Global Chin Augmentation Injectable Fillers Market

Market Size in USD Million

USD

307.90 Million

USD

590.92 Million

2025

2033

USD

307.90 Million

USD

590.92 Million

2025

2033

| 2026 - 2033 | |

| USD 307.90 Million | |

| USD 590.92 Million | |

| % | |

|

Chin Augmentation Injectable Fillers Market Size

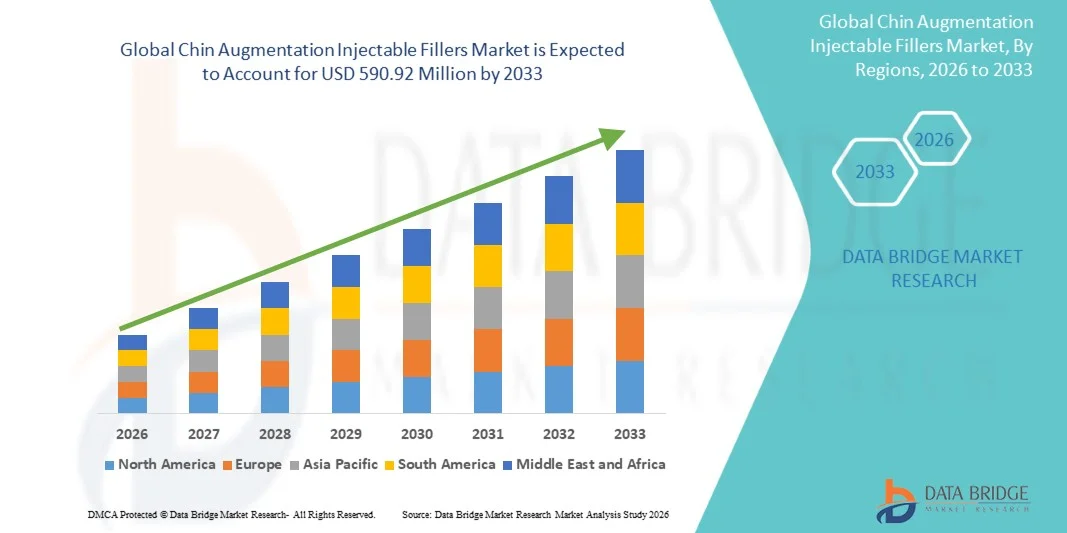

- The global chin augmentation injectable fillers market size was valued at USD 307.90 million in 2025 and is expected to reach USD 590.92 million by 2033, at a CAGR of 8.49% during the forecast period

- The market growth is primarily driven by the rising demand for minimally invasive aesthetic procedures, growing acceptance of injectable fillers for facial contouring, and increasing awareness of cosmetic enhancements among both men and women

- In addition, advancements in dermal filler formulations particularly hyaluronic acid and biostimulatory injectables alongside shorter recovery times and expanding availability of skilled practitioners are fueling global adoption. These combined factors are accelerating the uptake of chin augmentation injectable fillers, thereby significantly boosting the industry’s growth

Chin Augmentation Injectable Fillers Market Analysis

- Chin augmentation injectable fillers, offering non-surgical enhancement and contouring of the chin and jawline, are becoming increasingly popular in aesthetic medicine due to their ability to deliver natural-looking results with minimal downtime. These treatments enhance facial balance, correct chin retrusion, and improve overall symmetry using advanced filler formulations such as hyaluronic acid and calcium hydroxylapatite

- The growing demand for chin augmentation injectable fillers is primarily fueled by the rising preference for minimally invasive cosmetic procedures, increasing social media influence on facial aesthetics, and continuous innovation in filler technology that enhances longevity and safety

- North America dominated the chin augmentation injectable fillers market with the largest revenue share of 40.2% in 2025, supported by high consumer spending on aesthetic treatments, the presence of established cosmetic clinics, and strong brand portfolios from leading dermal filler manufacturers in the U.S.

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, driven by increasing beauty awareness, expanding medical tourism, and a rapidly growing middle-class population seeking affordable non-surgical aesthetic enhancements

- The hyaluronic acid filler segment dominated the market with a share of 46% in 2025, attributed to its superior safety profile, reversibility, and natural-looking outcomes, making it the preferred choice among dermatologists and aesthetic practitioners for chin augmentation procedures

Report Scope and Chin Augmentation Injectable Fillers Market Segmentation

|

Attributes |

Chin Augmentation Injectable Fillers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Chin Augmentation Injectable Fillers Market Trends

“Personalized Aesthetic Enhancements Through AI and Advanced Filler Technology”

- A significant and accelerating trend in the global chin augmentation injectable fillers market is the integration of artificial intelligence (AI) and digital imaging technologies into facial analysis and treatment planning, enhancing precision, customization, and patient satisfaction

- For instance, AI-driven facial mapping systems are increasingly used by aesthetic practitioners to simulate post-procedure outcomes, helping patients visualize chin and jawline enhancements before treatment

- The incorporation of smart injectables and advanced filler formulations, such as cross-linked hyaluronic acid and biostimulatory fillers, enables longer-lasting results and better facial harmony through controlled volume restoration

- AI tools further assist in identifying the most suitable filler type, injection depth, and technique for each patient, improving safety while minimizing the risk of overcorrection or asymmetry

- This convergence of digital assessment tools and scientifically advanced filler materials is revolutionizing aesthetic dermatology, making non-surgical chin augmentation more precise and personalized

- Consequently, companies such as Allergan Aesthetics and Galderma are investing in AI-supported aesthetic platforms and next-generation filler technologies to strengthen their market presence and enhance treatment predictability

- The demand for AI-guided, minimally invasive facial contouring solutions is growing rapidly across dermatology clinics and medical spas, as consumers increasingly prioritize safety, personalization, and natural-looking enhancements

Chin Augmentation Injectable Fillers Market Dynamics

Driver

“Rising Demand for Minimally Invasive Aesthetic Procedures and Social Media Influence”

- The increasing global preference for minimally invasive cosmetic procedures, combined with the influence of social media beauty trends, is a significant driver for the rising demand for chin augmentation injectable fillers

- For instance, in March 2025, Galderma launched an advanced hyaluronic acid-based filler designed for precise chin and jawline sculpting, reflecting the growing industry focus on non-surgical facial enhancement solutions

- As consumers seek facial symmetry and defined jawlines without surgery, injectable fillers offer a quick, effective, and low-risk alternative with minimal recovery time

- Furthermore, the growing presence of certified aesthetic practitioners and the availability of advanced filler formulations are broadening patient access to safe, natural-looking outcomes

- The convenience of short treatment sessions, affordability compared to surgical implants, and instant aesthetic improvement are key factors propelling filler adoption globally. The increasing participation of men in cosmetic enhancements and the trend toward facial balancing further contribute to market expansion

- For instance, Allergan’s Juvéderm Volux XC has gained traction as a specialized chin and jawline filler, highlighting the market’s movement toward region-specific injectable innovations

- The rapid rise of aesthetic clinics and medspas across emerging economies, supported by social media-driven beauty awareness, is expected to further boost global filler demand during the forecast period

Restraint/Challenge

“Skin Irritation Issues and Regulatory Compliance Hurdle”

- Concerns regarding potential side effects such as swelling, bruising, and delayed-onset nodules following filler injections pose a significant restraint to market growth

- For instance, reports of temporary inflammation or allergic reactions associated with certain filler formulations have led to heightened safety scrutiny by regulatory authorities

- Addressing these challenges through improved biocompatible materials, standardized injection protocols, and post-treatment care guidelines is essential for maintaining patient confidence

- Companies such as Merz Aesthetics and Revance Therapeutics are focusing on extensive clinical testing and transparency in ingredient safety to meet evolving global regulatory standards

- In addition, the complex and varying approval processes across regions can delay product launches and limit market penetration for new filler technologies. While awareness and training initiatives are improving, regulatory compliance remains a key challenge for global market expansion

- For instance, varying approval timelines between the U.S. FDA, EMA, and Asian regulatory bodies often slow international product rollouts, restricting global accessibility for new injectables

- Growing concerns over counterfeit or unregulated filler products in developing markets also threaten patient safety and brand reputation, underscoring the need for stricter market surveillance and practitioner certification

Chin Augmentation Injectable Fillers Market Scope

The market is segmented on the basis of type, application, gender, and end user.

- By Type

On the basis of type, the chin augmentation injectable fillers market is segmented into Hyaluronic Acid (HA) Fillers, Calcium Hydroxylapatite (CaHA) Fillers, Polymethyl Methacrylate (PMMA) Fillers, Poly-L-Lactic Acid (PLLA) Fillers, and Others. The Hyaluronic Acid (HA) Fillers segment dominated the market with the largest revenue share of 46% in 2025, owing to its superior safety profile, biocompatibility, and reversibility. HA fillers offer immediate volumizing effects and are easily adjustable, making them the preferred choice for aesthetic practitioners and patients seeking natural results. Their hydrophilic properties enhance chin projection and contour definition effectively, with minimal downtime. The rising use of HA fillers in aesthetic clinics is also supported by growing FDA approvals for chin-specific applications. Moreover, top brands such as Allergan’s Juvéderm Volux XC and Galderma’s Restylane Defyne have strengthened their presence through advanced HA formulations tailored for facial sculpting.

The Poly-L-Lactic Acid (PLLA) Fillers segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for long-lasting, collagen-stimulating injectables. PLLA fillers gradually stimulate natural collagen production, offering sustained enhancement and firmness over time. Their growing adoption among younger demographics seeking preventive aesthetics reflects the shift toward bioactive and regenerative treatments. In addition, ongoing innovations by companies such as Suneva Medical and Revance Therapeutics are expanding the application of PLLA-based fillers beyond facial rejuvenation to structural contouring, including the chin and jawline.

- By Application

On the basis of application, the market is segmented into chin projection enhancement, correction of chin retrusion, chin contouring, and touch-up procedures. The Chin Contouring segment dominated the market in 2025, as patients increasingly seek balanced and defined lower-face profiles without surgery. Non-surgical contouring procedures using advanced dermal fillers have become highly popular among millennials and working professionals due to their quick recovery and customizable results. The precision and control achieved with advanced injectables allow practitioners to enhance the chin and jawline proportionately, contributing to improved overall facial harmony. The segment’s growth is further supported by the rising preference for subtle yet refined cosmetic enhancements amplified by social media and digital imaging tools.

The Chin Projection Enhancement segment is expected to exhibit the fastest growth from 2026 to 2033, driven by increased awareness of facial proportionality and rising adoption of minimally invasive methods to address recessed chins. Injectable fillers provide a safe, reversible solution compared to surgical implants and are increasingly used to improve facial symmetry in both men and women. The use of advanced HA and CaHA fillers enables precise volume restoration and profile improvement, leading to natural results. Furthermore, digital pre-visualization tools and AI-based facial analysis are aiding practitioners in customizing projection procedures, further driving segment expansion.

- By Gender

On the basis of gender, the market is segmented into female patients and male patients. The Female Patients segment dominated the global chin augmentation injectable fillers market in 2025, accounting for the largest revenue share due to the high acceptance of cosmetic enhancement procedures among women. Women are more such asly to seek aesthetic treatments to enhance facial harmony and rejuvenation, with chin contouring playing a key role in achieving the desirable V-shaped facial profile. The increasing influence of social media and celebrity endorsements continues to normalize aesthetic treatments across younger female demographics. In addition, growing access to advanced filler options and flexible payment models in clinics has made treatments more accessible and routine.

The Male Patients segment is projected to grow at the fastest rate from 2026 to 2033, supported by increasing acceptance of aesthetic procedures among men seeking more defined and masculine jawlines. Non-surgical chin augmentation offers subtle enhancement without downtime, aligning well with male aesthetic preferences. For instance, demand for chin enhancement among men in North America and East Asia is rising sharply, influenced by cultural trends emphasizing strong facial structure. Clinics are now tailoring treatment protocols and marketing strategies specifically for male patients, further accelerating segment growth.

- By End User

On the basis of end user, the market is segmented into aesthetic clinics, medspas, hospitals, and ambulatory surgical centres (ASCs). The Aesthetic Clinics segment dominated the market in 2025, attributed to the high concentration of skilled dermatologists and cosmetic surgeons providing specialized filler treatments. These clinics are equipped with advanced facial analysis tools and product options, offering precise and tailored chin enhancement solutions. The personalized consultation experience and trust in qualified experts continue to drive patient preference for clinical settings over general healthcare facilities. Furthermore, strategic collaborations between filler manufacturers and aesthetic chains are enhancing product reach and treatment awareness among patients.

The MedSpas segment is anticipated to register the fastest growth from 2026 to 2033, fueled by increasing consumer inclination toward convenient, affordable, and non-invasive aesthetic treatments. MedSpas bridge the gap between medical expertise and luxury wellness, providing quick injectable procedures in a comfortable environment. The rising trend of “lunch-hour makeovers” and expanding presence of certified practitioners in spa-based facilities are contributing significantly to this segment’s growth. In addition, partnerships between medspa chains and established dermal filler brands are increasing accessibility to premium products, further strengthening their market position globally.

Chin Augmentation Injectable Fillers Market Regional Analysis

- North America dominated the chin augmentation injectable fillers market with the largest revenue share of 40.2% in 2025, supported by high consumer spending on aesthetic treatments, the presence of established cosmetic clinics, and strong brand portfolios from leading dermal filler manufacturers in the U.S.

- Consumers in the region highly value advanced, non-surgical treatments that offer natural-looking results, shorter recovery times, and customizable outcomes for facial balancing and contouring

- This widespread adoption is further supported by high disposable incomes, a well-established network of aesthetic clinics and medspas, and growing social media influence promoting facial enhancement trends, establishing North America as a key hub for chin augmentation injectable filler procedures in both male and female demographics

U.S. Chin Augmentation Injectable Fillers Market Insight

The U.S. chin augmentation injectable fillers market captured the largest revenue share of 82% in 2025 within North America, driven by the increasing popularity of non-surgical facial contouring and the rising influence of social media beauty standards. Consumers are increasingly opting for injectable fillers to achieve facial symmetry and enhanced chin projection without undergoing invasive surgery. The growing preference for hyaluronic acid and calcium hydroxylapatite fillers, combined with advancements in injection techniques and FDA-approved products, is fueling market growth. Moreover, the widespread presence of aesthetic clinics, skilled practitioners, and premium product availability further reinforces the U.S. market’s leadership.

Europe Chin Augmentation Injectable Fillers Market Insight

The Europe chin augmentation injectable fillers market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by a surge in aesthetic consciousness and the preference for minimally invasive cosmetic enhancements. Rising adoption of dermal fillers in countries such as Germany, France, and the U.K. is supported by advanced healthcare infrastructure and a growing population seeking facial rejuvenation procedures. Furthermore, the presence of key global filler manufacturers and regulatory approvals for new filler formulations are accelerating adoption across the region.

U.K. Chin Augmentation Injectable Fillers Market Insight

The U.K. chin augmentation injectable fillers market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by an increasing demand for aesthetic procedures among both women and men. The market’s growth is supported by expanding awareness of non-surgical treatments, the influence of beauty trends, and the availability of skilled aesthetic practitioners. In addition, stricter clinical standards and a rise in boutique medspas offering customized filler solutions are contributing to market expansion in the U.K.

Germany Chin Augmentation Injectable Fillers Market Insight

The Germany chin augmentation injectable fillers market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong preference for high-quality, safe, and clinically proven dermal filler products. Germany’s focus on precision-based cosmetic procedures and its advanced dermatology and aesthetic care infrastructure make it a leading destination for injectable filler treatments. Moreover, the increasing participation of men in facial enhancement procedures and growing awareness about facial harmony are enhancing market penetration across both urban and suburban areas.

Asia-Pacific Chin Augmentation Injectable Fillers Market Insight

The Asia-Pacific chin augmentation injectable fillers market is poised to grow at the fastest CAGR of 25.4% during 2026–2033, driven by the rising acceptance of aesthetic medicine, rapid urbanization, and an expanding middle-class population seeking facial contouring solutions. Countries such as China, Japan, and South Korea are at the forefront due to cultural beauty preferences emphasizing defined facial features. The growth is further supported by affordable treatment options, availability of advanced filler formulations, and a high concentration of aesthetic clinics in metropolitan regions.

Japan Chin Augmentation Injectable Fillers Market Insight

The Japan chin augmentation injectable fillers market is gaining momentum due to a growing inclination toward non-surgical beauty enhancements and precision-based aesthetic techniques. Japanese consumers emphasize subtle and natural results, which aligns with the demand for injectable fillers that provide soft yet defined chin contouring. The integration of technologically advanced fillers and increasing acceptance among younger demographics are fueling growth. In addition, local innovations and safety-focused clinical standards further strengthen Japan’s market presence.

India Chin Augmentation Injectable Fillers Market Insight

The India chin augmentation injectable fillers market accounted for the largest revenue share in Asia-Pacific in 2025, supported by the country’s expanding aesthetic industry and growing preference for non-invasive facial treatments. Increasing disposable incomes, rapid urbanization, and the influence of social media-driven beauty standards are major drivers. Moreover, the proliferation of aesthetic clinics and medspas in urban centers, coupled with the availability of cost-effective international filler brands, is propelling adoption. India’s youthful population and rising male participation further reinforce market growth potential.

Chin Augmentation Injectable Fillers Market Share

The Chin Augmentation Injectable Fillers industry is primarily led by well-established companies, including:

- AbbVie (U.S.)

- GALDERMA (Switzerland)

- Merz Pharma (Germany)

- Hugel Inc. (South Korea)

- LG Chem (South Korea)

- Medytox (South Korea)

- IBSA Institut Biochimique SA (Switzerland)

- Laboratoires VIVACY (France)

- Prollenium Medical Technologies (Canada)

- Croma Pharma (Austria)

- FillMed Laboratories (France)

- Humedics Co., Ltd (South Korea)

- TEOXANE (Switzerland)

- Sinclair Pharma plc (U.K.)

- Bioscience GmbH (Germany)

- Amalian GmbH (Germany)

- Bioxis Pharmaceuticals (France)

- Mesoestetic Pharma Group (Spain)

- Jalupro (Italy)

- BIOPLUS CO., LTD. (South Korea)

What are the Recent Developments in Global Chin Augmentation Injectable Fillers Market?

- In November 2025, Galderma’s Restylane Lyft with Lidocaine received FDA approval for augmentation of the chin region to improve chin profile in patients over 21 with mild-to-moderate chin retrusion. This approval validated a HA injectable for chin profile correction, reinforcing the trend of fillers gaining specific lower-face indications and expanding treatment offerings for chin enhancement

- In January 2024, Galderma announced regulatory approval in Canada for Restylane SHAYPE, a new hyaluronic acid injectable designed specifically for chin augmentation using NASHA HD™ technology. This product is tailored for chin region augmentation, reflecting the evolution of filler technology to target chin contour and projection more precisely

- In January 2023, JUVÉDERM VOLUX XC was launched nationally in the U.S. for aesthetic practices, becoming widely available to consumers over 21 with moderate-to-severe loss of jawline definition after its earlier approval. This launch expanded access and signalled commercial readiness of specialized lower-face injectable solutions

- In August 2022, The JUVÉDERM VOLUX XC earned FDA approval for improvement of jawline definition in adults over 21 with moderate-to-severe loss of jawline definition. The approval underscored the heightened demand for structurally stronger fillers in the lower face and gave practitioners a firmer gel option for chin/jawline enhancement

- In February 2021, The Restylane Defyne hyaluronic-acid filler received U.S. Food and Drug Administration (FDA) approval for the augmentation and correction of mild-to-moderate chin retrusion in adults over 21. This marked one of the first fillers to be specifically labelled for chin enhancement rather than off-label use

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.