Global Cocoa Butter Market

Market Size in USD Billion

USD

3.30 Billion

USD

5.62 Billion

2025

2033

USD

3.30 Billion

USD

5.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.30 Billion | |

| USD 5.62 Billion | |

| % | |

|

What is the Cocoa Butter Market Size and Overview?

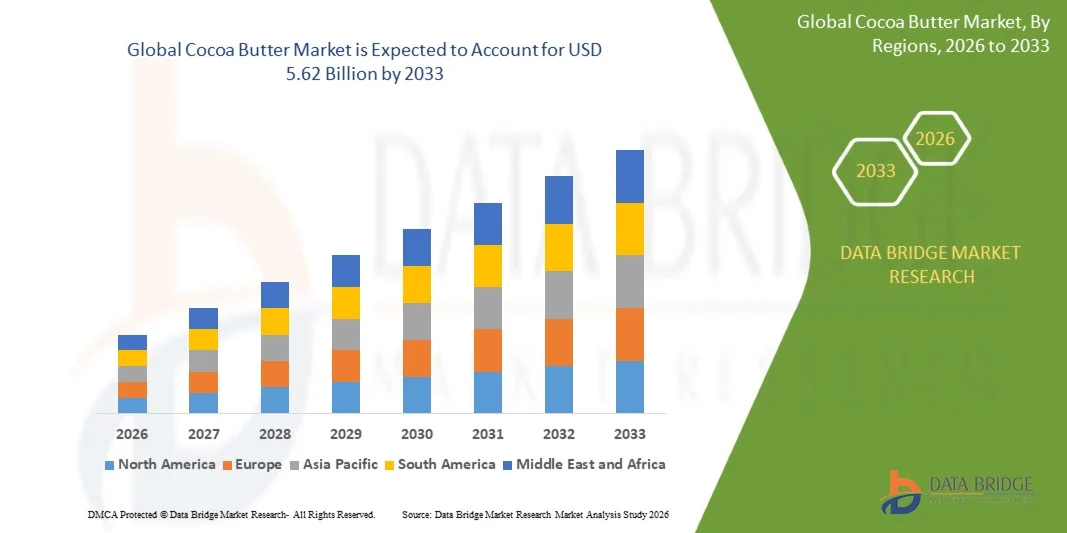

As per Data Bridge Market Research Analysis the Cocoa Butter Market was valued at USD 3.30 billion in 2025 and is projected to reach USD 5.62 billion by 2033, growing at a CAGR of 6.90% from 2026 to 2033. The market is witnessing steady growth driven by rising demand for premium confectionery and bakery products, increasing use in cosmetics and personal care formulations, and expanding applications in pharmaceutical ointments and skincare products.

The growing consumer preference for natural and plant-based ingredients, combined with the expansion of chocolate manufacturing and clean-label product trends, is accelerating cocoa butter consumption worldwide. In addition, increasing demand from the cosmetics industry for moisturizing and anti-aging formulations, along with stable supply chain developments in cocoa-producing regions, is further supporting market expansion.

Market Size & Forecast

- Global Market Value (2025): USD 3.30 Billion

- Expected Market Value (2033): USD 5.62 Billion

- Forecast CAGR (2026–2033): 6.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the Cocoa Butter Market with the largest revenue share of 35.08% in 2025, supported by strong demand from premium chocolate manufacturers, well-established cosmetics and personal care industries, and high consumption of processed and functional foods.

- The Natural segment led the market with a 44.6% share in 2025, driven by its strong demand in premium chocolate manufacturing, organic cosmetics, and clean-label food formulations.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.9% from 2026 to 2033, fueled by rising disposable incomes, expanding middle-class population, and increasing Western-style dessert consumption in China, India, and Southeast Asia.

- Deodorized is the fastest-growing type, projected to register a CAGR of 6.8%, reflecting the surge in wide usability in mass-market chocolate production and cosmetics where neutral flavor and odor are required.

- The Blocks segment dominated the form type category with a 52.3% revenue share in 2025, led by its widespread use in chocolate manufacturing, cosmetics production, and pharmaceutical formulations.

- Conventional accounted for 61.8% of the market, preferred by large-scale availability, cost efficiency, and widespread use in industrial chocolate and cosmetic production.

- The Organic segment is the fastest-growing nature category, with a CAGR of 7.9%, driven by demand for increasing consumer awareness of clean-label products and sustainable sourcing.

Report Scope and Cocoa Butter Market Segmentation

|

Attributes |

Cocoa Butter Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Cocoa Butter Market?

Trend: Rising Demand for Clean-Label and Natural Ingredient-Based Products

Food and cosmetics manufacturers are increasingly prioritizing clean-label cocoa butter due to strong consumer preference for natural, minimally processed, and chemical-free ingredients in chocolate, bakery, skincare, and pharmaceutical formulations. This shift is being driven by heightened health awareness, regulatory pressure on synthetic additives, and rapid growth of organic and premium product categories across global markets. Cocoa butter is widely valued for its natural fat composition, smooth texture, and functional benefits such as skin hydration and product stability, making it a key ingredient in reformulated premium offerings. The trend is also reinforced by sustainability expectations, with brands focusing on ethically sourced cocoa ingredients to improve brand perception and consumer trust.

Cocoa Butter Market Dynamics

Key Market Driver: Expanding Use in Premium Chocolate and Cosmetic Applications

The growing global demand for premium chocolates, artisanal confectionery, and high-performance skincare products is significantly boosting cocoa butter consumption worldwide. Its unique melting properties, smooth mouthfeel, and emollient characteristics make it essential in luxury chocolate production and advanced cosmetic formulations such as anti-aging creams, lip balms, and body lotions. Rising disposable incomes, urbanization, and lifestyle upgrades in emerging economies are accelerating demand for indulgent food experiences and premium personal care products. In addition, manufacturers are increasingly using cocoa butter to differentiate high-end product lines and enhance sensory appeal, leading to stronger integration across food and cosmetics industries.

Key Restraint/Challenge: Volatility in Cocoa Bean Supply and Pricing

A major challenge in the Cocoa Butter Market is the instability in cocoa bean supply chains, which directly impacts production consistency, pricing structures, and long-term procurement strategies. Cocoa cultivation is highly dependent on climatic conditions, including rainfall patterns and temperature stability, making it vulnerable to weather fluctuations and climate change impacts. In addition, cocoa crops are affected by pests, diseases, and aging plantations in major producing regions such as West Africa, which supplies a significant share of global cocoa beans. Political instability, export regulations, and labor challenges further contribute to supply disruptions and price volatility, creating uncertainty for manufacturers across food and cosmetics sectors.

For instance, supply shortages and export constraints in Ivory Coast and Ghana have historically triggered global cocoa price surges, forcing manufacturers to adjust formulations, optimize sourcing strategies, or pass increased costs to end consumers.

Key Market Opportunity: Growth in Sustainable and Ethical Sourcing Initiatives

The increasing global emphasis on sustainability, ethical sourcing, and environmental responsibility presents a strong growth opportunity for the cocoa butter market. Consumers are becoming more conscious of deforestation, child labor concerns, and environmental degradation associated with cocoa farming, pushing companies to adopt transparent and responsible sourcing practices. As a result, certification schemes such as Fair Trade, Rainforest Alliance, and organic labeling are gaining widespread adoption across supply chains. In parallel, digital traceability tools, including blockchain-based systems, are being implemented to ensure end-to-end visibility from cocoa farms to final products. This is helping manufacturers build trust, enhance brand reputation, and meet regulatory and ESG requirements.

For instance, several global chocolate manufacturers and cosmetic brands are partnering directly with certified cocoa cooperatives in West Africa and Latin America to secure sustainably sourced cocoa butter and strengthen ethical supply chain commitments.

Cocoa Butter Market Scope

The cocoa butter market is segmented on the basis of type, form, nature, end use, packaging, and distribution channel.

- By Type

On the basis of type, the Cocoa Butter Market is segmented into natural, deodorized, and semi-deodorized cocoa butter. The Natural Cocoa Butter segment dominated the market with a 44.6% share in 2025, owing to its strong demand in premium chocolate manufacturing, organic cosmetics, and clean-label food formulations. It retains its natural aroma and flavor profile, making it highly preferred in artisanal and high-end confectionery products. The segment benefits from rising consumer preference for minimally processed and chemical-free ingredients across food and personal care industries. Natural cocoa butter is also widely used in skincare formulations due to its superior moisturizing and antioxidant properties. Increasing adoption in organic product lines and sustainable sourcing initiatives further strengthens its market dominance. Its premium positioning continues to drive consistent demand in developed regions such as North America and Europe.

The Deodorized Cocoa Butter segment is expected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by its wide usability in mass-market chocolate production and cosmetics where neutral flavor and odor are required. It is highly preferred by large-scale manufacturers for product consistency and formulation flexibility. The removal of natural cocoa aroma makes it suitable for applications requiring added flavors or fragrances. Growing industrial demand from processed food manufacturers is accelerating its adoption. Expansion of packaged food and confectionery industries in emerging markets is further supporting growth. Its cost-effectiveness and scalability make it attractive for high-volume production environments.

- By Form

On the basis of form, the market is segmented into blocks, powder, and liquid cocoa butter. The Blocks segment dominated the market with a 52.3% share in 2025, primarily due to its widespread use in chocolate manufacturing, cosmetics production, and pharmaceutical formulations. Block form offers ease of storage, longer shelf life, and efficient handling during industrial processing. It is the most commonly traded and standardized form in global supply chains. Manufacturers prefer blocks for bulk melting and consistent quality control in production processes. The segment also benefits from strong demand in large-scale confectionery production units. Its logistical efficiency and stability make it the most preferred format globally.

The Liquid Cocoa Butter segment is expected to grow the fastest at a CAGR of 7.4% from 2026 to 2033, driven by increasing use in cosmetics and skincare formulations where direct blending is required. Liquid form allows easier incorporation into creams, lotions, and pharmaceutical ointments. It reduces processing time and improves formulation efficiency for manufacturers. Rising demand for ready-to-use cosmetic ingredients is boosting adoption. Growth in premium skincare and spa-based wellness products is further supporting expansion. Technological improvements in controlled melting and stabilization are enhancing its commercial viability.

- By Nature

On the basis of nature, the market is segmented into organic and conventional cocoa butter. The Conventional Cocoa Butter segment dominated the market with a 61.8% share in 2025, due to its large-scale availability, cost efficiency, and widespread use in industrial chocolate and cosmetic production. It is the primary choice for mass-market confectionery brands and standardized formulations. Established global supply chains ensure steady production and affordability. High demand from emerging economies further supports its dominance. The segment benefits from strong integration into food processing and personal care manufacturing systems. Its scalability and price advantage continue to drive global consumption.

The Organic Cocoa Butter segment is expected to grow the fastest at a CAGR of 7.9% from 2026 to 2033, driven by increasing consumer awareness of clean-label products and sustainable sourcing. It is widely used in premium chocolates, organic skincare, and natural pharmaceutical products. Strict regulatory support for organic certifications is enhancing market credibility. Rising demand for environmentally friendly and chemical-free ingredients is boosting adoption. Premiumization trends in food and cosmetics are further accelerating growth. Expansion of certified organic farming practices is improving supply availability globally.

- By End Use

On the basis of end use, the market is segmented into food and beverage industry, pharmaceuticals, and personal care and cosmetics. The Food and Beverage segment dominated the market with a 48.9% share in 2025, driven by extensive use of cocoa butter in chocolate manufacturing, bakery products, dairy-based desserts, and confectionery applications. Its unique melting profile and smooth texture make it essential in premium chocolate production. Rising global chocolate consumption and expanding packaged food industries further strengthen demand. The segment benefits from strong industrial-scale usage across developed and emerging markets. Continuous innovation in flavored and functional confectionery products supports growth. Its role as a key structural fat makes it indispensable in food processing.

The Personal Care and Cosmetics segment is expected to grow the fastest at a CAGR of 8.1% from 2026 to 2033, driven by increasing demand for natural moisturizers, anti-aging creams, lip balms, and organic skincare formulations. Cocoa butter is highly valued for its emollient, healing, and skin-protective properties. Rising consumer preference for clean beauty products is significantly boosting adoption. Expansion of luxury skincare brands is further accelerating demand. Growth in spa, wellness, and personal grooming industries supports long-term expansion. Increasing incorporation into pharmaceutical skincare products is also contributing to rapid growth.

- By Packaging

On the basis of packaging, the market is segmented into tins, cartons, plastic containers, paper containers, and others. The Tins segment dominated the market with a 39.7% share in 2025, primarily due to its superior protection against moisture, heat, and contamination, making it ideal for preserving cocoa butter quality during long-distance transportation. Tins are widely used in industrial bulk packaging for food and cosmetics manufacturers. They provide durability, recyclability, and extended shelf stability. The segment benefits from strong adoption in export-oriented supply chains. High compatibility with bulk storage systems further supports dominance. Its premium packaging perception also enhances brand value in certain markets.

The Plastic Containers segment is expected to grow the fastest at a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for lightweight, cost-effective, and flexible packaging solutions. These containers are widely used in cosmetics and pharmaceutical applications. They offer ease of handling, portability, and reduced transportation costs. Growth in retail-ready packaging formats is further boosting adoption. Expansion of e-commerce distribution channels is supporting demand for consumer-friendly packaging. Technological advancements in food-grade plastics are improving safety and sustainability.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct and indirect sales. The Direct Sales segment dominated the market with a 67.4% share in 2025, driven by strong procurement relationships between cocoa butter manufacturers and large-scale buyers such as chocolate producers, cosmetic companies, and pharmaceutical firms. Direct sourcing ensures better price negotiation, quality consistency, and supply chain reliability. It is widely preferred for bulk industrial transactions. Long-term contracts and strategic partnerships further strengthen this segment. It also enables better traceability and quality control across supply chains. The dominance is reinforced by globalized manufacturing networks.

The Indirect Sales segment is expected to grow the fastest at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand from small and medium-sized enterprises and expanding retail and online distribution networks. Distributors and wholesalers play a key role in reaching fragmented markets. Growth in e-commerce platforms for cosmetic and food ingredients is further supporting expansion. Indirect channels offer flexibility, lower entry barriers, and wider geographic reach. Rising demand from emerging economies is boosting distributor-led supply chains. Increasing product availability through specialty ingredient retailers is also accelerating growth.

Which Region Holds the Largest Share of the Cocoa Butter Market?

North America dominated the Cocoa Butter Market with the largest revenue share of 35.08% in 2025, supported by strong demand from premium chocolate manufacturers, well-established cosmetics and personal care industries, and high consumption of processed and functional foods. The region also benefits from advanced food processing capabilities, strong presence of global confectionery and skincare brands, and rising preference for clean-label and organic ingredients. Increasing use of cocoa butter in luxury skincare formulations and premium chocolate products continues to strengthen North America’s leadership position in the global market.

U.S. Cocoa Butter Market Insight

The U.S. cocoa butter market is witnessing strong growth due to rising demand for premium chocolate products, expanding clean-label and organic food trends, and increasing consumption of natural skincare and cosmetic formulations. The country’s well-established confectionery and personal care industry, along with strong presence of global brands, is driving large-scale cocoa butter utilization across food, pharmaceutical, and cosmetics applications. In addition, growing consumer preference for plant-based and chemical-free ingredients is accelerating adoption across premium product categories.

Europe Cocoa Butter Market Insight

The Europe cocoa butter market remains a major contributor to global revenue, driven by strong chocolate consumption culture, advanced food processing industries, and high demand for natural and organic ingredients. The widespread use of cocoa butter in premium confectionery, luxury cosmetics, and pharmaceutical applications is supporting regional growth. Increasing investments in sustainable sourcing practices, coupled with strict quality and environmental regulations, continue to enhance market expansion across Europe.

U.K. Cocoa Butter Market Insight

The U.K. cocoa butter market is experiencing steady growth, supported by rising demand for premium chocolates, expanding cosmetics industry, and increasing consumer preference for natural and ethically sourced ingredients. Growth in artisanal chocolate brands and clean beauty products is contributing to higher cocoa butter consumption. Furthermore, strong retail presence and increasing focus on sustainable supply chains are strengthening the country’s position in the European market.

Germany Cocoa Butter Market Insight

The Germany cocoa butter market is expanding steadily due to strong demand from the confectionery industry, well-developed cosmetics manufacturing sector, and high adoption of organic and sustainable ingredients. German chocolate manufacturers are major consumers of cocoa butter for premium product formulations, while cosmetics companies are increasingly using it in skincare and pharmaceutical applications. Continuous innovation in sustainable sourcing and high-quality production standards is further driving market growth.

Asia-Pacific Cocoa Butter Market Insight

The Asia-Pacific cocoa butter market is expected to witness rapid growth, driven by rising disposable incomes, expanding urban population, and increasing demand for chocolate and premium personal care products. Growing awareness of Western-style confectionery, rising beauty and skincare consumption, and expansion of retail distribution channels are supporting regional market expansion. In addition, increasing investments by global food and cosmetic brands are accelerating cocoa butter adoption across emerging economies.

Japan Cocoa Butter Market Insight

The Japan cocoa butter market is witnessing consistent growth due to strong demand for high-quality confectionery, advanced cosmetics formulations, and premium skincare products. The country’s focus on innovation, precision manufacturing, and luxury consumer goods is driving cocoa butter usage across multiple industries. Moreover, increasing adoption of natural and functional ingredients in food and personal care products is further supporting market expansion.

China Cocoa Butter Market Insight

The China cocoa butter market is growing rapidly, driven by rising chocolate consumption, expanding middle-class population, and increasing demand for premium skincare and cosmetic products. Strong growth in e-commerce channels and expanding domestic confectionery production are boosting cocoa butter utilization. In addition, rising health awareness, rapid urbanization, and increasing adoption of Western dietary and beauty trends are positioning China as one of the fastest-growing markets globally.

Which are the Top Companies in Cocoa Butter Market?

The cocoa butter industry is primarily led by well-established companies, including:

- Blommer Chocolate Company, (U.S.)

- Barry Callebaut AG, (Switzerland)

- Cargill, Incorporated, (U.S.)

- Olam Group Limited, (Singapore)

- Guan Chong Berhad, (Malaysia)

- JB Foods Limited, (Singapore)

- AAK AB, (Sweden)

- Nestlé S.A., (Switzerland)

- The Hershey Company, (U.S.)

- Mars, Incorporated, (U.S.)

- Ferrero International S.A., (Luxembourg)

- Puratos Group, (Belgium)

- Irca S.p.A., (Italy)

- Valrhona, (France)

- Mondelez International, Inc., (U.S.)

- Bunge Global SA, (U.S.)

- Meiji Holdings Co., Ltd., (Japan)

- Fuji Oil Holdings Inc., (Japan)

- CÉMOI Group, (France)

- Ghirardelli Chocolate Company, (U.S.)

What are the Recent Developments in Global Cocoa Butter Market?

- In March 2025, the global cocoa market experienced a significant price surge caused by adverse weather conditions and crop diseases in major producing regions such as Ivory Coast and Ghana, which in turn impacted cocoa butter availability. Leading chocolate manufacturers responded by raising product prices, reformulating recipes, and increasing reliance on cocoa butter alternatives to manage cost pressures. This development highlighted the vulnerability of cocoa butter supply chains to agricultural disruptions and its direct impact on global confectionery pricing strategies

- In June 2024, Blommer Chocolate Company, a major cocoa processor in North America, launched a cocoa butter alternative product line called “Elevate”, aimed at helping confectionery manufacturers manage rising cocoa butter costs driven by global supply shortages. The solution uses alternative plant-based fats while replicating key functional properties of cocoa butter such as texture and stability, reflecting the industry’s growing shift toward cost optimization amid raw material volatility

- In June 2024, Nestlé introduced an innovation that enables the utilization of up to 30% more of the cocoa fruit, including pulp and husk, in chocolate manufacturing processes. This development reduces dependence on traditional cocoa bean extraction, enhances resource efficiency, and supports sustainability goals by minimizing agricultural waste. It also strengthens supply chain resilience at a time when cocoa butter availability is under pressure due to climate-related production constraints

- In October 2023, Barry Callebaut expanded its Forever Chocolate sustainability initiative, focusing on responsible cocoa sourcing, deforestation-free supply chains, and improved farmer livelihoods. The program emphasizes traceability and certification to ensure long-term supply stability of cocoa butter raw materials, while strengthening ethical sourcing standards across global markets. This initiative reflects growing industry-wide commitments to sustainability and supply chain transparency in cocoa-based ingredients

- In May 2021, Mars Incorporated reinforced its long-term sustainable cocoa sourcing strategy by expanding partnerships with cocoa farming communities in West Africa. The initiative focuses on regenerative agriculture practices, farmer income improvement, and supply chain traceability, all of which directly support stable cocoa butter availability for global chocolate manufacturing. This move also strengthens ethical sourcing frameworks and reduces long-term supply risks in the cocoa butter value chain

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Cocoa Butter Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Cocoa Butter Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Cocoa Butter Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.