driver of the global aneurysmal subarachnoid hemorrhage market

- For instance, public health campaigns and hospital-led stroke awareness programs are improving early detection and timely intervention, driving demand for advanced diagnostics and therapies

- Rising adoption of prescription drugs such as nimodipine, anticonvulsants, and antiemetics to manage complications associated with aSAH is boosting market growth

- For instance, neurology departments in leading hospitals have standardized nimodipine administration protocols to reduce vasospasm-related complications post-aneurysm rupture

- Government-funded neurovascular centers in North America and Europe are introducing specialized aSAH care units with state-of-the-art surgical and imaging facilities

- Increasing investments in neurovascular research and infrastructure by hospitals and biotech companies are expanding treatment capacity and availability, further driving market growth

Restraint/Challenge

Limited Access to Advanced Treatments and High Treatment Costs

- The high costs of minimally invasive procedures, advanced imaging technologies, and associated hospitalization can hinder adoption, especially in developing regions, posing a significant challenge to market growth

- For instance, small hospitals or clinics may not be equipped with high-resolution CT or MRI scanners required for precise aSAH diagnosis, limiting patient access to optimal care

- Lack of trained neurosurgeons and interventional radiologists in certain regions reduces the availability of advanced endovascular treatments, slowing market penetration

- For instance, rural and semi-urban areas in Asia-Pacific and Latin America often rely on traditional surgical interventions due to a shortage of specialized personnel

- Inconsistent healthcare coverage and reimbursement policies across regions further restrict patient access to costly treatments, affecting adoption rates

- Patients in regions with limited insurance support may delay intervention or rely on basic supportive care rather than advanced endovascular procedures

Aneurysmal Subarachnoid Hemorrhage Market Scope

The market is segmented on the basis of drug class, treatment type, route of administration, mode of purchase, and distribution channel.

- By Drug Class

On the basis of drug class, the global aneurysmal subarachnoid hemorrhage market is segmented into antiemetics, anticonvulsants, and nimodipine. The nimodipine segment dominated the market with the largest revenue share of 46.5% in 2024, driven by its proven efficacy in preventing vasospasm and improving neurological outcomes post-aneurysm rupture. Hospitals and neurocritical care units often prioritize nimodipine due to its established clinical protocols and robust safety profile. The high adoption of nimodipine is also supported by guidelines from neurology societies recommending its use as a standard therapy for aSAH patients. In addition, the segment benefits from widespread awareness among clinicians regarding dosing strategies and administration routes that optimize patient recovery. The drug’s compatibility with both intravenous and oral administration routes enhances its versatility in hospital and outpatient settings.

The antiemetics segment is anticipated to witness the fastest growth rate of 7.8% from 2025 to 2032, fueled by rising patient volumes experiencing nausea and vomiting post-surgery or intervention. Increasing recognition of patient comfort and improved recovery protocols is driving the adoption of antiemetics in both inpatient and outpatient care. New formulations with fewer side effects and improved bioavailability are gaining preference among neurocritical care practitioners. Hospitals are increasingly integrating antiemetics into comprehensive aSAH management regimens, often in combination with nimodipine or anticonvulsants. Growing investments in drug research and the introduction of generic alternatives further support the expansion of this segment.

- By Treatment Type

On the basis of treatment type, the aneurysmal subarachnoid hemorrhage market is segmented into CT scan, MRI scan, cerebral angiography, transcranial ultrasound, and lumbar puncture. The CT scan segment dominated the market with a revenue share of 39% in 2024, owing to its rapid availability, high diagnostic accuracy, and widespread use in emergency settings. CT scans are often the first-line imaging modality for suspected aSAH patients due to their ability to quickly detect hemorrhage and guide immediate intervention. Hospitals and trauma centers favor CT scans for their speed, cost-effectiveness, and reliability in acute care settings. Continuous technological improvements, such as high-resolution and 3D reconstruction capabilities, further bolster CT scan adoption. The segment benefits from integration with PACS (Picture Archiving and Communication Systems), enabling clinicians to access and share imaging data seamlessly.

The cerebral angiography segment is expected to witness the fastest growth rate of 8.2% from 2025 to 2032, driven by its critical role in detailed aneurysm visualization and endovascular treatment planning. Interventional radiologists and neurosurgeons rely on angiography to evaluate aneurysm morphology, size, and rupture risk accurately. Advances in digital subtraction angiography and 3D rotational imaging are increasing procedural precision and patient safety. Hospitals are investing in hybrid operating rooms and imaging suites to facilitate real-time angiographic procedures alongside interventions. The growing preference for minimally invasive procedures also propels demand for angiography as it allows targeted therapeutic approaches.

- By Route of Administration

On the basis of route of administration, the aneurysmal subarachnoid hemorrhage market is segmented into intravenous, oral, and parenteral. The oral segment dominated the market with a revenue share of 54% in 2024, primarily due to the convenience of administration in inpatient and outpatient settings and high patient compliance. Oral formulations of nimodipine and other supportive drugs allow for flexible dosing schedules and long-term management of post-aneurysm complications. Oral medications are widely used in rehabilitation units and follow-up therapy, complementing hospital-based intravenous treatments. In addition, oral drugs reduce hospital resource utilization and provide cost-effective treatment options for healthcare providers.

The intravenous segment is expected to witness the fastest CAGR of 6.9% from 2025 to 2032, fueled by the need for rapid therapeutic effect in acute and emergency aSAH cases. Intravenous administration ensures immediate bioavailability and precise control over dosing, critical for patients with severe complications. Hospitals prefer intravenous routes in intensive care units for continuous drug delivery and monitoring. Technological advancements in infusion systems and monitoring devices further enhance safety and efficacy. The segment is supported by increasing acute hospital admissions for aSAH and adoption of standardized intravenous protocols in neurocritical care centers.

- By Mode of Purchase

On the basis of mode of purchase, the aneurysmal subarachnoid hemorrhage market is segmented into prescription and over-the-counter (OTC). The prescription segment dominated the market with a share of 91% in 2024, as most aSAH medications, including nimodipine and anticonvulsants, require professional medical supervision due to potential side effects and precise dosing requirements. Hospitals and specialized neurovascular centers rely heavily on prescription-only drugs to manage complications effectively. Prescription medications ensure proper monitoring, adherence to clinical guidelines, and minimize risk of adverse events. The segment benefits from regulatory approvals and widespread acceptance in clinical protocols globally.

The OTC segment is expected to witness the fastest growth rate of 5.5% from 2025 to 2032, primarily due to increasing availability of supportive care drugs such as antiemetics for post-discharge patients. Consumer awareness regarding symptom management and home care is driving gradual adoption of OTC options. Pharmaceutical companies are introducing safer, easy-to-use OTC formulations that complement hospital-prescribed therapies. Growing focus on patient convenience, home-based care, and post-surgical recovery monitoring supports the expansion of this segment.

- By Distribution Channel

On the basis of distribution channel, the aneurysmal subarachnoid hemorrhage market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacy segment dominated the market with a share of 51% in 2024, owing to direct supply to neurocritical care units and emergency departments. Hospitals prefer centralized pharmacy procurement for quality control, immediate availability, and adherence to treatment protocols. Integration with hospital information systems allows seamless tracking of inventory, prescriptions, and patient-specific dosing. The segment also benefits from bulk purchasing agreements and collaborations with drug manufacturers, ensuring consistent supply of essential aSAH medications.

The online pharmacy segment is expected to witness the fastest CAGR of 9.3% from 2025 to 2032, driven by increasing internet penetration, rising e-pharmacy adoption, and convenience for post-discharge patients. Online channels provide access to prescription refills, home delivery, and a wider range of medications, enhancing patient adherence. Telemedicine integration further supports online pharmacy growth by enabling physicians to electronically prescribe necessary drugs. The segment is expanding rapidly in regions such as North America and Asia-Pacific, where digital healthcare adoption is accelerating.

Aneurysmal Subarachnoid Hemorrhage Market Regional Analysis

- North America dominated the aneurysmal subarachnoid hemorrhage market with the largest revenue share of 42.5% in 2024, attributed to advanced healthcare infrastructure, high adoption of modern diagnostic technologies, and significant investments in neurovascular research

- Hospitals and neurocritical care centers in the region emphasize rapid diagnosis and timely intervention using advanced imaging modalities such as CT scans, MRI scans, and cerebral angiography, improving patient outcomes and driving market demand

- The widespread adoption is further supported by substantial healthcare expenditure, presence of key pharmaceutical and medical device companies, and ongoing research in neurovascular treatments, establishing North America as a leading market for both pharmaceutical and procedural aSAH management solutions

U.S. Aneurysmal Subarachnoid Hemorrhage Market Insight

The U.S. aneurysmal subarachnoid hemorrhage market captured the largest revenue share of 44% in 2024 within North America, fueled by the widespread adoption of advanced diagnostic and interventional technologies. Hospitals and neurocritical care centers prioritize rapid imaging using CT scans, MRI scans, and cerebral angiography for timely detection and management of aneurysms. The growing emphasis on minimally invasive procedures, combined with increasing patient awareness and government initiatives on stroke prevention, further propels market growth. Moreover, the presence of leading pharmaceutical and medical device companies, along with robust research and development activities, is significantly contributing to the expansion of the U.S. market.

Europe Aneurysmal Subarachnoid Hemorrhage Market Insight

The Europe aneurysmal subarachnoid hemorrhage market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare expenditure, availability of specialized neurovascular centers, and rising awareness regarding early diagnosis and treatment. The growth of urban healthcare infrastructure, coupled with demand for advanced imaging and endovascular procedures, is fostering market adoption. European healthcare providers are also emphasizing comprehensive patient management and rehabilitation programs, supporting long-term treatment outcomes. The region is witnessing significant growth across both public and private hospitals, with advanced aSAH management protocols being incorporated into standard care practices.

U.K. Aneurysmal Subarachnoid Hemorrhage Market Insight

The U.K. aneurysmal subarachnoid hemorrhage market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising incidences of cerebrovascular disorders and increasing government initiatives for stroke awareness. Healthcare facilities are adopting advanced imaging techniques, such as high-resolution MRI and CT angiography, for early diagnosis and improved patient outcomes. In addition, concerns regarding mortality and complications post-aneurysm rupture are encouraging hospitals and neurocritical care centers to implement endovascular and pharmacological interventions. The U.K.’s strong healthcare infrastructure and emphasis on research and clinical trials are expected to continue stimulating market growth.

Germany Aneurysmal Subarachnoid Hemorrhage Market Insight

The Germany aneurysmal subarachnoid hemorrhage market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s well-developed healthcare infrastructure and rising awareness of cerebrovascular disorders. Germany’s focus on advanced diagnostic imaging and minimally invasive surgical procedures promotes the adoption of modern aSAH treatments in both public and private hospitals. Integration of neurocritical care units with sophisticated imaging and monitoring systems is becoming increasingly prevalent. Moreover, a strong emphasis on patient safety, research, and innovative treatment protocols aligns with local expectations and supports sustained market growth.

Asia-Pacific Aneurysmal Subarachnoid Hemorrhage Market Insight

The Asia-Pacific aneurysmal subarachnoid hemorrhage market is poised to grow at the fastest CAGR of 6.5% from 2025 to 2032, driven by rising healthcare expenditure, urbanization, and increasing prevalence of cerebrovascular disorders in countries such as China, Japan, and India. The region’s growing inclination towards advanced medical care, supported by government initiatives for stroke prevention and improved hospital infrastructure, is driving market adoption. Furthermore, Asia-Pacific is emerging as a hub for affordable medical devices and pharmaceuticals, increasing accessibility to advanced aSAH diagnostics and treatments for a wider patient population.

Japan Aneurysmal Subarachnoid Hemorrhage Market Insight

The Japan aneurysmal subarachnoid hemorrhage market is gaining momentum due to the country’s advanced healthcare system, rapid urbanization, and increasing focus on preventive care. Hospitals emphasize early diagnosis using CT, MRI, and cerebral angiography, complemented by minimally invasive interventions and pharmacological management. Integration of hospital information systems with imaging and treatment protocols enhances patient care. Moreover, Japan’s aging population is expected to spur demand for timely and efficient management of aSAH, particularly in residential and long-term care facilities.

India Aneurysmal Subarachnoid Hemorrhage Market Insight

The India aneurysmal subarachnoid hemorrhage market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rising healthcare awareness, urbanization, and increasing availability of advanced diagnostic and interventional facilities. India is witnessing growing adoption of CT, MRI, and angiographic procedures, particularly in metro cities. Expansion of private neurocritical care centers and government initiatives for stroke management are supporting market growth. In addition, affordable treatment options and increasing medical tourism are further propelling the adoption of advanced aSAH management solutions across residential and commercial healthcare settings.

Aneurysmal Subarachnoid Hemorrhage Market Share

The Aneurysmal Subarachnoid Hemorrhage industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker (U.S.)

- Abbott (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Arbor Pharmaceuticals, Inc. (U.S.)

- Edge Therapeutics, Inc. (U.S.)

- Actelion Pharmaceuticals Ltd. (Switzerland)

- Idorsia Pharmaceuticals Ltd. (Switzerland)

- Evgen Pharma plc (U.K.)

- Grace Therapeutics (U.S.)

- GE Healthcare (U.K.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens AG (Germany)

- Trivitron Healthcare (India)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- BIT Pharma (India)

What are the Recent Developments in Global Aneurysmal Subarachnoid Hemorrhage Market?

- In September 2025, a multicenter, randomized, double-blind, placebo-controlled Phase III trial (CASH trial) commenced to evaluate the efficacy and safety of cilostazol, an antiplatelet agent, in improving outcomes for patients with aSAH. The trial aims to assess the potential benefits of cilostazol in reducing complications associated with aSAH

- In August 2025, Grace Therapeutics announced that the U.S. Food and Drug Administration (FDA) accepted its New Drug Application (NDA) for GTx-104, an injectable formulation of nimodipine aimed at improving outcomes in patients with aSAH. The FDA has set a Prescription Drug User Fee Act (PDUFA) target date of April 23, 2026, for its review

- In August 2025, Grace Therapeutics announced the launch of GTx-104, an injectable formulation of nimodipine designed to improve outcomes in patients with aSAH. This product aims to address the limitations of oral nimodipine by providing more consistent drug delivery and potentially better clinical outcomes. The launch follows successful Phase 3 trials and is expected to offer a new treatment option for aSAH patients

- In June 2025, Grace Therapeutics secured a strategic collaboration with Nantahala Capital, involving a USD 15 million upfront investment with the potential for an additional USD 15 million upon the exercise of accompanying warrants. This partnership aims to support the pre-commercial planning, commercial team build-out, and product launch of GTx-104, contingent upon regulatory approval. The collaboration underscores the confidence in GTx-104's potential to become a significant advancement in aSAH treatment.

- In May 2023, the American Heart Association (AHA) and American Stroke Association (ASA) released updated guidelines for the management of patients with aSAH. These guidelines provide evidence-based recommendations for the prevention, diagnosis, and treatment of aSAH, aiming to improve patient outcomes and standardize care practices

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.